Hi Sahil,

How did you screen sarthak metals and tirupati forge, considering they are micro caps?

Also in your case, what is the best way to screen stocks? By best, I mean a filter, applying which most of the noise gets reduced automatically and we have to read only small set of companies.

I am contemplating a position in Ultramarine Pigments. Here is my thesis:

Background - Cyclical Lows

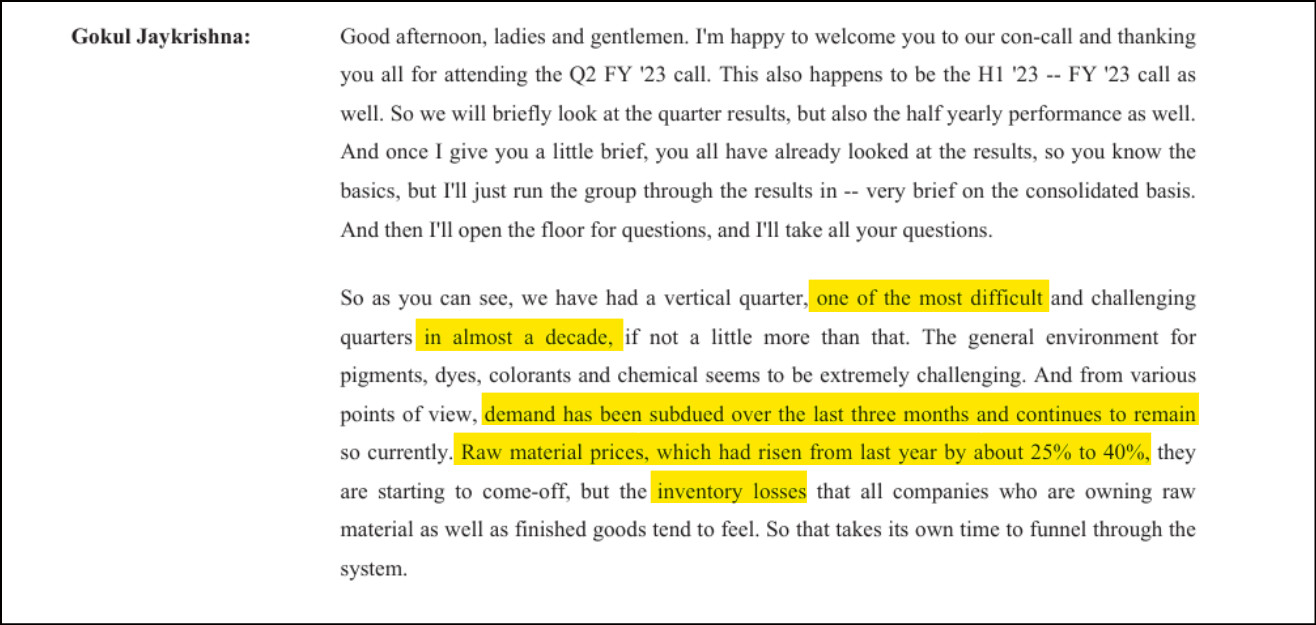

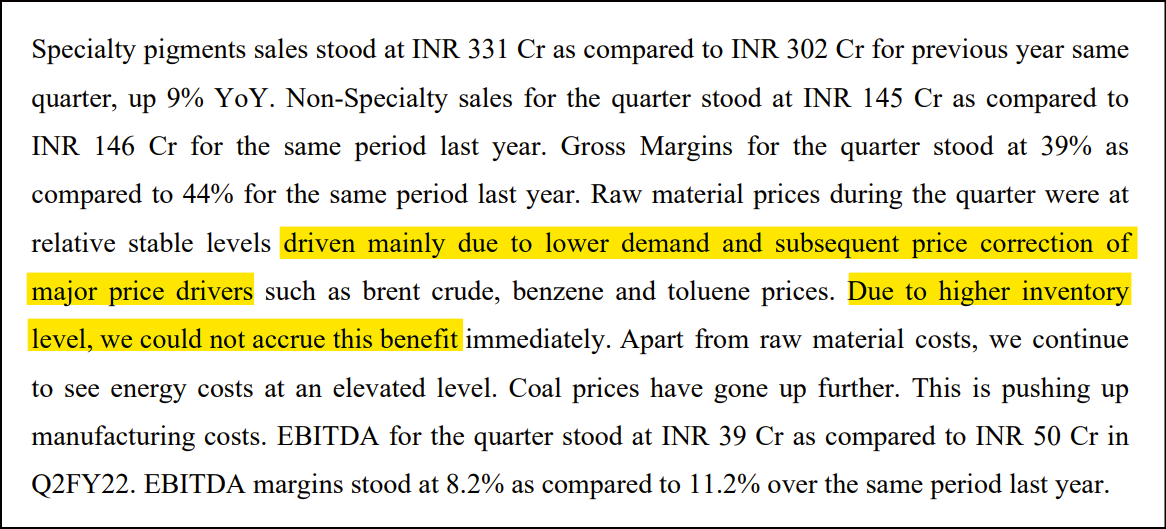

The entire dyes/pigments pack is trading at cyclical lows, and has seen tremendous margin pressure in the last two quarters. So much so, that Asahi called the last quarter the worst in more than a decade.

