Yeah Results are good as per me too. QoQ is something folks do look at thus mentioned the reason for some flattishness sequentially. Otherwise I also see on annual basis.

1 Like

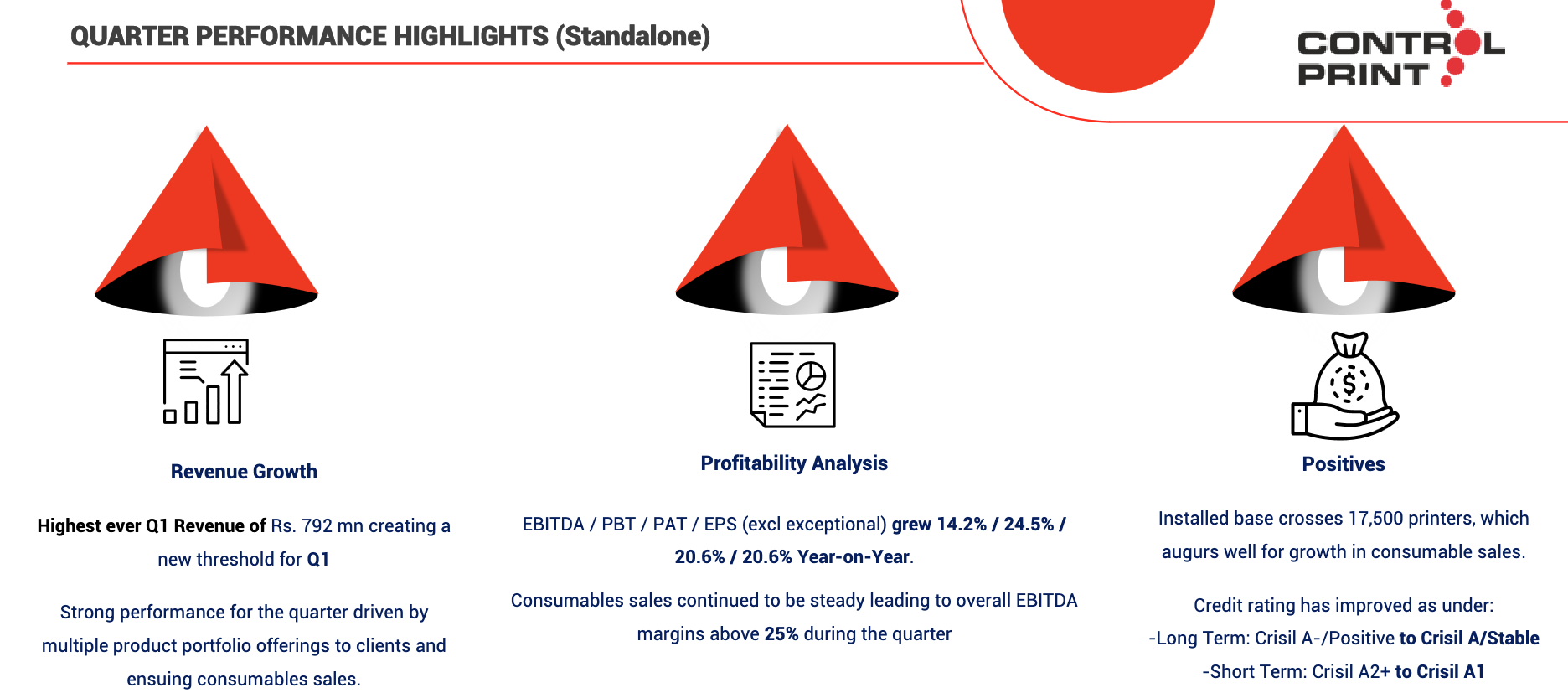

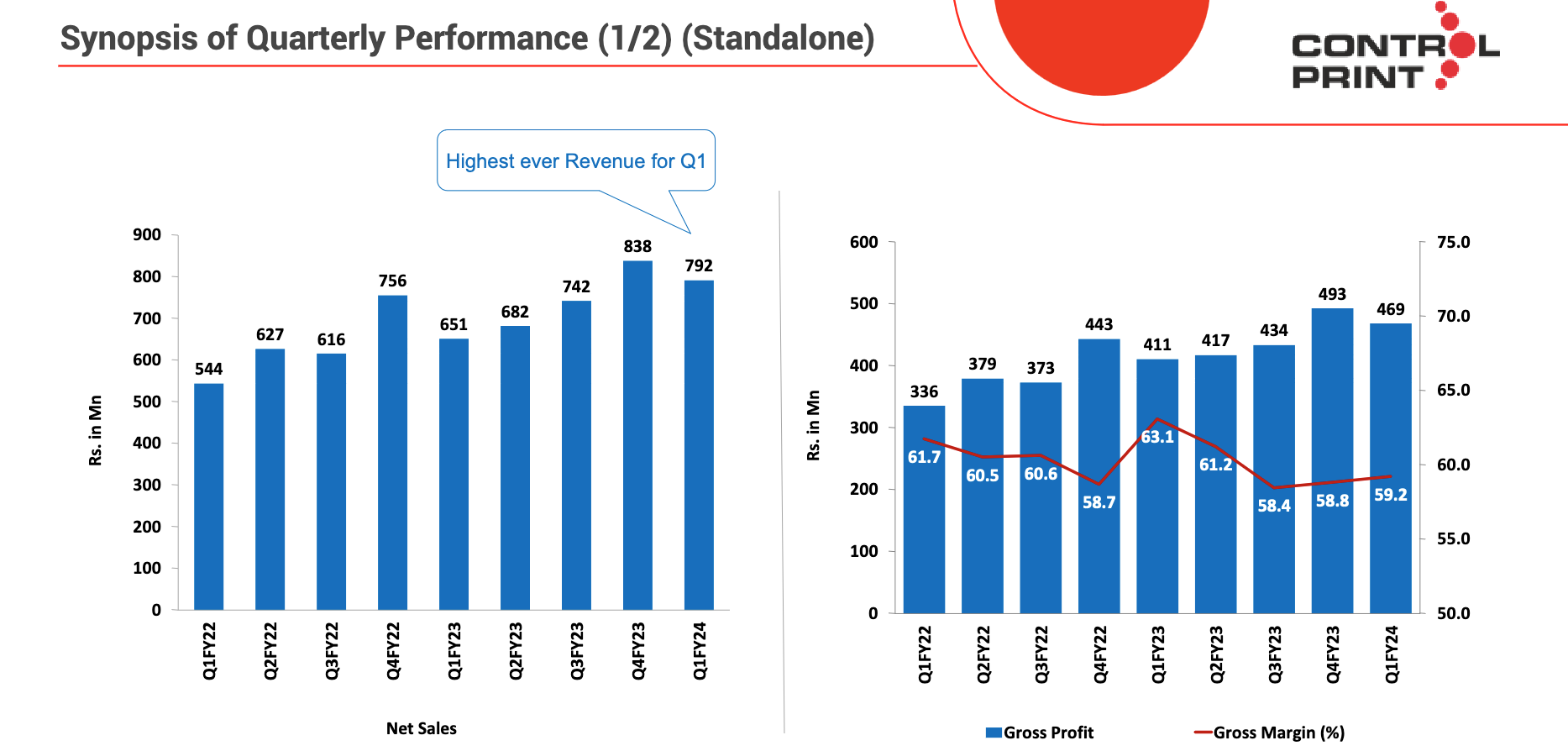

Another good quarter for the company, with 26% sales growth and 21% EPS growth. Growth was largely driven largely by rampup in consumable sales. The recent enforcement of barcodes on top 300 drugs is a material positive for their track & trace division. Concall notes below

FY24Q1

- Printer base increased to 17500+ (sold 650 printers in Q1 vs 750 in Q1FY23). Lower sales was due to some technology problems

- Revenue breakup: printers (17%), consumables (63%), spare parts (7%), service (13%)

- Markprint quarterly revenues was 2.35 cr.

