AllyGrow Netherlands is almost offsetting the profits of Allygrow Technology private ltd.

Your thoughts ?

@Maheshcm - Yes, you are right. Allygrow isn’t at that level of expertise as their rev/employee also indicates. AllyGrow is 16 lakhs/emp and AllyGram I think was 25 lakhs/emp if I remember right, as compared to KPIT’s 40 lakh/emp or so.

@ankit_tripathi - If I remember right from the AGM, this is a one-time hit for something that happened in the past (dont quite remember)

Some broad market views I was thinking of today.

Nifty, Monthly

Getting back into the wedge. The month of course isn’t over yet and we have 3 more trading days. If Nifty manages to recover to 19300 odd levels, we could have a strong rally next month. If not, and if next month tests 18300 levels (bottom of the wedge) unsuccessfully, we could have a rising wedge breakdown, which is a common pattern. In fact these sort of rising wedges are bearish setups. Similar setup on the weekly with just 1 trading day left (tomorrow) shows this bearishness is more or less likely, barring a miracle

Midcap 100, Weekly, Similar distribution and breakdown on the Nifty Midcap 100 index as well. 7 weeks of sideways movement has given off this week.

Smallcap 100, Weekly - This was the original chart I shared on Sept 1st week. There is confirmation of the breakdown this week though this went sideways for 7 weeks since my post.

The microcap chart is the best of the lot. It is yet to even take support on 20 WMA.

Liquidity clearly is strong in the micro/smallcap space going by the relative strength they have shown. The concern I have is that, these can catch up much faster to large/mids when they start showing weakness.

The past 7 weeks offered some good bets which had valuation comfort like Shilchar, Garware, Goodluck, PDS, Ceinsys which worked out well (Swelect, Mazda which didn’t) but I am not comfortable initiating fresh positions if market conditions deteriorate further now that there is confirmation, as compared to my speculation in Sept 1st week when bullish fervour was high. We will have clarity once week and month finishes. It is strange though culling a pf which is doing so phenomenally well.

Disc: Back to 35% cash and will reduce further once I have weekly/monthly confirmation. Still have positions in all names mentioned but at reduced allocations and bullish to that extent

53 Likes

Most of the results are out and overall pretty good performance

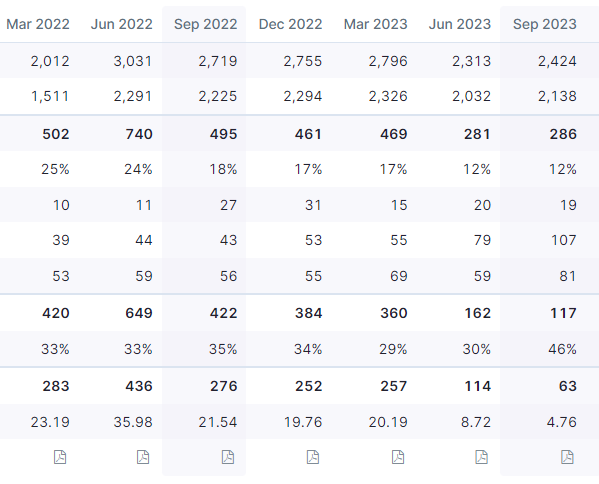

Shilchar - Phenomenal performance and probably the best of the lot from the pf. There’s also possibility of domestic contribution this quarter as the numbers arent fully accounted by just growth in exports. At current levels though good numbers are discounted for the next few quarters. The promoter too seems to agree and has been selling.

It is generally hard to make great money when promoters are selling. I am not sure who is buying though at 2800 - could be FIIs, as it happened in Apar. They pay very little heed to valuations - a mistake us small retailers cannot afford to commit. I think at 2800 this is a very risky buy. I have been selling and intend to hold around 3% as an investment position.

Garware - The PPF contribution is going up and the 118% utilisation and long-term contract with XPEL are all great signs. The drop in IPD revenues played spoilsport though (32% decline in revenues) and so the numbers appear flat. It is however surprising though that the commodity part of the business has performed poorly when Cosmo/Polyplex seem to have done better QoQ. I was expecting a explosive growth in earnings here like Shilchar, so it is a bit disappointing. Like Shilchar, I had big allocation here which I have been reducing due to valuations entering fair value zone (1500+). I will leave a 3% investment position when am done reducing.

I did not expect this sort of runup in Shilchar (doubled in a month) and Garware (50% in 2 months) so overall these two have been good trades. The momentum could very well carry them further in this market.

Goodluck - Pretty solid performance here too YoY. The big bottomline growth QoQ though is attributable to higher tax paid last quarter. This business seems to have lot of tailwinds and could continue surprising. I intend to hold on to this trade as is long as the tailwinds sustain

PML - Flattish, given the valuations and continues to remain expensive. There is also guidance of EV growth softening but smart-meter demand picking up in the note that came with the results. Maybe the two will balance out? They have also done capex for the alloys business to manufacture superalloys used in aerospace and defence. More importantly, looks like Quadrant JV too proceeding well and sales should start commencing from Q4. However they seem to be starting with magnetic assemblies and not manufacturing NdFeB magnets - which might be a good thing as it might be less capex intensive and probably make higher margins (hoping). This position has now turned long-term for me. The overall size of the position though has shrunk with the other trades in rest of pf working out better

Mazda - Pretty good growth here too but margins are lower compared to last 3 quarters and continues to remain cheap (now trading at 16x). Food business seems to be ramping up well. I think margins here will continue to improve as utilisation goes up.

Ceinsys - Pretty good results. The receivables situation seems to have improved too. This reminds me a lot of my trade in AurionPro (somewhere in this thread) which is currently trading at fancy valuations. I didnt hold it long enough though as I had concerns on the business quality there (regular write-offs). I feel AllyGrow as a business deserves better valuations and so will hold and see it through

Swelect - The softening prices of modules and dumping from China has probably affected the numbers. Until there’s protection from dumping, am afraid this situation will continue. Its a small position I continue to hold to follow if situation changes - especially if policies favor the manufacturers in MNRE approved ALMM list

Taal - Breakout from long-term resistance and re-test.

The company now doesn’t do air chartering so its main line of business is Taal Tech which is a wholly-owned subsidiary of the company which will soon be merged with Taal Enterprises. So for all intents and purposes, this is now a Engineering services firm. The AGM transcript is a good read. They have about 60 customers and largely export oriented and margins are pretty healthy. Current quarter results are pretty good and valuation reasonable.

Overall this results season lot of businesses are doing quite well. A lot is being priced in though with lot of small/microcaps trading at even 30-40x and some SMEs are at stratospheric valuations. We can’t fall into the trap and storify liquidity driven price runups though and indulge in BaaP behaviour (performance of Marcellus’ little champs portfolio is a good reminder of what happens when we do)

I am ~30% cash so views could be somewhat bearishly biased. It helps me stay hungry and look for good bets (selling in Sept 1st week was what led me to buy Shilchar for eg.)

Disc: Have positions in Taal between 2200-2400 and the rest as disclosed in this thread and in this post. Not an advisor and I am just a novice sharing my thoughts.

65 Likes

Overall view of the market:

(Market Turned bullish after Shakeout)

The last two weeks were very interesting weeks with lots of results and the market made many to turn bullish. (who turned bearish in Sept-Oct). ( I am also one of them. P:)

Above is the weekly chart of SmallCap 100 showing classic patterns with a lot of details.

Last two weeks price action was based on earnings and overall the earnings were quite better than expected. I consider (may prove to be wrong) this price action strong as it was based on strong results with all the uncertainties of war in the Middle East.

Also, by just looking at the technicals, ignoring all other facts, There was a heaving breakdown of the chart but took the support of 20 EMA and bounced back quickly.

Clearly, a shakeout move on the Index, and this move is visible on a lot of stocks so this was market-wide making it a strong comeback.

After coming back to the small box range, It spent a week there and then this week a breakout of the Range. A classic continuation of the uptrend.

Now What’s Next:

Most probably next week there will be the continuation of the uptrend in the market …but … but if there is a fall again in the range box then there will be a long pause before.

So, for me, this is not the time to sit with cash as I can see what is happening and have to make decisions based on that and not by predicting what can happen.

Here are a few of the Stocks on my radar

Now that the direction of the market is decided for me, it is time to select stocks.

