This worked out well -shared at 700.

Went up to 2100 and moved downwards.

This worked out well -shared at 700.

Went up to 2100 and moved downwards.

Blue jet healthcare - Not sure about the legality of posting charts after latest SEBI regulations, so sticking to only discussing fundamentals. There isn’t much in the chart anyway - it looks overbought on the daily and is in fact bearish.

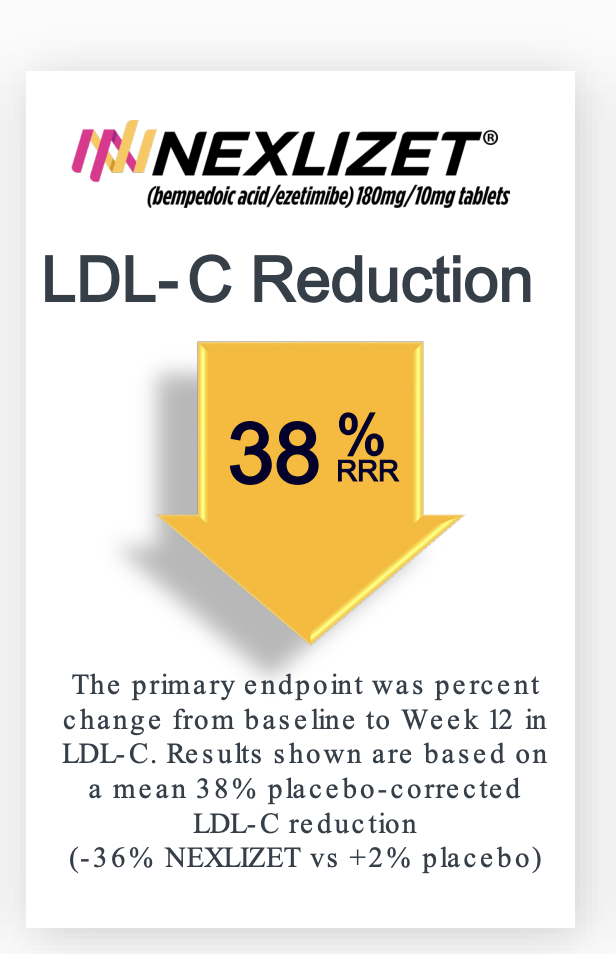

What got me interested was the breakout growth, in revenues, profits, margins - so the obvious question was - is this lumpy one-off or is this sustainable? The growth is coming from an intermediate used in the manufacture of bempedoic acid which is used for lowering LDL-Cholesterol, just like statins. What’s also nice is that this isn’t some generic drug but is an NCE (Innovator: Esperion Therapeutics) which is seeing breakneck growth. The drug is sold as Nexlizet (Bempedoic acid and Ezetimibe) and Nexletol (Bempedoic acid) in the US and as Nustendi (Bempedoic acid and Ezetimibe) and Nilemdo (Bempedoic acid) in Europe. Daiichi Sankyo has license to manufacture and sell in Europe.

The US prescription growth is great even on a quarterly basis.