- A large part of coding and printing market is driven by regulations. For e.g. company will benefit due to enforcement of new regulation of barcode for top 300 medicines

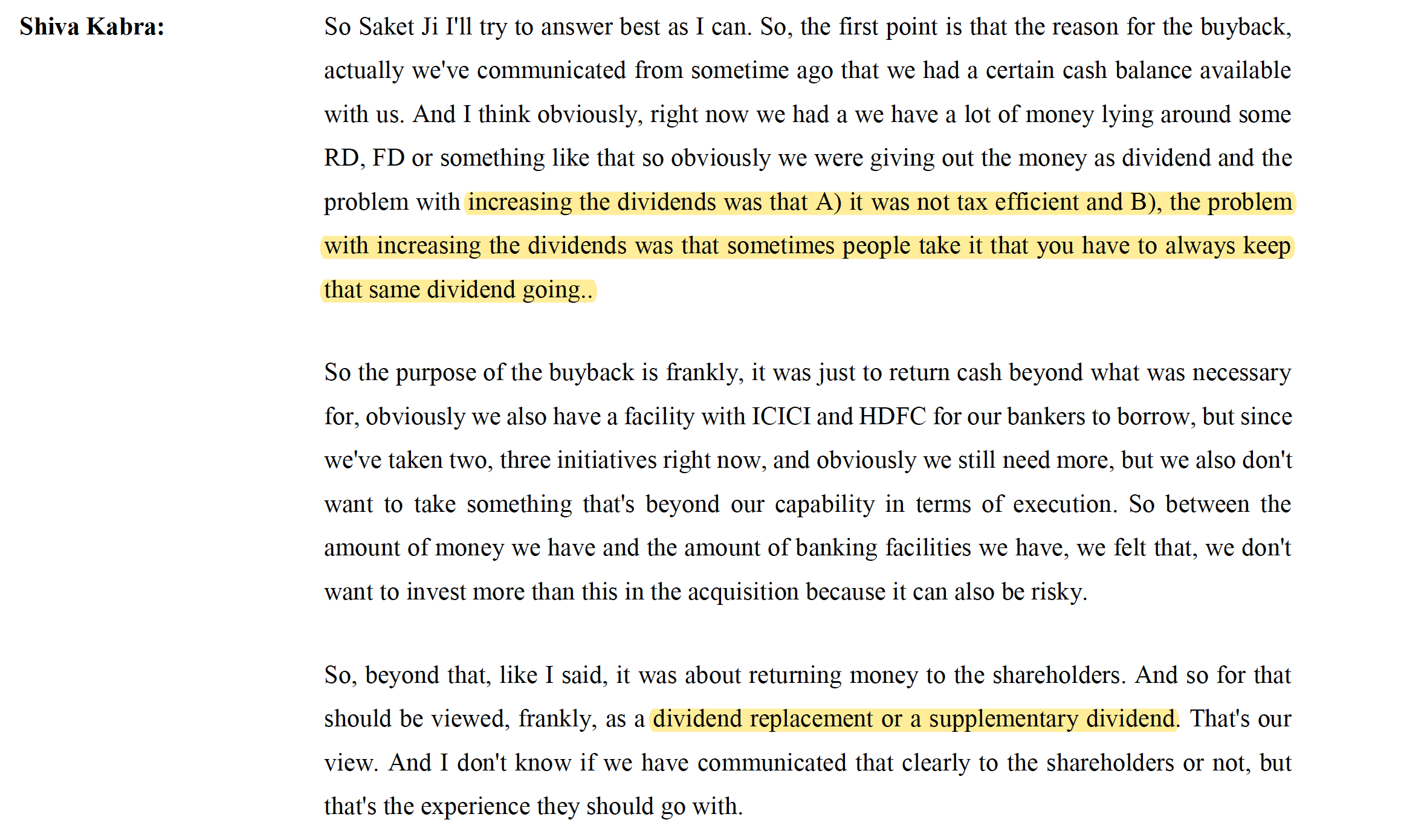

- Buyback should be seen as a special dividend given in a more tax efficient manner

Disclosure: Invested (sold shares in last-30 days)

Didn’t buyback, I have turned into a slow seller, I try to sell in tranches over a few months.