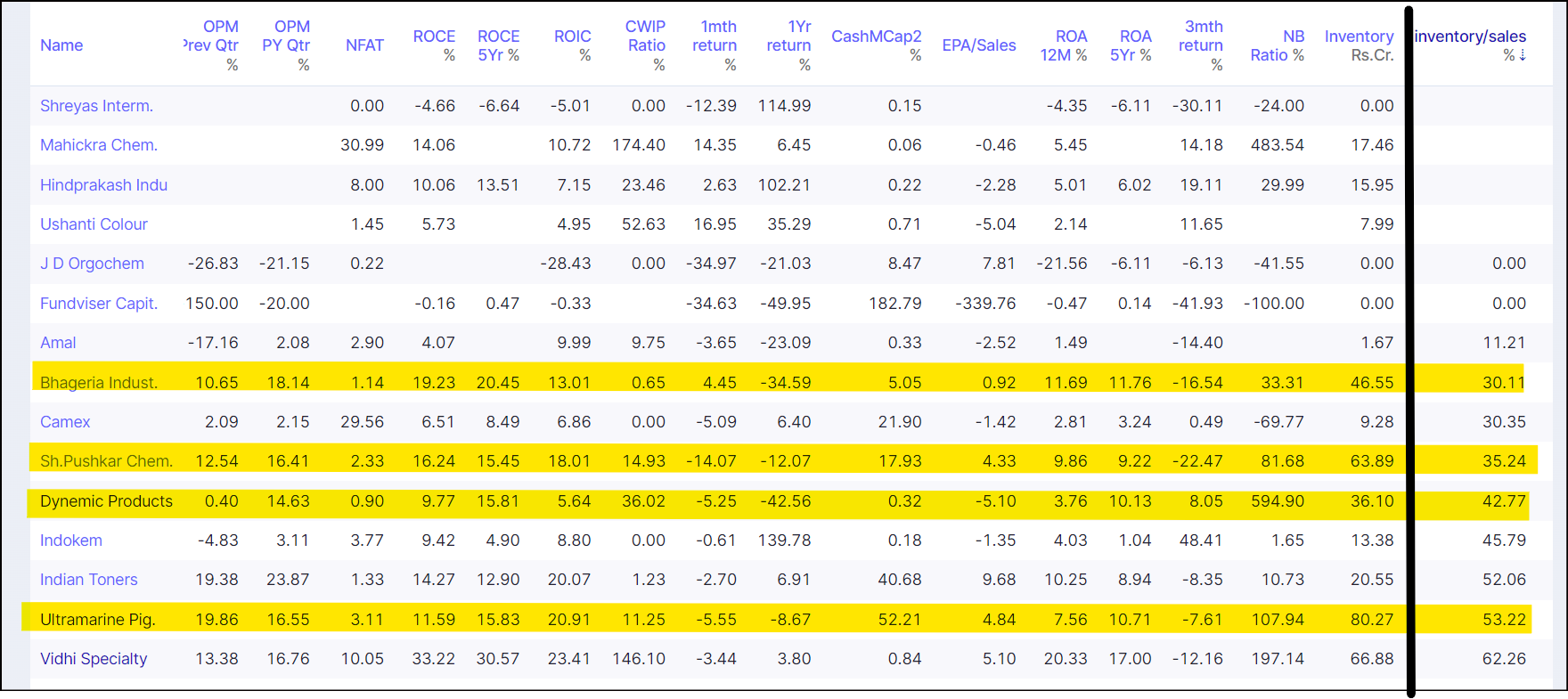

If companies in the space will need 3-6 months to clear high cost inventory, the companies with lowest inventory on hand stand to benefit, mean reverting first.

Therefore, I create a ratio on Screener that compares inventory to quarterly revenue. The companies with highest inventory will be hit hard, I want to focus on the companies with the lowest inventory.

Companies like Asahi have much higher inventory, and are not highlighted. This picks out four interesting players.

On gross margins, Ultramarine and Dynemic have the highest at around ~45%, followed by Pushkar at 30% and Bhageria at 20%. I reject Bhageria on these grounds, and prefer Ultramarine and Dynemic to Pushkar.

Coming to dependence on EU/UK, both Ultramarine and Dynemic have <10% revenue from these regions and pass this check.

These two have an additional optionality in capex.

Dynemic has more leverage, but has recently completed an enormous capex:

I have sold Godawari Power today. Friends who track the company very closely think there’s still upside left, valuing it at around 5x EV/EBITDA (compared to 4x EV/EBITDA today). I’m happy to give up some of the upside.

To summarise my current framework:

I have roughly 50% of my portfolio in investments where I see longer runways of growth. I do not plan on touching these unless:

Something I’ve priced in turns out to be untrue.

There’s a large one-off that has resulted in a rally that takes valuations to a point that is unsustainable.

There is a sudden change in business momentum during which holding results in an extremely unfavourable risk-reward.

The remaining 50% I want to keep rotating into ideas that I think can produce a 30% upside. Here, I’d like to be stricter in entry/exit, even if I lose out on the upside. Then, move into companies that are cheap, and repeat.

So far, I’m happy with my hit rate in this basket.

NMDC, AB Capital, Godawari Power, Equitas, SJS, and now Suryoday have played out.

PDS, Deepak Fert and Aegis are examples that used to belong in the first basket, but moved into basket 2 and were subsequently sold. Would leap at the opportunity to add them again.

Current watchlist and thought process:

I’m planning on reducing Avanti Feeds from 7% to 5% during the next rally, lowering my average in the process.

Stock

Thesis

Trigger

Caplin Point

Very successful scale up of sterile injectables, with multiple optionalities

H2FY23 Onwards

Kriti Industries

Recovery from the fire, horrible base for earnings. Sector has seen pain

After Q3FY23 results

Ultramarine

Discussed above

-

Sudarshan Chemicals

Can benefit from demand from the paints industry, competition from China is exiting the space

After Q3FY23 results

Punjab Chemicals

Great business, horrible margins. Thesis is of growth, and margin expansion closer to peers.

Possibly after Q3 results

Maithan Alloys

Lowest cost producer of alloys. Great business even during downcycles. Is currently at bottom valuations.

?

Gokaldas Exports

High inventory from retailers should hurt the business in the next 2-3 quarters.

H2FY24?

On performance, portfolio is up 20.8% on realised profits, and around 27% including unrealised since April 1 2022. Small cap index is up 4% in the comparable period. Currently hold around 20% cash.

@Chins

Hi sir,

I see my way of investing very similar to yours like I also prefer to hold 50% to 60% for long term and play around with rest of the money. The only difference is I also love to trade on my long term holding as I understand their movement to some extent.

I have had very similar picks to you without even knowing that you have bought them or interested in. Eg NMDC, AB CAPITAL, DEEPAKFERT, GPIL

and it is quite interesting that my cash as of today is 18% :grinning

Just wanted to get some insight form you

Do you plan to maintain your cash balance? are you waiting for some dip in the market? how do you plan to use your cash?

Do you still plan to hold NMDC considering it gave a pretty decent move or you plan to hold it and enjoy dividend.

Are you comfortable with DEEPAKFERT valuations or you expect some more correction here?

If I were to ask your view on manappuram fin, Indiamart, IEX, zensar tech, bandhanbank. If you are tracking these stock or just a very basic view of your in these stocks?

