Quoting from one of the best threads in FY22, @sahil_vi’s write up on platform companies,

Let’s use the framework set up in that discussion to talk about PDS Multinational.

Business Model and Scalability

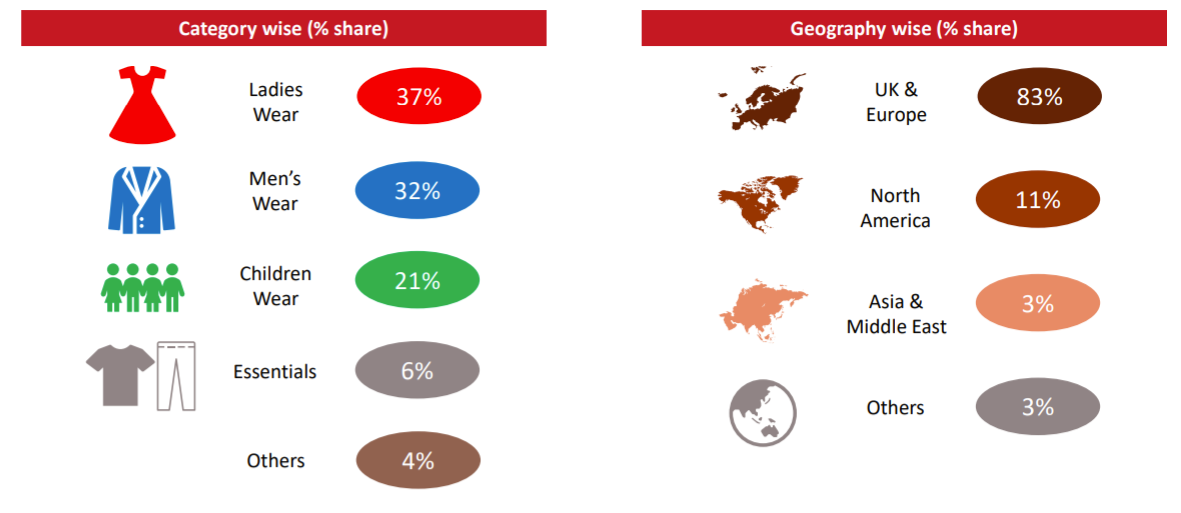

PDS is a platform which curates the supply chain for multinational companies. As a brand, where do you want your fabrics from? Are you looking for a design team to be onshore or offshore? Where would you like your manufacturing facilities and warehouses to be located?

(DRHP, 2014)

PDS has spent the last decade expanding their network, and becoming an economy of scale:

The first thing that should stand out while reading this paragraph is that their clients include Walmart, Primark, Sainsbury’s and Tesco. These brands are known for selling clothes at the absolute bottom price range. If these people come to PDS, PDS must run an incredibly tight ship, and is a cost setter. Indeed, even Amazon is a customer.

If we were to assign a score to the scalability of the platform, it depends on two factors:

-

If PDS is connecting brands with manufacturers, there is a huge potential for scaling as it entirely depends on PDS’ distribution network, and is not limited by physical assets or capacities.

-

The second driver of scale is the number of repeat customers PDS has. If new business comes at the cost of people switching to a different sourcing company, PDS is on a treadmill. Crucially, 98% of PDS’ business is from existing customers, up from 89% in FY15.

