Hello friends,

It’s been 9 years since I joined this wonderful community of selfless investors. Here’s my first attempt at initiating a thread on a business that I feel is potentially under-priced. The business is an auto-ancillary called Sharda Motor Industries Limited (to be referred as SMIL, henceforth).

But first, some initial caveats and disclosures:

- There is an existing thread here on this forum. However, that thread is closed and hence, I created a new one. I am happy to move this content to the other thread if the admins unlock it.

- I am not a SEBI registered analyst.

- The goal of this thread is to collaborate with other investors who may be tracking this business, uncover blind spots and possibly, do some scuttlebutt with automotive experts in this forum.

- I am invested in SMIL with an allocation of 3% at an average price of Rs. 769.

Summary of why this business could be interesting:

—————————————————————————

- SMIL has 30% market share in exhaust systems in passenger vehicles/LCV segment

- Entered into a JV with Eberspaecher for exhaust systems in MHCV segment. Eberspaecher brings in technological know-how and is a segment leader in US/Europe. This JV brings the capability to scale up in MHCV segment and capture market share.

- Legislation tailwinds - BS VI emission norms along with RDE has the potential to increase content per vehicle in PV/LCV segment. CEV-V and TREM V regulations in 2024 will bring all Construction Equipment Vehicle and Tractors under emission regulation. This has the potential to double the target addressable market in value.

- Optionalities in EV, sub-component exports and make-for-the-world in the Eberspaecher JV

- High ROCE business, negative working capital, healthy cash generation

- Net cash balance sheet. Available at EV/EBITDA of ~9x TTM

Detailed Analysis

—————————

About the company

——————————

CMP as on July 28, 2022 - Rs. 736

Market Cap - 2183 crore

SMIL is an established auto ancillary company offering products and services in the following market segments:

- Emission control and Exhaust systems

- Suspension systems

- Roof systems

It has also entered into the EV space through a JV with Kinetic Green, India. In the initial phase, the JV will focus on assembly of EV battery packs and BMS, primarily for 2W and 3W. It will also explore sub components that go into BMS.

Brief History of the company:

——————————————

1986 - Inception of SMIL

1998 - Foray into Exhaust systems for passenger vehicles with Chennai unit and agreement with Hyundai

2002 - Ventured into Suspension assembly business. Established R&D for exhaust system.

2010 - Established R&D for emission control

2018 - Entered a technical partnership with Bestop Inc. USA for manufacturing of roof systems

2019 - Eberspaecher and SMIL enter into a JV to manufacture CV exhaust systems in India. Eberspaecher brings in global know- how for the local market

2020 - To resolve a family dispute, demerged NDR Auto component limited into a separate listed entity.

2021 - Kinetic Green and SMIL enter into a JV for assembly of Lithium batteries along with BMS for Electric Vehicles – 2W, 3W and Stationary applications

Product Portfolio and market share

—————————————————

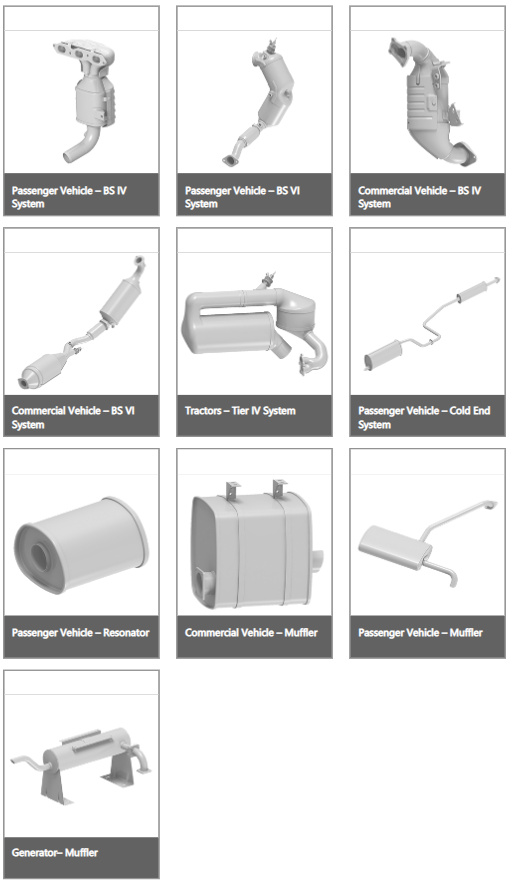

- Exhaust systems - This forms 90% of SMIL’s revenue and therefore, the bulk of the revenue. It caters to the following sub-segments:

- Passenger Vehicles and Light Commercial Vehicles - SMIL treats PV and LCV as a same sub-segment because the engine sizes are similar and hence, exhaust sytems are same. SMIL has 30% market share of exhaust systems in the PV/LCV segment. It is a supplier to all major PV/LCV OEM’s except Maruti. SMIL has an in-house intellectual property for these exhaust systems.