No such plan in terms of the broader markets. I’d like to allocate as and when things in my watchlist fall into my valuation zone.

I sold NMDC a while ago.

I think TAN realisations are unsustainable, given that prices are 3x their long term averages. The new plant will raise sustainable margins, but I thought it best to exit at the peak of the cycle. Perhaps the market may like the demerger news.

I was initially skeptical of Manappuram and the gold loan pack once banks started entering the space. Now I realise there were two good contra plays: IIFL and Manappuram. IIFL has grown their loan book the fastest in the pack, Manappuram has more to it than just being a gold financier.

I hope a single snip from a Morgan Stanley report is okay; I do not wish to circulate the report. Will delete the post otherwise.

I’m building a position in both Manappuram and CreditAccess at the moment. No views on the others.

D: Please do not take this as investment advice. I am very often wrong.

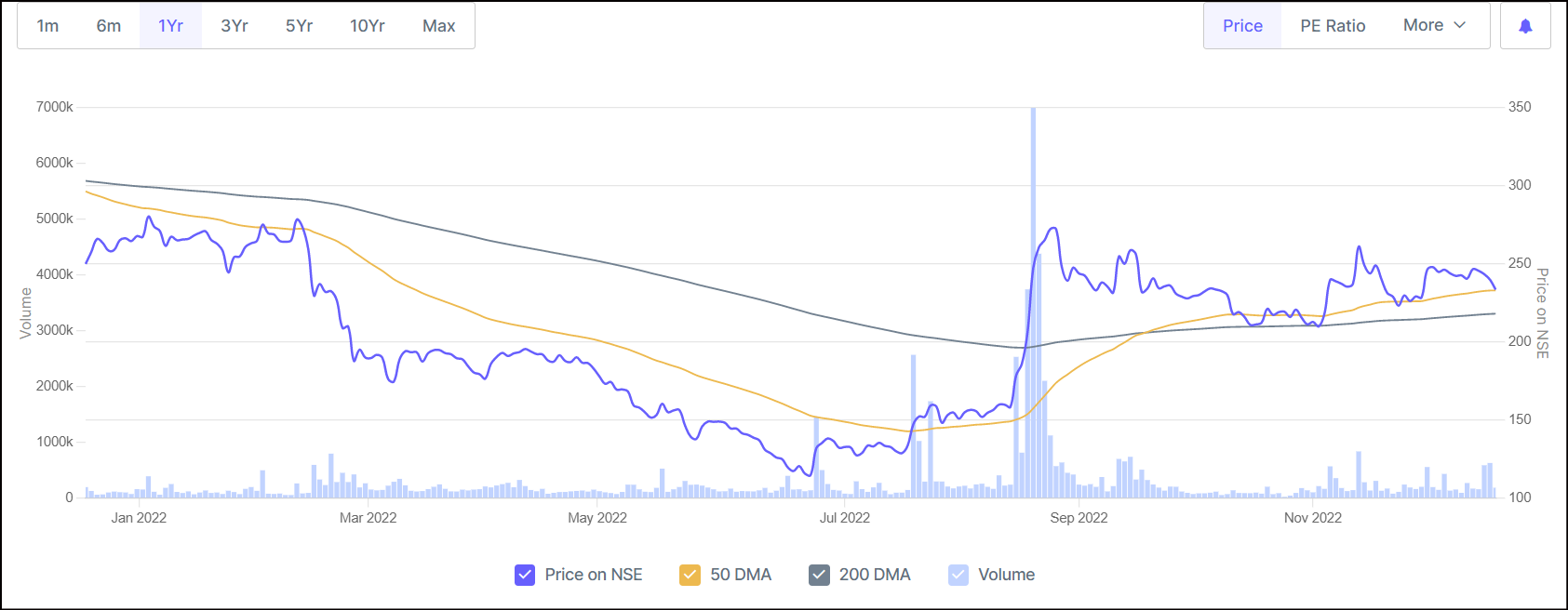

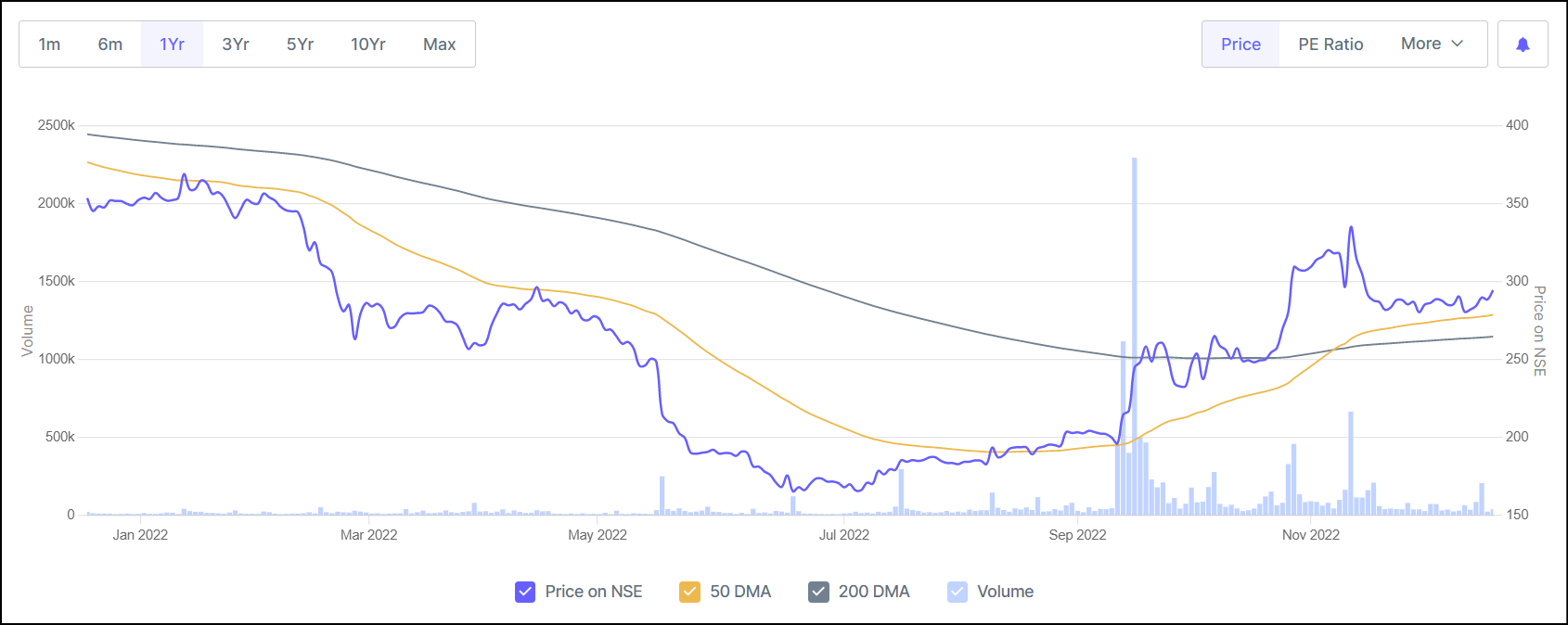

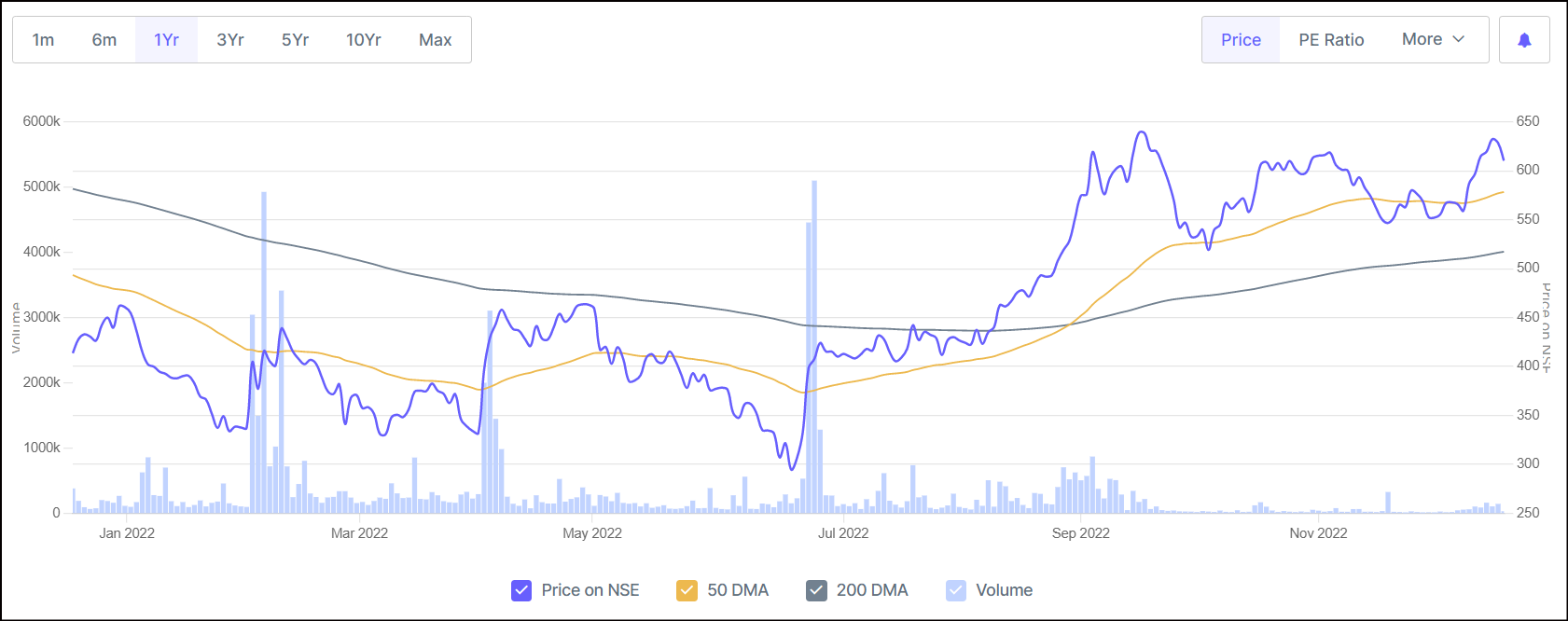

Would you please share your thesis on suryoday? I noticed it due to recent breakout and now trading above 200 DMA first time after listing. However I saw today promoter holding came down due to main promoter selling.

JLG Defaults - They acquire customers and make collections via joint liability group meetings. During covid, they weren’t able to conduct any group meetings. This was made worse by the fact that people within the JLG who defaulted on loans during covid pressured others into not paying.