5 Likes

Hi Harsh,

Thanks for summarising the con call. I wasn’t able to attend so waiting for the transcripts and audio recording.

What are your views on the promoters deciding to participate in the buyback?

I didn’t expect them to participate. I would have thought that

-

They would use the buyback to increase their shareholding percentage.

-

Considering their promising future outlook and immediate FY25 standalone sales targets, the share price definitely has scope to go higher than the buyback price.

How would you evaluate the management on this event now? Were there any questions asked in the concall on this topic?

Disclosure: Invested and contemplating whether to participate in the buyback due to the management’s decision to participate

4 Likes

Buyback should be seen as a more tax efficient way to distribute cash, basically a replacement to special dividend. If they had instead declared a special dividend, it would have also gone to promoters. Then I dont see how a promoter participating in a buyback impacts future prospects of a company.

5 Likes

Thank you for sharing your perspective. I have the following thoughts

-

Promoters participating in the buy back means that they are selling their shares not in the open market, but at a predetermined price, although their stake in the company wouldn’t be reduced.

-

The buy back price is currently at around a 13% premium to the current price, definitely there is scope for the price to go higher than now or in the future, so there isn’t much benefit that they would get on selling their shares.

-

Them participating might mean that the entitlement ratio for other shareholders tendering shares would now be lesser.

-

I’m not very clear on this final point, so apologies for my misinformation. Won’t the buy back attract capital gains tax for the selling shareholders?

While yes, there is no issues with the promoters participating in the buy back and it’s a very small % of shares that they would be tendering, in an ideal world, I was hoping that they would have seen this as a way to increase their shareholding in the company, and believe that they could gain more by the share price moving higher in the long run.

2 Likes

Buyback tax is paid by co (~23% including CESS) and is tax free in hands of shareholders. Dividends are taxed at normal tax rate for investors. Most large investors (including promoters) end up paying 40%+ on dividends, thats why a lot of companies now opt for buybacks as it has become a more tax efficient way of returning cash.

Investors’ contribution in building the business has been an absolute zero. Promoters are entitled to bearing the fruit of their own work, and please keep in mind promoters are the largest shareholders. Indian laws are anyway very favorable for minority shareholders, we should try to keep our expecations at an appropriate level.

13 Likes

Company continued reporting good growth, with sales growing by 21% and EPS by 26%. I continue to be surprised how they are sustaining these growth rates, when the industry is growing at 10-12%. Concall notes below

FY24Q2 & CNBC

- Printer base increased to 18,000+ (sold 705 printers in Q2 vs 675 in Q2FY23)

- Since last year, have focused more on larger corporates who give higher business per printer. These entities contribute ~70% of current revenues. Due to this shift in focus, number of printers sold in FY24 might be lower

- Market share has increased to 19% (vs 18.5%)

- Revenue breakup : printers (15%), consumables (62%), spare parts (7%), service (14%)

- Consumable capacity utilization is 60-65%, but its pretty easy to debottleneck these. Don’t want to go beyond 75% utilization

- Industrials: 65%, packaging: 35% (peers are 35% industrials and 65% packaging)

- Pharma track and trace: have got some of the top 300 brands, but they don’t have first mover advantage here. One production line can generate revenues of 25-45 lakhs

- Hoping to see similar growth in H2FY24 if current business trajectory continues

- Won’t be looking at much capex, might go for inorganic expansion

- 1750-1800 cr. was industry sales in FY23 (big 4 was 1350-1400 cr.)