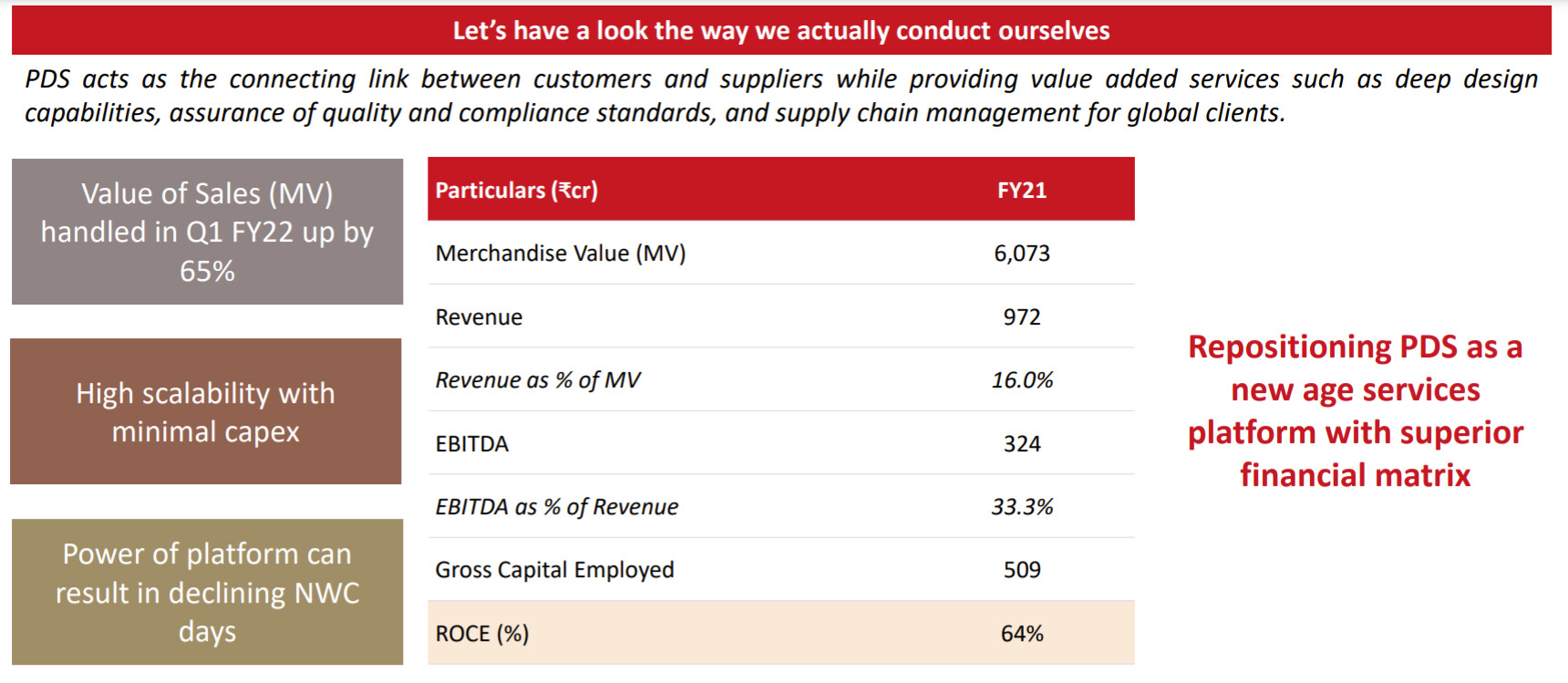

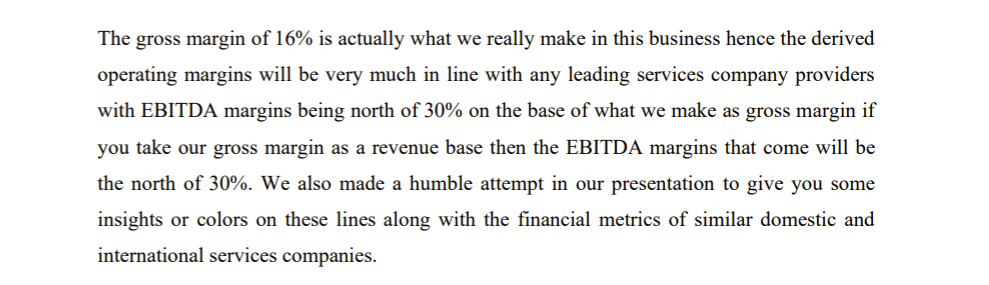

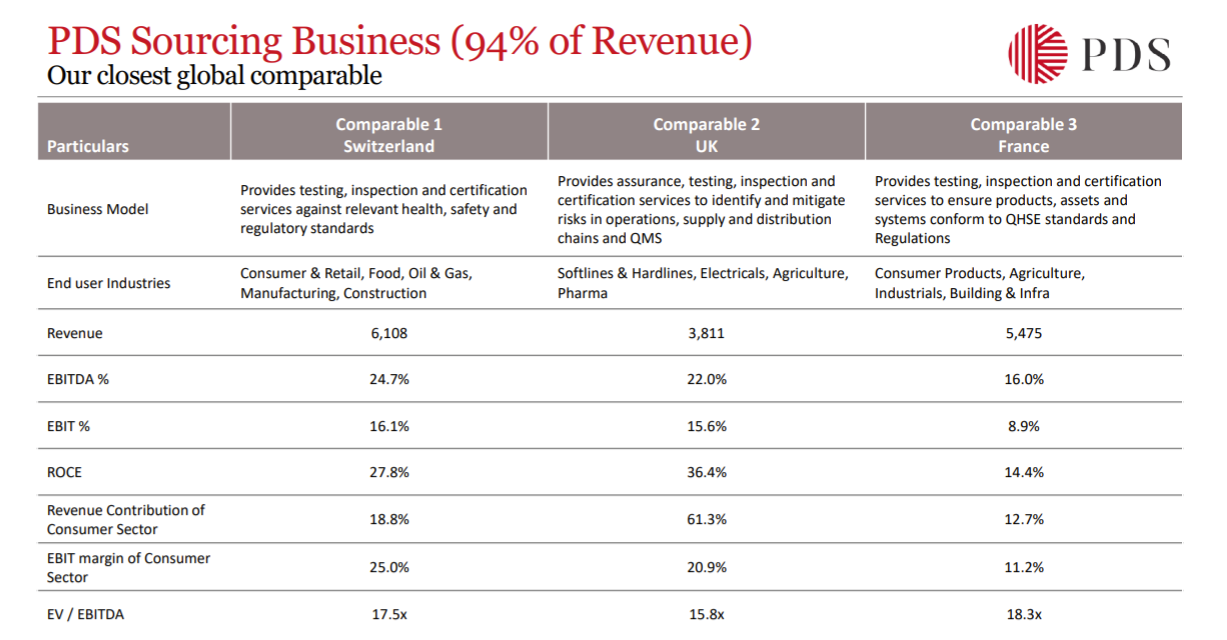

This sourcing business takes up ~95% of their revenue. At this point, we should expect that anyone who sells to Amazon and Wal-mart won’t be a high margin business, and we would be right.

