Thanks for the kind words ![]()

As a lot of your questions are those of fact, please refer to the following resources:

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11376&Mode=0

Is the RBI circular that started the co-lending framework. The annexure contains information on revenue / profit sharing and examples of weighted averages of interest charged. There’s a more recent circular from 2020 that included housing finance, here’s SBI’s co-lending policy:

This is a nice talk Ugro’s management has given on co-lending, which explains a lot of what’s happening.

As a bonus, here’s a column written by Mr. Nath on the ILFS crisis, and an excellent read on Ugro shared higher up in this topic:

After understanding the basics of how co-lending works, one notices that almost every bank / NBFC has started to talk about co-lending in their exchange filings. Whether this is coincidence, or a sign of what’s to come is an investor’s call to make.

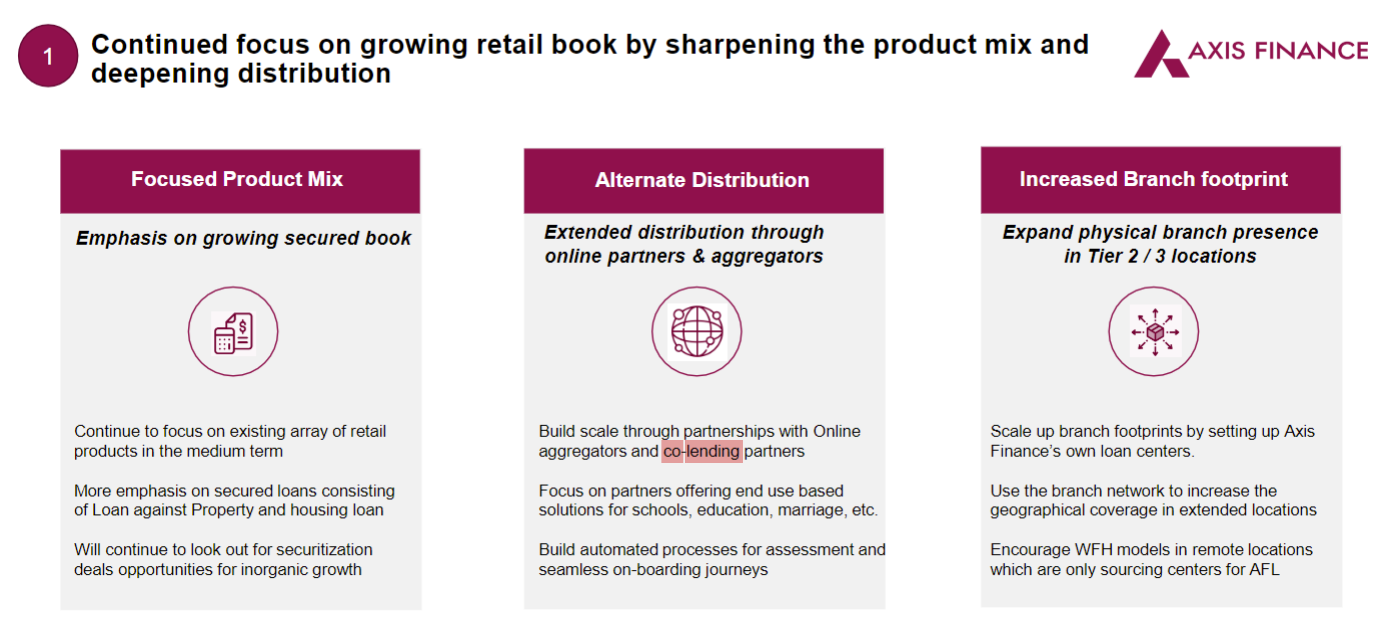

Axis:

Bank of India

Bank of Maharashtra:

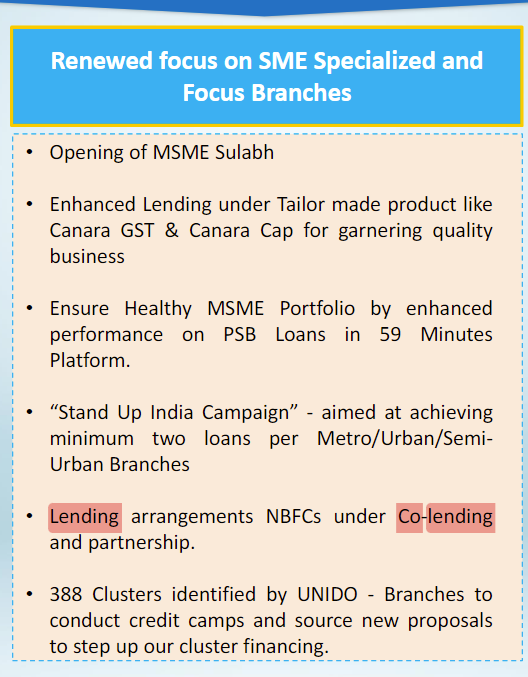

Canara Bank:

CBI:

HDFC:

Chola:

Kotak Mahindra:

M&MFin:

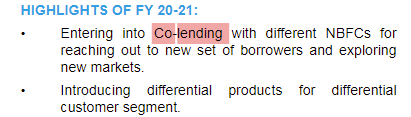

SBI:

To my knowledge, the well known NBFCs are talking about implementing a model for co-lending and are working towards this. In contrast, this is Ugro’s singular focus, their platform and hiring has been focused towards building a working co-lending model.

