I do that by screening for

Sales growth > 15 and

Sales growth 3 year > 15 and

Sales growth 5 year > 15 and

Sales growth 7 year > 15

11 Likes

Hi @Chins

What is your view on Deepak fertilizer after it has corrected almost by 50%. Does this counter look attractive to you given their next 2 to 3yrs plan or the valuations are still not decent enough and you are waiting for a better opportunity.

I think there are numerous posts written in the older VP threads on this topic. I try to keep track of volumes and realisations to see what’s the growth driver. I also try to read what other companies in a sector are saying to know what cycle the industry is overall feeling.

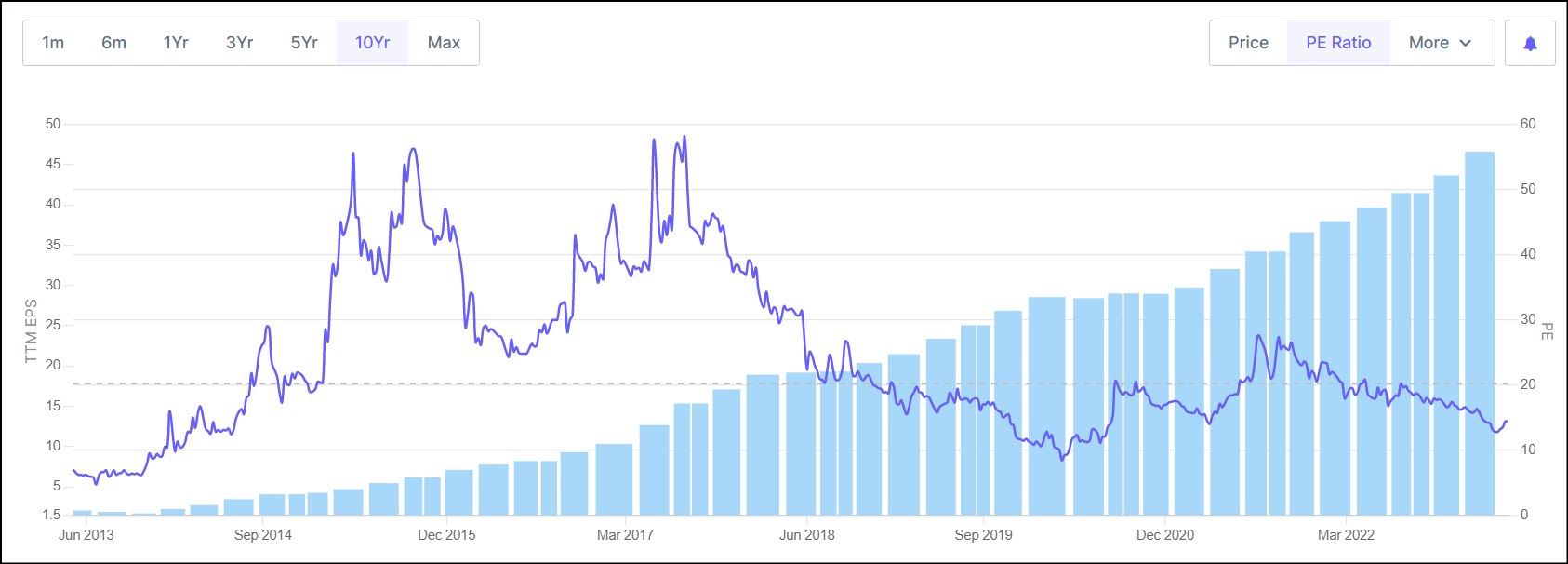

I quite like the company, and was the largest driver of returns in my portfolio last year. I believe the share price currently reflects the prices of TAN, as it contributes over 70-80% to Deepak Fertiliser’s bottom line.

My guess is that they’ll do around 160-200 Cr. of PAT in Q4FY23, similar to Q3FY22.

Their capex unfortunately comes onstream just as an incredible cycle comes to a close. As someone sitting on the sidelines, I’m hoping the new capex runs into teething issues, or delays. I’d like a little more value before investing again, especially if TAN falls another 50% from here.

7 Likes

Hi Sahil…will the crash in some of the big Global banks impact the Indian banks as well…what’s your view on these 3 at this point of time

Sarthak Metals

South Indian Bank

Tirupati Forge…

1 Like

Sorry for asking the question here.