- Price increase has been successfully passed on the customers

- Tax: Guwahati lower tax benefit will go away in May 2025, FY26 will go to normal corporate tax

Disclosure: Invested (sold shares in last-30 days)

12 Likes

At what level you bought? Currently, seems overvalued by a lot.

1 Like

Marcellus might be looking to invest. Positive for the company!

4 Likes

Control Print: A Monopoly in India

In October of 2021, I was looking at different monopoly/duopoly stocks. Among them were certain common names like IRCTC, IEX, CDSL, BSE, CAMS, etc. which everyone would have heard about and would be investing in them. But I found a new name “Control Print Ltd.”

Control Print Ltd is involved in development, research, manufacturing, and marketing of printing machines, spare parts, consumables (fluids) and associated services. The sector they are present in is Coding and Marking Solutions. Their product portfolio involves Continuous InkJet, Thermal Inkjet, High Resolution, Large Character, Thermal Transfer, Laser Printer, Hot Roll Coder & their Consumables. The company is the only ‘Make in India’ company & is in the top four players in India commanding nearly 19% market share of the 1800-2000 cr. coding and marking solutions Indian market. Market share increased from 18.5% to 19% in 6 months. This will help in increasing consumables sales. Market share breakdown: 65% industrial, 35% packaging.

Company continues to witness improvement / market leadership in Building Products segment such as plywood, cement, laminates, pipes, cables, etc. Dairy, Chemical and Pharmaceutical industries are witnessing strong traction.

The price in Nov, 2021 for the stock was around Rs. 300 with a P/E of only 15. The valuation seemed reasonable given the company’s status and sector. It is a leader in the sector. I started investing in the stock around the same price. I was convinced with the sector as well as the business model.

Mainly, their revenue generation was from selling the printers and their consumables like ink. The more the printer base, the more they would be able to sell the consumables. In October, 2021 they had an installed base of 13000+ printers which increased to 18000+ in October, 2023. In FY23, Printers generated 13% of the revenue, Consumables and Spares generated 69% of the revenue and Services generated 14% of the revenue. They have very strong distribution network as well with strong field staff for sales. They are planning on increasing the field staff to cover more cities in India.

Today the price of the stock is around Rs. 950 with a P/E of 26.7. This valuation still seems reasonable for a high growth company. The company has given 20-25% revenue growth every year since 2021 and 30-35% PAT growth. The promoters have also recently bought stake from 51.78% in June, 2023 to 52.68% in September, 2023.

I still think that this company has the ability & potential to grow further and gain more market share in the long term which will eventually be factored in to the price of the stock. At current prices, I wouldn’t recommend buying the stock as markets are at All-Time-High but it is definitely a great stock to keep in the portfolio.

Let me know what you think of the stock in the comments!!!

Happy Investing!!!

12 Likes

I still regret that I couldn’t add it more when it was 680. It is at only 2% of my PF currently.

4 Likes

@Rj_Arora same here! Its in strong uptrend technically as well. I am looking to average up around 930 (current higher low)

3 Likes

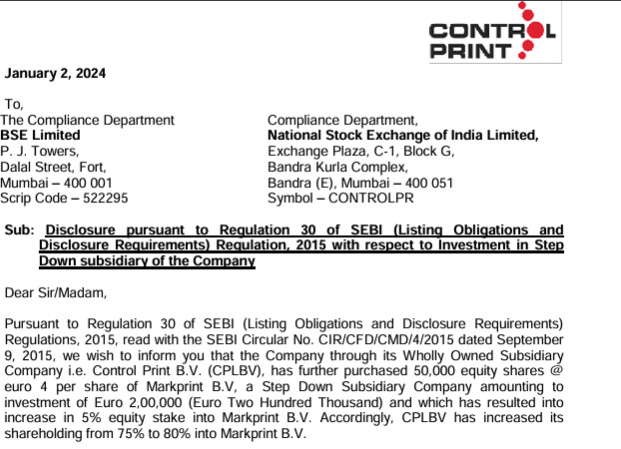

Control Print stake 5% up Markprint BV

4 Likes

Results weren’t great but this drop in share price seems like an overreaction. What does the community think?