Small collection team - To keep costs low, they ran a small collection team. This was fine when they conducted group meetings, but when the meetings failed, they did not have enough people to chase customers.

Concentration in states worked unfavourably - The states with highest exposure had the lowest collection efficiency during the covid recovery.

What’s changed since?

Two of the issues above have been addressed over the last six quarters by completely re-evaluating their collection strategy, and disbursements away from JLG.

Ultimately, the thesis was that if the macro in the MFI sector was good, they’ll be able to make recoveries from their customers, and these have already been written off.

Given that the NPAs were akin to PSU banks, I did not size more than 2-2.5% of my portfolio. When I bought at a share price of 100, it was at 0.7x book. With the market now chasing after various financials, the worst lenders have been the ones to outperform.

I’ve really been enjoying myself over the last three days.

Many companies in my watchlist are now falling into a window where valuations are attractive enough to warrant a position.

In the last three days, I have done the following:

Friends have pointed out to me that post merger book value is closer to Rs. 45. Stock has corrected around 20% from my exit price, and I have bought 3% worth of Equitas SFB at 51.

Have initiated a 1% position in Fusion Micro Finance at 360 per share. I re-iterate that I’m not a fan of IPOs, but this is a company in the MFI space that can do 4.5% RoAs and is currently at 2x book. If they maintain the run-rate seen in H1FY23, it is currently available at a PE of around 10.