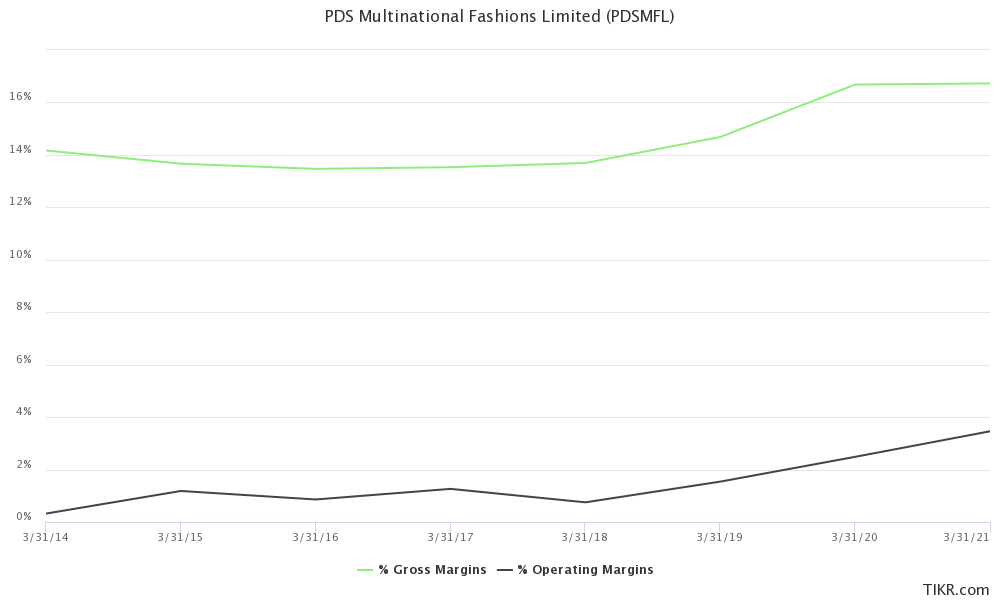

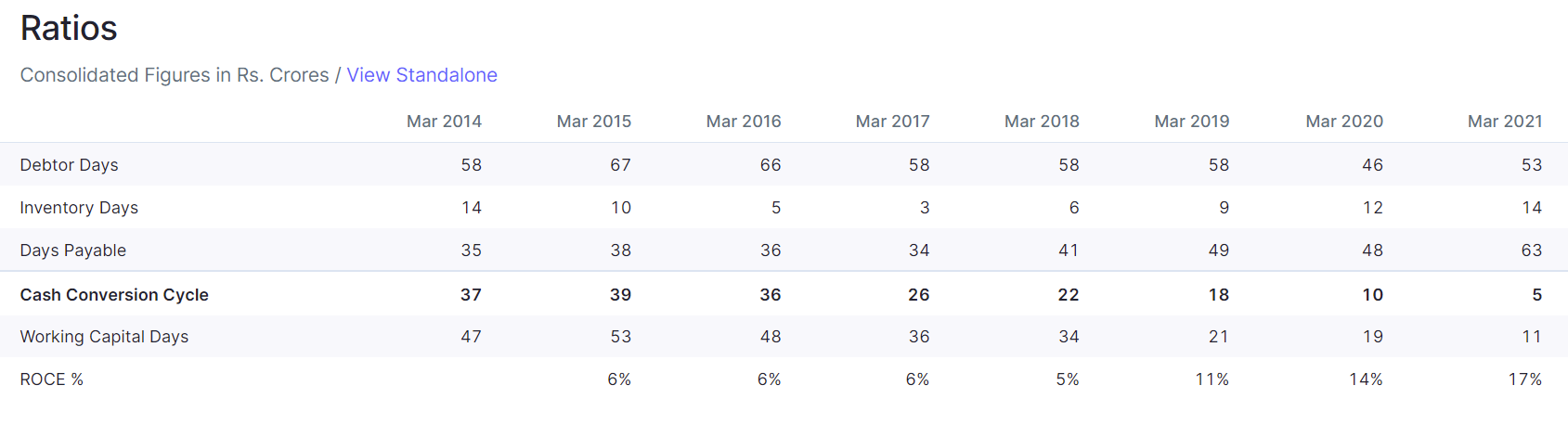

However, we note how both gross margins and operating margins have steadily been improving over the years. There are two important points to consider:

- There is more to the margin profile than meets the eye.

- Margin profile and return ratios are going to look much better from FY23.

1. Management’s Take On Margins

While their topline is 6000 Cr., the management looks at the gross margins as the revenue base. The 6,000 Cr. is the mechandise value of the goods they serve on the platform.

