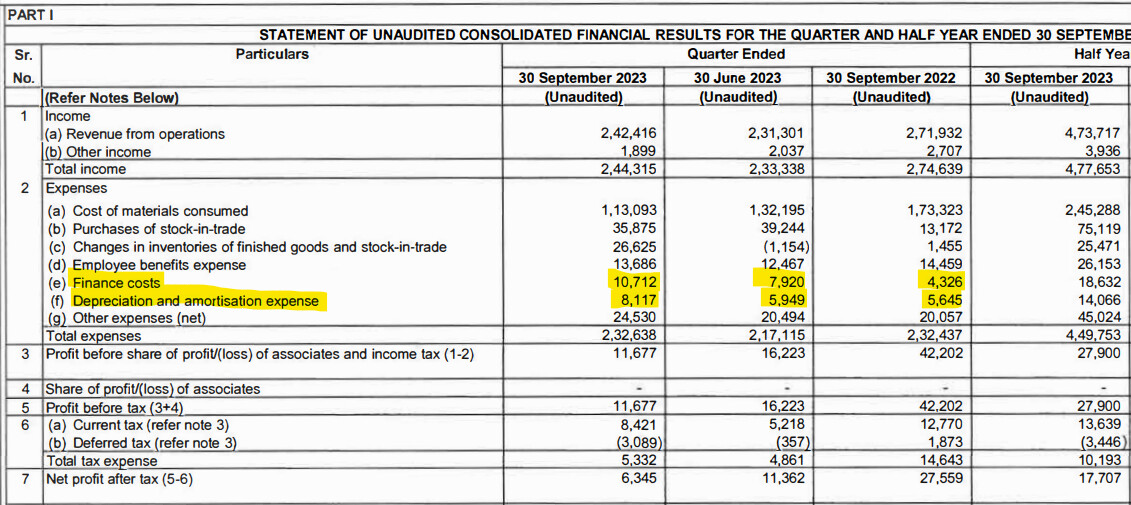

- Depreciation up from 60cr to 80cr and interest cost up from 80cr to 107cr on a QoQ basis

My take on the result

Please note this is my view and way of seeing I might be wrong happy if anybody can correct me.