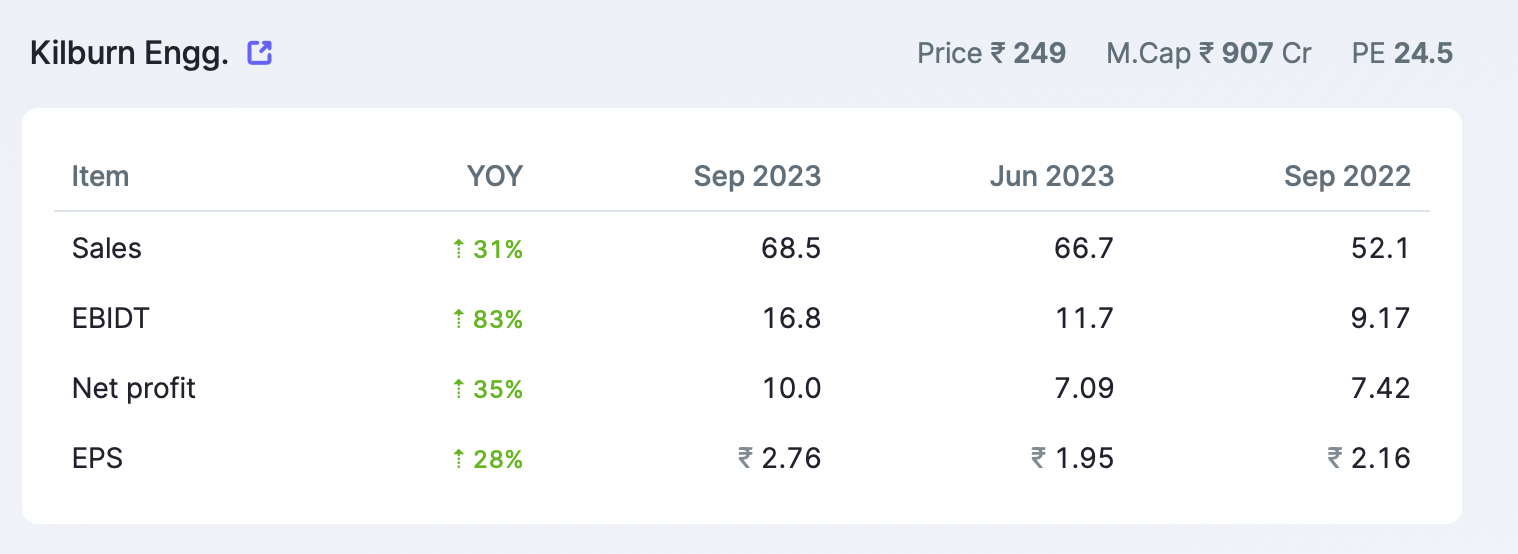

- Kilburn Engineering Ltd: The company manufactures equipment/systems for critical applications in several industrial sectors like Chemical, Steel, Nuclear Power, Petrochemical and Food Processing, etc. The company came out with good results

A proxy to capex in many sectors including oil and gas, pharma, chemical, petro, Carbon Black, metal, etc.

They have proposed the acquisition of ME Energy Private Limited which is in the segment of waste heat recovery These systems find application for thermal energy saving and/ or thermal energy cost reduction in almost all industrial processes.

What triggered me is that they are guiding for sales of Rs 500 cr by FY25 for the combined entity after acquisition. The current sales is approximately 250 cr, so effectively doubling in 1 and a half years or in 2 years. :

While current Qtr operating margins were 25% management has guided for 20% + margins for up upcoming few quarters based on the order book currently.

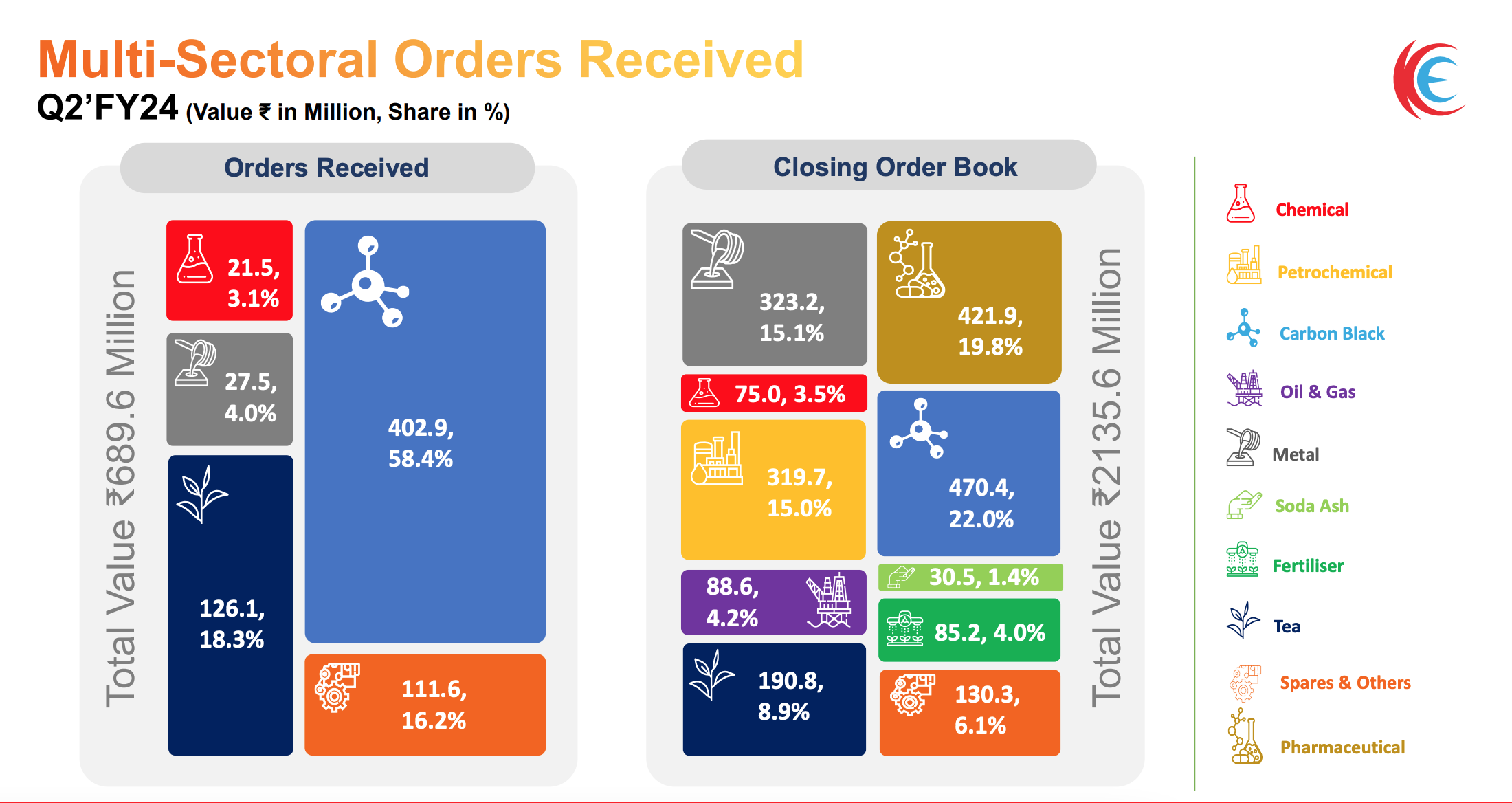

This is how the current order book of 200 cr plus which will be executable in the next 2 qtrs looks like

There are very few small-cap companies that have a 20% plus margin, which means that have some sort of capability and good value-added niche products.

On Charts:

Technically also the chart is breaking out from the upper trend line.

