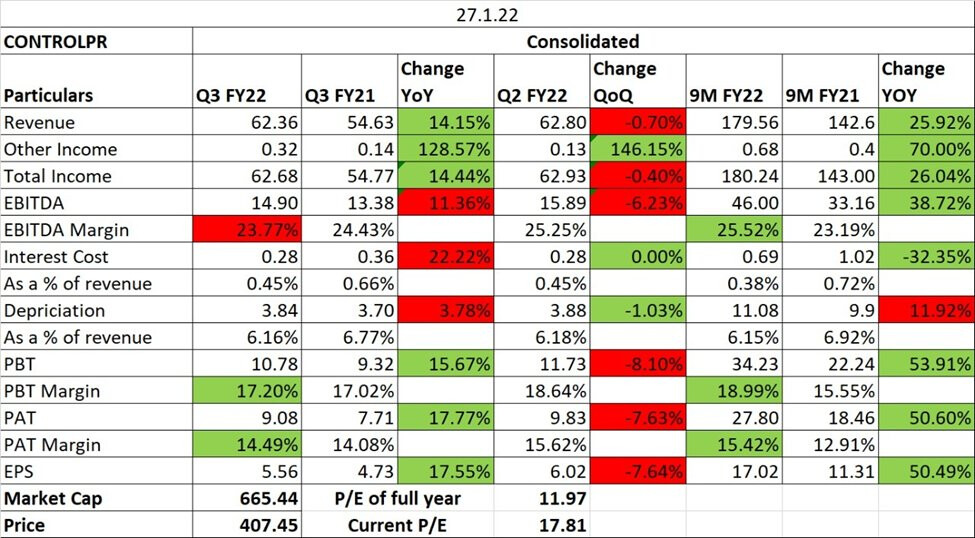

Superb number by companies. Any reasons for the increase in top line?

1 Like

Any thoughts on “Control Print Acquires majority stake (80%) in Innovative Codes (I) PrivateLimited (“ICIPL”) by acquiring 16,00,000 equity shares at the cost of 1,60,00,000 Rs.” ?

2 Likes

I am sharing some of my notes on the company.

While sales growth has been close to 8.65% in the last 5-years, services revenues have grown much faster at 33.45% (from 6.25 cr. in FY16 to 26.45 cr. in FY21). The proportion of high margin business (consumables + spares + services) has largely stayed constant at 80% in the last 5-years. Detailed data below.

| in cr. | FY08 | FY09 | FY10 | FY11 | FY12 | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Income from operations | 38.75 | 37.87 | 46.07 | 57.97 | 66.54 | 79.82 | 91.06 | 112.92 | 134.52 | 147.83 | 173.83 | 174.60 | 194.92 | 203.69 |

| Coding and marking systems | 8.31 | 11.00 | 12.95 | 19.32 | 19.27 | 19.54 | 19.07 | 24.28 | 26.49 | 27.18 | 30.62 | 34.32 | 39.48 | 40.78 |

| Consumables and spares | 30.44 | 26.87 | 31.99 | 36.12 | 43.26 | 55.58 | 67.61 | 84.07 | 105.95 | 105.56 | 128.48 | 123.18 | 133.05 | 136.24 |

| Services | 2.77 | 1.49 | 1.12 | 2.48 | 4.55 | 5.90 | 6.06 | 7.05 | 6.25 | 12.99 | 13.94 | 16.89 | 22.15 | 26.45 |

Exports: This hasn’t shown predictable growth in the recent past, below are the numbers. Sri Lanka operations turned profitable for the first time in FY21, though its still very small (revenues of 1.28 cr. and profits of 0.92 lakhs)

| in cr. | FY08 | FY09 | FY10 | FY11 | FY12 | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Export sales | 0.17 | 0.51 | 0.76 | 0.82 | 1.11 | 1.64 | 2.27 | 2.42 | 2.49 | 2.66 | 5.36 | 3.53 | 3.96 | 5.54 |