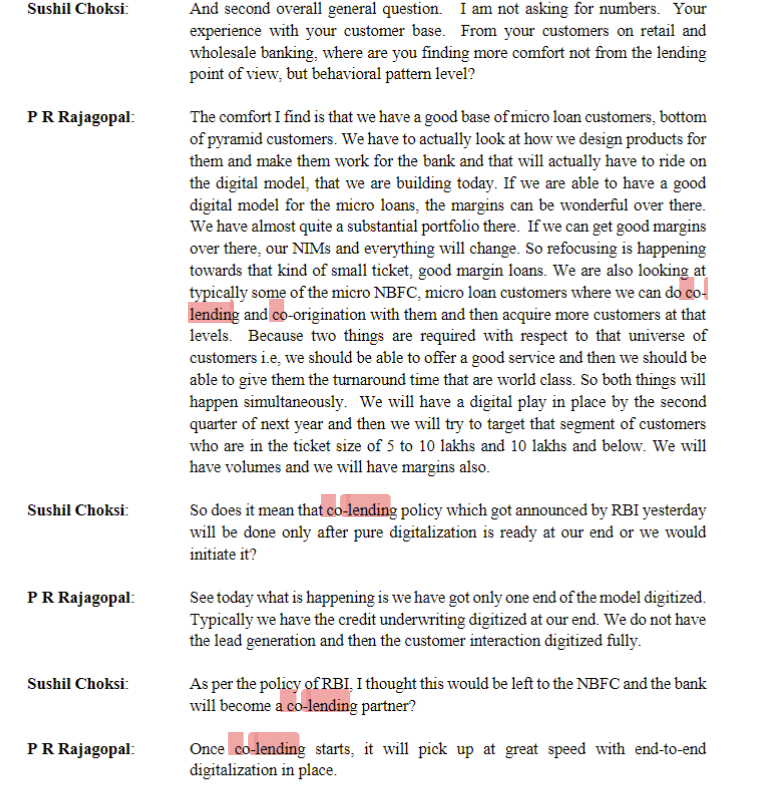

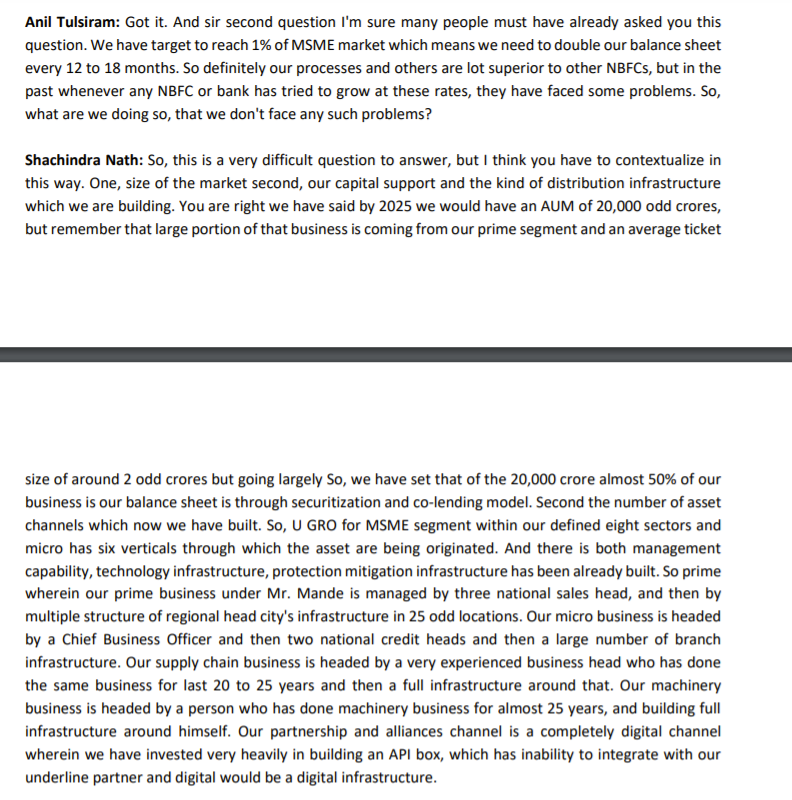

If one were to read only one section of last quarter’s excellent concall, it would be this:

There’s a whole lot more to say, but this is honestly an execution game now.

Edit: The other side of the coin for co-lending:

https://indianexpress.com/article/explained/explained-co-lending-rbi-criticism-7670354/

Invested, transactions in the last 30 days.