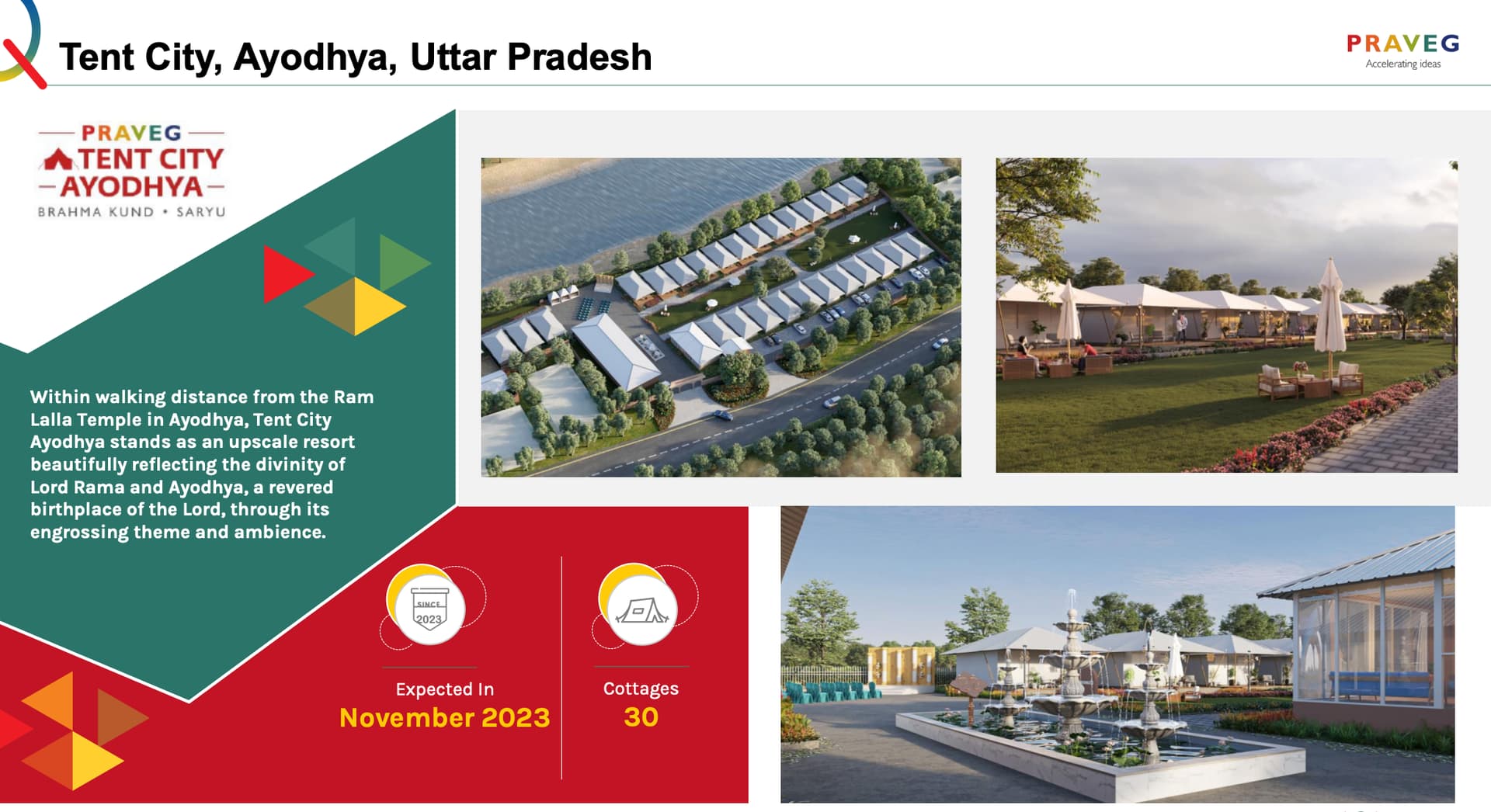

2. Praveg Ltd: Engaged in providing services to eco-responsible luxury hospitality. The Company’s resorts are located in areas of significance from a cultural and heritage point of view and places of exotic and natural beauty.

The company has a lot of upcoming plans. H2 will be stronger than H1 as most of the resorts have high occupancy in H2 due to the festive and holiday season. Also, the company is taking steps to reduce seasonality in H1.

So, the upcoming qtrs will be stronger than the previous two.

On Charts:

Trading near the breakout zone and had a very strong closing after a gap-down opening on Friday due to weak Q2 compared to YoY due to some upcoming work.

Clear Sign of shakeout.

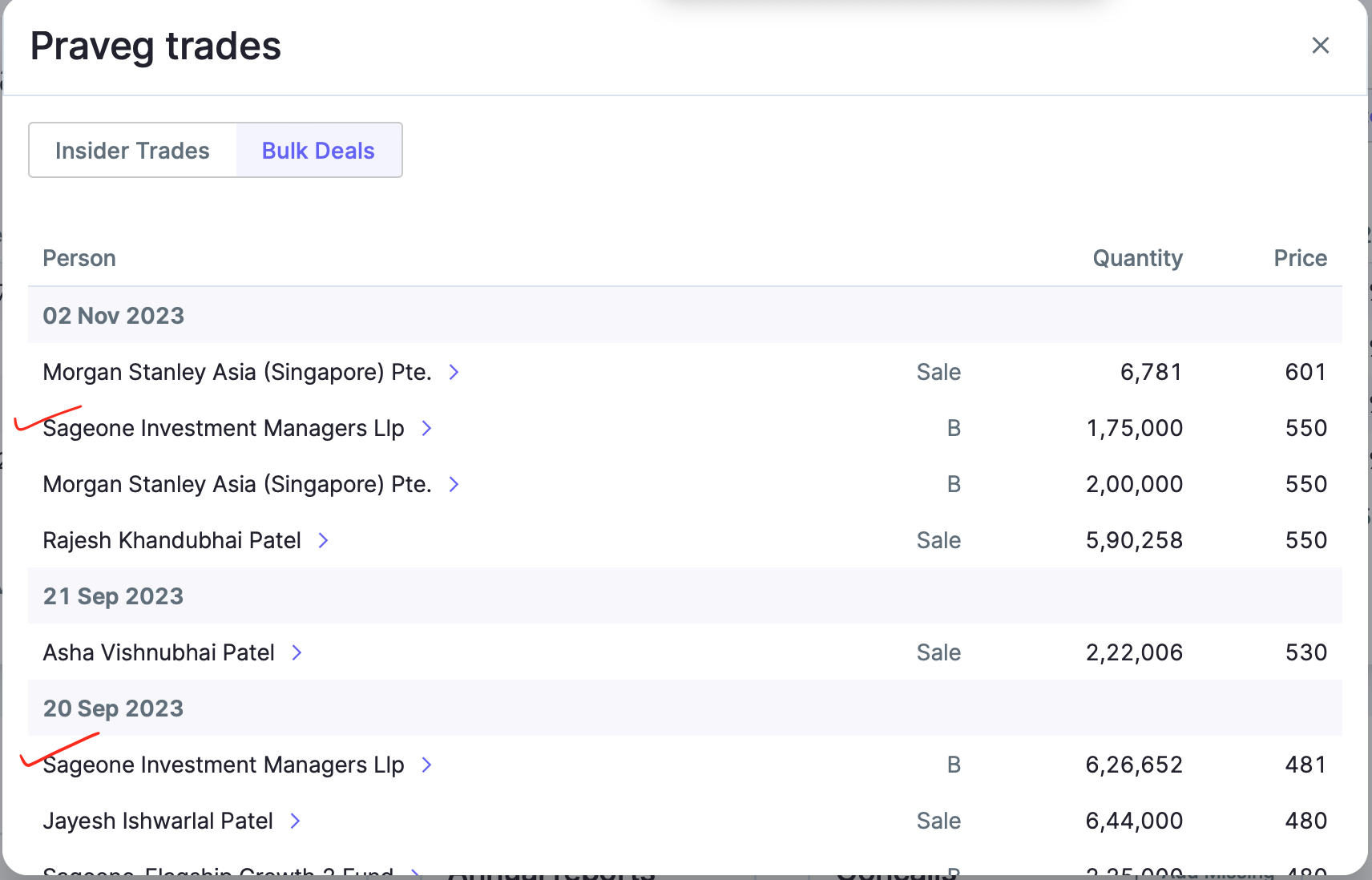

some interesting names in the recent Bulk trade of Praveg:

Buying by Sageone Fund (which is managed by Samit Vartak who is known for picking great stocks)

3. HBL Power: ![]() The results were very good and the sector is having strong tailwinds in its business. I am not following all those projections of analysts but the price action. Just ride the good stories with proper risk management because we don’t know how much it can rise from here with more value-added products coming from the railway and defense.