Royalty costs: Surprisingly, this hasn’t gone up and has gradually reduced from 4.94% of sales in FY16 to 2.44% in FY21. However, R&D costs have started happening which means they are developing more products in-house which is good. R&D + royalty has largely stayed in the 4-5% range of sales

| in cr. | FY12 | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 |

|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 66.54 | 79.82 | 91.06 | 112.92 | 134.52 | 147.83 | 173.83 | 174.6 | 194.92 | 203.69 |

| Royalty expense | 2.86 | 3.94 | 4.74 | 5.87 | 6.65 | 5.48 | 6.06 | 5.80 | 6.20 | 4.96 |

| R&D expense | - | - | - | - | - | - | - | 4.04 | 3.68 | 2.75 |

| Royalty + R&D | 2.86 | 3.94 | 4.74 | 5.87 | 6.65 | 5.48 | 6.06 | 9.84 | 9.88 | 7.71 |

| Royalty + R&D % of sales | 4.30% | 4.94% | 5.21% | 5.20% | 4.94% | 3.71% | 3.49% | 5.64% | 5.07% | 3.79% |

AR21 notes:

Domestic market size: 1200 – 1500 cr. (Control commands 18.5% market share)

Strategic focus:

- Special focus area would be OEM sales and Key Customer Accounts

- Participation in exhibitions in Tier 2 cities for capturing the last mile user

- Intensified focus on foraying into newer segments such as dairy, FMCG and building materials. Our strategic shift in sales from the traditional regional/ zonal orientation to the new sector/ product category wise targeting yielded good results. The Company has dedicated managers and devoted teams to drive the business verticals with a focus on Dairy, Beverages, Bakery (Biscuits), Frozen Food, Ready to Eat, Pharma, Packaging, Plywood, Lubricants, Carton Coding

Technology segmentation

- Continuous inkjet (largest market share due to high speed + efficiency on any surface + low cost continuous printing)

- Drop-on-demand (DoD)

- Laser coding and marking

- Print and apply labeling

- Thermal inkjet (TIJ): One of the fastest growing

- Thermal transfer overprinting (TTO): One of the fastest growing

New launches over last few years:

- Thermal Inkjet (TIJ)

- Thermal Transfer Overprintin (TTO)

- High Resolution (HiRES)

Miscellaneous:

- Main growth propellant has been increased production in some of the industries where Control Print has a stronghold (Pipes, Cables, Steel, Food, FMCG, Beverages etc.). The Company also witnessed growth in emerging sectors (Dairy, Pharma, Paints and Wood) that has contributed to company’s growth, increasing Penetration and market share.

- Face mask division is mostly for CSR activities

- The Company exports components to KBA Metronic Plant to China and looking at a possibility of exporting mounded components for Printer

- The Company is not manufacturing Empty Ink Cartridges for Thermal Ink Jet Printers. It is very high end Technology involving highly advanced Machinery in electronic and silicon chip availability. Development of the Empty Ink Cartridge, with special added features is outsourced. The new type of cartridges needs development of the Plastic Molding Tools and Number of trails runs of molded components, before concluding the final product. it is lengthy and time consuming process

- 48 contractual employees

- Contributed 2.3 cr. towards CSR (1.52 cr. in excess of required)

Disclosure: Not invested

10 Likes

Here are my notes from today’s concall

FY22Q2

- Confident of maintaining EBITDA margin in the 24-28% range

- Confident of double digit revenue growth, aspire for mid-teen sales growth

- Have gained few competitor accounts in the last year thus gaining market share. Current market share is 19-20% and hope to get to 25% mark in the next 5-years

- Want to get to 300 cr. in the next 2 years and reach 400 cr. in 5-years

- Needed minimum amount of inventory which has been reached and inventory as % of sales will come down going forward

- Recent acquisition of ICIPL (Innovative Code (I) Pvt Ltd.): Total coding & printing industry size is 1500-1600 cr. where the 4 organized players make up 1100–1200 cr. Rest 300-400 cr. is unorganized and the biggest company on unorganized side was Jet inks which ran into some issues during covid and the CEO of Jet Kings quit and started his own business (ICIPL with capital backing of Control Prints) catering to the more price sensitive part of the market. By doing this, Control Prints has started a new brand targeting to that segment which is different from their own network where Control Print couldn’t get into it directly because of the price sensitive nature of the market. ICIPL will lose money until a significant printer base is installed, they are also getting their own bank funding

- Don’t need any major capex for the next 2-2.5 years. Current capacity can support sales of 300 cr.

- Demand for printers is created whenever a new manufacturing line is added as a dedicated printer is attached to each line

- 20% revenues from printer (quantity was 700-750), 2-3% revenues from mask

- Real estate: no real movement on the Chandivali land plot

- Not too much churn in the equity portfolio (super weird that there was discussion on the relative performance of their equity book vs the market returns)

Disclosure: Not invested

15 Likes

Anybody can give some anti thesis pointers for Control Print Ltd other than slow manufacturing growth?