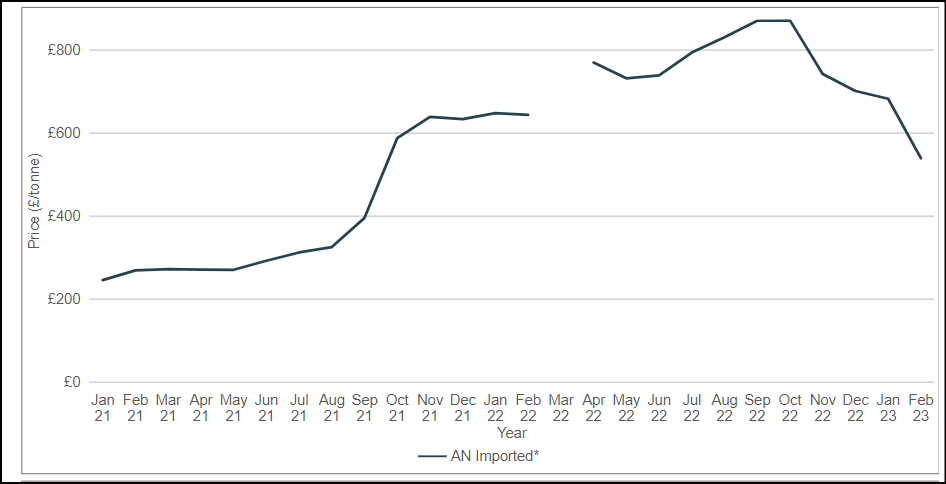

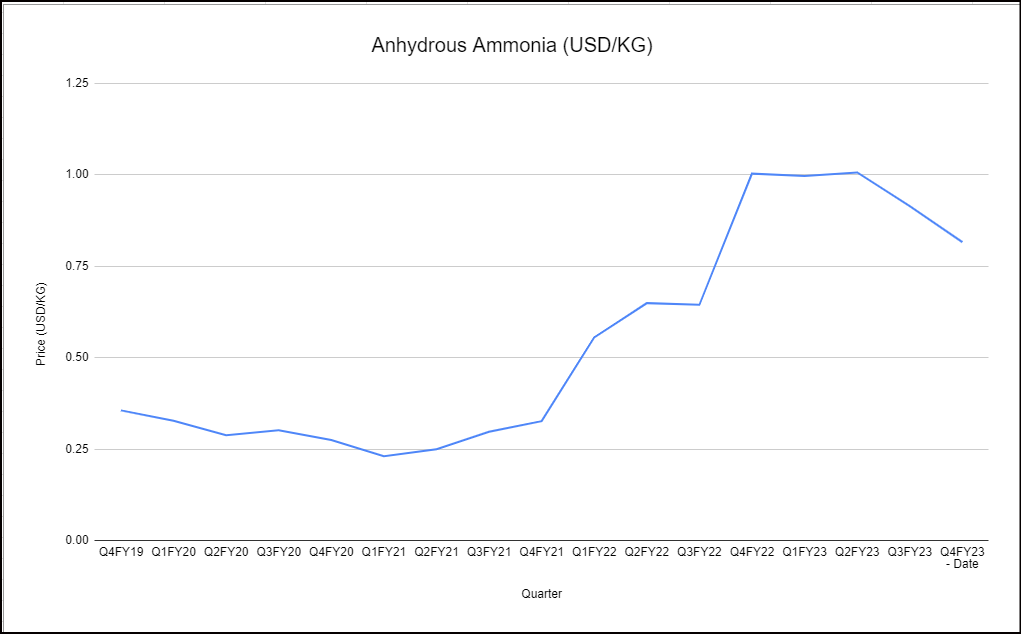

- Are these the price of Ammonium nitrate? If yes then how do you track the prices of AMMONIA the raw material for AN. Why because if I have to calculate the margins I will also need to quantify the fall in prices of ammonia.

What I don’t understand fully is the interplay between fertilizer subsidies, and their strategy for margin expansion given farmers with limited purchasing power are the end user. Once I understand this, I will write a follow up.

- Were you able to understand this ??

- What is the fall you expect in the price of AMMONIA for AN to fall by 50%

- Does the price of TAN have relation with its RAW material or it is purely demand and supply.

- Since every year we have an incremental demand of 60000tons of TAN and the gap between existing capacity and TAN keeps increasing and considering AN is just a byproduct for other players what kind of margins Deepak would have with a fall of another 50% in TAN. Considering RAW material price does not change.

- What kind of further value are you looking at. Please share if you are comfortable.

1 Like

I have multiple subscriptions to various sources of market intelligence, and track the prices of chemicals this way.

The price I’ve shown in the chart is the international price for ammonium nitrate. If you’d like to see the prices of ammonia, one can see the chart below. This is specifically the price Deepak Fert has paid for anhydrous ammonia over the last few years.

I think ultimately both depend on natural gas prices.