- Medium/Heavy Commercial Vehicles - SMIL has entered MHCV exhaust systems market through a 50:50 JV with Eberspaecher in 2019. Currently, it has 10% market share in this segment. As per management commentary, SMIL is a supplier to the 2 major MHCV OEMs in the country. Currently, this JV is a loss making entity contributing ~120 crores of revenue. As per management, the JV will breakeven at ~200 crore.

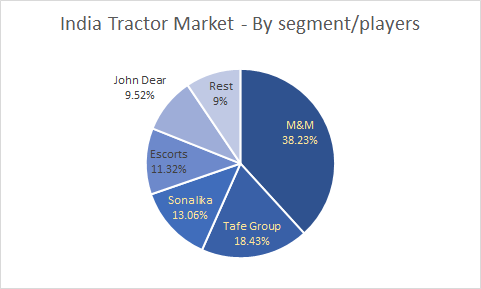

- Tractors - Currently, SMIL primarily caters to the export market in tractors where TREM 5 regulations are in place. This is a very small contributor to overall revenue.

- Construction Equipment Vehicle - Currently, SMIL doesn’t cater to CEV as the current emission standards don’t require their exhaust systems. However, I am mentioning it here as a sub-segment as this is going to substantially change in the next couple of years.

- Suspension systems - This contributes to ~6% of revenue. SMIL has 10% market share in this segment.

- Roofing systems - This is a niche category and SMIL entered this market with a technical collaboration with Bestop Inc. SMIL does convertible canopy and soft top canopy in this segment. This is only a minor contributor to SMIL’s revenues.

- EV battery assembly and BMS - SMIL has entered into 74:26 JV with Kinetic Green Energy for developing battery packs and BMS for EVs. The initial focus will be on 2W/3W EVs. Kinetic Green will be an anchor customer and already has a presence in electric 3W vehicles. Currently, there is no revenue out of this vertical and production is expected to start from Q3, FY23.

Competitive Landscape

————————————

As per management commentary:

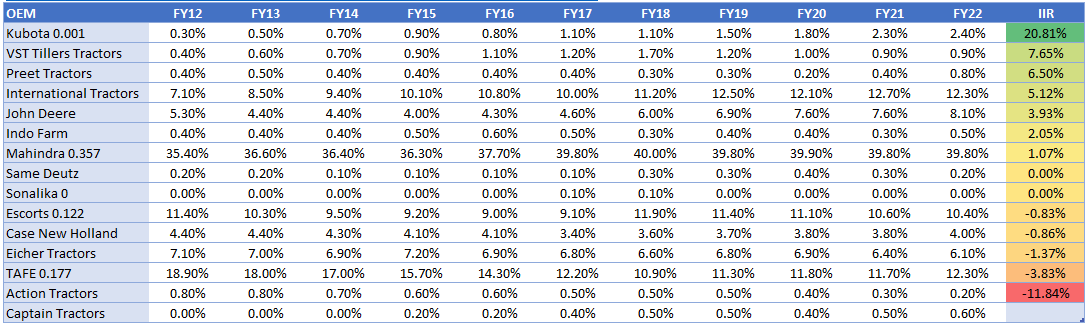

- Competitive intensity is relatively low in exhaust systems with market share split between 3 major players.

- PV has more competitive intensity relative to CV/Tractors. This is because the technology involvement is higher in the CV/Tractor segment.

- Apart from SMIL, the other players are MNCs. As per management, one is an American company and another is a French company.