The results were very good and the sector is having strong tailwinds in its business. I am not following all those projections of analysts but the price action. Just ride the good stories with proper risk management because we don’t know how much it can rise from here with more value-added products coming from the railway and defense.

Before, the results HBL was in corrective mode and has corrected to levels of around 260 from highs of 310 but now again after the results the structure looks very good on the charts.

So, after a lot of consolidation, the price is above all its major (295) and minor resistance (310) and a good close on Fridays with volume greater than the previous weeks.

Price retested its support of 310 and also the result Gap is still unfilled thus making it stronger support.

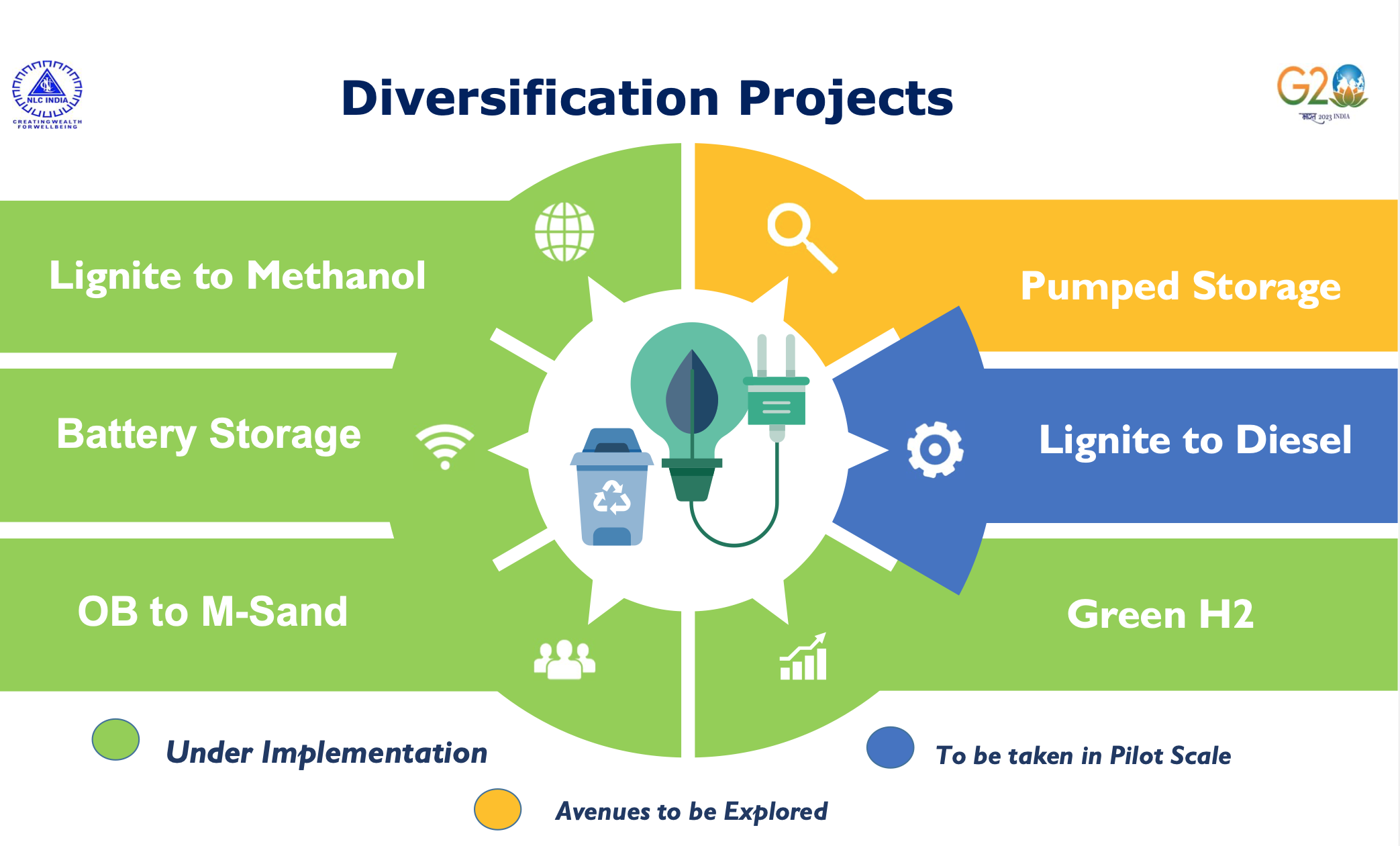

- NLC India Ltd: The combination of Mining, the power sector, and a PSU with low free float (Not like those PSUs with no profit in the last few years). NLC India is engaged in the business of mining lignite and generation of power by using lignite as well as Renewable Energy Sources.

Some of the Interesting diversification projects of the company

The public holding is continuously decreasing from 10% on Sept 22 to 6% on Sept 23. Showing institutional interest with DII holding increasing from 5% to 9% for a similar time.

Currently trading at a 13-year high zone with a retest of the breakout level of 115-120 on a monthly chart.

Stocks making multi-year highs must be on your watch list. and slowly build your position as the stock performs.

Disc: I have a small position in all of the names and planning to increase if the trade goes as expected. Hence biased. Just sharing my thoughts as a note to myself.

53 Likes

I am reading your threads for a while now and realize that valuation and charts are as important to you as anything else, if not the most important.

Do you have your eyes or views on Jindal saw which falls in that category and only at 12 PE till a couple of weeks back. I am specially asking you this since you discussed good luck.

A good candidate for rerating. at 97 RS on market smith, could be another doubler till March 2023.

5 Likes

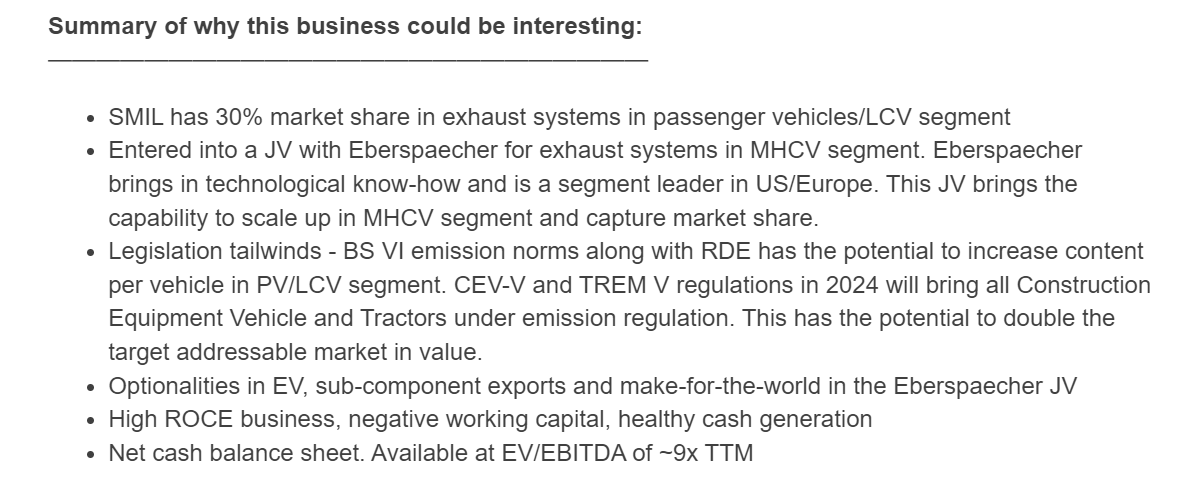

Sharda Motors, Monthly - Nice C&H breakout on the monthly. This has been a value buy for a long time but with growth in the future and not imminent. Now growth has also come in which is generally a potent combination

@manpritaurora and @nirvana_laha have done great work on the Sharda thread and I looked it back in Apr/May but gave it a pass with no immediate triggers. Now with numbers coming in and TREM V in the future, and chart setting up well, looks like its perhaps the right time.

Highlighting from the thread

Motilal Oswal Financial Services, Monthly - Getting out of the congestion zone around 1000-1100. Has done nothing in this raging bull market and has remained as a value pick.