Natural gas → Ammonia → Ammonium Nitrate

The price of natural gas was the driver for the cycle seen in 2022. Then, Russian TAN supply was off the markets and had a knock on effect to the price of TAN. Now things have ultimately cooled in natural gas, and I think both ammonia and TAN will ultimately revert back to long term averages.

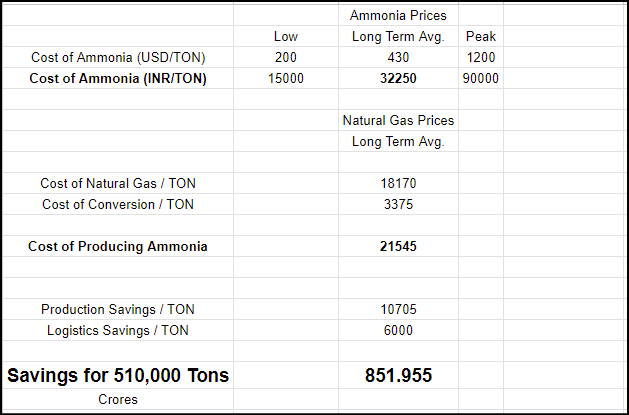

Hard to say. I think before the ammonia plant comes online, maybe 20-25% margins in TAN compared to the 35-45% margins seen in the peak of 2022. It’s hard to say because Smartchem has an NPK division inside it alongside TAN so the margins are not transparent. Similarly, the chemical division also includes nitric acid, which isn’t as high margin as TAN.

This calculation will of course change once the ammonia plant comes onstream. Management long ago explained the unit economics for cost savings and one can update it to include current prices:

As far as the fertiliser side of things is concerned, I wrote a post here:

https://twitter.com/Chins1729/status/1548322470637146115

To summarise, I have seen investors burn their hands in companies that have capex come onstream just after a powerful cycle. Here, the difference is that the capex is for in-house consumption. The plan however is to have a larger margin of safety before investing again.

With the demerger of their different entities, the hope is that the TAN vertical’s unit economics become transparent.

Hope this helps!

13 Likes

Updates on current portfolio and positioning for FY24.

| Financials | 29.97% |

|---|---|

| UGROCAP | 24.31% |

| FUSION | 3.37% |

| SPANDANA | 2.29% |

-

Have held Ugro for two years now. Stock has underperformed expectations and has remained cheap over the last two years, but I’m very happy with the underlying business. We’re now at the year where the scale in co-lending should reflect in the bottom line. Expecting 200 Cr. of PBT in FY24.

-

MFI sector looks to be set for a good cycle. Fusion and Spandana are both available at less than 1.5x FY24 book, and can both do 4%+ RoAs if the cycle remains strong.

| Chemicals | 18.80% |

|---|---|

| FLUOROCHEM | 4.17% |

| SHARDACROP | 3.54% |

| TRANSPEK | 3.25% |

| ULTRAMAR | 2.44% |

| PUNJABCHEM | 1.87% |

| SUDARSCHEM | 1.77% |

| VALIANTORG | 1.76% |

- I’ve used the time since the last update to scale my position in companies trading at 12-15x trailing earnings that can show good growth in FY24. GLS, Transpek, Caplin, Ultramarine, Sharda Cropchem, and many more fall into this category.

- Following on from this post, I have a basket of companies in the dyes and pigments space between Sudarshan, Ultramarine, and parts of Valiant’s business. I’ll scale both Sudarshan and Ultramarine post Q4 should the outlook turn more favourable.

| Healthcare | 26.34% |

|---|---|

| KRSNAA | 13.30% |

| CAPLIPOINT | 7.83% |

| GLS | 3.98% |

| RELIGARE | 1.23% |

- I have the highest confidence in Caplin Point’s IRRs at this price. It’s trading extremely cheap, with no impairment of earnings. There are additional optionalities with a loss making subsidiary turning profitable, strong product launches, and capex triggers towards the end of FY24. For this reason, I have scaled Caplin to 8% of my portfolio. My exit model is at 20x earnings, and 500 Cr. of PAT, around 1200 per share.

| Commodities | 9.91% |

|---|---|

| COASTCORP | 2.40% |

| SHYAMMETL | 2.17% |

| AVANTIFEED | 1.96% |

| MAITHANALL | 1.93% |

| NCLIND | 1.45% |

-

Coastal Corp has overpromised and under-delivered in the last year. There are three parts to the thesis: 1) client wins in Japan / South Korea that should drive growth in shrimp independently from what’s happening with Ecuador; 2) management claims Ecuador’s preferred market is China, and that inventory for shrimp should clear up in the US this summer, 3) their Ethanol plant could be the cheapest in the country and a very high RoE investment. Shrimp outlook in general is horrible and Q4 should be very painful.

