I am contemplating a position in Ultramarine Pigments. Here is my thesis:

Background - Cyclical Lows

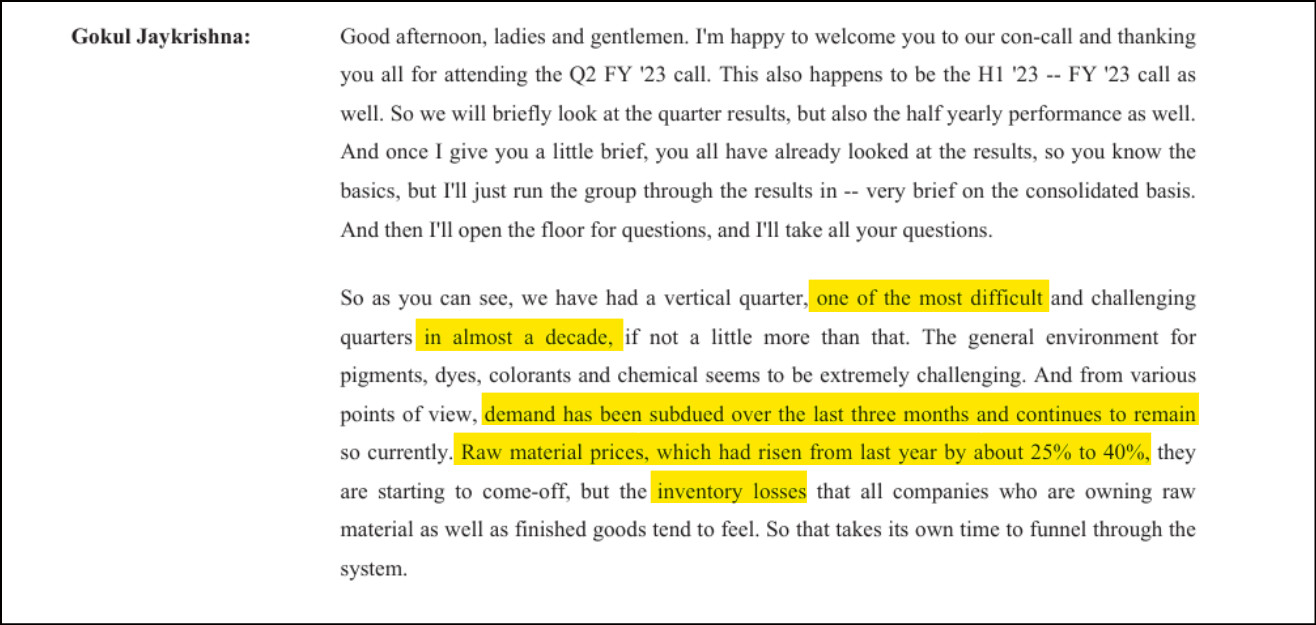

The entire dyes/pigments pack is trading at cyclical lows, and has seen tremendous margin pressure in the last two quarters. So much so, that Asahi called the last quarter the worst in more than a decade.

Sudarshan Valuations

Ultramarine Valuations

Asahi Valuations

Asahi Songwon and Sudarshan Chemicals both point to three particular problems on the ground.

- Subdued demand, especially from Europe.

