Added my comments, observations backed by relevant data. Intent is purely academic to share the knowledge and learn and grow inclusively. All comments(in red), highlights, screenshots are addition from my side for pure academic understanding and thought process sharing.

@sunny13nitk I have seen dozens of people around who go around using buffet quotes and tendering “buffet gyan” however your attempt to apply Buffet/Charlie’s advice into analysing Bajaj finance is really very commendable. Buffet’s journey of Geico definitely reinforces and reminds us of dear Charlie’s age old wisdom of ‘Buying wonderful businesses at a fair price and not the other way round’

And the way you have compared Bajaj finance with Geico brings to light many important points which convey that BF is definitely a business of equivalant quality and pedigree as Geico (if not more).

There is little or no doubt about the growth or the runway of growth for this business however i am just interested to know your thoughts about valuations (as i am looking to enter amidst this overall market crash). I still think a staggered buying approach from this point makes more sense.

Well to be quite honest I see no other business engine in Indian market so strong in my knowledge and analysis as bfal from current context. Being a solution architect with sap for decades has given me quite an experience in what bfal is trying to do on technology and reducing friction. It is years ahead of closest peers. It’s agility is state of the art.

Also refer my report analysis by Bob in vp forum under which you would see the promoter shareholding attachment. How smartly the promoters are raising equity capital.

If you ask me I would not shy away from owning only bfal as a single holding in my pf.

However considering recent fall I have been personally accumulating it on fall of every 100 rs and I hope to get it as much as I can even if it becomes 90% of my pf. I believe in very concentrated investing which has its own demerits that I m ready to live with.

Thanks for the quick response Sunny. Actually I did read your note yesterday which explains how astute the promoter group has been in raising equity capital while maintining and even increasing their shareholding. This does speak volumes about their business abilities which help them stay ahead of the pack. I live in the US and work in IT industry too and therefore would love to hear more from you (if its not too much to ask) on how BFAL differentiates itself from peers by leveraging tech.

And you have definitely answered my questions around the valuation part. Thanks a lot for that.

Thank you Sunny for sharing your views on BF.Last year after lot of considerations, finally started building heavy positions in BF and now accounts for 80% of my PF. No regrets- this correction holds more opportunity to add.They are way ahead in using tech to their advantage. In the current situation in India, biggies like BF could gain more traction and market share.

regards

@sunny13nitk I tried to search your analysis report on BFL on vp forum but could not locate it.could you post it again or e mail the same to me directly?

Thanks

Portfolio with 80% in one stock is never advisable. Absolutely no one can have complete understanding of a company and the environment in which it operates. People are largely focusing on the growth on the asset side. But past experience say even minor disruption in liability side can stall multi year growth.

My View BF is good business to own. Credit penetration in India is still shallow. But 80% I personally would be scared.

Remember the first principle of Investing in a Stock – MARGIN OF SAFETY. BF has no margin of safety.

Bajaj Finance is a great company. There is little doubt about that, but buying it at a P/BV of 6.27 is very expensive. This P/BV has factored in years of growth into the price.

From a minority shareholders perspective isn’t it expensive compared to other stocks available in the same category. Like M&M Fin going at 0.83 P/BV

Or as a proxy, one could buy Bajaj Finserv which holds 46% of Bajaj Finance.

Do you not think that Bajaj Finance is expensive, and has a lot of room on the downside in this crashing market?

Are you sure it’s due to panic selling only and not change in fundamentals? Bajaj Finance is mostly unsecured consumer credit to lower middle and middle class, and as unemployment is going to spike a lot (US Govt is projecting 30% unemployment in next one year, highest since 1929 great depression), CD loan defaults won’t skyrocket? I presume HDFC Bank is also sold on the same premise.

Sometimes there is a paradigm shift which challenges every assumption. I am not saying it’s one, but it would be wiser to keep eyes and ears open.