-

Maithan and Shyam are trading very cheap at the moment. Shyam has near term earnings triggers with a lot of volumes coming onstream soon. Maithan has not traded at these valuations for a long time, and often doesn’t remain below book value for long.

| Miscellaneous | 14.52% |

|---|---|

| GLOBUSSPR | 2.92% |

| KPIGREEN | 2.34% |

| DHRUV | 1.97% |

| RUPA | 1.88% |

| GOKEX | 1.68% |

-

KPI Green has time corrected since the last time I invested in it, higher up in the thread. Sitting on around 15% returns on it right now. Will probably sell if there’s a rally post earnings.

-

Have started building a position in the textiles space. I currently have a preference for US facing textiles and domestic. The UK / EU should continue to see a cost of living crisis, and PDS may see FY24 to be challenging. Will do more scuttlebutt and invest when things make sense. My plan is to increase allocations to both GokEx and Rupa with time, and maybe also buy Lux.

| Evaluating | |

|---|---|

| AURIONPRO | 1.66% |

| ANGELONE | 1.43% |

| ADORMUL | 0.63% |

| CELEBRITY | 0.50% |

- Recently met the MD of Ador Multiproducts to evaluate it as a turnaround candidate. Will make a company thread on VP soon.

Exits from the last update:

-

Sold IMFA at around 320 per share, making around 22% on my investment.

-

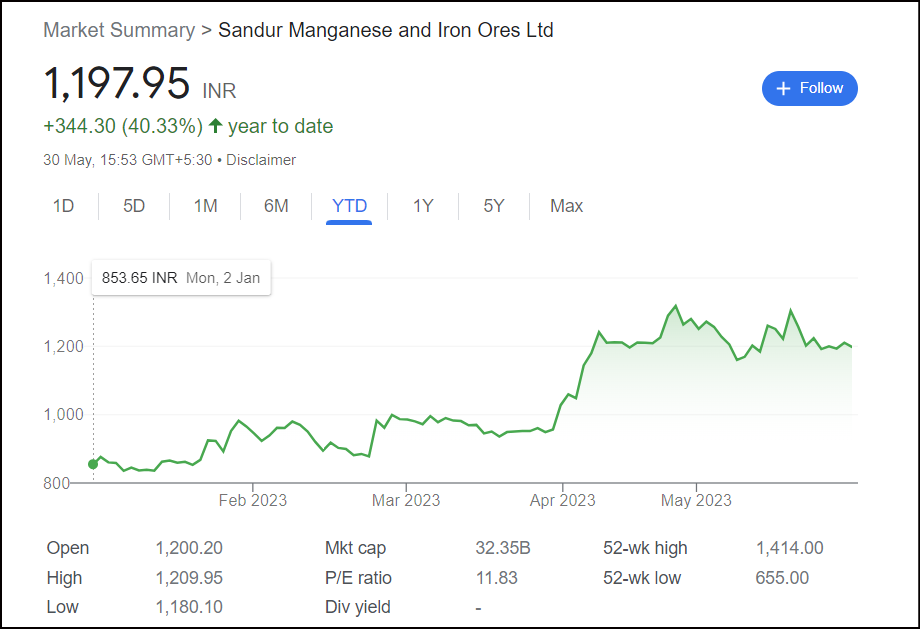

Sold Sandur Manganese at 1280 per share, making 38% on the trade.

-

Sold Shivalik Bimetals at 510 per share, making 82% on the investment.

-

Sold Kriti Industries at 107 per share, making around 26%.

I have a lot of ideas that I’d like to scale, but happy with my holdings right now and have no cash. Have brought down the valuations of the portfolio by buying more companies that are in the 12-15x earnings range, and in fresh sectors that have been seeing headwinds, like textiles.

There have been so many opportunities at these valuations that I’ve preferred to take multiple 2% positions, and only scale to 4% or more where I have more confidence that growth will sustain.