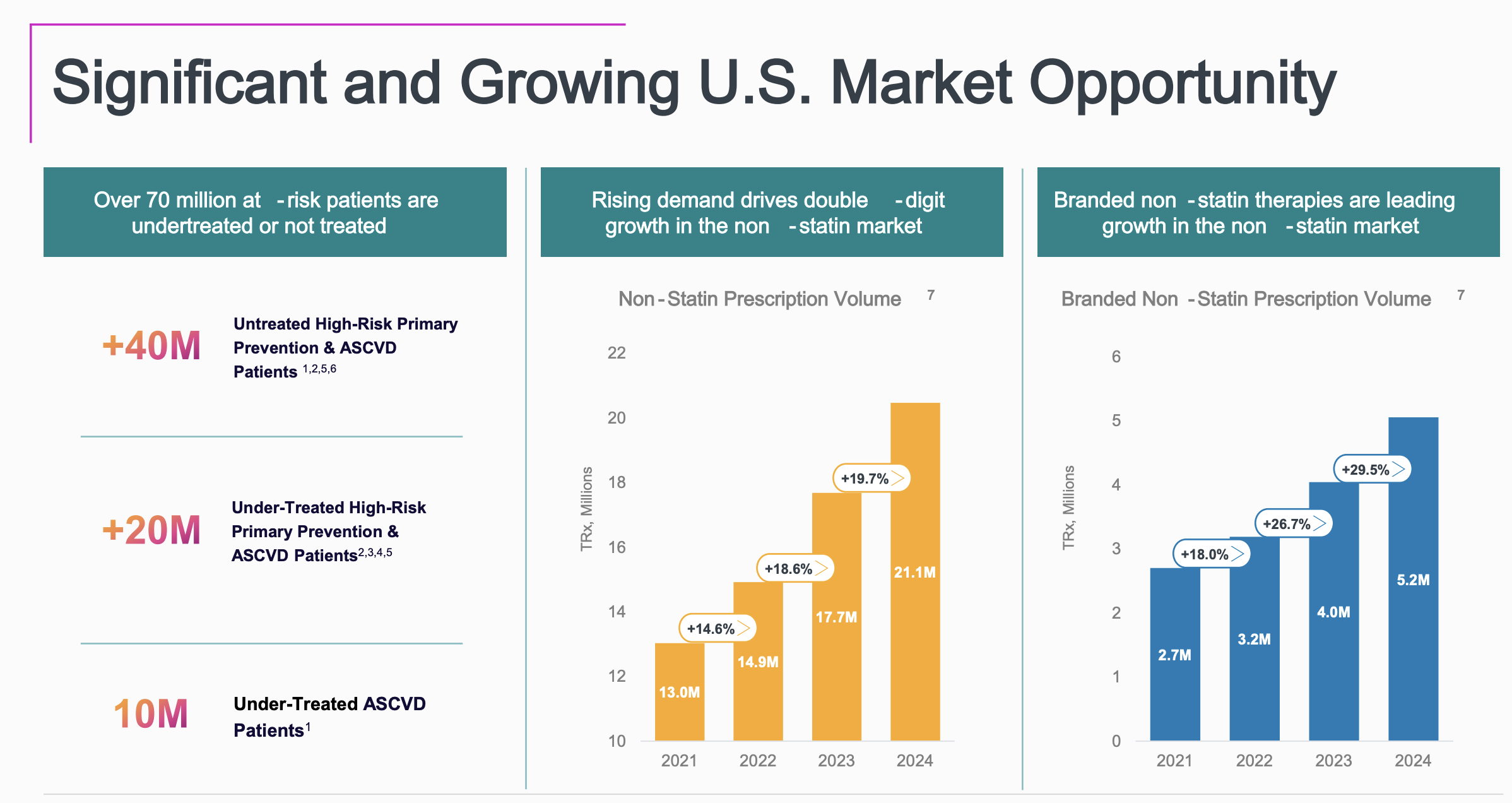

The overall TAM is 70 million patients in the US alone after the expanded label usage granted recently.

The non-statin growth has been strong due to multiple factors from statin-intolerance to side-effects of memory loss and muscluloskeletal issues.

Nexlizet’s LDL-C reduction is comparable to statins and looks like docs are prescribing it alongside statins as well going by this podcast

Currently PCSK9 inhibitors seem to be used in cases with high LDL-C as a non-statin treatment. This itself (Repatha and Praluent which are mAbs) is a $3b market which a oral drug like Nexlizet can challenge. Insurance coverage as well is there for these drugs.

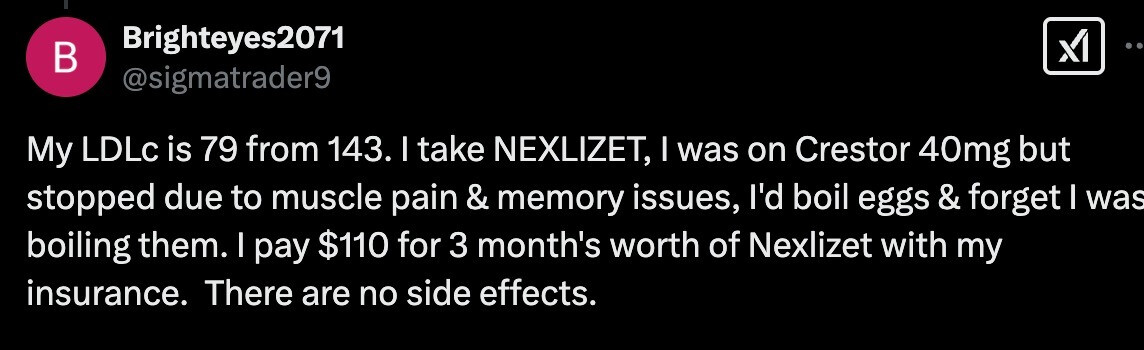

A real customer’s usage I saw on X.

The book “Ten Drugs”, talks about how statins were overprescribed and how Lipitor revenues soared to a cumulative $120b between '96 and '11. This is unfortunately how healthcare works which is an indicator for how Nexlizet prescriptions might go - its in stage 1 of Seige cycle (concept from the book of how uptake for drugs goes from Stage 1 to 3)

If the current rate of growth continues, there’s scope for a 500 Cr PAT in another 3-4 quarters.