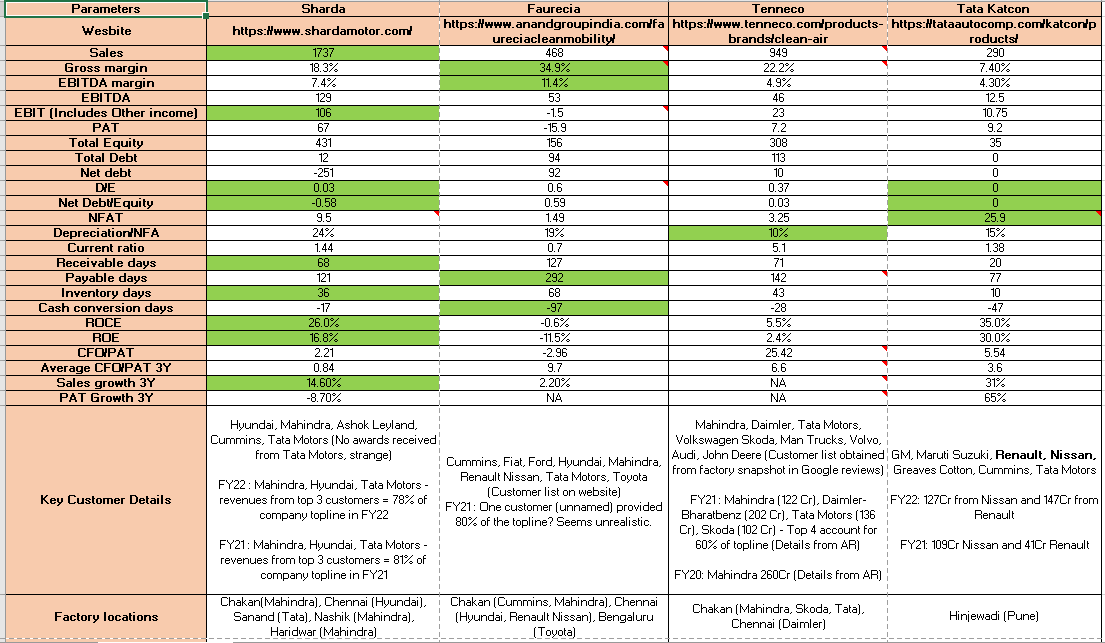

- As per an HDFC report shared publicly here, these MNC competitors appear to be Tenneco and Faurecia.

[The competitive landscape requires more detailed work and the management claims need to be independently verified. I have also ignored “Suspension Systems” business from competitive analysis as it only contributes 6% to revenue.]