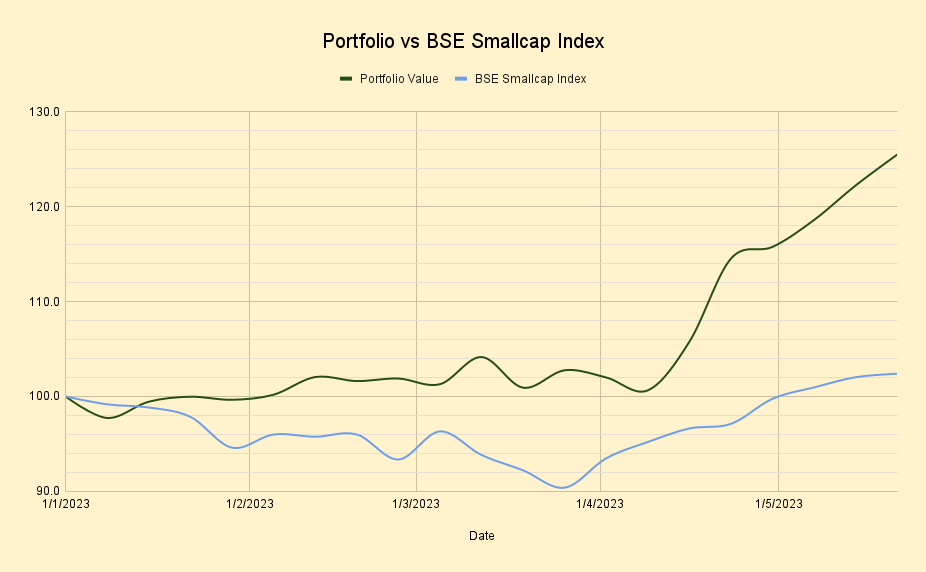

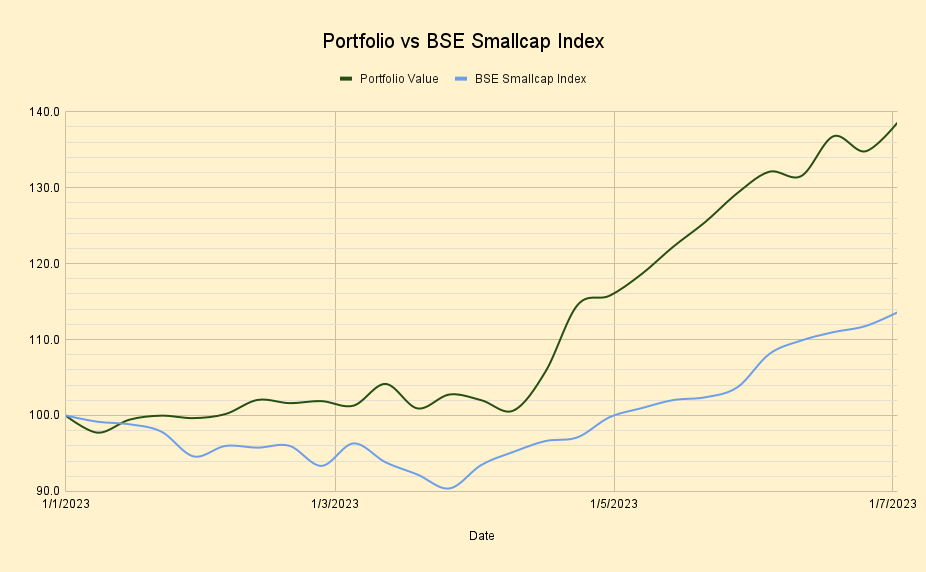

Portfolio is up around 11-12% since January.

Welcome any and all comments. ![]()

34 Likes

How do you view Ambika Cotton. Trading at 6PE. Earnings of last year may not be sustainable this year, but still would be cheaper as compared to GOPEX, RUPA or LUX. Large cash on the balance sheet. I know management is not very aggressive and hence use of cash maybe creating a doubt in the minds. But a large dividend is definitely a possibility here?

2 Likes

What is your rationale for exiting Shivalik - valuation or slowing growth in future?

Thanks

2 Likes

I haven’t studied it in detail. At first glance, it looks like margins will normalise to the 18-20% range with prices of cotton coming off. Secondly, the last two years have seen higher than average asset turns.

In the absence of known capex triggers, what do you think the optionalities are?

There are a number of companies in my portfolio that I’ve bought mid-cycle that are not objectively cheap. Fluorochem, KPI Green, Shivalik, arguably even Krsnaa. For all of these, I’d like to be more strict with weights and exits once I think incremental risk reward is unfavourable.

For Shivalik, if they can do 1600 Cr. of revenue in 5 years, it’ll be around 230 Cr. of PAT. From these valuations, my expectation is around 15-20% IRRs if they execute. It’s a phenomenal business and they’ll probably have more triggers with time. From here, if there’s ever an unfavourable turn in the cycle, I’d love to buy back in closer to starting valuations of 20-25 times.

In the family portfolio, companies like TCS and Infy showed a CAGR of 17% (without dividends) during the peak valuations last year, and post the de-rating in IT, it looks closer to 14% after 20 years. My current mindset is that holding for a longer period without churn works if companies are at really cheap starting valuations. RACL was at a PE of 3-4 during 2020, Shivalik was at a PE of below 10 in 2019. If I owned either from those valuations, I wouldn’t sell right now.