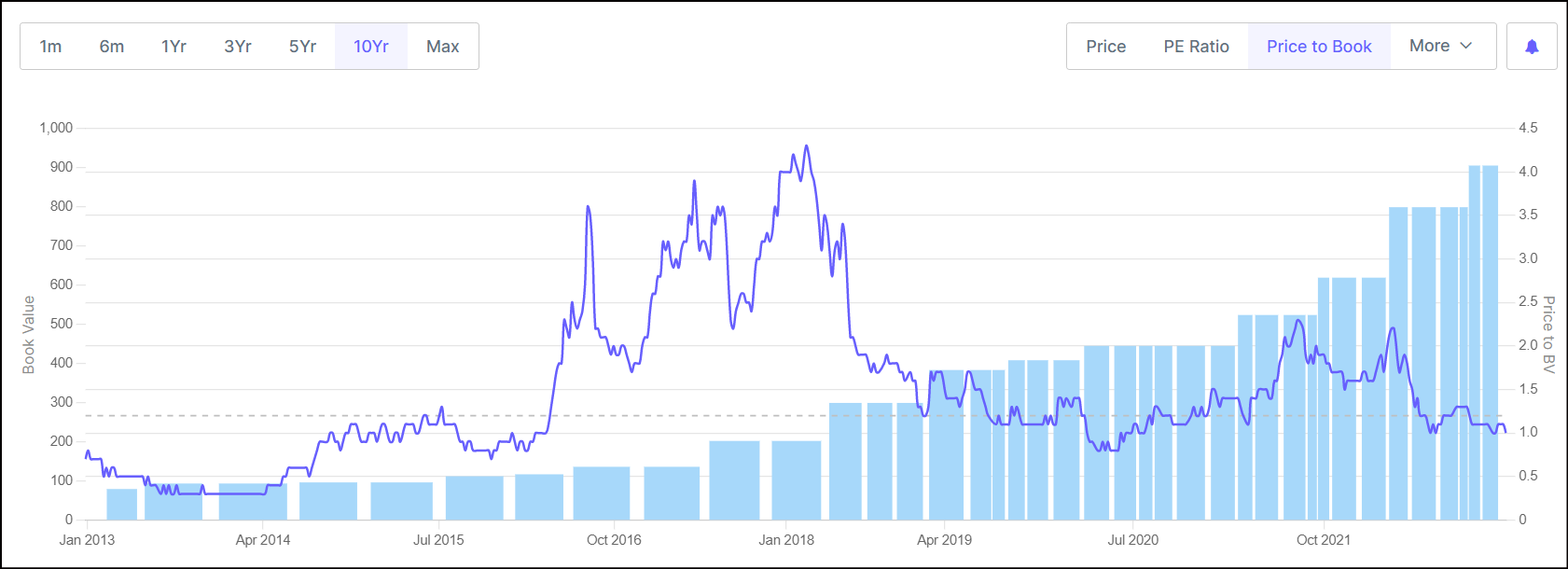

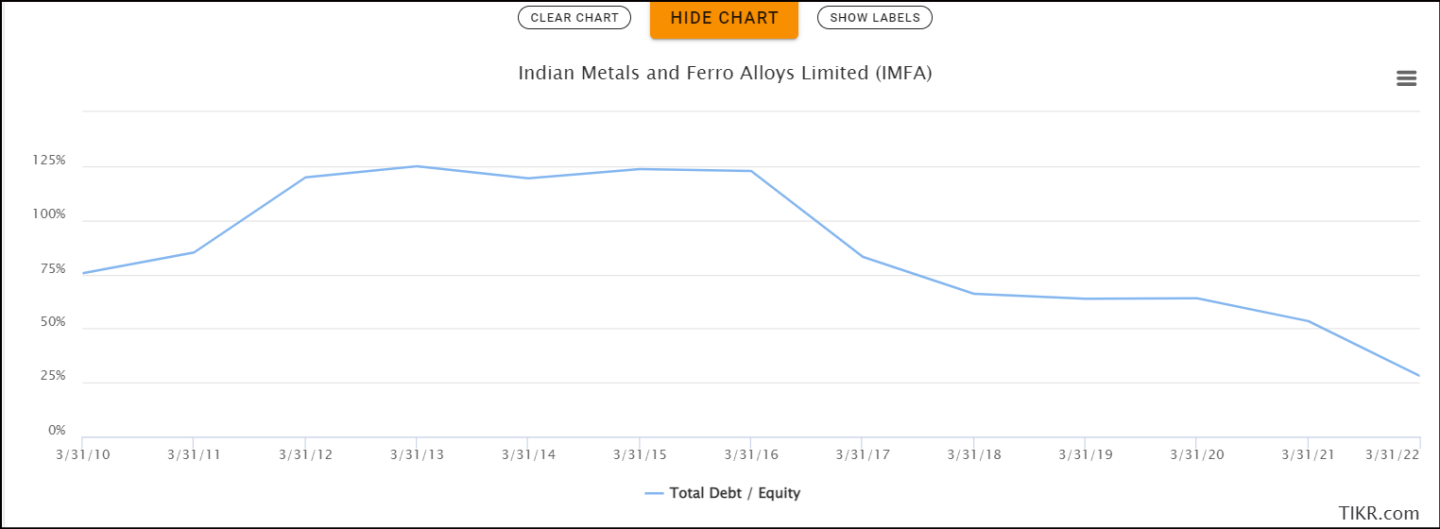

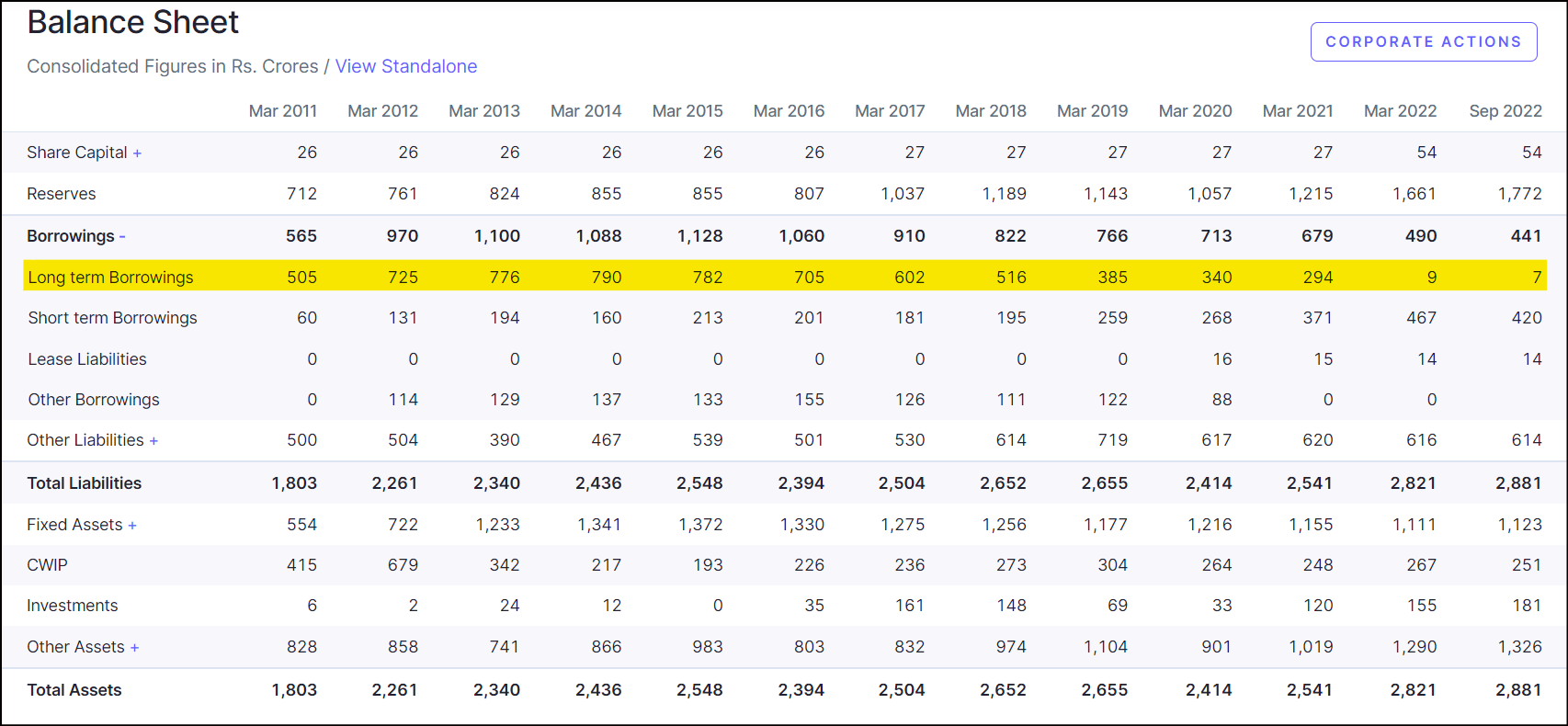

I have bought a 3% basket of Maithan Alloys and Indian Metals and Ferro Alloys.

Thesis for Maithan is just that it’s currently at book value, and has not broached this level after becoming debt free. There is no trigger on the upside presently, and I’m using it as a proxy for cash.

Now as of September 2022, they’ve paid off all of their long term debt, and after looking more closely at what their short term debt is, one realises that they’re in fact debt free. This means book value should be the bottom, unlike the downcycle valuations of the past.

My basket of Maithan and IMFA is a proxy for cash, and I’ll be raising my allocations in this basket through next week.

Have bought a 2% position in Sharda Cropchem. It’s an exceptionally good business that’s currently trading almost at lifetime lows that were only broken during the initial covid drawdown:

Based on the above, the bottom for their margins was already made in Q1/Q2, and things will improve from here. It’s a really high quality business, and I’m happy to scale up allocations here to 5% if valuations remain where they are.

Currently have around 14-15% cash. Looking forward to more blood on the streets.

Hi love your detailed styling of investment thesis and have added the style of sales/marketcap and other ratios before picking a swing trade

On this topic do look at valiant organics,It is the biggest producer of chlorophenol derivatives which is used in dyes, pharma ,pesticides and currently the dye industry demand are facing headwinds according to the management.Overall i feel this is extremely undervalued there is promoter selling which has taken the stock prices to lowest when we look @ marketcap/sales.i feel the selling is mainly by 1 family and there are multiple famlies in the group and if you read the thread the promoter holding is quite high.Also cagr and recent capex in current valuation are just icing on the cake.