Recent two quarters numbers are good but its not from durable streams like HFC and wealth management but from capital markets (FnO, Financialisation of savings) and Fund based activities (institutions raising capital) both of which are deeply cyclical so somewhat lower in quality IMO. But its perhaps cheaper than it deserves to trade at

Disc: Have position in Sharda Motors between 1100-1200 and MOSL around 1150.

37 Likes

Just evaluating the trades post monthly close. Some of the new trades from last 2 months are doing quite well.

Taal - Big breakout last month. Still considerably undervalued compared to other Engineering services firms. Taal Tech has respectable 40L rev/emp and exceptional margins. I feel compared to Tata Tech listed valuation (its rev/emp is 45L and a margin of 20%), this still offers great margin of safety. The hiring in recent months has been quite strong (EPFO) and is infact probably depressing the margins (should hopefully get back above 30% when it normalises). Compared to IT services businesses ER&D and Engineering services clearly is showing strong uptick in hiring and growth and should sustain due to the high wage inflation in Europe and US.

Ceinsys - The business has been winning and renewing orders in its geospatial and IoT business for Jal Jeevan and State water sanitation missions (SWSM). Ceinsys probably has a rev/emp of around 25L while AllyGrow likely tops 50L (And likely does 30% margins). Here again the engineering services division should grow strongly and the geospatial division is seeing strong revival with govt. orders in Jal Jeevan (both have strong tailwinds). Valuation remains cheap even post the strong breakout and consolidation.

Sharda Motors - Pretty strong breakout on the monthly as anticipated. Remain cheap still and hopefully should sustain the run

MOTILALOFS - Good breakout from the congestion zone around 1000-1100. Did a re-test of 1100 odd levels during the month and the shakeout should help contnuation of the trend. Still remains cheap

Holding most of the rest (PML, Goodluck, Mazda) as is and reducing Shilchar. Took a few new small bets in Wockpharma, Eimco Elecon and Electrosteel castings (EDIT) to delve deeper. First two especially appear quite promising. Wockpharma has been restructuring its business (it has no choice) and is betting big on WCK5222. Numbers may not come until FY26 but if they manage to raise money for phase 3 which appears very promising, can run up in anticipation. Its perhaps a good turnaround bet. Eimco Elecon, since govt is planning to increase underground mining by 3x and at the same time also planning to cut down on imports of equipment. Eimco is also doing well in diversifying its business away from Coal mines (mining of metals) and also into construction (piling rigs). These two appear the most promising in terms of triggers and valuations but over the medium/long term.

The GDP growth (13%+) in manufacturing, infra and construction clearly shows where the fish is - most of the bets that have worked well this year have also been in these sectors. This tailwind should hopefully continue. Engineering services too clearly has a strong tailwind due to wage inflation in the west and could be a trend that could sustain for sometime

Disc: Invested in the names mentioned and not qualified to advise

54 Likes

Electrocast as in Magma Electrocast or Electrosteel castings…

1 Like

Inox did pretty well at 350++ as on date

My next stock is Deepak Fertilizers

- 500 is a strong support and 500 was also their 2017 all time high, so big support + we have the 200 DMA at 500.

- After consolidation between 500 and 600 now 600 is turning to be a strong support, above 700 we can se big move.

-

Last 2 quatres we can see horrible performance at PAT levels but I believe that the uptrend in share price would start once we see YOY PAT growth which as per me should happen from Q3 or Q4

-

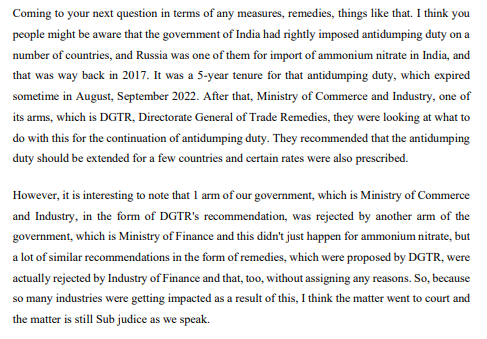

To explain them in short TAN is one of their most profitable segment and TAN is made from Ammonia, the company took huge debt and set up an ammonia plant to do backward integration but 2 months back ammonia price were at all time low.

-

TAN prices are artificially low, there is a ban on export which got lifted recently but the permissible limit to export is still very low + there is a huge dumping going on. So complete lift on export or an anti dumping duty is a trigger. (this is just an add on positive which can happen but not major one)

-

Ammonia prices have been rising and rising ammonia price = rising TAN realization. Based on Q2 ammonia price shared by the company(current might be even higher) they are saving 90cr to 110cr at EBITA level on a quarterly basis.

-

TAN volumes are extremely strong plus the company took 260cr of one time impact on their inventory on fertilizer segment because of subsidy reduction by GOI.

So they had ammonia price hitting all time low 2months back, TAN realization very low, subsidy impact from fertilizer segment, incremental depreciation from new ammonia plan started last quarter + incremental interest cost + interests rate pretty high + they also took a one time loss of 80cr in Q2 for plant stabilization (Everything has gone wrong for them in last few quarters)

Despite this they are showing strong support and I see lot of triggers going forward. My detailed post on them is here Deepak Fertilizers and Petrochemicals - #252 by manhar

H2 I am expecting things to improve drastically especially from Q4 onwards, I see 50% to 70% upside in next 5 to 6 months conservatively

Disc- invested, avg 650, can be wrong and will exit if things go wrong

25 Likes

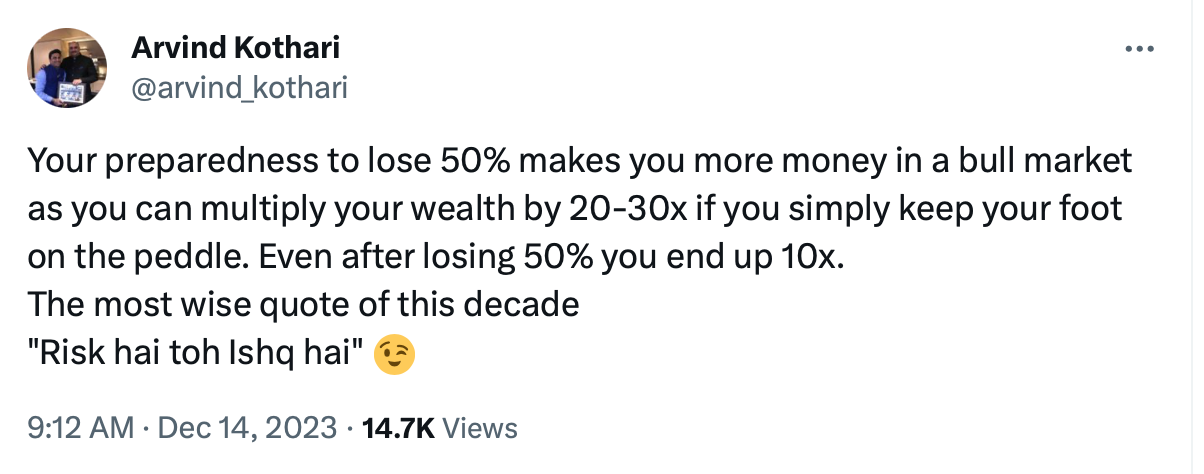

So, the bull run continues and I am keeping this quote from Arvind Kothari in mind.

So, be prepared to lose some money from your basket which has been increasing since April. This will make sure that you will enjoy this bull market and not exit early.

But the market looks stretched here. I will be alert and focused and I will make sure not to lose much from here if there is any correction in the market. Also should not run after every breakout in some kachra stocks.

The regret will always be there, I missed this stock, I missed that stock. I exited early, and so forth.

The SmallCap Index is up more than 11% in just one month after my last note.

In the last 2 weeks, large caps also showed similar strength to mid and small caps may be due to the return of FIIs or state election results.

Disc: Update on last month’s trades

Still holding my position moving slowly if this crosses 300 then further upside possible.

Also, there are a few new orders received by the company. and promotors were also buying from the market.

Closed my position with little profit as it was not moving as expected.

Simple clean move. Booked 50% today on this trade and trailing the remaining position.

I used to book full positions either in or out completely but I have missed many up moves so don’t want to miss either or give back all my gains to the market so trailing with a 50% position. Will book remaining position even with early signs of weakness.

The power sector, PSU, and mining magic playing out

Holding all the positions with Trailing stop-loss at 200. If it closes below 200 then I am planning to close it at the end of the day.

