I had published a short post on this company on BLOG covering background, revenues, margins, capital needs, valuation, etc.

Since a lot of these points are already covered in this thread, I am sharing the valuation section, capital allocation issues and my personal thoughts sections of the above post here in the hope that it useful to members. In case it isn’t, feel free to report the same and get it deleted

VALUATION

PART I: DCF Valuation

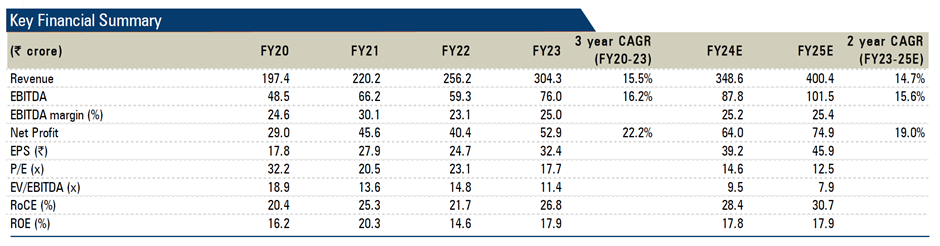

- Lets assume that the company reaches its target of Rs 400 crores turnover by FY25 (on standalone basis). This implies a y-o-y growth of 16% from FY22. Lets also assume that it gets its desired EBIT margin of 21%. Lets also take the company’s words that they do not need any capex until this 400 crores turnover. What to do thereafter?

- I have put my positive thinking cap on and have taken these assumptions for more years. I have assumed that the company continues the aforesaid 16% growth for a total of 5 years (i.e. Until FY27), and thereafter it moderates to around 6% by year 10. This implies that by Year 10 the company will have a revenue of Rs 856 crores. Lets do a sanity check on this revenue projection. The current organized market is around Rs 1200 crores. If this market grows a CAGR of 12% y-o-y for 10 years it will be Rs 3727 crores by then. Thus, at Rs 856 crores, the company will have a marketshare of 23% (current marketshare around 18%). Hence this revenue projection, while optimistic, is not in the improbable territory.

- For the reinvestment needs I have not considered any capex until 400 crores and thereafter projected it at a FAT of 4.25. For the working capital I have assumed a turnover of 2.1 given the high working capital intensity of the business.

- For the terminal value I have retained the high margins of 21% as well as the above FAT & Working Capital turnover and thereby preserved a high ROIC of 22% and taken a perpetual growth rate of 6%.

- Thereafter, I have added back investments, cash book value of land of liberty chemical and other small items

- Lastly, I have used a discount rate of 13%

With these optimistic assumptions, the DCF yields a value of 455/share which is very close to the CMP (around 430). What this means is that we will earn a CAGR virtually equal to the discount rate of 13%. Now, you will note that this result is with fairly positive assumptions built-in

PART II: Multiple Based Valuation:

Lets assume that you do not believe in DCFs and consider them BS. From a multiple perspective, as per screener, the market is giving them a PE of 16 (TTM basis) as of now, which is around its average of 15. It would be fair to say that the market has already considered some growth prospects in this company. Now by FY25, if we expect sales to become Rs 400 crores and EBIT margins to be 20% with a tax rate of 18% (MAT rate applied due to hilly region benefit) we get Rs 65 crores of Profits in March-2025.

Now what multiple to apply for March-2025? If we take a multiple of 15 and divide by the share count we get a result of Rs 602/share i.e. a good CAGR of around 14.5%. However, we expecting things to be perfect. We expect that the company will deliver the promised growth & margins and are also expecting that the market will continue to give a multiple of 15. Do some sensitivity analysis on growth, margins and multiples and check whether if it fits your margin of safety & return expectations. If it does then you can invest at this price too

Some IMPORTANT things to be aware prior to investing in this company:

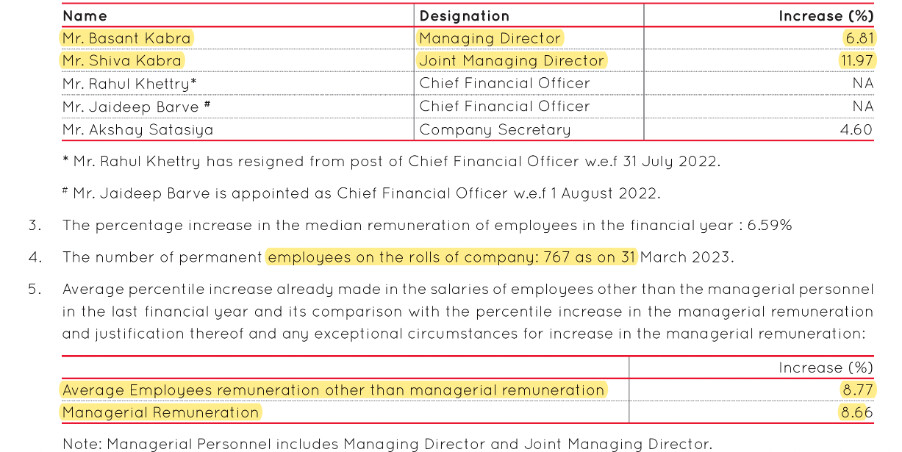

- Commission to directors: In addition to salary, the directors draw a commission. It was Rs 3.50 crores in FY22, Rs 2.60 in FY21 and Rs 1.70 crores in FY17. This could be ignored if it was in isolation. However, there other bigger things below

- Capital allocation history is not great

- Promoters also have a strong fancy to DIRECTLY invest in stocks. In FY22, this amount is Rs 39.31 crores which has increased from Rs 11.96 in FY17. Obviously some portion of this increase is attributable to the increase in value of the investment but still it is a large amount. Moreover such kind of equity investments are being done since the past decade! There is also an investment of Rs 0.5 crores in in Artha ‘Venture’ Fund along with a commitment of another Rs 0.5 crores (shown in contingent liability)

- Real Estate Diversification

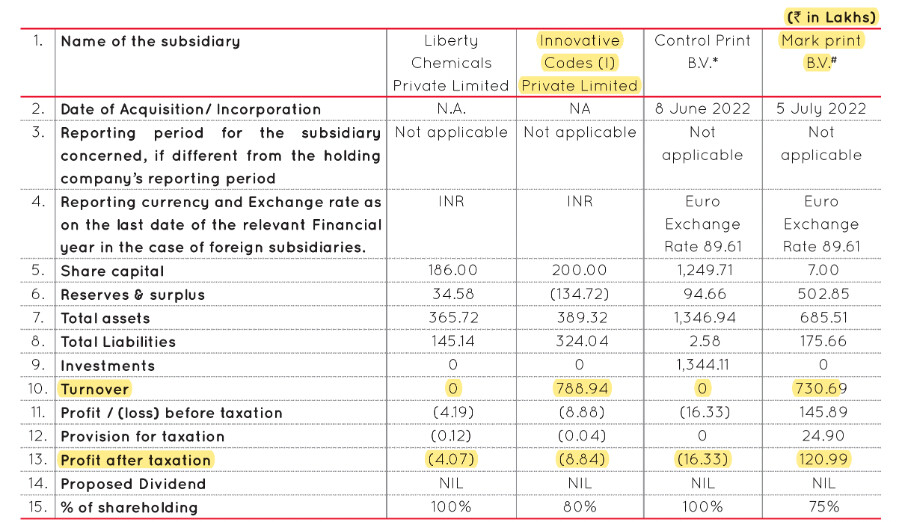

As per FY11 AR, “Your Company has entered into a MOU with M/s. Liberty Chemicals Pvt. Ltd., in the month of August, 2008, towards purchase of its property and a sum of ` 1,35,00,000/- was paid as advance. Subsequently the Company has acquired all the shares of M/s. Liberty Chemicals Pvt. Ltd., in the month of April, 2011 after considering the assets and liabilities of Liberty Chemicals Pvt. Ltd”.

As per FY12 AR, the company invested another Rs 3.70 crore in the above subsidiary by way of rights issue. As stated in the AR “the acquisition would enhance shareholders value since Liberty Chemicals Private Limited owns a plot of land as a valuable asset. Control Print Limited intends to explore diversification in real estate business in future post feasibility study on its plans.” The aforementioned land located in Chandiwali, Mumbai is still with the company. While one cannot put a value to this real estate investment without further details, it is fairly safe to presume that the company will earn a profit (atleast on an absolute basis) on this investment since it was done way back in 2008. Will the profit exceed the time value of money on the investment made? When will the sale/development happen? Will the company distribute the proceeds to shareholders too? We cannot know as of now.

- The Promoters spent Rs 10 crores on the mask division in FY21 (as per Conf Call 26.4.21). However, as stated in various Conf Calls, this division is not central to their operations and they did it “basically in the pandemic period for the society and the CSR activity”.