Disc invested ,would love to hear your views about the company.

I want to highlight my journey in 2022, and what’s driven me to the 50/50 approach in my portfolio.

At the beginning of the year, my “low churn / long term” portfolio looked like this (post from Jan):

Had I not actively managed my portfolio, and taken the call to remain passive, the year would have ended in disaster, at -6% returns, despite the unrealised returns looking really good at the time.

This is not an argument that passive investing doesn’t work, it’s just that this particular portfolio would have been the wrong one to construct.

However, I became a better investor over the year, and changes to my style were for the better:

I subsequently sold most of my highest conviction/allocation ideas from the start of the year after realising the holes in the thesis, or the unsustainability of earnings. Laurus was sold in July at around 525 per share, Deepak Fert was sold at around 920 per share, and PDS was sold recently.

All of their earnings still look good, but price action suggests the market expects softening in the quarters to come.

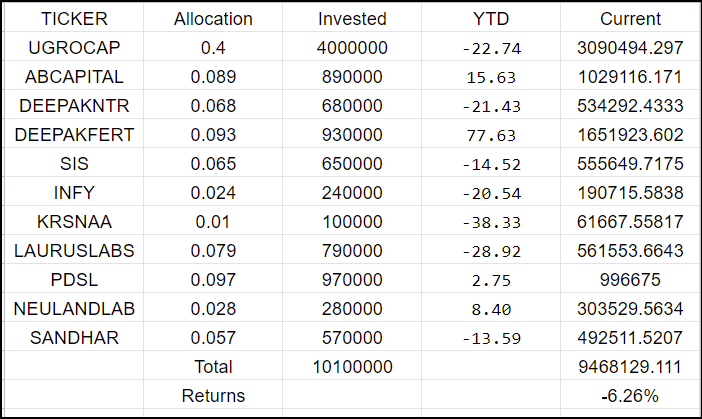

Ugro, which still remains my highest conviction investment had a horrible 2022:

Using market volatility, and booking profits with a high churn has helped generate returns where my two largest allocations have significantly underperformed the market: Ugro is possibly the only financial stock that has not participated in the rally over the last 3 months. Krsnaa has taken a beating along with the other diagnostics companies.

There are 80 companies above 800 Cr. market cap that have generated >100% returns YTD, but there are 200 companies that have generated >20% returns in the last 3 months. In other words, smaller movements in price happen more often, and are much easier to find.