There are some other triggers in the Contrast media business but they aren’t as exciting. (There’s a gadolinium based NCE called gadopiclenol for which Blue jet will supply intermediates from this quarter)

Risks:

Disc: Invested around 800-820.

Credits to @aga.ayush11 for digging deep on this one

Thanks a lot @phreakv6 for sharing your views. If I understand you are invested in Onesource as well (I guess you got demerged shares of Strides). Will you continue holding it or sell it? If holding, what do you think about the future prospects and current valuation? I am particularly interested in this because of their presence in GLP1 drugs.

Strange that the innovator Esperion Therapeutics is trading at $300M market cap on nasdaq while Blue Jet is trading at more than $1.5B market cap

Thanks @phreakv6 for spotting this and for your detailed analysis. The earnings call commentary made for an interesting and positive read and the company financials are robust. Seems expensive currently, but like you have said, the growth trajectory appears to be strong.

@24comlb, It looks like Esperion has faced high commercialization costs (sales force ramp up probably the main item but maybe there are other costs too) in the US as they have increased sales there. In Europe, they only get royalty as they have out-licensed to Daiichi which manufactures and markets it there. They have also licensed to other partners in Israel, Japan etc. If the drug continues to do well, their royalty payments will increase and presumably their US commercialization costs may stabilize too. Could be a good bet for those who buy US stocks, but probably needs to be studied further. Maybe it will take longer for them to turn profitable if there are other factors at play.

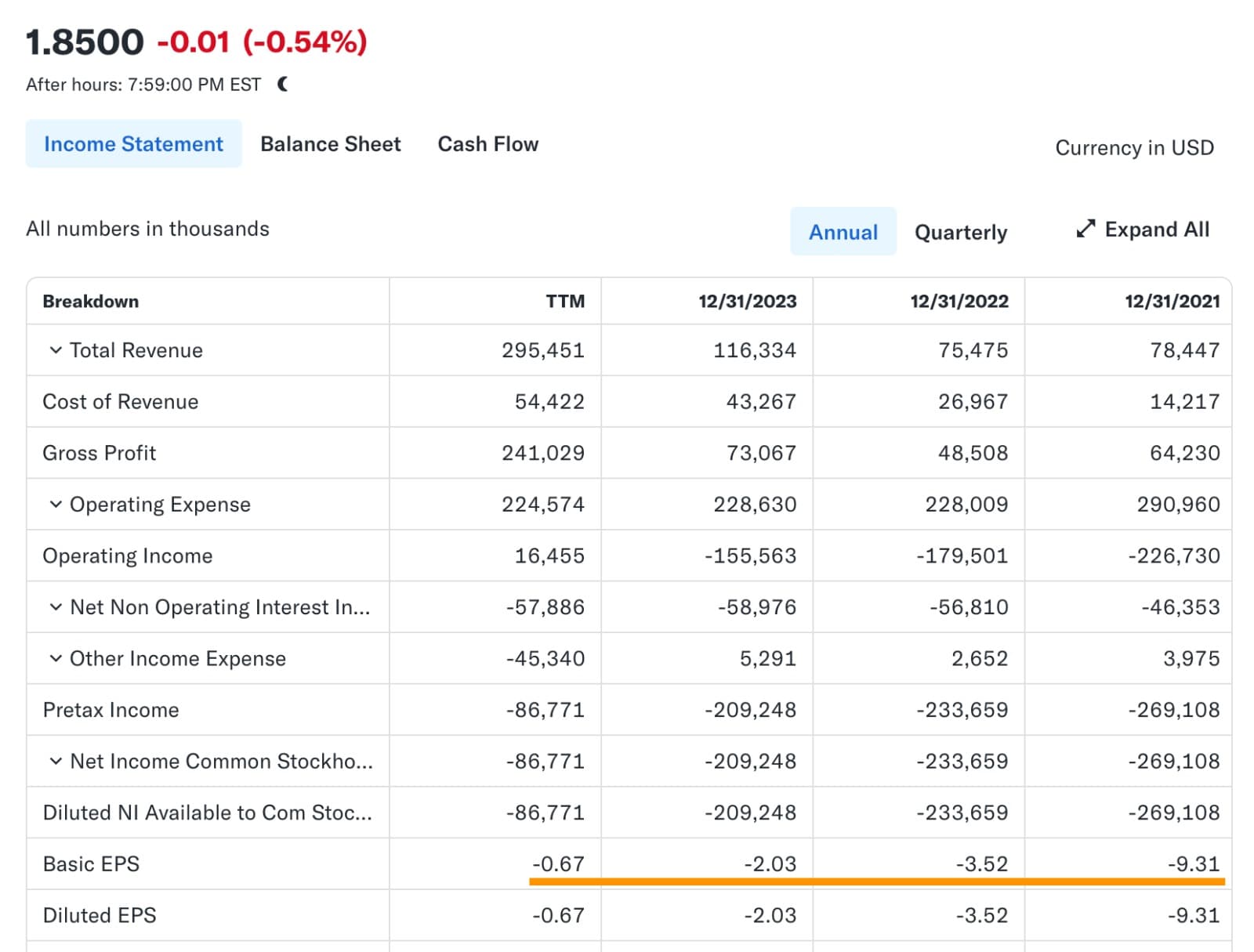

Here is the last quarter’s update by Esperion.