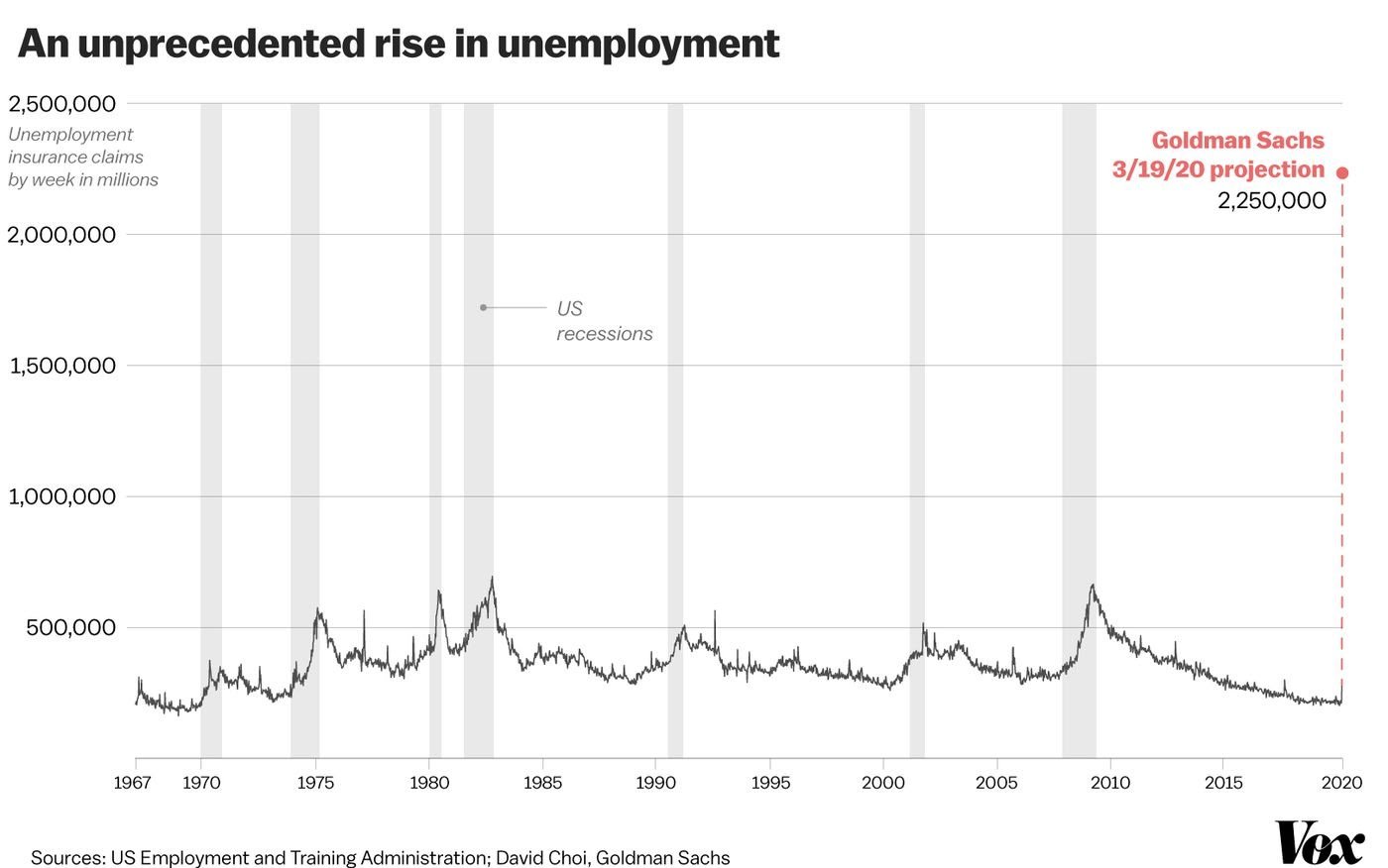

Key point to track in this unprecedented rise in unemployment is - How long will it take to get back to normal globally - 2 months, 6 months or 1 year.

Base case currently is 6 months

If virus dies faster and things return to normal in 2 months we will see an equally ferocious rally on the way up.

I don’t see this continuing for a year, if it does that would mean a severe bear market.

There has been a paradigm shift. Only a set of substantial factors can make Hdfc Bank, BajajFin to lose so much so quick.

FII are selling out, causing this fall. As a result all the extra enthusiasm is going to be cashed out. This is a point of worry for me, because

Bajaj Finance PB is 6.27

Whereas it’s Industry Average is 0.62

I know, I am presenting a crude science here. But, it appears there is plenty of room for FII to sell, book profits, and for the stock price to lose steam. A correction of another 50% is on the cards.

On the other hand,

HDFCBANK PB is 2.75

Industry average is 1.25

Comparing valuation metrics of BF and HDFC Bank with industry average is not right. These companies are best in class with a proven track record of managing risks. As and when a bounce happens, these will be the first one to go up. Check Aditya Puri’s interview yesterday in CNBC. As far as retail unsecured credit risk- there is no such reason to believe suddenly it is going to go belly up. India’s unemployment is already high and these guys are not lending to all and sundry. Their risk management is key. Of course we need to keep our eyes and ears open. If these companies collapse- we need to forget the India story.

As far as crash is concerned-unbelievable- but ETF or other levered guys are selling without bothering about price. Interesting question is -Who is buying ? Everything look surreal.

I feel Bajaj Finance is going to give a terrible surprise to its minority investors. There is so much future expectation grilled into its price that any disappointment is going to cause its price to tumble to at least the industry average… and that is going to be a serious tumble. The current circumstances have conspired a perfect storm for lenders.

The fear of the unknown is only going to make it worse. Certainly these are not the times for a lender to be overvalued.

Though PB is the right way to look at Valuations. Please look at coverage ratios. They through some more light as to why 2.75 PB for HDFC Bank is better than other bank at lower PB.

any approx calculations on the credit cost to the business due to corona lockdown?

one can make a educated guess if we have a idea of loans give to salaried vs self employed