If in the 50% of my portfolio that I allocate towards cyclical recovery, mispricing and swings I can generate a minimum of 30% returns, that will assure 15% returns in a year regardless of how my longer term ideas perform.

The more such plays one can successfully execute in a year, the higher these returns will be. My approach here is to categorise companies that I study/track into the quarter where I expect earnings to improve.

Also, having a cash position has helped me to deploy when there are fears on the market, and getting a really good price is half the work done. Purchases made last Friday are up between 12-23%. I have been harping about this approach in recent posts, but it’s where I’ve found most success till date, and suits my style.

Thanks for sharing. I do track valiant, and have taken up a position.

Hope everyone has a great 2023. Thanks for sharing your insights with me and helping me improve.

I think from here on out, I’ll only write update the thread quarterly, and when I’ve found candidates for the long term half of the portfolio.

Hi @Chins

Any updates on Sudarshan Chemicals. I don’t like pigment sections but two keywords attracted me here: cheap valuations & major capex completed and ramp-up coming in. Not forgetting the huge headwinds and debt laden balance sheet( had to sell land!!)

I’m also studying excel again but it feels like I’m going after Antony waste mgmt instead of a chemicals company(JK…)

I’m in the same boat as most people interested in this space:

Valuations of all dye/pigment companies have fallen, and it’s a question of timing when things will bounce back.

In addition to Sudarshan, Dynemic is also at attractive valuations, and I’m hoping it falls to 150-200 if the next two quarters are painful. I’m not doing anything special - reading what all companies in this space are talking about in concalls, looking at Indian exports of dyes.

Maybe a lot more groundwork is warranted in mapping out suppliers, and figuring out where earnings will bounce back, but I don’t have the bandwidth right now with the earnings season. Will write updates when I work on these companies, after earnings.

Post Q3 earnings season, want to share my current portfolio, and plan for each basket going forward:

Financials ( 40% )

Company

Allocation

UGROCAP

22.69%

SOUTHBANK

3.14%

SPANDANA*

2.36%

SHRIRAMFIN

2.27%

FUSION

2.22%

CSBBANK

2.19%

EQUITASBNK

2.13%

SBIN

1.97%

FEDERALBNK

1.76%

My exit for CSB is around 320 per share, 2x FY23E book value of around 160.

Federal Bank and SBIN are proxies for cash. Federal Bank is currently at 1.3x FY23 book, my plan for an exit is around 1.7x book.

Fusion and Spandana are very interesting to me right now. Fusion is currently at 1.9x FY23 book and is a 4.5% RoA business. Spandana has gone through a very large reshuffle and a lot of drama over the last 6 months. Now it’s available close to FY23 book value. Exit price for both depends on how long good times continue for the MFI industry, and whether they can partially bridge the valuation gap to CreditAccess.

Metals ( 10% )

Company

Allocation

IMFA

4.27%

SANDUMA

3.48%

SHYAMMETL

1.45%

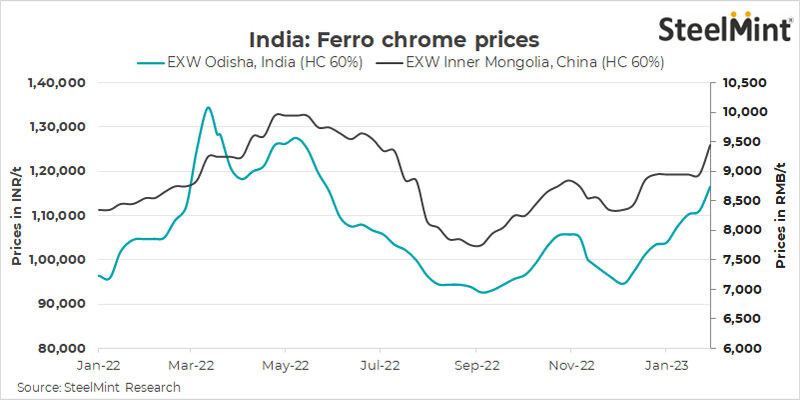

In this pack, higher allocations to IMFA have so far paid off. I am up around 25% on my average, and the ferro-chrome index signals that the next quarter should be a good showing. Looking to exit at around 350-370.

Sandur’s EC has come through for a huge expansion, and results should start to look better from here on out. The stock story is a great read on VP.

Shyam Metallics was once the case study used in conjunction with Godawari Power, as listing valuations for Shyam were very expensive compared to GPIL. Since then, it has corrected tremendously, and is now around book value. With a few large expansion works finishing 8 months early, valuations in Shyam are now attractive. I will be increasing my allocation to around 4% over the next week.

GPIL posted a good set of numbers, but they’re currently shutting down their sponge iron plant and completing some upgrades. My hope is that the share price will fall back to around 300-330.

Healthcare (10%)

Company

Allocation

KRSNAA

7.55%

CAPLIPOINT

2.86%

Have done a lot of work on Caplin Point in the last few months - they have executed their scale up in the US very well. Volume growth in Caplin Steriles has been exceptionally strong, at a CAGR of 34% over 3 years, and revenue growth is even higher as newer molecules have far higher realisations than older molecules like Ketorolac. Steriles currently has losses of 25 Cr. on the books which will cause a free swing in PAT through Q4 and FY24. Aside from this, Caplin has multiple triggers over FY24, and is trading at a discount to historic valuations. This is the third time I’ve owned Caplin Point since 2020.

Chemicals (15%)

Company

Allocation

FLUOROCHEM

4.23%

SHARDACROP

4.18%

ULTRAMAR

2.73%

VALIANTORG

1.79%

PUNJABCHEM

1.76%

At the behest of VP collaborators, studied GFL during the last month and I understand why the story is this exciting. New age fluoropolymers have much higher realisations than legacy products, and supply scenario in Chinese fluoropolymer producers suggests a favourable cycle for refridgerants. Overall, it is a very complex story with many moving parts. For such complicated companies, I need multiple quarters to better understand everything, and will scale my position accordingly.

Valiant Organics is now a turnaround story, and margins should recover as their chlorination vertical sales normalise, and the dye industry recovers.

