Wouldn’t the risk be similar to the existing retail financing wing of BajFin? These are essentially small ticket EMIs distributed across customers, so the risk management wouldn’t be much different

1 Like

Agree. My point was not if there are risk controls measure or not. My Point was that focusing only growth at all costs could harm in long run. Even the recent NBFC issue people kept focusing on Growth and Kept investing and did not focus on risk of not being able to raise resources.

There have been a lot of other mismanagements in addition to growth which has lead to this situation in some NBFCs . Some of it kept hidden by management, covers by rating agencies and not discovered by regulators.

2 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/73c28af9-a14d-4731-a611-6398e356b66e.pdf

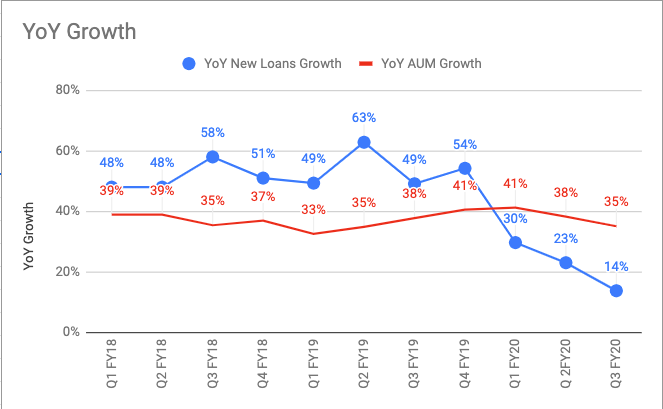

Although AUM growth was good at 35%. The real concern was the growth in new loans booked which just increased by 13.2% Y/Y just to give some perspective the same figure during Q3 FY19 was 49%

Wouldn’t that mean ticket size has gone. I am assuming these would be going to repeat customers.

AUM growth base is excellent- 35% +

Something doesn’t add up 2.5 M new customer added in Qtr where as new loans are 0.9M only. Isn’t each new customer mapping to at least one loan??

Cross selling a loan to existing customers will count as a new loan so it is not a valid argument. Regarding ticket size I am not sure it is possible esp because Mortgage loans contribute more to the loan book but even considering that the drop in growth of new loans seems to be pretty significant

1 Like

Number of loans booked during this quarter amounts to 7.7M and number of customers added is 2.5M so it adds up.

I have tracking YoY growth in new loans and AUM for the past 10 quarters now. As you can see from the below chart the AUM growth has been fairly stable.

This means that they are giving out higher ticket loans. I am guessing that they are doing more SME loans and fewer consumer loans. We’ll get clarity in the next call.

11 Likes

must be housing loans

they said want to make their hfc very big

I feel, they are doing more Working Capital Finance for Industry as a whole. WC funding is a big issue now… With significant churn in NBFCs, WC funding a big issue now

Even taking into account that Bajaj Finance is cautious about taking new customers and not willing to do business with the bottom 15% of the riskiest customers due to the prevailing economic conditions the drop in growth rate of loan volumes appears steep. This indicates that they might finally be losing some ground in the high volume low ticket size consumer durables segment to possibly HDFC Bank (HDFC Bank was very gung ho about this festive season and reported strong loan growth). This is all the more surprising since Consumer goods sales during this festive season was very strong. See the article below.

Now the question is will the loss in consumer durables space me made up by growth in other areas.? Possibly yes considering the low base that Bajaj has in those areas and also much higher ticket size in verticals like mortgages. However we will have to track margins closely as consumer durable loans had great margins unmatched by other type of loans. It is also possible when Bajaj feels better about the macro environment the consumer durables portfolio will return to higher growth as they will be adding new customers whom banks like HDFC will not service through their credit card.

Have exposure to Bajaj Finance through Maharashtra Scooters. At the moment I am taking a wait and watch approach

1 Like

Bajaj Finance continues to find innovative ways of reaching out to prospective customers.

12 Likes

I have had first hand experience of availing Bajaj Finance service at appolo few weeks back.

Basically one of my relative was admitted to Appolo but the health insurance did not cover that disease and thats were Bajaj finance swung into action swiftly.