2 Likes

is there some new developments in the company cause i think it is doing pretty fine, but the share price is getting hammered?

1 Like

1 Like

4 Likes

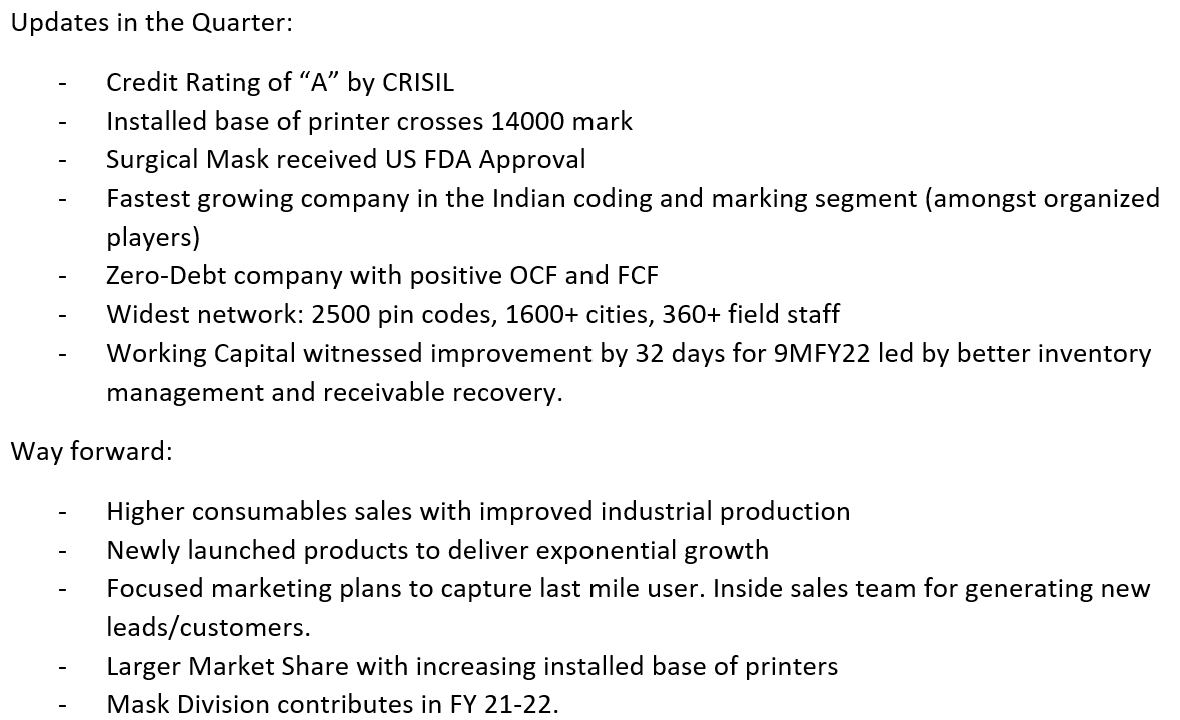

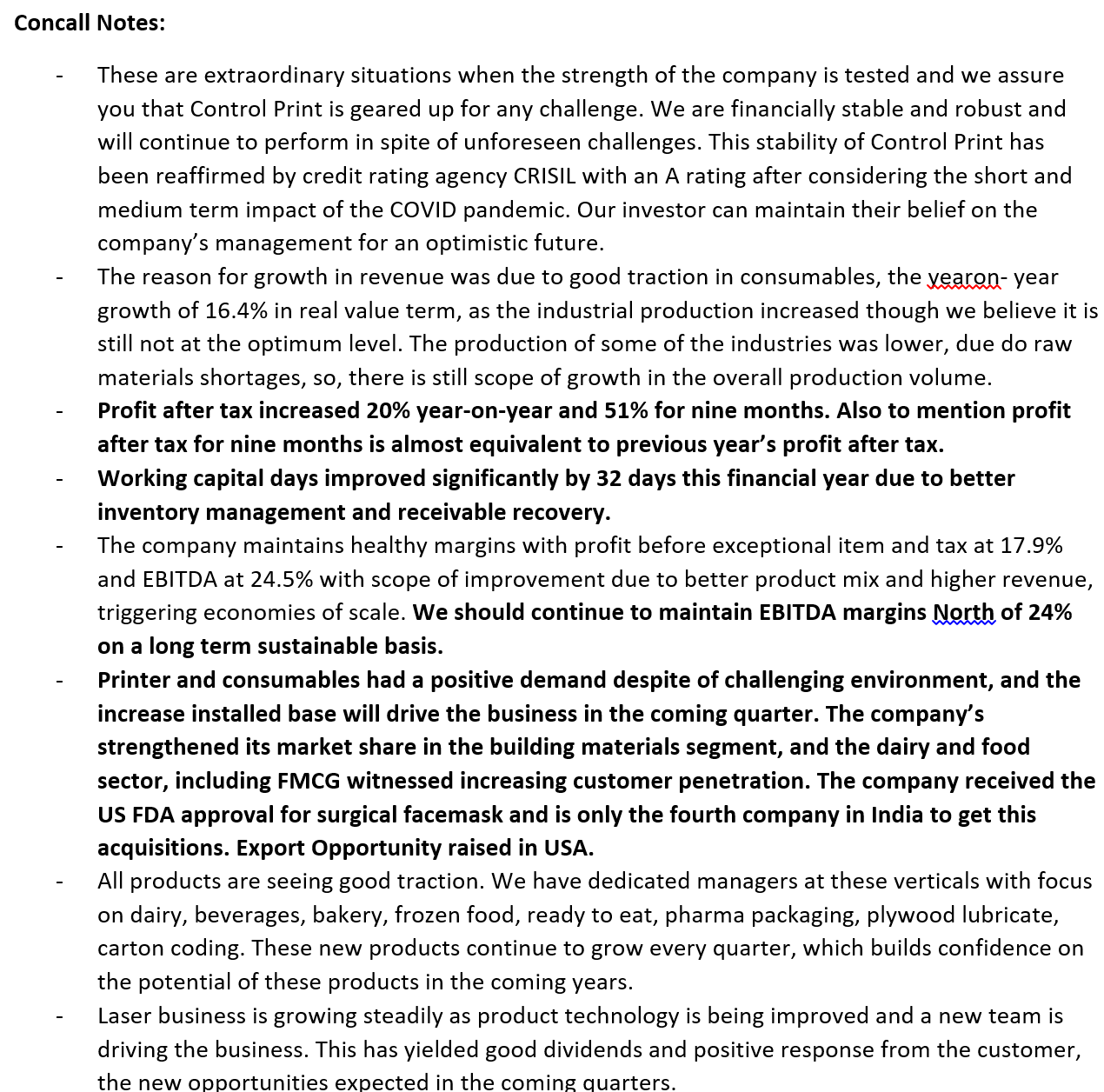

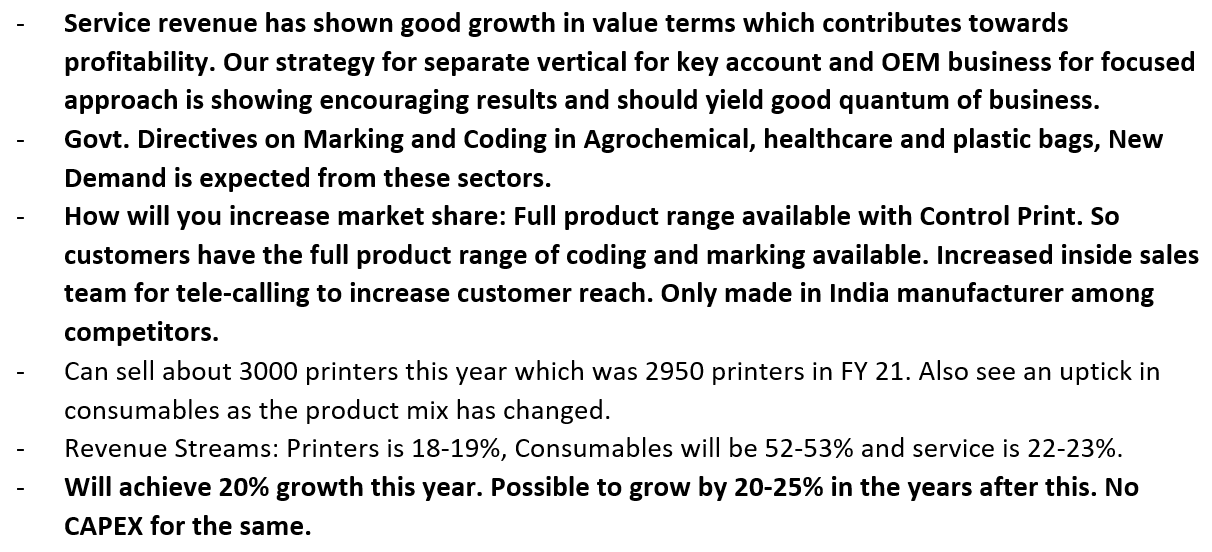

Good set of results from the company, they have maintained 60 cr.+ quarterly revenue runrate and are confident of growing topline by 20%+ in FY22. After that, they are aspiring for 15-20% revenue growth. Here are my notes from the concall.

- Strengthened market share in building material segment and got new customers in dairy foods division

- Got FDA approval for masks division; Currently this division is doing 2-2.5 cr. monthly revenues. Will look at supplying to US customers. Don’t have clear visibility on growth as it is very covid wave specific. Don’t need any further capex for ramping up mask division

- Sold ~2100 printers in 9MFY22, looking to reach 3000 this years

- Have lower market share in packaging side compared to industrial side. Packaging is also bigger in terms of market size than industrial and has a more diverse mix of printers. Slowly gaining market share on packaging side because of new printers launched in the last 3 years which was not company’s specialization before

- On line for 20% sales growth in FY22, after that aspire to grow sales at 15-20%

- Guwahati consumable capacity utilization is 50-55%, capacity was built keep a long term demand in focus