Great learning new things via ur posts

Ten Drugs

Typical life cycle of blockbuster drugs in three phases:

![]() Stage 1: Discovery & Early Adoption – A new drug is introduced, often with excitement and aggressive marketing. Sales grow as doctors start prescribing it.

Stage 1: Discovery & Early Adoption – A new drug is introduced, often with excitement and aggressive marketing. Sales grow as doctors start prescribing it.

![]() Stage 2: Widespread Use & Peak Revenue – The drug becomes mainstream, generating billions in revenue. Pharmaceutical companies push it heavily, and prescriptions soar.

Stage 2: Widespread Use & Peak Revenue – The drug becomes mainstream, generating billions in revenue. Pharmaceutical companies push it heavily, and prescriptions soar.

![]() Stage 3: Saturation, Decline & Resistance – Side effects, competition (generics, new drugs), or shifting medical guidelines slow down sales. Sometimes, lawsuits or safety concerns emerge.

Stage 3: Saturation, Decline & Resistance – Side effects, competition (generics, new drugs), or shifting medical guidelines slow down sales. Sometimes, lawsuits or safety concerns emerge.

![]() Example:

Example:

As per my channel checks in US in some pharmacies, as of now doctors are writing this molecule who has Adverse drug reactions with statins. Insurance coverage is less as of now. Any new product insurance coverage will take some time, I hope coverage part will get better that will increase prescriptions.

I was interested in the GLP-1 fill-and-finish as well which was why I bought before the demerger but it was not a big position to start with. Post demerger I sold Strides and wanted to hold Onesource but was surprised to see the promoter selling Onesource. In this market these sort of deeds at least put an intermediate top on the price. Along came Bluejet around the same time and I found it reasonable to switch.

Yes it is cheap any which way you look at it. I had shared this with a friend who invests in US markets few days back to have a look.

As of now they are serving probably somewhere between 0.25-0.5 million patients and when they reach a million patients, they should achieve a $1b in sales which will make it a blockbuster drug. At that time I wouldn’t be surprised if they achieve $1 in EPS which means they are trading at a P/E of 2. Japan/Canada markets are yet to be accessed as well on top of this. But then I dont invest in US markets and these sort of loss-making biotech are a dime a dozen there and of late looks like big pharma is looking for molecules in China since its cheaper there which is bound to derate US biotech further. But still knowing the molecule in the last week or so, I believe ESPR should do well too. No reason why Blue Jet shouldn’t do well as well (Varun Beverages and PepsiCo is a good analogue to this arrangement - VBL continues to do well for a bottler and has $20b mcap against $200b for PepsiCo though it has bottling rights for a fraction of the regions PepsiCo sells in while holding no patents)