For the upcoming week my focus is on selective Pharma and chemical stocks.

Orchid Pharma came on my radar after the gap-up on 8th December and today it crossed the tight range with good volumes.

Fundamental triggers: Merger with Dhanuka Lab, promotor holding to surge to 74.45 pct vs 69.84 pct due to proposed merger of Dhanuka Lab research upgrade. The company also targets to 1400 cr turnover.

Orchid Pharma | Source: JM Financial

- The management is confident of delivering 20-25% Revenue CAGR over the next few years (excl. PLI);

- The company is also guiding for 100-150bps EBITDA improvement annually;

- The company has multiple growth levers: (1) capacity expansion; (2) new product launches in regulated markets; (3) PLI for 7ACA and downstream products; (4) NCE Enmetazobactum; and (5) Cefiderocol, which will play out in the next 4-5 years;

- The company is at a land acquisition stage in Jammu (for PLI) and expects an update by the end of this fiscal;

- The company is now debt-free. Post-takeover, the company has taken several cost initiatives to improve margins. Strategically, the company is backward-integrating and forward-integrating its operations to become an integrated player in cephalosporins.

|| Gap-up stocks are generally considered strong technically if the gap is not closed and the price consolidates with the gap ||

This happens when there is overnight something positive development or news and the market has not discounted it previously.

One more example of a Gap up and then price consolidating in the range is Ceinsys Tech Ltd.

You can read more about it in the previous post of @phreakv6 with the upcoming triggers.

:: Just sharing my thoughts and update of last post

17 Likes

Eimco, Weekly - Broke out of the triangle consolidation with resistance around 1600 levels backed by strong policy action from the govt.

This is a play on 3x increase in underground mining that the govt. is planning, while also restricting gear imports

It looks optically expensive, especially post the runup but its something that can do very well over time if this plays out. The risk though is if this restriction on imports is going to apply only to Coal india or also to its mine operators and their subcontractors as well. This is where there could be many a slip. Also its unclear what margins Eimco can make. The breakout gap on the chart can get filled over next few weeks giving some buying oppoertunity around 1600 levels. The terminal value risk here will reduce over time as the piling rigs business is also doing well and could be a play on growth in skyscrapers in the Indian skyline.

Wockhardt, Monthly - Nice chart with base formation and kicking up from it. This is not a sector I understand well but here the play is quite simple. The success of this trade is going to depend on their new molecules WCK5222 and WCK4873 (Nafithromycin). Latter recently completed phase 3 approval. Former might need some capital to get it to completion sometime in the next year and could see contribution from FY26 if successful. From what I understand the opportunity size is huge, running into billions as per management but I think it could be more like $200-300m but with great margins since these will be out-licensed and royalty should be good. No point modeling anything considering this is a zero-to-one bet

Synergy Green, Monthly - First level breakout from 200 levels and another from 250 levels, both showing decent accumulation. If unwilling to play wind through Suzlon, Inox or Sanghvi as an ancillary, SGIL offers a good opportunity with 85% revenues from Wind and with good cash flows. The company currently has 30k MTPA of casting capacity which will be 45k MTPA by June '23. The promoter interview has good details on the business. They have Vestas, Gamesa, Senvion, Adani as clients. The revenue is driven not just by domestic but to OEM sales that end up abroad and also direct exports. They do casting of windmill parts including turbines.

The machining cost is a significant part of the cost structure and there’s possibility of margin expansion here as the capex coming next year also includes machining capacity if I understand right.

The promoter has pretty strong goals to get to 100k MTPA by FY27 which would mean a topline of 1000-1200 Cr and at a margin of 16-18% could mean significant upside if its pulled off -

it could happen if the govt. doesn’t mess up the wind energy plans and exports continue to remain strong. Initial signs are very promising with the Repowering policy that came up last week. Govt is incentivising developers with land that can generate better PLF to go for better modern technology and also compensating them for scrap and also for the terminal value. This seems to be a very positive move but I am not expert.

Roto Pumps, Weekly - Has a small breakout but has pulled back and given up all gains but still trading above 20 WMA which should offer support. There’s a FII that has been selling continuously which is keeping price down. As a business whatever I have found about this is very promising, be it the margin profile (not many Indian manufacturing businesses can boast of a 25% OPM), new products, new geographies the company is getting into, the consolidation happening in the space with Ingersoll Rand acquiring Roto’s main competetor Seepex and Hydro Prokav. It is heartening to see an Indian business competing worldwide across geographies with German and USA made pumps.