Disclosure: Invested (position size here)

6 Likes

Have they set up a facility to manufacture masks?

And even if they didn’t, why are they putting in capital and resources into an unrelated commoditised business whose time is over?

While the other stuff sounds okay, such capital allocation decisions would only distract management from the core business where the need to beat strong, well-funded competitors.

1 Like

Yes the capacity was already setup to manufacture masks at very minimal investment. In the beginning this was done as a CSR activity, however now they are doing 2-2.5 cr. monthly sales (meaning 25-30 cr. annual nos.). On a 230-240 cr. base, this is already quite significant. However, I will not hold my breath for growth from mask division, its directly a function of covid waves.

About capital allocation, management has been very quite prudent with capex returning a large part of free cash back to shareholders (~50% payout).

About mask being a commoditised business, I am not very sure. They are only the fourth Indian company to get FDA permission to sell masks in US. For context, we have 100+ Indian pharma companies selling drugs, I don’t know which one is more of a commodity.

5 Likes

Pharma products can be both commoditised or niche, not sure about the point of your argument. Some pharma companies have great ROIC while others struggle to even meet the cost of capital.

Masks are pretty much commoditised, with no niche really possible in most cases. Not much point in looking at only Indian suppliers since Chinese dominate.

Also, not sure why you’re looking at just revenues, when ultimately return on capital employed and growth matter.

Growth without value accretion to shareholders is worse than no growth, because management spends time and resources on a low potential business.

Like I said, I like the core business and the many seems capable, but this decision seems hasty. I have a feeling that the mask business won’t even be mentioned by next year.

Again, just an opinion.

3 Likes

Another good set of results from the company, quarterly sales has grown past 70 cr. and company has made inroads into competitor accounts in pharma division. My notes from concall are below.

- Consumable sales for the newer printers (TIJ/TTO) are lower (at 80’000 – 100’000 per printer) as customers are new to this printer and will ramp up gradually. Older (CIJ) printer consumable sales are higher at 1-1.2 lakh

- Sold 3025 printers in FY22, installed base (i.e. active ones) have crossed 15’000

- In this quarter, printer sales ~ 18-19%, consumable ~ 51-52%, services ~ 21-22%

- Not concentrating on mask division as of now, the related assets should be depreciated by end of FY23

- Have a backlog of CIJ printer orders due to chip shortage (could have sold 75-100 printers more if not for the chip shortage)

- Current inventory situation is at normalized level (65-70 cr.)