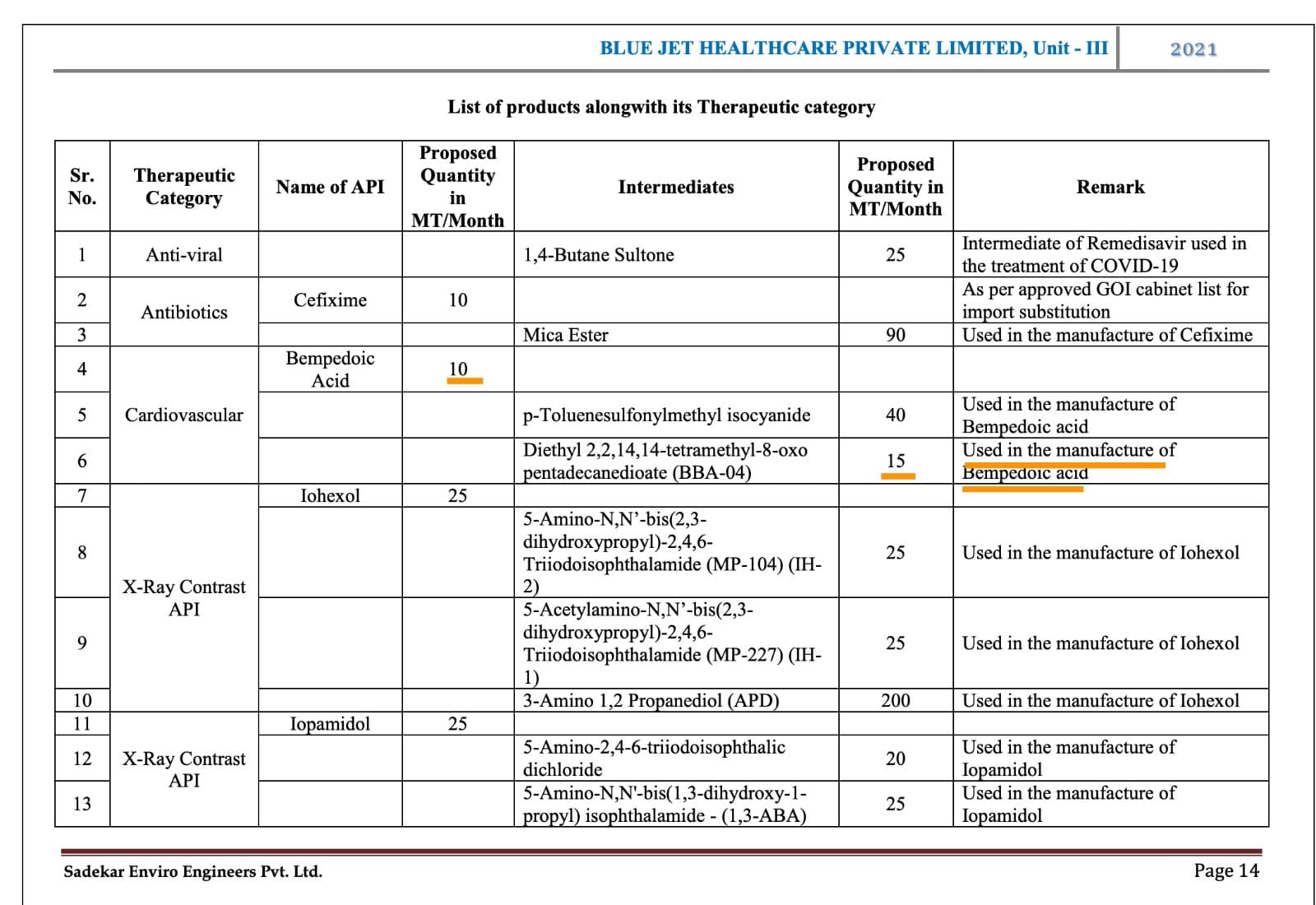

Since the last post, @aga.ayush11 @ganeshrpl and I found some more details. The EC for Unit-3 of Blue Jet shows intermediate capacity for Blue Jet at 180 MTPA (15x12) and they even have a sanctioned Bempedoic Acid capacity of 120 MTPA (which clearly is not operational as yet)

Debottlenecking this 180 MTPA is how they are probably going to double it to 360 MTPA going by the concall.

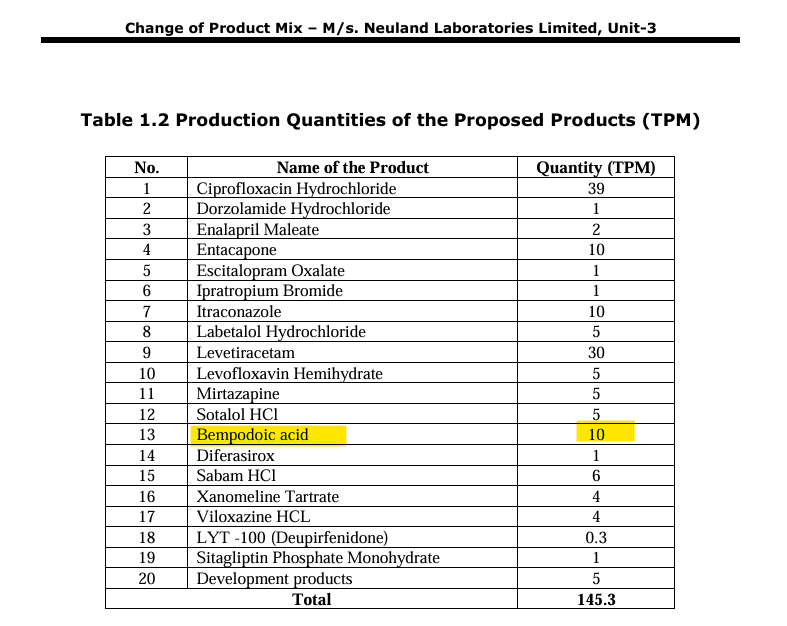

To put it in perspective Neuland has a sanctioned capacity of 40 MTPA (109.6x365) of Bempedoic Acid as per EC. As of now Blue Jet has a much larger intermediate capacity and also has BA capacity which isn’t put up though they have clearance.