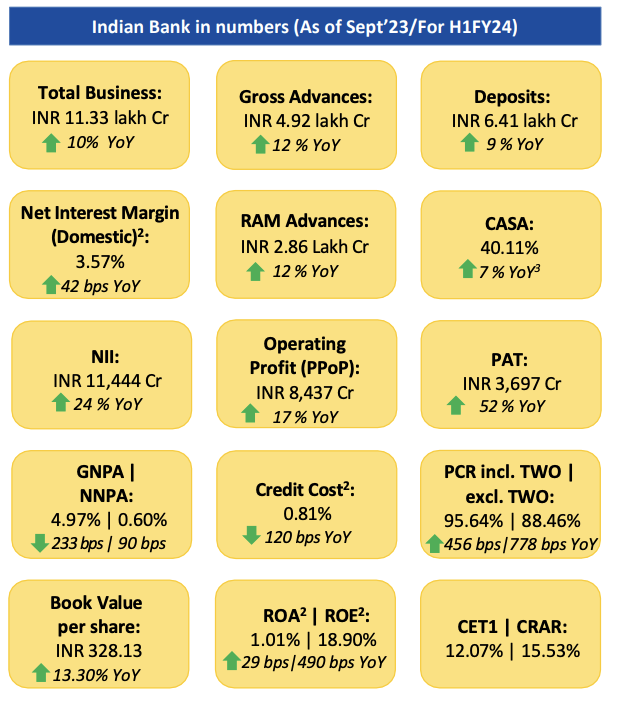

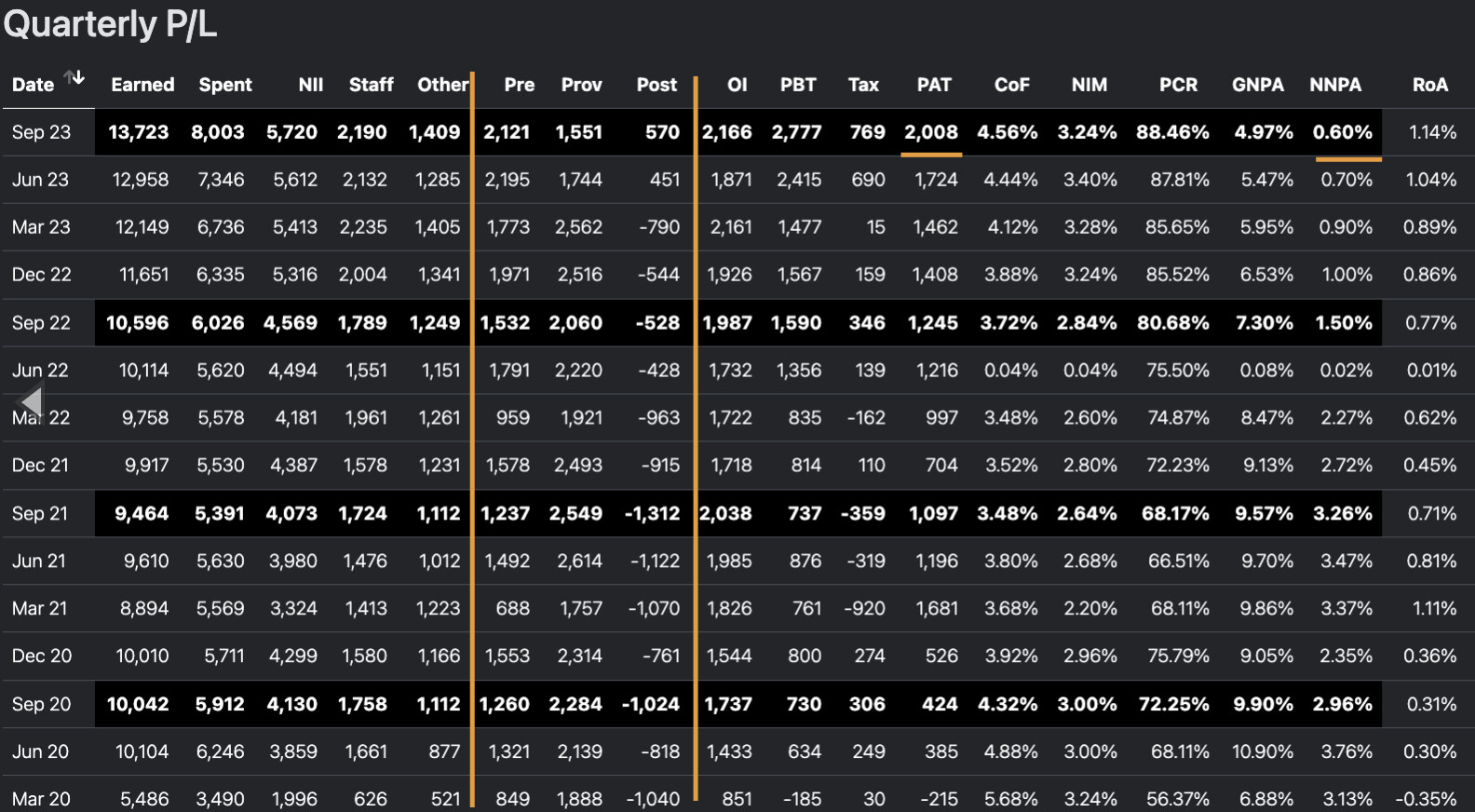

Indian Bank, Monthly - Nice breakout on the weekly after a consolidation.

This is not something I would typically touch but its very tempting. BV is 328, so trading roughly 1.4x book.

I believe BV should grow a fair bit over the next 2-3 quarters since the provisions are about to hit bottom (NNPA at 0.60%) over the next quarter or two and from then on, the growth post-prov profits should be lot higher and I wont be surprised to see 10k Cr PAT here. The same is the case with couple of other PSU banks like Union Bank and PNB as well and could be played as a basket.

Some updates in existing positions

Taal - On the approval for merger of Taal Tech with Taal Ent, the management had promised it could happen in Q3/Q4. There was a hearing on 14th sept and a follow-up on 12/12

I see in the comments as everything being received and don’t see any follow-up being posted. My guess is that this is more or less a done deal and might get to completion in this FY. Hopefully next year’s AR will reflect Taal Tech’s capabilities (the curious can go through employees’ linkedin profiles and get everything they need) and be one befitting a Engineering Services firm, aiding in discovery (as I discovered PML post AR last year)

Ceinsys - Has closed at a weekly high post 8 weeks of going sideways after the breakaway gap as mentioned by @Azlan above. There’s some supply around 370-380 levels that needs to be absorbed before it gets a move on.

Goodluck has had a good close on the weekly and looks to be readying for QIP of 200 Cr. Promoter has made hay here issuing warrants at 300 odd and paying 25% of the 40 Cr (10 Cr upfront) which is already worth 90 Cr. As a trade it still appears cheap and QIP seems to be par for the course in the bull market.

Only risk to this bull market at this point are the promoters

Disc: Positions in Eimco between 1650-1800. Wocky around 340. Synergy around 290 and Roto 380-400 and rest as disclosed earlier

56 Likes

In relation to Eimco, do you have any thoughts on International Combustion? Their revenue mix is like this:

Mineral & Material Processing & Handling Equipment: 60%

Industrial gear: 30%

Building Material: 10%

Seems to be in a similar space to Eimco and Elecon. Trades at 15 pe TTM with very good growth.

3 Likes

I am little wary of having this post in this thread - in the fear that we will dilute or digress from the core idea of the thread, but at the same time I am not sure if I should start my own thread for posts like these. Just putting it here as it pertains a lot to learnings and thoughts about the approach of constructing and churning a techno-funda portfolio.

This year has been good, so good in fact that I doubt it will be matched in any subsequent year, anytime soon. Lot of stuff worked - VBL, PML, Apar, Shilchar. Some like Welspun Corp, Garware, Spandana, Ugro, PDS were great trades in short period of time. A few like Vimta, HOEC, Mazda, Honda Power flattered to deceive. In the current portfolio, Taal, Ceinsys, Goodluck have done quite well. Sharda Motors and Wockhardt are setting up quite nicely. PML has been a rank underperformer over last 6 months but I hope that changes in '24. I will find out a thing or two about long-term investing with PML as against my current strategy of churn based value investing.

Some ideas

Time Machine - Regret is a powerful emotion that can suck the joy out of even good outcomes. I feel only regret worthy of having is a “future-regret” - and our strategy should be geared towards avoiding future regret. Which decision if you don’t make today will leave you in regret in the future?

To avoid situations of regret, and also to learn from past trades - what I have found to be useful is a tool I use to re-visit a past portfolio as of a specific date - say Jan 1, 2023. The tool also shows what the returns on that portfolio will be, had I not made any decision from that point. When we are stuck with regret arising from narrow-framing (something like “oh I should not have sold Neuland labs”), it is better to look at all decisions together (broad-framing) for we leave out the other good that arose from this one seemingly bad decision. If the time machine shows you are better off not having churned (can happen a lot in 1-2 month timeframes), there could be something worth learning - especially in longer-timeframes (for a trader in a raging bull market that is ~6 months).

Trading Journal - Also worth having is a trading journal for the person making the decision is very different from the person evaluating the decision post facto. In Kahneman terminology, its the "Experiencing self’ vs the “Remembering self”. This ensures there’s a voice to the person who made the decision. A lot of times i have found a bad decision (say selling too early) arose out of my biases against a sector or business. Avoiding a certain trade (say Inox Wind) as well was due to same bias. I clearly have to see if those principles hold in a raging bull market.

Collaboration - I have for long worked alone. I led a large team at a OTT last year and that has changed the way I look at teamwork. I have made myself a lot more receptive and consequently found numerous great folks during the year to collaborate with who have enriched my thinking a lot. I feel this has been a crucial improvement for me personally in '23. Collaboration is a force multiplier

Market Participants - concentrate vs diversify, illiquid vs liquid, short-term vs long-term holding period, meet vs avoid managements, charts vs fundamentals, value/growth/momentum, deep vs shallow research, micro vs macro, top-down vs bottoms-up - everybody has their moment in the sun and everything works or doesn’t and there’s no holy grail. In a bull market everyone is misled to feel that they have the holy grail. If you are not outperforming the index (I use microcaps to evaluate myself) over 6-12 month periods, it is time to re-evaluate and re-calibrate approach. You are not answerable to anyone unlike a fund manager who cannot afford to have style-drift

Macro - It is amazing how quickly the macro threats the global economy was facing in Sept dissipated in a matter of weeks. Oil nearing $100 and 10Y yields nearing 5%. Does it mean we shouldn’t use macro? I still feel at the turning points, macro dictates further moves. In this case, it de-escalated as quickly as it escalated. That’s the outcome and there’s no point resulting. In an alternate universe, '23 proobably ended up with normal returns. What’s important is being able to change mind quickly when information changes.

Position-sizing - It is hard mentally to think position-sizing only in terms of percentages as related absolute amounts take time to get accustomed to for the mind in a pf that has grown fast. I know people who only use constant position sizes and make lot of bets as pf grows bigger but their time horizon is lot longer (A longer time horizon is an antidote to a lot of folly). If your time-horizon is shorter, you have to think in percentages or you will end up making a lot of 2-3-5% bets because that’s the only amount your mind is comfortable with and that will do nothing to the overal pf returns.

Hunger - Your hunger drives returns. Without hunger you will find reasons to stay out. What we lack most of the time is appetite for returns. By nature our culture is non-materialistic and has a love/hate relationship with wealth. If you feel sated, take a break and come back when there’s hunger or develop an appetite.

Technofunda - This has worked really for me but I notice that most of the time, the importance I give is to charts. It is a weird thing to admit when you can do fundamental research as well as anyone else. Everyone is a closet technician. As of now, I feel if I have to give up one thing between technicals and fundamentals, I will give up fundamentals (I am going to regret saying this I think). This is akin to Thom Yorke of Radiohead saying he would prefer drum machines and a computer to making music with guitars - on why he may never make a record like ‘In Rainbows’ again. I will continue to use technofunda though as the narrative bit from fundamentals is what makes me feel like I “deserve” the returns.