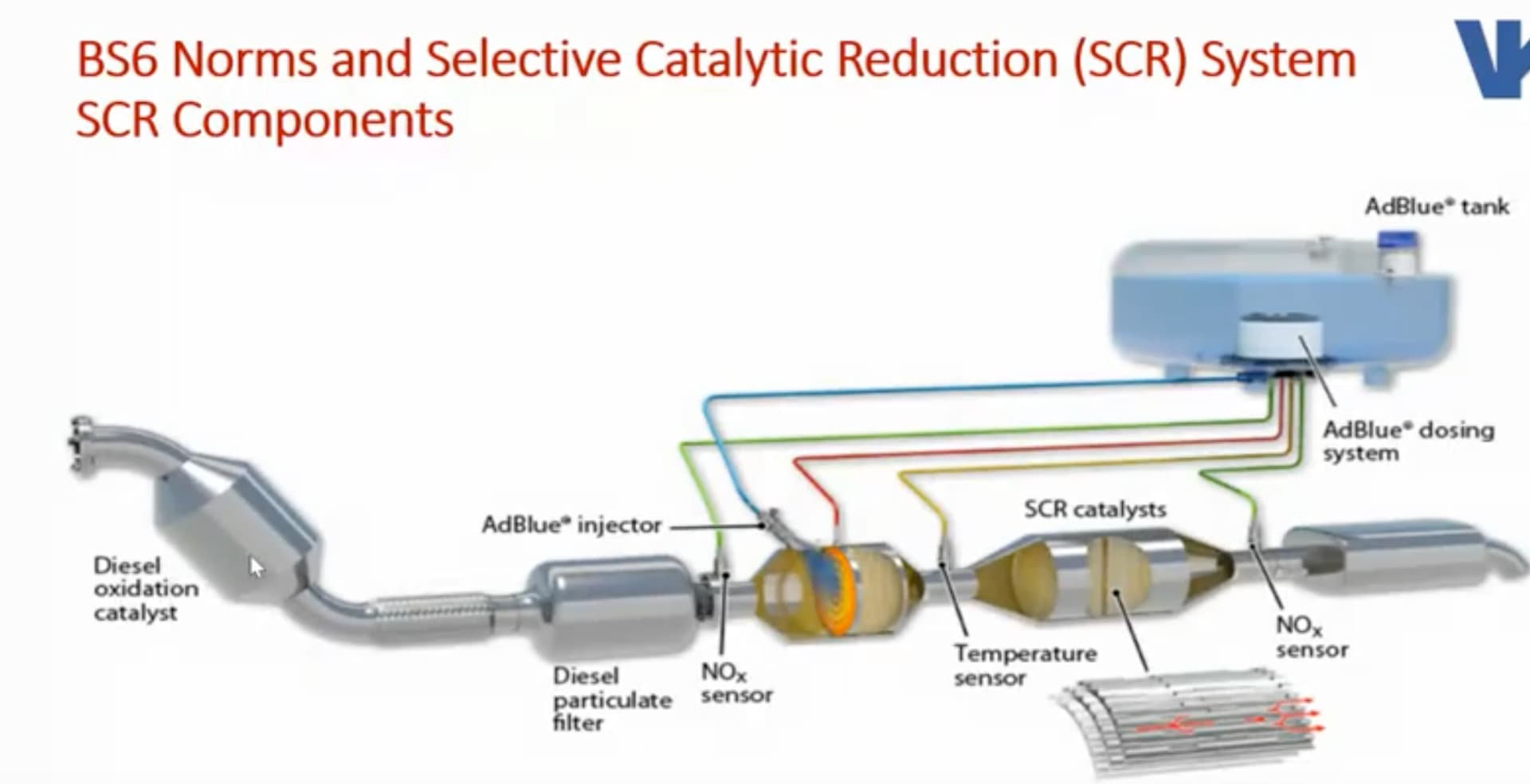

Legislation tailwinds

——————————

The below slide from SMIL’s investor presentation captures the legislation tailwinds:

To summarize from the above slide:

- BS VI RDE norms by Apr 2023 has the potential to increase the content per vehicle by 10%-15%

- CEV V and TREM V norms will bring in all construction vehicles and tractors under its ambit and this has the potential to double the market size SMIL serves today. SMIL already has existing relationships with tractor OEMs and expects a sizable market share in this segment.

Key Risks

——————

- The biggest risk to SMIL’s business is the gradual move towards EVs that will make the exhaust systems business redundant. This means assigning a terminal value of 0 to that line of business. As per management, the following is their thought process on this risk:

- They see the electrification happening rapidly in 2W/3W space and hence, their JV with Kinetic on EV batteries/BMS to take advantage of this opportunity.

- However, in the PV space, they see the shift to happen gradually in India and for CVs and off-road segment, they don’t see the electrification happening in the next 10 years. This needs to be independently validated. Tube Investments recently invested in IPL Tech Electric Pvt Ltd, an electric heavy commercial vehicle startup, as per the news here. It is possible that this transition may happen sooner.

- The management is also exploring the sub-component export market and intends to be power train agnostic

- The other risk is the delay in implementation of the emission norms which will push the new market opportunity further down the road. As per management, delays in order of months could happen but not more.

- Cyclicality in autos is definitely a risk and needs to be managed via the valuation one pays and the allocation