My thesis in Ugro is that it’s quite cheap for the business model that they’ve built, and in my view, it is as cheap today as RACL and Shivalik were in the past. If they can execute and prove themselves on asset quality, if RBI continues to have a favourable view towards co-lending, and there isn’t a blackswan event in MSME lending, a business that can generate 5% RoA at scale shouldn’t trade at book value.

In all my other holdings, if valuations run far ahead of earnings, I’ll reconsider my weights in them as things progress.

I could be very wrong. ![]()

28 Likes

Just a short update as earnings are coming in.

Fusion and Spandana have come out with great results.

I have doubled down and added Satin Creditcare, Ujjivan Small Finance Bank and Manappuram Finance in my MFI basket. Post this re-jig, MFI is now 20% of my portfolio.

- Satin is the cheapest in the MFI space right now at 0.6 times FY24 book. Ujjivan is at 1.3 times FY24 book, and Manappuram at around 0.9x FY24 book. I’m happy to go overweight on MFI and assess constantly as things play out.

I have swapped out of Maithan to raise my stake in Shyam to 6%. Shyam too has come out with a great set of results, and is trading extremely cheap. There are multiple volume triggers over the next few quarters while realisations across the space have been beaten down.

The plan with Shyam is to hold for a few quarters until the other commodity players fall into my price range.

The other new addition to the portfolio has been in the chaddi companies. I have 3% in dollar, 2% in Rupa and Lux. From here margins should recover over the next few quarters.

As a final note, my portfolio is up around 26% YTD. Around 10% of this has come from Ugro’s recent rally.

Currently evaluating Solara and Shilpa Medicare. Would like to add to Coastal post results.