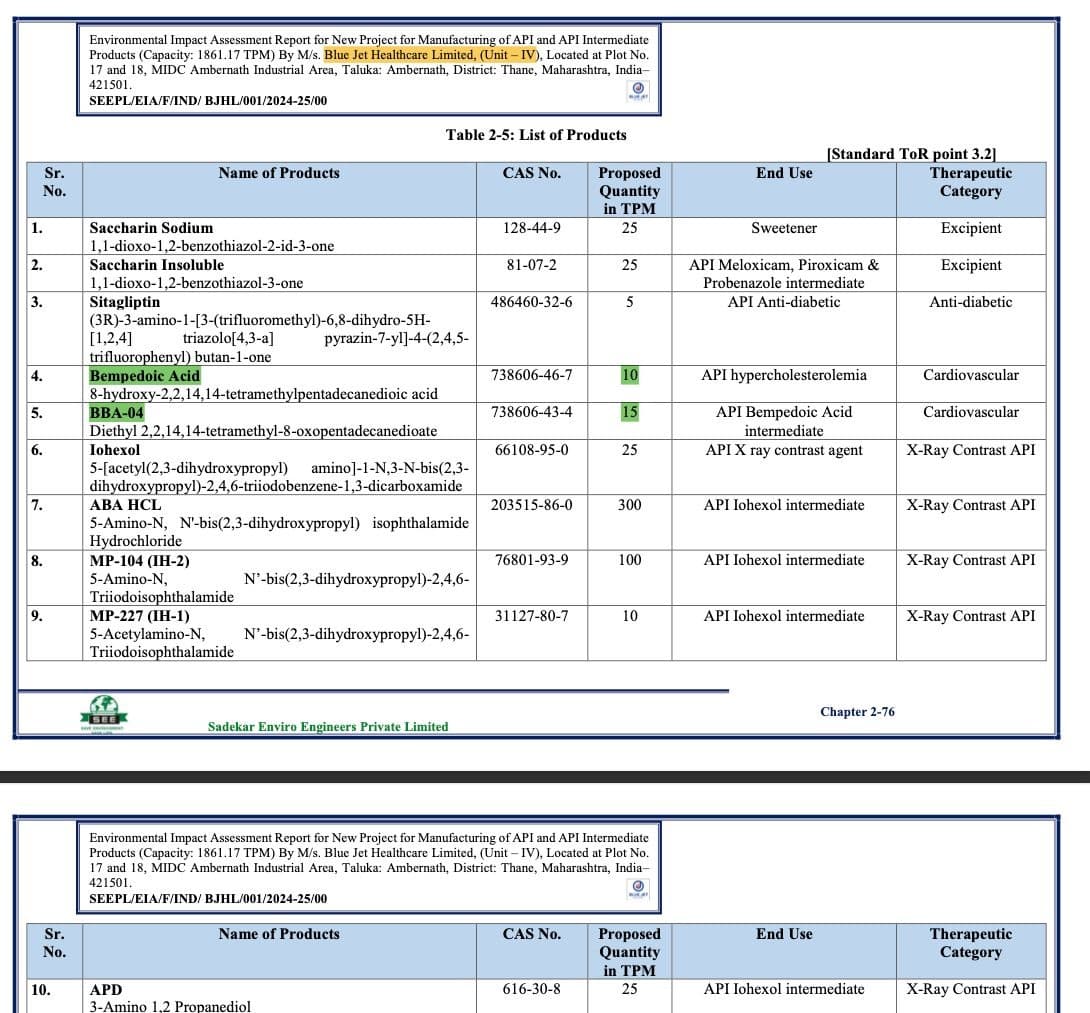

Other interesting thing is Blue Jet also has applied for EC in Oct '24 for Unit-4 to expand BA intermediate (180 MTPA again) and also BA itself (120 MTPA).

Why would they expand in Oct '24, that too double their capacity in a new unit while debottlenecking current capacity to double it already, if they didn’t have good visibility as of Q3? To me, it gives me confidence that Blue jet may have hit something big here. However, its better to wait a quarter or two until clarity emerges on what Neuland really has, as the molecule scales. Even if it does have additional capacity (there’s no EC we could find other than the 40 MTPA they have), there’s no reason why Blue Jet at least do as well as it did in Q3 and do a 500 Cr annualised PAT in FY26.

Disc: Invested and have recent buy transactions, so I am bound to be biased

What can be the affect of reciprocal Duties in US on Indian Pharma Companies? Will reciprocal duties make China Pharma product cheaper compared to India? or will China have even higher duties which will not affect Indian Pharma?