Financials

—————

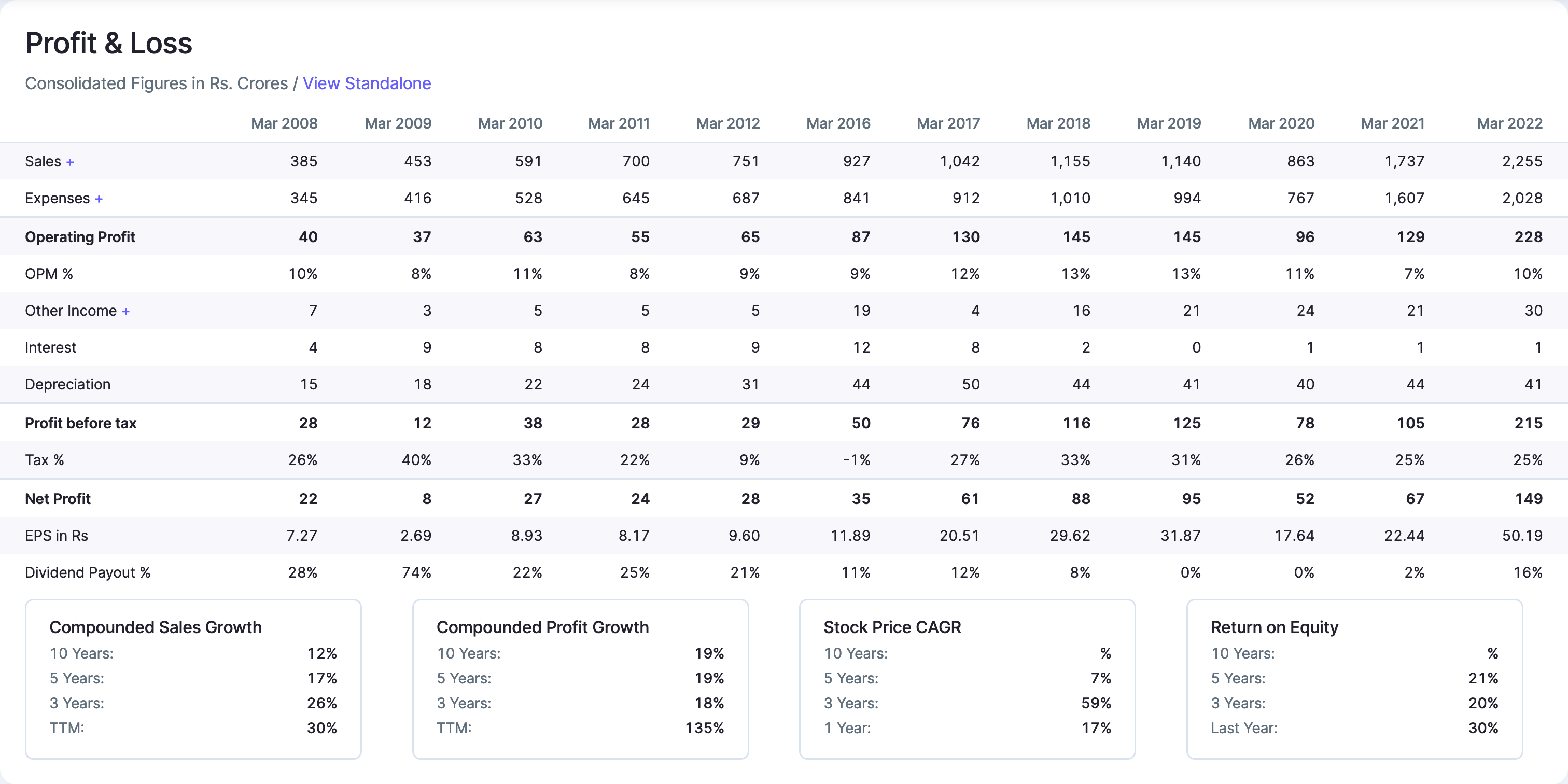

Pasting the screenshot of financials from screener below:

-

P&L

-

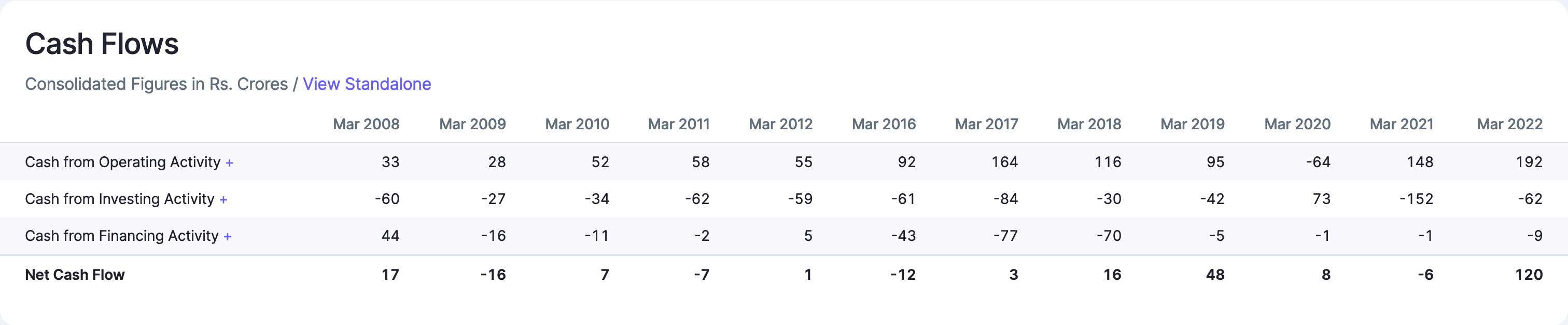

Cash flows

-

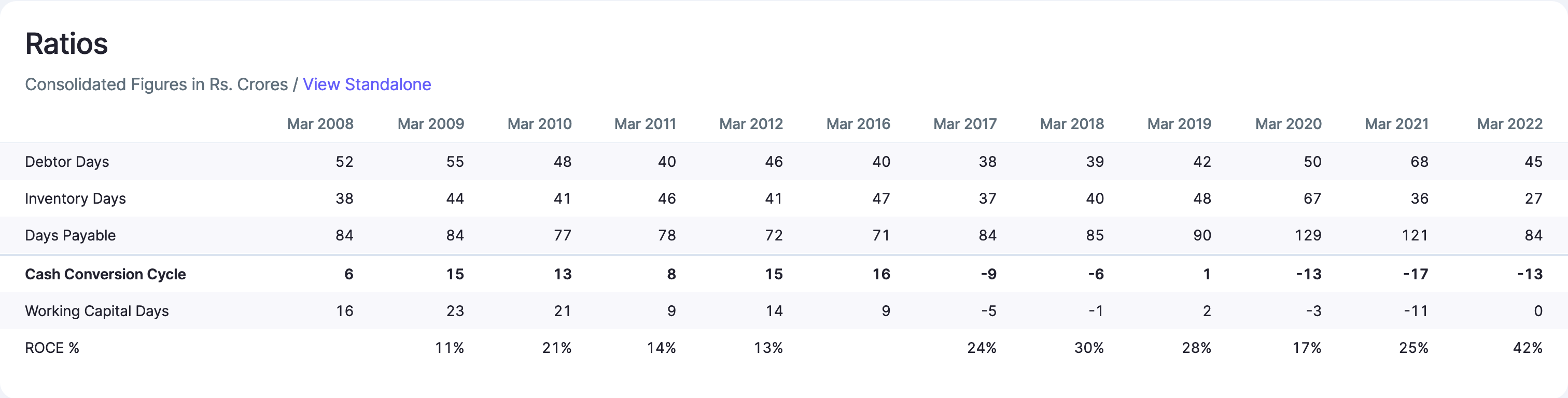

Ratios

Important things to note

-

The auto seating business demerged in 2020 as NDR Auto. Therefore, the long term numbers should be seen in that context i.e numbers before 2021 also include the seating business revenues.

-

In the auto-ancillary space, OEMs tend to have a bargaining power. It is notable that SMIL has a negative working capital cycle as an auto-ancillary. It indicates that they may have some bargaining power with OEMs in terms of receivable days and also with their suppliers in terms of payables.

-

ROCEs are therefore, high for the business as the capital employed is less due to negative working capital and high asset turns. Management has indicated that only incremental capex is needed to grow the business indicating lower capital intensity in the business. This needs to be investigated more.