2. Margin Profile and Return Ratios in FY23

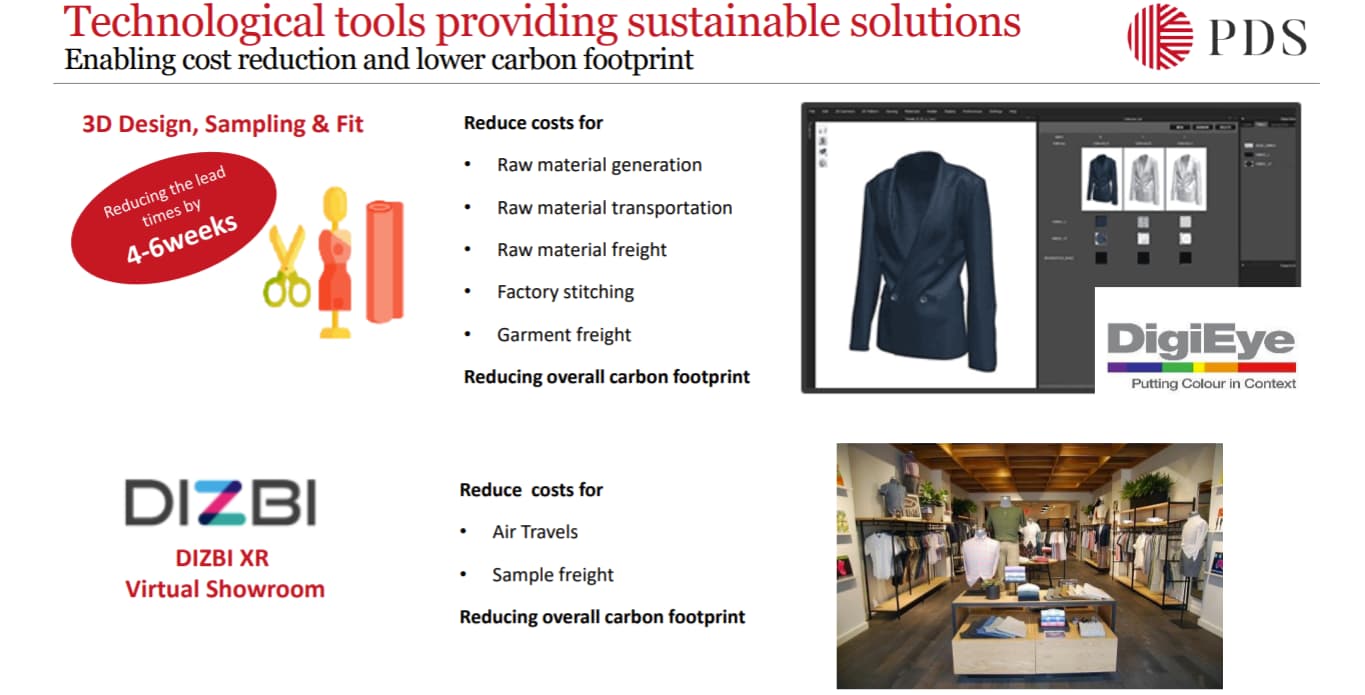

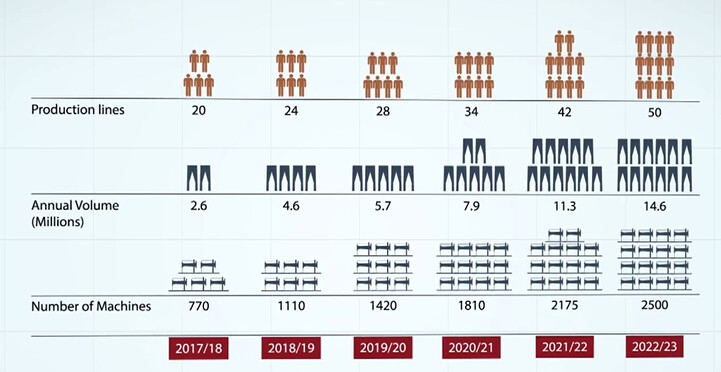

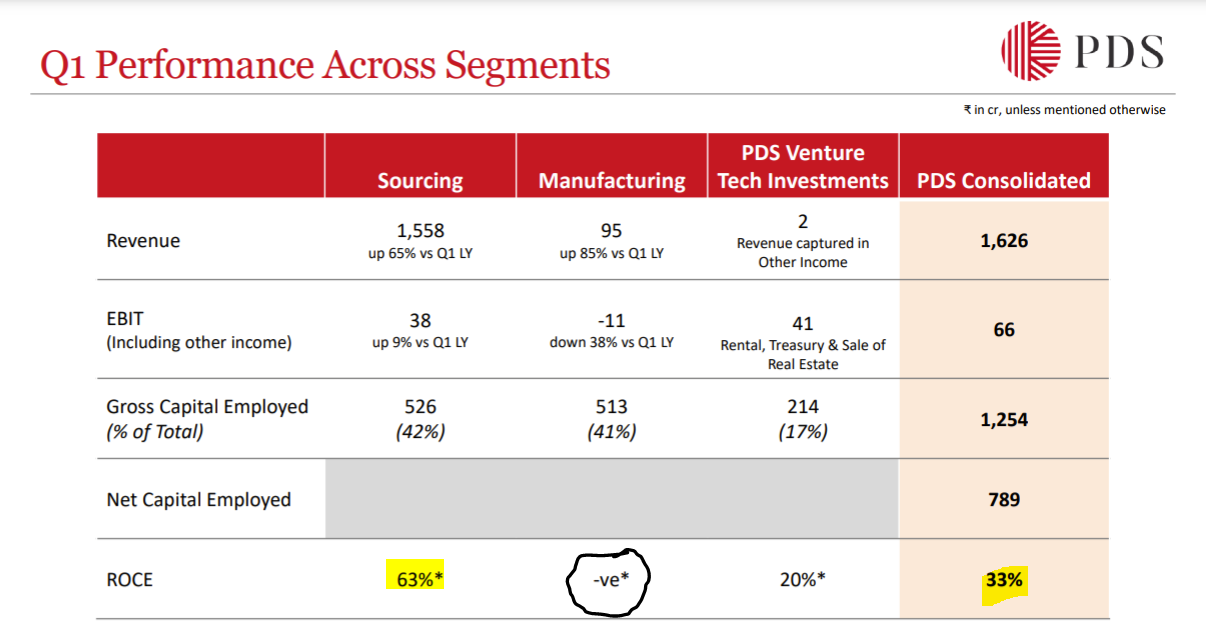

PDS has slowly started to fulfil some of the manufacturing contracts in house, padding the margin profile. In 2018, they made investments to create two state of the art manufacturing facilities in Bangladesh. In subsequent annual reports, they’ve mentioned that these two factories need about 3-4 years to break even from the high initial investment. The reason why I call them state of the art will become clear in the next section.

From being a new segment in 2018, manufacturing is now 6% of the topline.

These two plants are expected to turn profitable in the next 4 quarters, and the overall RoCE and margin profile will look a lot better. Let’s not make the mistake of assigning a multiple to a loss making component.

Durable Competitive Advantages

Aside from being a genuine economy of scale which is needed to thrive in such a cut-throat environment, PDS is actually a thought leader in sustainability.

In the west, there is a huge campaign surrounding the waste that is generated through various industries. In retail, 92 million tonnes of waste is produced each year, along with CO2 emmissions. Brands are trying to clean up their supply chain to make sure:

- Workers are paid living wage.

- Factories have limited environment pollution.

- Water consumption is moderated.

We have seen this play out in various chemical companies, renewable energy, etc. and ESG metrics are incredibly important to foreign funds investing in emerging markets.

When PDS built the two factories in 2018, here’s how forward looking they were with their design:

- Since investments in manufacturing was recent, we made sure they were completely sustainable - high automation, new technology.

- The environmental impact of these factories are minimal, they are 21st century factories. Solar panels, glass panelling reducing ambient temperature, comfortable for workers.

- Any waste is recycled using boilers to generate electricity.

- Salaries for workers are above industry normal, closing in on living wage.

This was planned in 2018, well before sustainability became a trend. Not only is this something they’ve perfected, but they’re passionate about this if you listen to the management speak. They recently acquired a majority stake in a company known as Yellow Octopus in the UK. What Yellow Octopus does:

- Yellow Octopus management is incredibly passionate about sustainability.

- Partnered with ASDA and George in the UK.

- If you think of Paypal for payment solutions within one ecosystem, Yellow Octopus offers the same function in sustainability.