They were stationed next to health insurance department of Appolo and heard the conversation. Once we left arguing (Wrongly!!) with insurance folks on why the disease isn’t covered and all,Bajaj finance guys approached us in 2 minutes and almost majority of the treatment cost(No cost EMI with processing fee of 1400rs) was given by Bajaj finance team. The amount given as no cost EMI was in excess of 2 Lakh rupees.

Documentation was hassle free and everything was done in mere 30 minutes time.

28 Likes

how does bajaj fin make money on no cost emi ?(1400 rs seems so less for 2 lakh loan).

I apologize if the question is not appropriate in this thread

2 Likes

5 Likes

Most of the time Insurance pays hospital with a 15-60 days delay, also Insurance rates are less compared to retail rates. Enough scope for hospital to pass discount to financier.

1 Like

5 Likes

I attended Bajaj Finance Q3FY20 concall. Some of the points I noted during the call:

• A good quarter despite slowing demand. RoE was helped by lower corporate tax rate.

• Loan loss to avg AUF is a red flag during the quarter.

• January 26, 2020 was an important day for us. Significant slowdown in intent to purchase in Q3 on a yoy basis. However, since December seeing some uptick. Republic day sales was reasonably strong. It is lot more structural. Spread across metro, rural, urban etc. Seeing across for past 30 – 40 days.

• LAS grew less due to default of large broker and conservative stance we took.

• Continue to have a growth stand. Opening new locations consistently. Location means addition of city and town in India.

• Liquidity is pretty strong for us. Have excess liquidity for us.

• Have gone to RBI for additional ECB funds and got approval for USD 650 million.

• Liability has diversified.

• 67% of deposit book is retail.

• Taken 85 crore provision for that broker account and 15 crore provision for the coffee account.

• Auto finance turned red for the quarter. In few quarters we should start to see improvement in the portfolio.

• Bajaj Housing Finance continues to do well.

• Digital product portfolio deterioration has improved during Q3.

• Salaried personal loan continues to do well. Self-employed customers continues to be highly stretched.

• Consumer B2B sales finance business – AUM has remained flattish for past 3 quarters. Is it on account of increased competition? The share of manufacturer’s subvention scheme has remained steady for us. We have 2000 cities in India. Penetration sales are pretty steady. Decline in search for new business. Last year it was 51% growth in searches last year in Q3 while this year there is a decline of 6%. Clearly, our share is very steady. Our share of manufacturer and retailers are steady. If HDFC Bank is gaining, market is consolidating? Are we loosing market share to them? Not sure on who is loosing or gaining. We wan to keep our customers. We can track data of manufacturers in India but cant track 50,000 dealers.

• Cross sell worsening? Other than salaried personal loan all other businesses are up by atleast 20%. It’s a steady growth. Margins are very strong and steady.

• Auto Loan has turned red. What’s the thought process there? This the only business which is captive. The business is a highly profitable business and sustainably generates equal RoE to company’s overall RoE. Taking corrective actions to improve it. In general, what we are seeing close to demonestisation environment. Its much like December, 2016 kind of number.

• Growth rate in cross sell is reducing. Reason? We remain committed to add 7 – 8 million customer franchisee every year for a foreseeable period.

• Auto finance business – captive finance. Where exactly do we play there – financing 3 wheeler guys with high credit score? We have seen that consistently that we have a dominant share of the sales that happen from point of sales for 3 wheelers, 2 wheelers and commercial vehicles. We are a steady play and we play across all three. Proportion across these products? CV will be very small in auto finance business. Average yields are quite in the range of 23 – 24%.

• Overall, available customer base for us? Retail ecosystem – 30% sales is in lending for consumer durables. Working with public data system on prospects in India. By preapproving them, we can give 50 – 60 million people. We have 40 million customers. Strategy for past 4 – 5 years that it takes lot of efforts to organize and strategize customer base.