I would like to scale Punjab Chemicals to 5-6% of my portfolio over time. Expecting Q4 to be flat, with multiple triggers in the future as they move to more complex chemistries, and scale higher realisation molecules. The thesis is an eventual improvement to 18% margins and beyond, coupled with 20% sales growth.

Components (5%)

Company

Allocation

SBCL

4.56%

XPROINDIA

0.78%

I think there will be many opportunities to scale Xpro India to around 5% of my portfolio over the next six months. The next 3-4 quarters should be flat on PBT from the Biax division, and the Coex division is seeing a slight decline in revenue. However, they did not pay any tax in the last 3 quarters. As they will now be paying tax, the swing in the PAT will make earnings look weak until the Biax capex comes onstream. I think it is currently at a one year forward PE of 25, and should hopefully correct.

Kriti Industries has seen incredible volume growth in Q3. The agri-pipes sector has seen muted numbers since covid due to the pandemic, and subsequent high price of PVC. This is now being resolved, and I expect blockbuster numbers for Kriti in Q4 and Q1 as the demand carries over into their seasonally strongest quarters.

@Chins : - Hv u exited frm Sandhar Tech completely??

Apologies if u hv mentioned this in the thread earlier as I followed u frm Sandhar thread and havent read this pf thread in detail.

Why I find it undervalued - Though the mgmt has been aggressive in guidance, with majority of new plants capex behind thm and TVS + Honda projects lined up for next yr, don’t u think nos. nd margins vl start to improve frm here on??

The mgmt guided 30% rev. growth in next FY, If we take 25% on this yr’s base plus EBITDA margin in double digits owing to operational leverage - The co. is at 3.5X EBITDA.

Yes, I had worked on Sandhar a lot in the past. I was invested in Sandhar, but decided to switch into SJS Enterprises for two reasons:

It is in the bracket of auto ancs with the highest gross margins, seen in this post:

I am fairly confident that the standalone entity for SJS can maintain 30% EBITDA through most business cycles, and therefore the cyclicality for SJS is in the topline, not the margins. Sandhar went through a particularly bad pain period for margins in the last 3-4 quarters in comparison.

For these reasons, I thought SJS should command higher valuations, and I had bought into the company earlier at around 360-380 per share, and then got a very nice exit a few months later.

Now if it falls below 400 I’d be happy to pick it up again.

This is an excellent thread and I regularly learn from it. Churning on Caplin three times in 3 years approx. is too much don’t you think. What I am trying to get at is, once you build the conviction is it only till you see the cycle turn? Aren’t you afraid that at some point the combination of churn and a bad investment will take down a significant part of your portfolio?

Sorry if those questions are too direct, I am just trying to learn from someone who I think is better at investing than me.

Thanks

This thread captures my journey in arriving at better ways to think about businesses. The first time I owned Caplin at the start of the thread, my investing process was to sit on Screener, find a high growth/high RoCE/high quality business and invest. Some of the posts from the first year of the thread are unrecognisable to me.

The second time I owned Caplin, the process had become following business updates on concalls, reading every inch of an annual report and I thought I was on top of the business by doing this.

In hindsight, the problem with both of these approaches is obvious. With high RoCEs / margins it’s more likely to be the result of a favourable cycle than a consistently superior business model. I now work a lot harder for all of my companies to find out how much is being driven by realisation trends and map out the supply landscape with as much granularity as possible.

I now think my equating concalls to staying on top of the business was a large error, and gives one an illusion that a thesis is intact. The market knows a whole lot more between quarters. For export facing companies for example, the market knows exactly when a large shipment has been made, when realisations are falling, when companies are going to have a poor quarter, and in most cases, this is reflected in the price.

Now, on the third time owning Caplin, my investing process is a lot more scuttlebutt based - I try to talk to 1-2 industry experts a week, talk to many different stakeholders in the value chain and try to nail down the industry landscape, competitive advantages and map out supply. My investing is a lot more collaborative now, and a lot of this work is not mine alone, but has come out of working with fellow investor friends.

It depends on the business. There are some I’d like to hold across cycles, and those I’d prefer not to. If I had to place companies I’d like to own for a longer term into brackets based on my understanding of the business, it would look like this (non exhaustive):

Tier 1

Tier 2

Tier 3

Krsnaa Diagnostics

Punjab Chemicals

Caplin Point

Ugro Capital

Shivalik Bimetals

Fluorochem

PDS Limited

Here, I am confident I have a very differentiated understanding of the companies in the first bracket.

Krsnaa and Ugro I’d like to own across multiple cycles and are examples where the answer to your question is no. With Krsnaa, I have a higher confidence that we’ll see a good cycle for 5-6 years. I sold Punjab when it looked like market was pricing in a little more than what would come in the next two quarters. I have recently bought back in. With PDS, the earnings still look good, price action doesn’t indicate anything is wrong, but I think there will be pain reflected in the next couple of quarters.

Aren’t you afraid that at some point the combination of churn and a bad investment will take down a significant part of your portfolio?

The current process has come from my mistake in Strides. From here, if I make a bad investment in my core holdings, it shouldn’t come from unknown supply risks, a sudden turn of the cycle, etc. My hope is that it’ll be from a new gap in my understanding. So I’m not scared.

I’m however going through a phase of buying junk businesses when valuations in the companies I follow aren’t attractive enough, and then going back up the quality curve in broader corrections like we’re seeing now.

Lets see. The goal is to become better every quarter, and to add more companies into the tier 1 bracket with time.

Thanks for the reply and for being honest, really appreciate it.

This is where investors like me will get handicapped as we don’t have the time or the execution skills to pull off scuttlebutts. In the long term (8+ years) I’d want to analyze how much of a lift did your non-core holdings give your portfolio. If you already have an answer from someone you follow please let me know. I hope its in the range of 5% CAGR.

This was such a good comment and we all relate to it so much.

Best of luck and you are getting better. On top of it all you are also making this community better.

Thats very intriguing.

I used to select companies in the same way by looking at screener Sales CAGR, Profit CAGR, price CAGR, ROE, ROCE…but since these figure are compounding numbers, some 2-3 years good numbers make the long term average good and similarly 2-3 years bad numbers make longbterm average look bad. This will inevitably make us to choose companies with good recent performance and to avoid those companies with latest bad performance. How can we see each year’s performance independent of CAGR influence? So that we can seperate out consistent performance from one-off good performance?