20 Likes

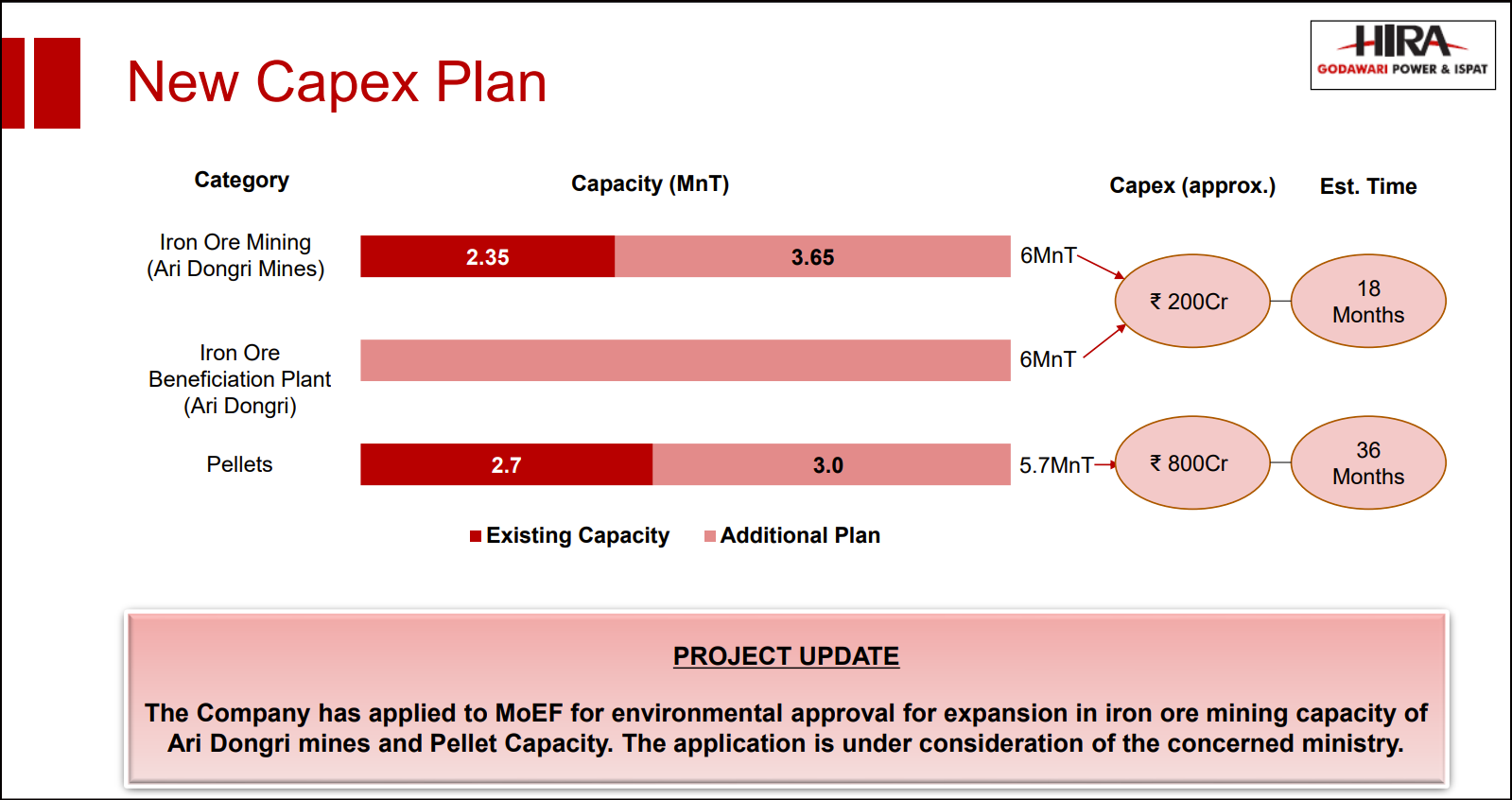

Isn’t GPIL better placed considering capacity expansion plans & even cheaper valuations?

I disagree. Everyone has capacity expansion plans, the question is when these triggers play out and how early one wants to be. In the absence of volume triggers, this sector largely moves with the sentiment of the underlying commodity.