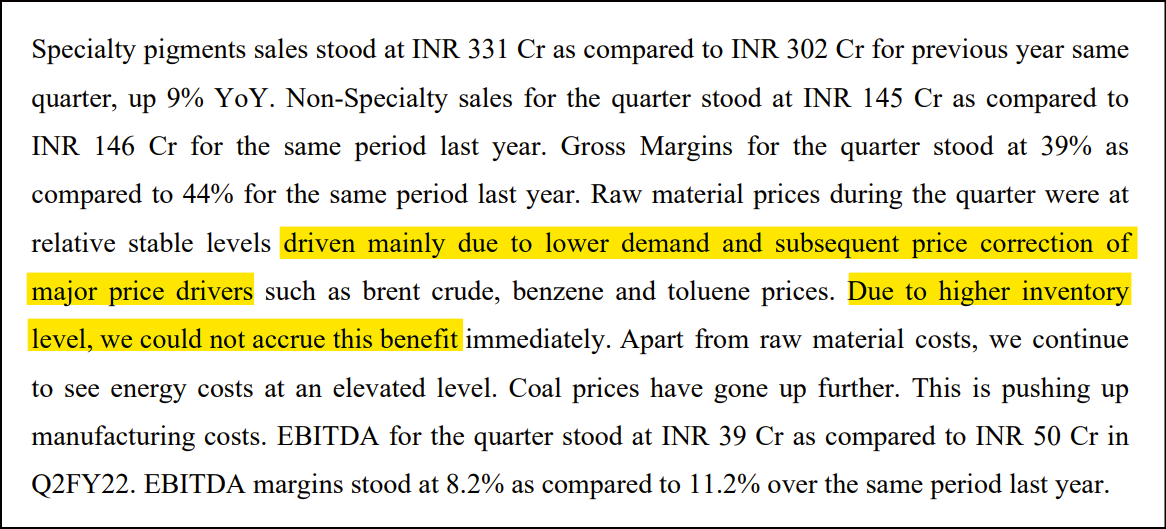

- High raw material prices that are starting to cool.

- Inventory losses from high cost RM.

Asahi concall:

Sudarshan concall:

Thesis - Focus on the 3 Points

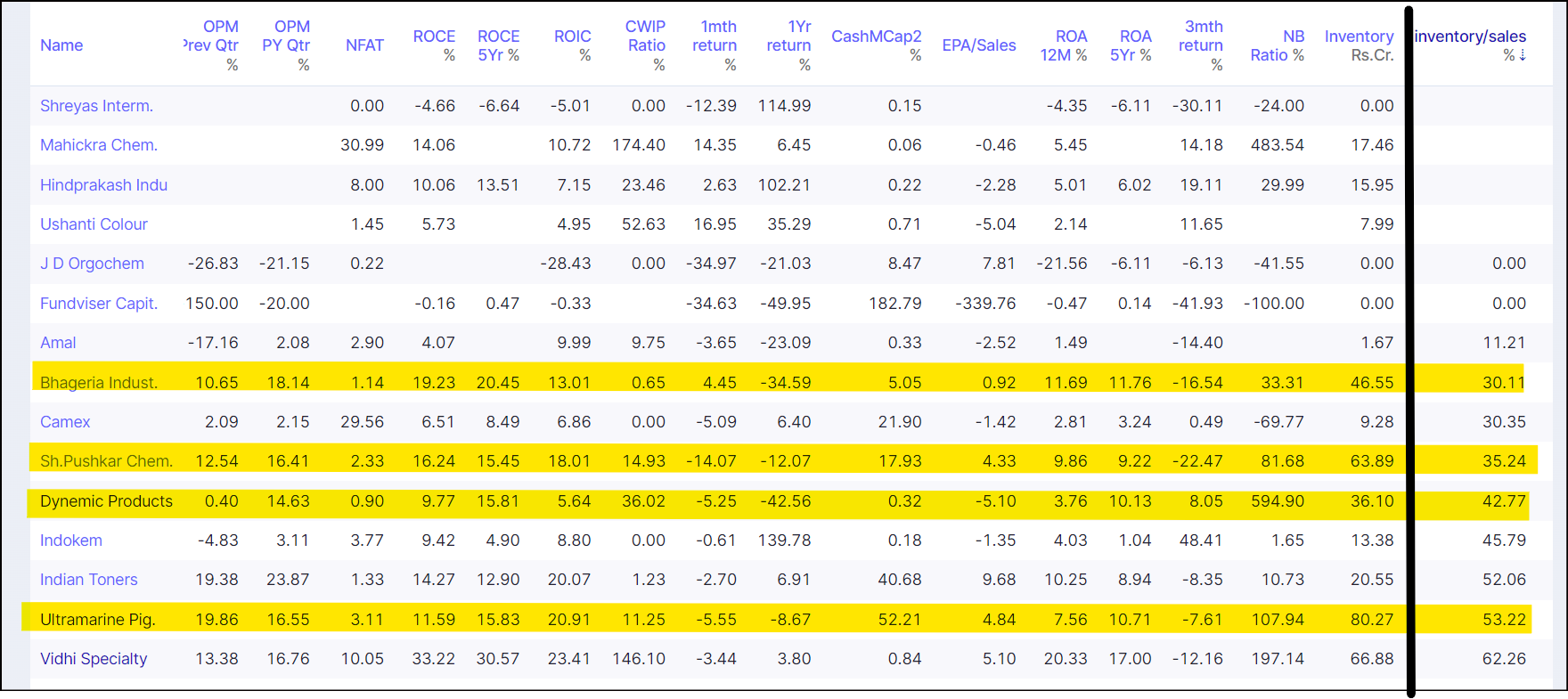

If companies in the space will need 3-6 months to clear high cost inventory, the companies with lowest inventory on hand stand to benefit, mean reverting first.