-

CFO/EBITDA is > 84% for the last 2 years

-

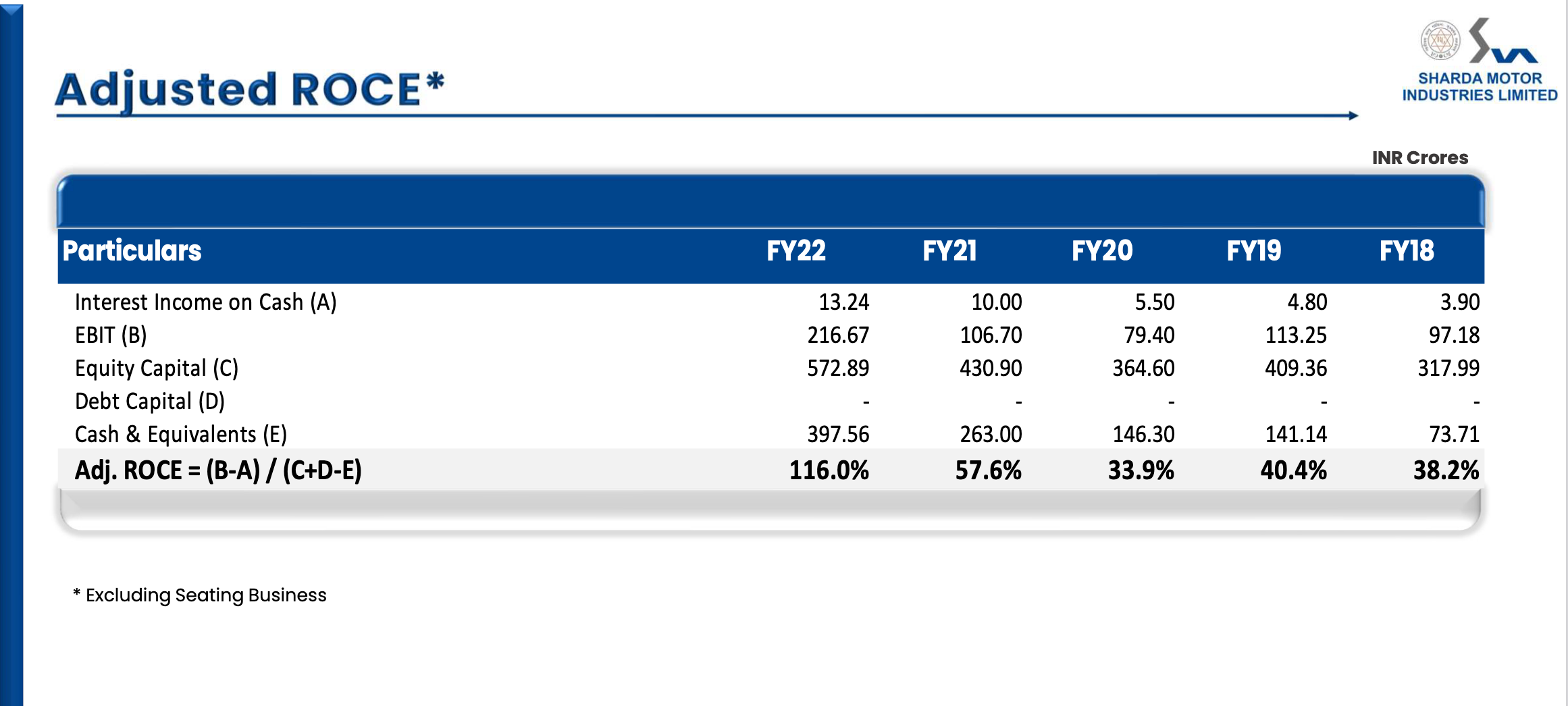

Management has provided a slide on adjusted ROCE excluding the seat business. Here is the screenshot:

-

As can be seen, the adjusted ROCE for last 2 years has been 57% and 116% respectively.

Valuations

—————-

Since SMIL is a net cash business, EV/EBITDA is a suitable valuation metric:

Current market cap - 2183 crore

Net cash as on March 2022 - 454 crore

Enterprise Value - 1729 crore

TTM EBITDA - 228 crores

EV/TTM EBITDA - 7.5

Average EBITDA of last 2 years - 178.5 crores

EV/Avg EBITDA - 9.7

The valuation range is [7.5 - 9.7] based on what one chooses as denominator.