- Won competitor account in pharma segment

- Do not undercut competitors on price, compete on services

- Utilization in consumable segment is 50-55%

Disclosure: Invested (position size here, sold few shares in last-30 days)

6 Likes

AR22 notes

Domestic market share: 18.5% market share

Business strategic focus:

- Dedicated managers in sectors (Dairy, Beverages, Bakery (Biscuits), Frozen Food, Ready to Eat, Pharma, Packaging, Plywood, Lubricants, Carton Coding)

- Increased conversion strike rate by growing sales staff for tele communicating with customers

Technology

- Continuous inkjet (largest market share due to high speed + efficiency on any surface + low cost continuous printing)

- Drop-on-demand (DoD)

- Ribbon-based technology

- CO2 technology

- Hot roll coders

- Laser coding and marking

- Thermal inkjet (TIJ)

- Thermal transfer overprinting (TTO)

- Developed 230 ml. Maxi Cartridge. This is Unique Model with 4x ink capacity and company has applied for IP Rights

- Implemented CRM software to centralize, optimize and streamline engagement with customers

Miscellaneous:

- Small Character Printer (SCP): Growth was attributable to better output in sectors like dairy, healthcare, food, cable and wire, agrochemicals, pharma, paint and wood

- Laser: Gradually expanding with improvement of product technology and a new team

- Large Character Printer (LCP): Grew with modest improvement in cement & sugar sectors. With introduction of new applications, company is shifting attention to non- Cement industry

- Original Equipment Manufacturer (OEM): Approach for a separate vertical for major accounts and a more focused strategy is yielding promising results

- Impressive growth rates were registered by Thermal Inkjet Printer (TIJ), High Resolution Printer (HiRes) and the thermal transfer overprinter (TTO) divisions

- Aspire to grow revenues to 400 cr. in 3 years, should grow sales in double digits in FY23 while maintaining 24%+ EBITDA margins

- The newer products allow to print on any surface ensuring continuous operation

- Invested in Innovative Codes (Chennai based) to augment offerings in price sensitive segments. Revenues: 2.18 cr., PAT: (-0.66 cr.)

- Industry is witnessing shift towards coding and marking solutions which enables high-volume printing at high speeds (like continuous inkjet)

- 300+ sales and service field workers spread throughout 9 branch offices in India and Sri Lanka

- Strengthening in-house software development team to create comprehensive solutions to meet the customer needs

- In building materials section, Company increased market share. In dairy and food sectors, Company saw increased customer engagement

- Control Prints became the fourth Indian company to receive US FDA approval for surgical facemasks

- In view of economic and political uncertainty in Sri Lanka, company has decided to wind-up the Sri Lanka operation

- Export: Sri lanka, Bangladesh, Nepal, Bhutan, Kenya, Italy, Tanzania, Germany. Company has exported components used in Printer Manufacturing to its Technology Partners KBA-Metronic in Germany. Company has also started exporting components to KBA Metronic Plant in China

- 62 contractual employees (vs 48 in FY21)

- Contributed 1.18 cr. towards CSR (0.75 cr. in excess of required)

Disclosure: Invested (position size here, no transactions in last-30 days)

8 Likes

New to the company. Just wanted to know on how do you all feel the longevity of the business in terms of growth. And is the management walking the talk? coz I saw they mentioned to achieve 400cr of revenues but they did ~250-300 I guess…

(I might be completely wrong as well. just want to see other perspective.)

2 Likes

Control Print reported highest ever quarterly sales in last quater with 50%+ contribution from consumables (high gross margins); reported improvement in working capital cycle; future growth drivers is increased inroads into packing industry; capacity utilization is about 50%; I believe it is reasonably valued at PE of 20. Disclosure Invested.

4 Likes

Its a very sticky business with limited profit pool (therefore limited competition), and is a very good proxy to industrial growth. The delta in terms of growth in this sector is low as most printing is because of regulatory requirements and each competitor is quite good. This means that once a factory installs a printer on a production line, it will not change the supplier unless something goes very wrong. So, gaining competitor accounts is not easy and you need to have newer lines to penetrate into the customer.

About guidance, management didn’t guide 400 cr. in FY22 but by FY25. Growth wise, they have executed very well gaining accounts in newer sectors where they were not present before. Also, they are doing these small acquisitions (like Innovative Codes last year, Markprint recently) to increase potential market size. Additionally, company is investing in software vertical as they want to be a complete service provider (e.g. in pharma division, they have come up with QR code that tracks production batches which is implemently directly by Control Print instead of the pharma company). So, I feel management is trying very hard to unlock new growth avenues.

If you have any specific question, please feel free to ask. Hope this helps ![]()

Disclosure: Invested (position size here, no transactions in last-30 days)

11 Likes