Long-term Investing - I think I will segue into long-term investing when the pf hits the large number I have in mind. As a long-term investor, it will be the fundamentals that will let you sit tight. So over time, I do think the transition to fundamentals and less of technicals is bound to happen. One thing @ayushmit bhai told me this year I will hold dear for a long time to come. Long-term investing is like sitting in a bus from start to finish, others travelers will get in and get out - but your destination is different. He meant this in the context of Shilchar which I was in a hurry to sell for flimsy reasons. Even now I feel I have committed a blunder in selling but you can only take the horse (me) to the water but can’t make it drink.

I hope I haven’t cluttered this thread with random stuff. I felt like documenting these thoughts from the year for posterity and it pertains a lot to this style of investing.

I hope '24 is good for all of us. Happy new year!

208 Likes

@phreakv6 Beautifully articulated as always.

Which tool is this?

5 Likes

Oil has bottomed now and we are looking at oil prices recovering. That will probably bring a final rally in stocks that should last into March.

Large infrastructure expenditures that usually follow recession or hard landing will hopefully lead us into a commodity boom, this can be seen in copper and iron prices firming up as well as crude bottoming on price action and fundamentals most of which are due to underinvestment in commodities sector. New oil discovery drilling or mine development for commodities that was very commonly seen on London, Toronto and Australian mining sector has virtually been zero since Covid and that will show up shortly as shortages.

Prices of stocks such as xom have bottomed and industry leaders like Warren Buffet who is generally early on trends buying and adding into his holding of OXY

On Indian stocks companies like Hindustan copper have already doubled. Steel companies, hindalco, national aluminium, nmdc etc are well bid as everyone is expecting a rotation of funds into commodity stocks as tech and other companies would see an outflow due to impending hard landing and a froth. They were the go to assets when things got tough during the GFC in 2008. Because when a crises like hard landing and unemployment will hit, most of the government focus will be spending on infrastructure.

Indian infrastructure companies are having a good run with a good order book and that will only lead to higher shortages in commodities.

Powell has been promising soft landing and I know most Indians believe the Indian market and economy is isolated from the shocks of international markets but really can we source cheaper iron, copper and cement prices if international companies find it hard. Can we export more fabrics or implement more IT projects if the demand slows internationally. I don’t really understand the logic that our economy and stocks are isolated

12 Likes

Excellent year end thoughts… Thanks for sharing regularly here… Apart from Hitesh sir, this is another thread I follow regularly for your thoughts. God bless you

8 Likes

Thank You for such a wonderful post…!! It is always wise to learn from others mistakes and winning strategies than to be taught from the pain that experience teaches in ones journey of Life or Investing…!! This is the first time i am writing anything in Valuepickr Forum and I wanted to start off with my thoughts in reply to yours (I intend to be more active from now onwards…maybe a New Year thing…!!).

On Regrets paving way to new learnings: Being a Business Owner, I always had challenges of my own in being able to spend much time following the markets closely. I have always bought and held onto stocks for several years (Laurus from IPO days being a case in point). Held a very very large position (average of 550 a piece of 10 Re FV Share) and sold 1/6th of the position to recover my investment and 1:1 profit. Left the balance holding as it is for lack of Technicals knowledge at that point of time…!! Left a huge amount of money on the table (which I could have encashed happily) and waited until the stock fell to what it is today. This prompted me to think hard on my deficiencies and paved way to my enrolling into lot of courses and reading relevant books. Happy for that…!! Never lost money in the markets but would have made much more if I was more learned ![]()

On Long Term VS Momentum Investing: Being a Long Term Value Investor (for lack of time being in Business, adopted a strategy to buy a good company at a reasonable price and hold for reasonably long time until it gave multifold returns), I never knew a thing or got a taste of Momentum Investing. After I made good friends with like minded investors whom I met in various courses, investors meets etc, I started learning about Sector Rotations, Tailwinds etc and what is Momentum and Technofunda Investing, Now I have a war going on in my head as to my Long Term Buy and Hold Strategy is better in itself or should I invest a portion of my portfolio into Momentum Stocks based on Technicals for Entry and Exit,.!! Since my portfolio is of a good size, maybe I should think about Time Value of Money as well (at the same time, a challenge of being able to get enough volumes exists today)…!!! It is very difficult to avoid comparing with friends who have smaller portfolio sizes but higher XIRRs and CAGRs and focusing on what I should set for myself as a good benchmark for returns on a portfolio of my size and be happy with it…!! Coming to terms ![]()

On Hunger : I am sure I would have done very well with my portfolio returns (since it has grown and become large over a period of time and I paid a lot of taxes) but I have never calculated XIRRs and CAGRs until date (right or wrong don’t know). Not that I never cared for returns but always tried to do my best and accept whatever was bestowed. Kind of upset at the moment looking at friends who are heavily into Power, Defense, Railways etc ![]()

On Collaboration : Held a large quantity in Titagarh at 80, Garware Hitech Films at 600, Powermech at 450, Aurionpro at 300, Skipper at 75 etc etc…!! Got out for various reasons from time to time before enjoying the fruits. Lack of collaboration didn’t help. Came a long way now. Hope all the learnings of the past 2 years will pave way for a much better future and journey in investing…!!

Best Wishes and Happy New Year…!!

21 Likes

Garware Hi-Tech Films, Weekly - Strong breakout post 15 weeks of sideways movement.

Good example of stocks going sideways when expected outcome doesn’t happen but expectation itself still stays anchored forming a bottom to the price (similar thing in PML around 1400 levels as it waits for next triggers to price them in). A quarter or two here and there doesn’t affect the sentiment too much.

Here PPF volumes were very good in last quarter earnings but IPD played spoilsport giving rise to a flattish looking PnL. PPF volumes however continues to grow along with utilisation that even without a IPD turnaround, we should have decent growth and whenever the commodity business swings - be it in current quarter or next, the swing in earnings could be huge.

Ceinsys, Weekly - Similar sideways movement and breakout and getting a move on post breakout and consolidation. These weekly moves where it retraces some of the breakout week can be good point to buy in (especially useful when following monthly charts alongside as bulk of retracement is covered during the last week of the month)

Wockhardt, Monthly - If this month ends above 500 levels, it could imply a turnaround in fortunes for the company from the 7+ year decline. A double-bottom base has been formed around 200 levels and this month could be the breakout month. Did some fundamental work here on this. Fundamentals imply a much bigger upside through this year as there are lot of triggers aligned during the year from WCK 5222 Indian emergency use trials, taking WCK 4873 to other markets, growth in Emrok, US business restructuring impacting the PnL positively, the WCK 5222 phase-3 progress in US among other good things happening in the vaccines and biologicals business.

Sharda Motors, Monthly - Nice C&H breakout on the monthly followed by a month of consolidation and this month continuing in the direction of the trend. The HDFC Sec note covers all important details. Remains undervalued and has lot of triggers that can play out in the near/medium term.

Taal, Weekly - Been going sideways post reaching 3000. Sees good supoprt around 3000 levels. Any close on the weekly abvoe 3300 levels could ensure continuation of trend. Next NCLT hearing is on 8th Feb for the reverse-merger with Taal Tech. Not that important a factor but it is a overhang that needs to be done with

PML, Monthly - I used to think this was expensive though I continued holding it but considering the state of the rest of the market, on a relative basis, lot of VP fav stocks like SBCL, PML, RACL, PIX are starting look attractive - as at least the business quality is wel lknown in these. Export data doesn’t suggest PML is going to do very well in Q3, unless domestic business surprises. The company is adding significantly to its capabilities every year which doesn’t completely show in PnL or in the Balance Sheet as intangibles - but these complimentary capabilities over time can substantially change earnings trajectory if horizon is longer.

Disc: Have positions in all

46 Likes

CanFinHome cmp 780

Low Risk High Reward setup with multiple supports to be used as SL

Above 800 can open doors for new all time highs.

Real estate market is on steroids and provides good tail wind for the entire HFC sector.

A couple of HFC have already posted good Q3 numbers.

Good consolidation since last 5-6 months.

12 Likes