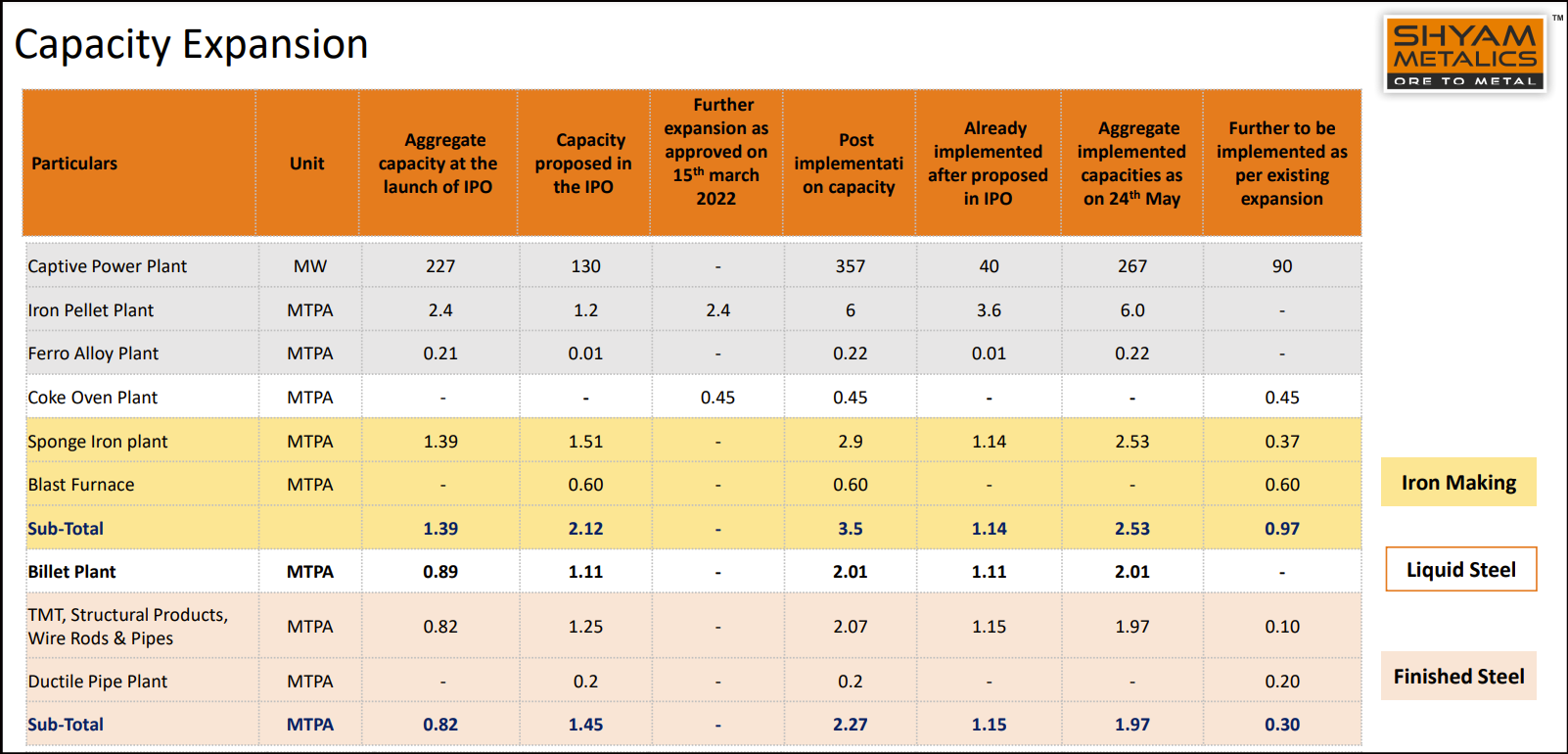

For Shyam, a lot of this capex has been capitalised, so one has volume growth even though the underlying index is in the doldrums.

Sandur Manganese too had an incredible first half of the year with the stock rallying on expectations of their mining EC coming through.

In GPIL’s case, despite all the stories written on the company thread, it looks like FY24 is a year of consolidation in terms of volumes, and capex triggers will play out in FY25 and beyond.

There are many nuances in the story. Shyam didn’t have captive mines until recently, and then they had to pay a premium. I’m playing this in the simplest possible way: to have volume growth on my side until realisations recover.

I’ll churn out of Shyam eventually depending on how the cycle moves.

8 Likes

The recent results suggest that the volumes are back to normal. The margins however are still suppressed. None of the management have clarified it yet. My expectation was that once the yarn price stabilize/rise, the higher demand will lead to margin revival.

Was this as per your thesis or was it a surprise?

Edit: Rupa clarified that it was because of the high cost inventory

3 Likes

Hi Chins, saw that you are interested in the green energy space. Id love to know your views on SW Wilson? Looks like they are going to be able to turn around the company in FY24. However, given that their book value has been practically brought down to zero, what’s the correct way to value such a company?

1 Like

@Chins wanted to know thesis about this. Are the valuations really in the sweet spot here?

Take rupa for instance. If we assume management’s guidance of 25% revenue growth and 11% EBITA, then it’s trading at 18 times FY24 earnings. The mean PE has been around 20.

I’ve been looking to play the mean reversion in textiles but the equation hasn’t been lucrative enough for me. What are your thoughts on this?

3 Likes

Also, what are your views on VIP industries with recent preferential issues and suni alagh joining board?

1 Like

Hi Chinmaya. Hope you’re doing well.

Wondering if you would care to explain why you think so? Could you please elaborate on how you track the MFI space; in particular, what metrics or parameters are ‘predictive signals’ towards a forthcoming upcycle or downcycle in microfinance? E.g., any metrics around provisions/NPAs? Any management teams whose commentary in concalls you consider to be a good indicator of the future? What combination of leading and lagging indicators are you tracking to monitor the phase in the cycle? Thank you so much.

2 Likes

Would like to hear your thoughts/analysis on both Aurion Pro and Ador Multi products as you were evaluating these companies

Thanks

1 Like

I haven’t been very active on the forum this year; the markets and work have been keeping me busy.

Portfolio Updates

This has been a very good couple of months. My portfolio is up around 39% YTD.

Top Holdings:

| Stock | Allocation |

|---|---|

| Ugro Capital | 25% |

| Krsnaa Diagnostics | 13% |

| Caplin Point | 8% |

| Shyam Metallics | 8% |

| Satin Creditcare | 7% |

| Sudarshan Chemicals | 7% |

| NMDC + NMDC Steel | 6% |

| Coastal Corp | 5% |

| Solara | 5% |

| HOEC | 4% |

| Spandana | 4% |

Some exits from the last update:

| Stock | Exit | Profit/Loss | Allocation |

|---|---|---|---|

| Fusion | 510 | 36% | 4% |

| Fluorochem | 3389 | 29% | 4.2% |

| Sharda Cropchem | 550 | 20% | 3.7% |

| Transpek | 2000 | 20% | 3.5% |

| Manappuram | 128 | 19% | 5% |

| GLS | 541 | 24% | 4% |

| Globus | 1000 | 28% | 3% |

| Gokex | 480 | 33% | 2% |

| Shilpa Medicare | 300 | 31% | 2% |

In hindsight, I should have been more aggressive with Gokex and Shilpa at that price point, but overall, around a third of my portfolio was churned since the last update, booking around 8% of overall portfolio value in profits.

Currently evaluating:

-

Man Industries

-

Lakshmi Electrical Control Systems thanks to @Malhar_Manek

-

Looking to raise weight in Solara and NMDC steel

Thank you for reading the thread, and I’m sorry I haven’t found time to answer the questions above, I’ll get to them perhaps over the weekend.

28 Likes