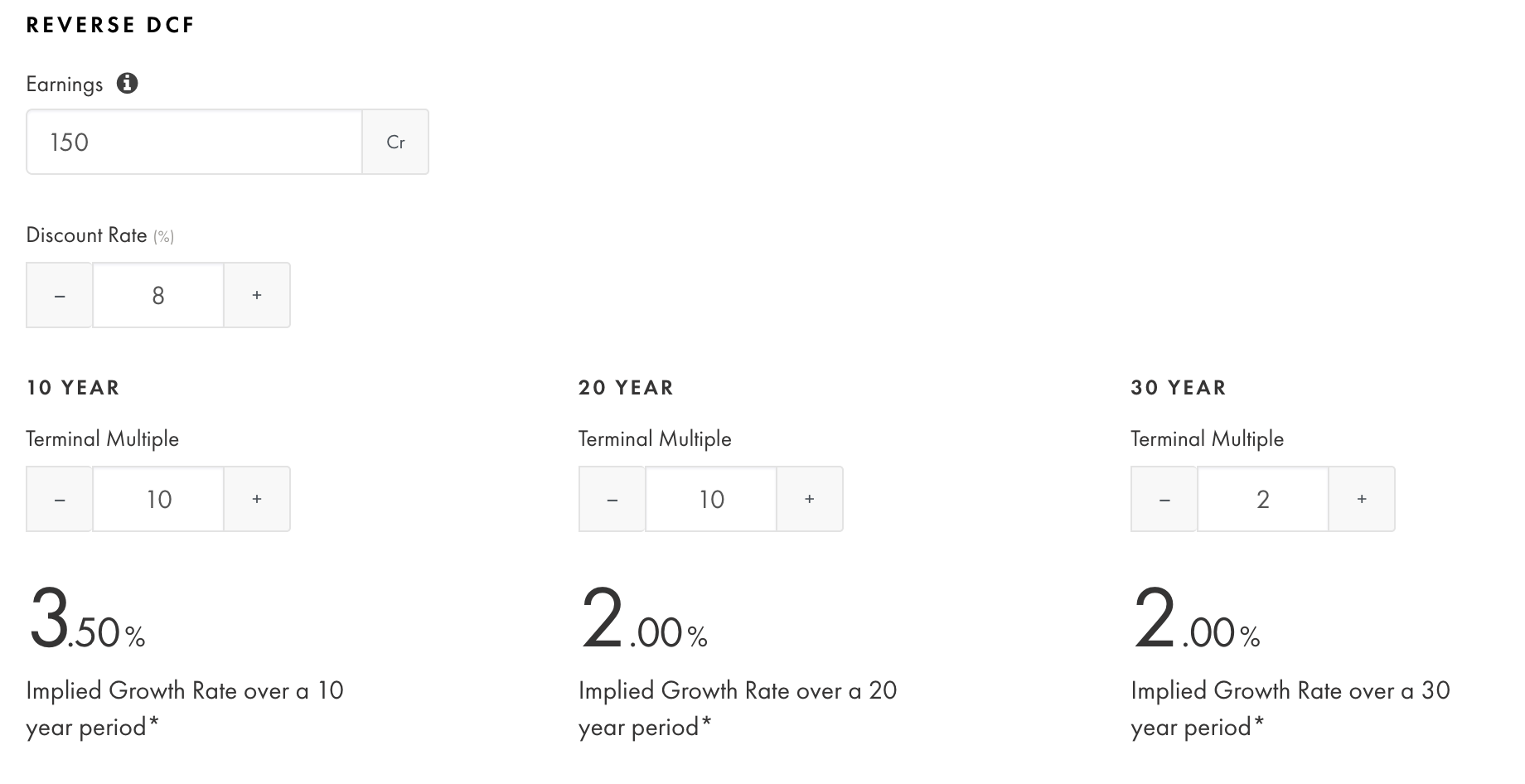

Reverse DCF

- I did a reverse DCF on Tijori finance. Below is the screenshot:

- At a terminal multiple of 10, the market is pricing is 3.5% of growth over the next 10 years.

- It appears that the market is pricing in a faster de-growth in the PV/CV exhaust systems than the growth due to tailwinds in CEV/Tractors and optionalities in EV and sub-component export market.

Missing pieces in the story

- I have not done a checklist on Management Quality yet. Aashim Relan, the CEO, sounds competent in the conf calls. However, I have not done an objective check on walking the talk, capital allocation history and related party transactions.

- Most of the information here is from conf calls and research reports. I am yet to go through Annual Reports and look at possible accounting tricks.

- It is not clear why Maruti is not a customer of SMIL when all other major OEMs are. This needs to be digged into.

- All claims of the management in terms of regulations need to be independently verified through scuttlebutt.

I have heard @Rokrdude in the conf calls and would be happy to hear his thoughts on this business.

Of course, since valuepickr is a collaborative community, I am looking forward to views from everyone.

Sources

- Investor presentation May 2022

- Conf call transcripts Aug 2021, Nov 2021, Feb 2022, May 2022

- HDFC securities publicly available report