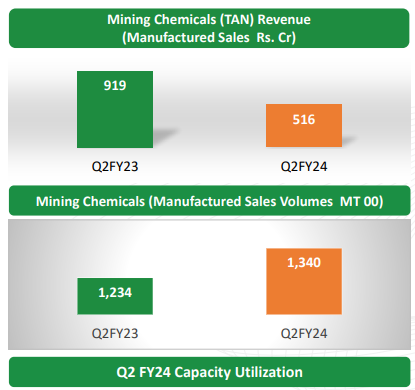

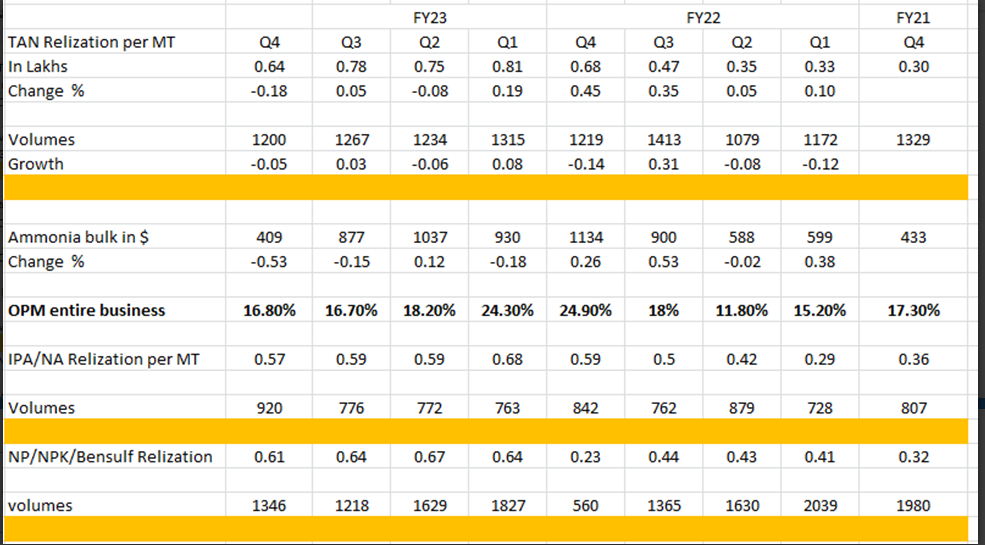

TAN segment has done extremely good on the volume side but the realization has come down significantly to 38lakh per ton, Now this realization is equal to Q2FY22. In Q2 FY22 on a standalone basis they did a PAT of 28cr and in this quatre a PAT of 65cr. If somebody could educate me which all segment comes under their standalone business because on same TAN realization PAT has doubled. Posting the table for reference which I have posted earlier.

Also to add dumping is happening from russia and we have export BAN on TAN by the government and If I am understanding the second point correctly this is the value added services they have talked about in TAN so once this picks they get to charge a premium here as well

- They have taken huge one of kind of loss on fertilizer segment and on stabilization of ammonia plant.

If we adjust for the losses then H1 they would been almost 425cr at a PAT level taking 30% as TAX, now I dont know if this is the right way to see taking the entire thing as PBT but if true they have done a brilliant job, this is too good with such huge headwinds.

On top of this their debt has increased and intrest rates are on a rise + ammonia prices have just hit all time low, In my view this is the worst period the business is in as expected and at lest in my eyes they are doing a good job.

Some positives

I am not remembering the first point will get back and correct myself if I am wrong, this was like deepak fert is eligible for the GST wavier 9% SGST until they recover 75% of the project cost so now it has been changed to 100% that means 1000cr more wavier which is huge(How this wavier will be calculated I have discussed on my previous detailed post)

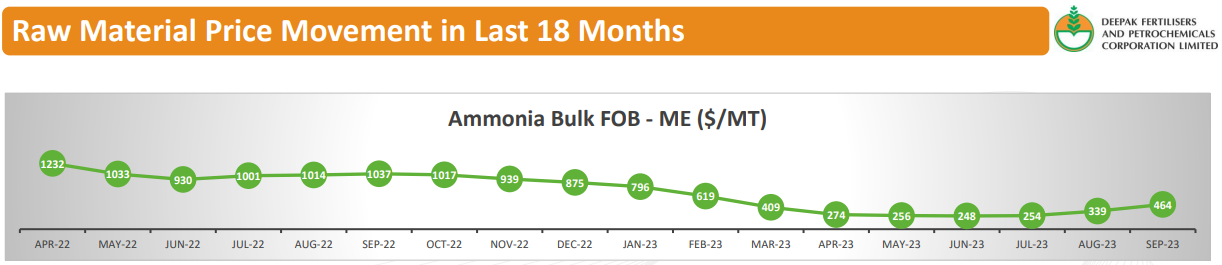

- The company is expecting the ammonia prices to improve in the near future

Just to let everybody know the biggest good news I think now they would profit from ammonia plant the price is 468$

4.Expansion plan in WNA and TAN is also there, just a reminder this quatre TAN utilization was 118%

Overall take

- This quatre they have done as expected I would say some what better than what I expected

- I would not want to talk about future triggers because anything which happnes now only be a positive trigger

This company has decently reduced the commodity portion(cannot be quantified but it has reduced), Like I am just remembering that in a chor company if the choriness reduces they deserve to be valued better similar if comodityness reduces, they are taking the right steps in each segment, the ammonia capex was a 4000cr + capex for a 8000cr company, it is going to benefit them big time, I think the right time to buy a cyclical company is at it worst phase the only thing we have to evaluate is they dont go bankrupt because of the debt, I think deepak would now start saving the cash on ammonia and that should help them reducing their debt going forward.

Just to address one last question their gas prices have been contracted taking various index as benchmark with different suppliers, spot market volatility does not apply to them

Looking forward to concall will add the notes

Disc- I am a young kid who can go horribly wrong so please do you own evaluation, I have taken a position and would be looking to increase it