Therefore, I create a ratio on Screener that compares inventory to quarterly revenue. The companies with highest inventory will be hit hard, I want to focus on the companies with the lowest inventory.

Companies like Asahi have much higher inventory, and are not highlighted. This picks out four interesting players.

On gross margins, Ultramarine and Dynemic have the highest at around ~45%, followed by Pushkar at 30% and Bhageria at 20%. I reject Bhageria on these grounds, and prefer Ultramarine and Dynemic to Pushkar.

Coming to dependence on EU/UK, both Ultramarine and Dynemic have <10% revenue from these regions and pass this check.

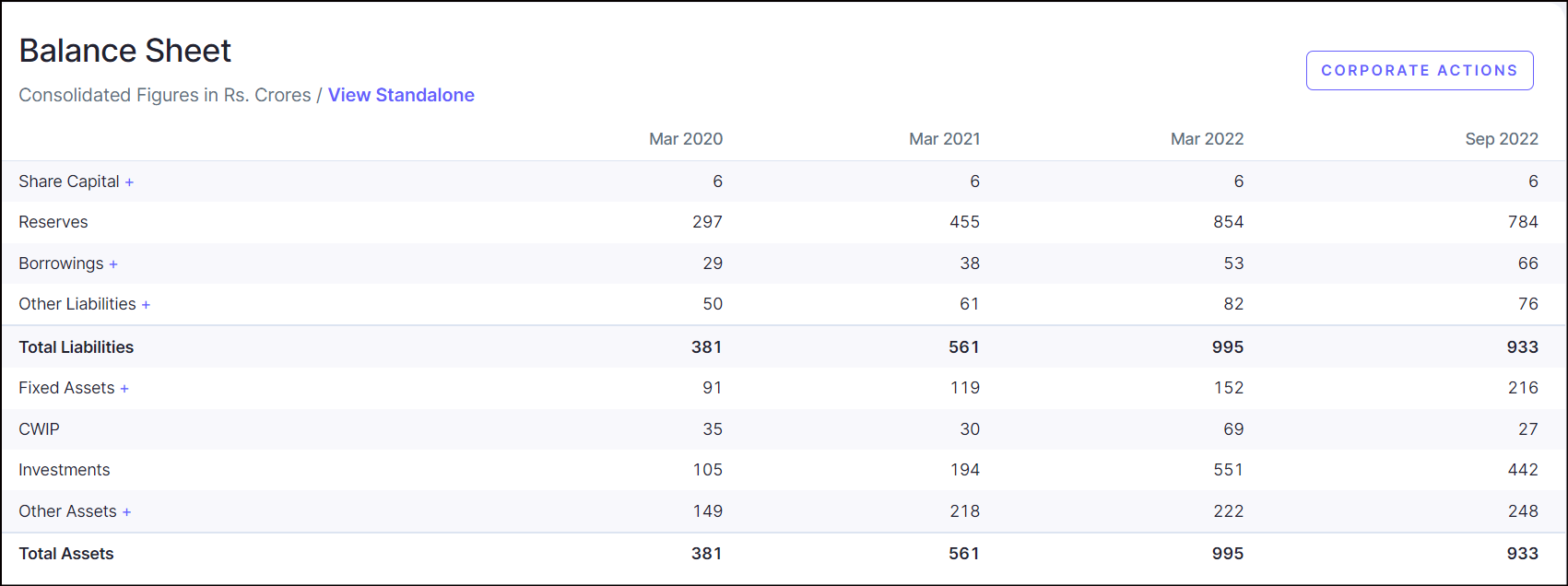

These two have an additional optionality in capex.

Dynemic has more leverage, but has recently completed an enormous capex:

Ultramarine has a cleaner balance sheet.

Currently studying the surfactant division.