- Stock exits - assist retailers with excess inventory, customer returns.

- Take back - We created the first digital take back app in the world https://regain-app.com/

- Re-commerce - Most advanced recycling right now is re-using. Prolonging life cycle of products.

- Impact investing - We invest in new innovations in circular fashion. Connect the dots

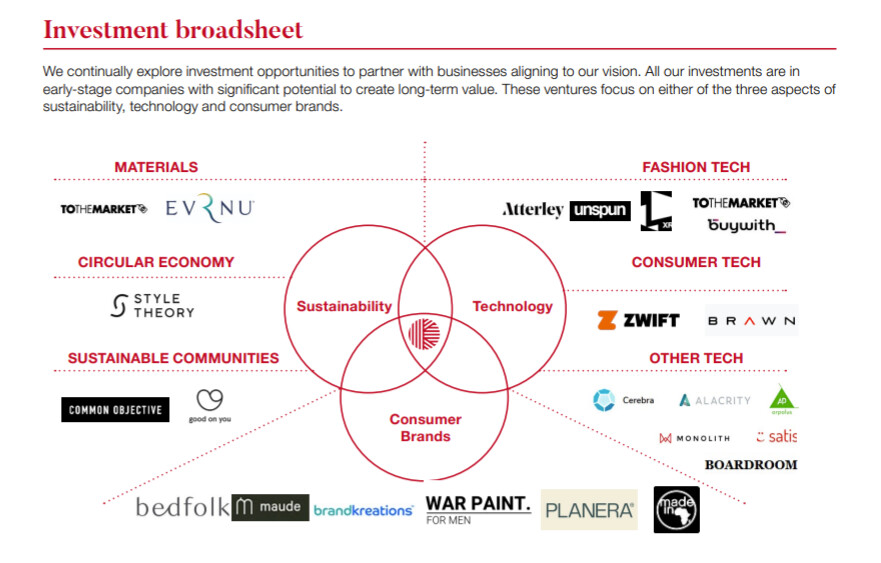

PDS Venture Capital Fund

The third business vertical is investing in a plethora of early pre seed sustainability startups.

Investment Thesis, Peers, and Valuations

The summary so far is that we have an end to end solutions provider, working at global scale with several marquee clients. They’re investing heavily on forward looking ideas that may pan out in the next few years to arrive at ever improving return ratios.

Today, they’re trading at a P/Sales of about 0.5x, and an EV/EBITDA of 10. (This is including a loss making component in the earnings!)

Risks

-

They have 100 subsidiaries. A lot of these have to do with the many ventures in the fund, manufacturing facilities, land deals, etc. Complex structure of subsidiaries would leave a bad taste for many investors. (Was a sticking point in the SIS thread, many similarities as some subsidiaries haven’t been audited by the main auditors.)

-

Low operating margins could wipe them out if there’s an even tighter run ship.

-

Risk from labour reforms in Sri Lanka / Bangladesh that could impact profitability.

-

Retail risk is seasonal, forecasting demand is crucial during holiday season to prevent overstacking inventory / loss of revenue from underestimating demand.

-

The largest revenue share comes from UK and EU customers, even though top 10 clients only account for 6-7% of the revenue each.

-

The stock is fairly illiquid with a 50 day average volume of 9000 shares, or about 1 Cr. daily turnover.

-

There is no analyst coverage from what I can tell. Investors are currently in this alone, and will have no external help on predicting revenues and working out pricing / valuations.

This is a work in progress thread.

To come:

- Management discussion - Lots of recent senior hiring, will be addressed in the next post.

Venture fund composition - Many companies in this venture fund which include global e-commerce marketplaces, and sustainable companies that have partnered up with Nike / Adidas. These deserve their own post. This will underscore just how much attention they give to sustainability.Summary from annual reports

Disclosure: Invested.

Inviting @Investor_No_1, @sahil_vi, @Lynch, @Malkd and regulars for comments. Thought you may find this interesting as we’ve had discussions on similar spaces to what PDS operates in.