Veterans kindly share your thoughts…

NEXLIZET and NEXLETOL are indicated:

The bempedoic acid component of NEXLIZET and NEXLETOL is indicated to reduce the risk of myocardial infarction and coronary revascularization in adults who are unable to take recommended statin therapy (including those not taking a statin) with:

As an adjunct to diet:

Thanks @Meetkatrodiya . Can you please post a link to the doc?

So it looks like Neuland’s expanded capacity could be 120 MTPA + current 40 MTPA = 160 MTPA in bempedoic acid. Blue Jet’s intermediate capacity of 180 MTPA would cater to a bempedoic acid capacity of 140 MTPA (Assuming 1.3 ton of n-1 for 1 ton of bempedoic acid). So total expanded capacity would be 300 MTPA of bempedoic acid (before Blue jet’s debottlenecking effort to increase capacity that is).

Now lets convert this to number of patients who will be catered to. Each patient takes 180mg of bempedoic acid per day - Assuming zero wastage between API → formulation → fixed dosage - this means 1 MT of BA API should cater to…

180 mg per day x 365 days = 65.7 gms/yr per patient

so 1 MT or 1000000 gms works out to 1000000/65.7 = 15220 patients/MT

(Please note this is too simplistic and conservative as there is bound to be wastage due to variety of reasons)

So based on today’s capacity of Neuland at 40 MTPA + Blue Jet’s 180 MTPA of intermediate (140 MTPA of BA probably at Fareva) - 180 MTPA translates to 2.7 million patients.

Putting this 2.7 million patients in context - current patients are likely around 650k as of Dec '24 (We don’t have Esperion’s Dec '24 number as earnings not out for quarter - I have made an educated guess based on RPE growth as per Corp presentation in Jan '25)

Since BA’s intermediate would take 9-12 months to end up in retail shelves, its likely that Esperion is planning its supply chain a year ahead based on expected growth. Going by the growth post label expansion, just in current markets of US and Europe, we should see doubling to 1.3 million patients by Dec '25.

Throw in Japan where they should start selling this year and in the near future in Canada and Israel as well. We should also factor in the fact that Esperion hasn’t been able to grow in US market meaningfully so far (Jun '23 revenues in US and Europe were same $20m - today its $61m in Europe and only $34m in US) probably due to issues with insurance coverage, a lack of marketing efforts (having been embroiled in a legal tussle with DSE) - this clearly has potential to grow 100%+ YoY just like Europe, especially since ~30% of the US market is statin intolerant.

Also whatever capacity is being put up is to cater to demand for next 2 years in a scenario of expanding market and expanding acceptance of the drug which should lead to exponential growth and we are probably only at the cusp of the initial stages of the S-curve right now. Along with debottlenecking and a corresponding expansion at Fareva and with Neuland’s expanded capacity, we should have capacity to cater to 6 million patients at peak utilisation, 2-3 years from now. This is not a commodity and there’s only one buyer in the market and all capacity is put up based on order backing and visibility.

Blue Jet might make hay next 3 quarters with debottlenecking until Neuland’s capacity comes online which means 150-160 Cr sort of PAT for next 3 quarters which may drop off a bit after that but even in the worst case scenario the 100 Cr PAT per quarter Blue Jet posted in Dec '24 remains the base case assumption for me and is what we should work with, to be conservative.

The biggest risk is drop in prescription growth which needs to be monitored every quarter. The best case assumption is at least 15-20 million patients on the drug across markets (US, Europe, Japan, Israel, Canada) in 3 years which would be a 25x growth in patients from here.

Disc: Invested

Will these materials (Bempedoic acid or an advanced intermediate) attract tariffs in US. Trump is talking about tariffs on pharmaceuticals. How will this change the numbers of profitability?

Wondering whether blue jet or neuland would be able to maintain pricing power

Disc. Invested in blue jet from lower levels

Neuland Unit-3 EC

Unit 3.pdf (7.2 MB)

Some relevant data points regarding US patients on lipid lowering medication and trends therein

Given these data points which suggest that between 10-20% of patients may either be statin intolerant or unwilling to take statins and the CLEAR outcome trials which clearly demonstrate that bempedoic acid is able to significantly reduce risks of major cardiovascular events (MACE) in statin intolerant patients, it should logically follow that over time, at least 10% of the population which takes lipid lowering medication, should transition to bempedoic acid formulations. The current global statin market is estimated to be between USD 15-20bn.

They key takeaway by the American College of Cardiology on the CLEAR trial outcomes is summarised as below

Alternative treatment options like PCSK9 inhibitors are very expensive as compared to bempedoic acid, costing as much as 14-15k USD for a 3-month dosage vs as less as 150-600USD for bempedoic acid. Insurance coverage of bempedoic acid is also therefore naturally much higher than PCSK9 inhibitor therapy. As these findings seep through the medical community and the American Heart Association also revises guidelines to include bempedoic acid as a key therapy for lipid lowering, sales of the molecule should increase significantly in the coming years.