All said and done the above shows the attitude of the promoter to invest company’s funds in different ventures. While the company has paid dividends, it is not to extent of the FCF generated by the company. However this attitude appears to be changing for the better. In the Conf Call 26.10.22, the company said:

“The board has decided that INR 50 crores is what we’ll keep as cash on books, including whatever investments, cash,bank balance, whatever form of liquid investment,how you’re going to term it, and we have our limits for any acquisition or other opportunities that come…….”

“And whatever more than INR50 crores the board has said that we will largely return back to the shareholder”

If you want to believe in what the management was stated, you can addback 50 crores to the assets. Consequently the Fixed Asset Turnover of the company will reduce and you can project the fixed assets requirements accordingly.

-

The company has a contingent liability payable to Videojet. Pursuant to an appeal made by the Company against an Arbitration Award, the Bombay HC Order had ordered an amount of Rs 2.30 crores to be deposited by the Company (Click here). The company has duly furnished a BG of that amount. I am no legal expert but upon reading the order a liability of Rs 2.30 crores looks likely. However BGs of this sort and that too to a High Court nowadays are not given by banks without corresponding cash/security collateral (sometimes to the tune of 100%) and hence this amount (in all likelihood and IMHO) may not have any impact from an ‘actual cash’ perspective since the company has already furnished the BG to the Court but will impact the P&L statement if & when the company loses the appeal.

-

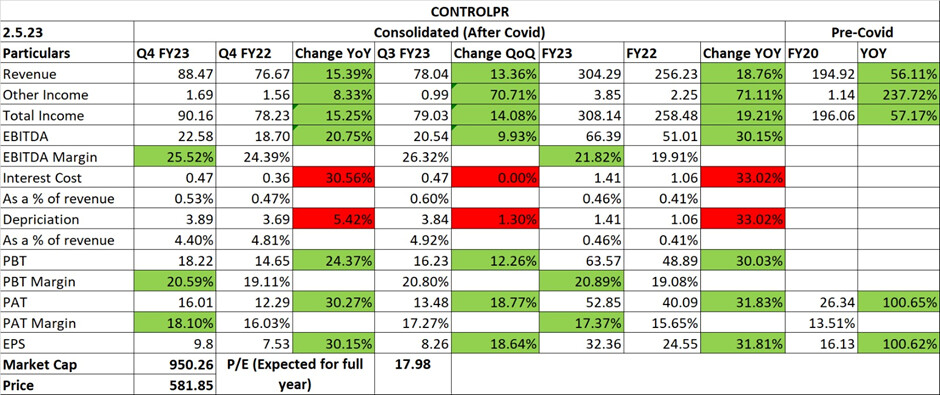

P&L Statement shows inventory write-downs in several years (See: Exceptional items of these respective years). Rs 3.95 crores in FY21, Rs 6.12 crores in FY18, Rs 5.39 crores in FY17 and Rs 0.72 crores in FY15

Are these ‘exceptional’ items really ‘exceptional’? Need to do more digging in inventory (& also receivables) to get some context. I haven’t done it because the valuation (without considering the above) was already was too high for me

Some personal thoughts

I could have ignored most of the negative factors IF the stock price was lower. However, at the current price (around Rs 430/share), its a little difficult for me to ignore them as it cuts MY margin of safety. I believe that when a company does not share the proceeds with shareholders or is not a good capital allocator, our returns are more dependent on the moods of Mr. Market and/or the company meeting or exceeding the growth expectations especially since the margin of safety is not sufficient. Moreover, no investment can be seen in isolation and one must see what returns/risks their alternate investment options offer. Hence I have chosen to pass this one (for now).

On the other hand, lets not forget that the company is showing great sale of printers, has shown good growth in consumables, is showing better margins, is doing the right kind of acquisitions and has made a cap of Rs 50 crores on investments/cash. It could also enjoy a tailwind of higher industrial growth which leads to higher industrial output which in turn leads of higher sale of consumables. Thus, there are quite decent chances that not only the company achieves its revenue target of Rs 400 crores on standalone basis by FY25 but also exceed it. There is also a possibility that the Chandivali land gets sold/developed & gives good profits and/or that is YOUR margin of safety. Maybe the new acquisition done by the company does very well. Maybe Mr. Market continues to give the current multiple & more to the company even in the future. Maybe your margin of safety and return expectations defer from mine.

I have also been overly conservative in such situations in the past and thus it could be that even for this situation my conservatism is (unconsciously) showing up again. Obviously, my views are (and should be!) subject to change based on new data and stock price.

")