1 Like

I am adding it on dips with such a drop.

Disclosure - Invested and maybe baised

2 Likes

Thanks, Lajja. This is really helpful. One of basic quick parameter I have seen over years being EPS and that’s increasing

1 Like

There are 4 key growth drivers apart from the core printer business if they can make any one of these in large scale that’s a huge positive.

- Track and trace as SAAS

- Mark print BV - digital printing will lead to more sales in consumables

- Vshapes packaging as of now they say only pharmaceutical players can afford this due to the cost constraints and they are exploring ways to reduce manufacturing cost. In the lastest concall they said this is a very complex material to manufacture so it’s not easy it will take its own time.

- Exports is on radar of course it will take sometime or years to materialize but the fact that it is on the cards is interesting.

I added more at 941 ![]()

5 Likes

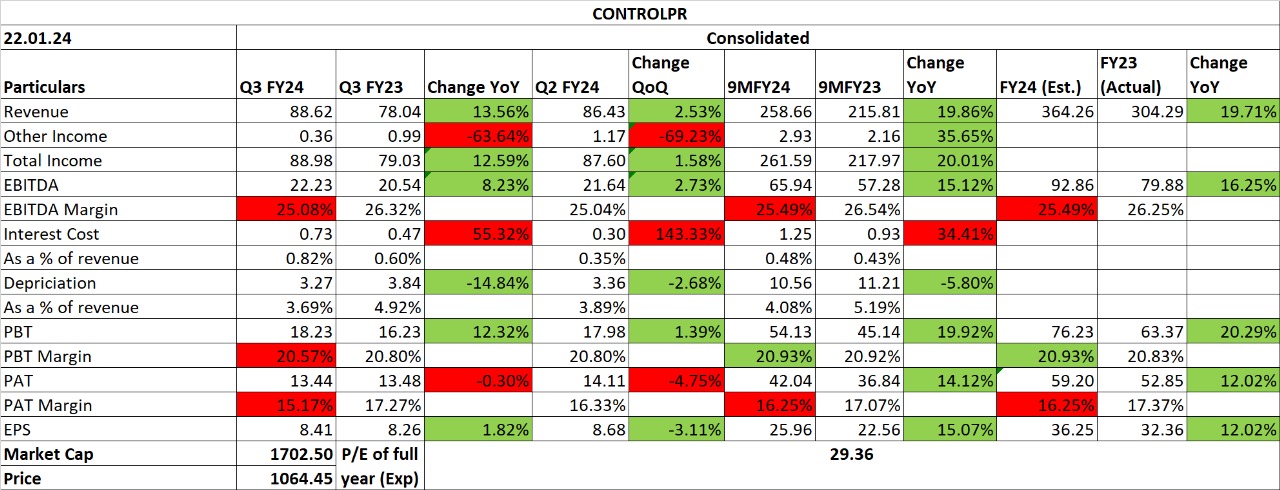

Growth was slower this quarter, printer sales have come down as they are prioritizing customers who can give higher consumable business. Concall notes below

FY24Q3

- Printer base of 18,000+ (sold 630 printers in Q3 vs 814 in Q3FY23). Have been more selective about their customers, preferring those who give higher consumable business

- Main focus is on increasing sales, margins can fluctuate depending on SG&A expenses. Gross margins have been maintained in a range

- Market is very positive currently

- Revenue breakup: printers (16%), consumables (62%), spare parts (7%), service (14%)

- V-shapes: looking to reduce costing on a per sachet basis. Currently only pharma sector can afford this

- Life of a printer is 10-12 years

Disclosure: Invested (sold shares in last-30 days)

6 Likes