Disc: invested.

@phreakv6 , A great admirer of your thoughtful analysis, combining fundamental as well as techical analysis. Also timing for such investment entry is picture perfect timing.

In terms of Bluejet (BJ) analysis, in view of present market correction, Neuland (NL) is also available at similar valuation range (TTM basis). To choose only one of it, I had some basic queries: (comparison between them)

NL has failed multiple times and after evoluation transformed in present form, vs BJ a recently listed company in blockbuster drug development space. Further, FDA history, compliance track record, and vintage (old is gold) in terms of quality of management - critical factors favoring NL IMHO.

Also risk management point of view, haven’t studied BJ in detail, but too much dependence on particular family of drugs vs pipeline of many drugs, and clear visibility of growth vs expectation of growth.

one more overhang - in terms of 1-2 year position building for BJ, 86% promoter holding, and supply of 16% shares would be an imminent overhang on share prices.

Not an expert on the sector, and have very limited pharma business understanding

really appreciate investment philophy of @phreakv6

This is key to the prospects of Bempedoic Acid. Being a practicing Physician, present understanding among medical fraternity is as follows…Clinical studies have demonstrated that bempedoic acid effectively reduces LDL-C levels. When used as monotherapy, it achieves a reduction of 17% to 18%, and when combined with ezetimibe, the reduction increases to about 28% in statin-intolerant patients. Experts express caution due to potential side effects, such as hyperuricemia and an increased risk of gout and tendon rupture in susceptible patients. The present view on bempedoic acid is, as a valuable addition to the lipid-lowering drugs, especially for patients unable to tolerate statins. Its market potential is significant but may be limited by its current positioning as an alternative rather than a replacement for statins.

US Food and Drug Administration (FDA) approvals for Bempedoic acid have been fast. This may be because the promoters are pushing it hard!

●In February 2020, the FDA approved the drug as an adjunct to diet and statin therapy for the treatment of adults with familial hуреrϲhοlеѕterοlemia or established atherosclerotic cardiovascular disease who require additional lowering of ԼDL-С.

●In February 2020, the FDA approved a combination of Bempedoic acid and ezetimibe.

●In March 2024, the FDA expanded the above indication for Bempedoic acid to include use of the drug without statin therapy in statin-intolerant individuals in primary and secondary prevention of cardiovascular disease.

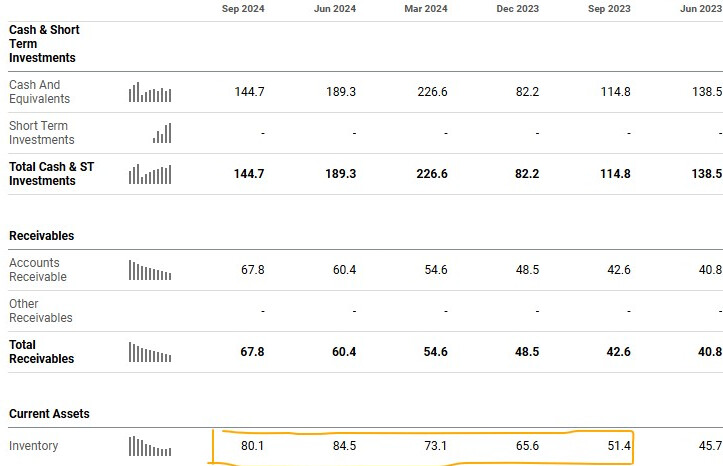

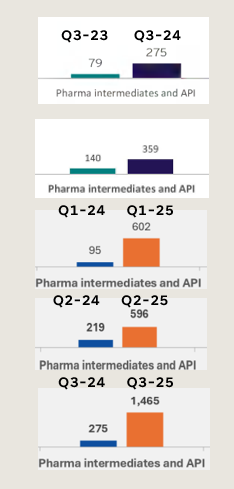

My apologies if its naive way of looking at this aspect, I wanted to understand if the Esperion inventory trajectory matches with supply of Bempedoic acid from BlueJet, following are two images

which shows supply from Bluejet, and reported inventory from Esperion.

Trajectory of Blue jet supplies of intermediate ![]()

Inventories at Esperion ![]()

I am unable to correlate the qoq inventory build of Esperion vs supplies from Blue jet

Is this an appropriate way to look?

I’ve been tracking BlueJet, Neuland and esperion since March 2024 and invested in Esperion since May 2024. Here are some key observations:

Once Daiichi has its own manufacturing supply chain, BlueJet’s revenue from intermediate will depend on Esperion’s performance in the U.S.