• Karvy – it is pretty obvious that money that security was not there. What went wrong? The matter is subjudice at this point of time. Every loan loss represents an opportunity to learn. 22,000 crore industry entire industry runs like that – regulator allowed it. Regulator started telling in June that debit and credit is not allowed. Broking cos were dealing with customers for 20 years like that. In hindsight, we should have squared up our positions on October 31, 2019. We are focused on operational and credit risk but missed regulatory risk. That’s the learning there. Taken 85 crore provision. Working with the company and draw a line to it by March, 2020. Learning to be taken is that regulatory risk we should have acted on. On the point of origination, the entire industry exposure of 22,000 crore to brokers even today runs like that.

• PCR coverage – same line of business in auto finance – PCR is seeing fluctuating? When we repossess the asset we realize 40 – 45% of the asset irrespective of whether its an entry level or high end bike.

• Status of IL&FS, Tanglin and Karvy account? IL&FS working closely with management. Received 8 – 10 bids and given time till early February. 60 crore provision on the account and 30 crore lying in escrow. Account is over-collateralized. In past 10 days, there is some legal noise there. Tracking it closely. Tanglin – from public domain and what information we get is that the issue will get resolved in 30 days. In Karvy, the company has demonstrated intent to pay us back. Next 60 days are critical in the account. Will draw line for it next 30 days.

• Are payment banks allowed to issue credit cards? Payment banks are not allowed to lend. Payment banks are virtually debit bank.

• We keep on hearing that some of the large competitors getting aggressive in consumer B2C space. How are we seeing competitive intensity there? Don’t want to be arrogant but it is more noise than substance. Fundamentally, if you can deliver to the customer, it is one part of the puzzle. Other is managing 25 million customer base and collect 10% bounce rate every month with 100 cost is a part of the puzzle. It’s a damn hard thing. One has to make very tough choices. This business is a multi-year game and quite hard to crack. We have taken huge time to generate good business in gold loan. Feel we have cracked it and scaling the business. Our competitors are where we are in gold loan business.

• Provisions – 30 day DPD increased across the portfolio except salaried PL, lifestyle and home loans. Further increase in provision? They have stabilized in past 2 months. Credit cost from here shouldn’t increase. Most likely has peaked. Adjusted for one off, we feel credit costs are elevated. However, we have not started to see significant improvement. One more quarter will settle this in our heads and we will then provide the outlook to you.

• Break up of fees income? Its bilateral in nature and we have a good strategic partnership with our insurance partners.

• Do we have client stickiness? Client stickiness we have 20 million storecard customers. The process is frictionless. Lower the price of products, lower the involvement in buying decision – you will go with the one which does that. out of 20 million customers, 15 million will end up doing transaction with us. Its not one on one relationship it should tell about stickiness of the franchise. Value of the true franchisee is if he is willing to do the business with us.

• What competition do we see from banks having lower cost of fund and tie up with Fintech players? Small part of total credit in India – Just 1.4% of total credit. Economy will grow at 4 – 5 or 6%, we are here for business. Relatively low size – 98.6% total credit available for us to grow. As long as the businesses are above our profitability model, we remain growth oriented. First 9 months, balance sheet growth started from 41%, 38% and now 35%. During that period, provisions have gone up. Despite higher credit costs and good balance sheet growth, we are giving same RoAs. We can calibrate, NIMs, credit cost and opex and maintain RoA. Fintech hearing about them for lot of time. But nothing has happening. No view on Fintech business.

• Fee income – traction in all the four segments or is distribution income key driver? Fee income part of it has a degree of linearity. In slowing environment, fee and other income are slower. As overall demand comes back, on %age basis we are pretty steady. Volume will have a role to play going forward.

• Bajaj Housing Finance – Q3 was strong RoE and even on 9 month basis. Can we deliver same RoE? We can deliver 13 – 15% ROE in Bajaj Housing Finance. Building sum of parts model where it delivers lower risk and lower ROE. It provides stability and solidity to over model. It’s a young business. We will have to give it time. Next full year will the third year of the business and will have normalization of the business.

28 Likes

This is scary and we will have to be cautious in coming times across financial institutions(FI). We already know that ICICI, HDFC and IndusInd had lent to Karvy. Probably will have to check such portfolio size across FIs to get a sense of the size of issue in the market

1 Like