Ather is doing surprisingly well courtesy Rizta and it is now very visible in numbers. Q2 numbers should be around 20/25% higher volumes vs Q1 and we could see another significant improvement in EBITDA.

Would be interesting to see EL platform and how they break into the world of motorcycles

One concern I have about Ather is kind of Honda/VW/Ford/Skoda vs Maruti/Hyundai story. Although Honda has some great products e.g. Amaze Car but in comparison majority Indian buys Maruti dzire ( excluding commercial sales). Ford had to exit Indian market.

In general Indians are more attached to already prevalant brand and price, and ends up buying what others are buying ignoring superior products. Can Ather overcomes this, specially when they expand in North India, needs to see ?

While your concern is valid, we are compairing Apples to Oranges here.

Electric is completely new Tech and pioneers will thrive with this.

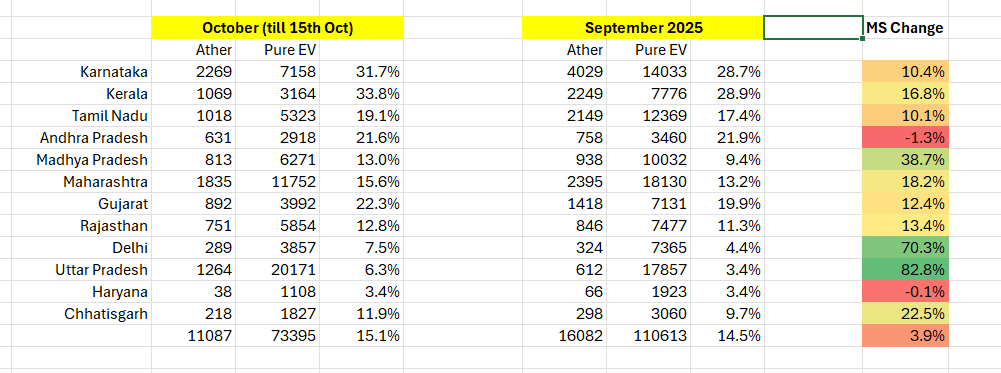

Just to give you example, Till March 2024, Ather had 5% Market share in Gujrat and after launching Rizta, it climbed to 25% by December and they also became leader in Gujrat.

They need to keep listening to market and keep improving.

Not exhaustive. Illustrates distribution led growth. In southern markets, where the distribution is at par / near par with traditional players, Ather is dominating the market. I’ve taken pure EV as a proxy for 2W sales since PV EVs are not that huge.

Predicted Q2 summary:-

Strengthening leadership position in South

Gaining market share in Middle and Rest of India

Production constraints since plant is nearing full capacity utilization - work accelerated on MH plant

I had a Kinetic Honda. Once its spark-plug gave some trouble while starting back from office, the local mechanics could not find the spark-plug. Wisened, I went for a Maruti when buying my first car. My second car was also Maruti. The ease of getting it serviced is the primary attraction.

Bajaj/Honda are comparable in the sense of being a legacy company. But Bajaj and Hero are not known for their EV vehicles (though TVS EV scooters sell well). Ola had the first- mover advantage, and it did generate lot of excitement. Ola squandered the opportunity by substandard product, and trashy service-scooters waiting for months for service. Assuming the EV scooter was the only vehicle the middle-class youngman had for going to his office, the anger is understandable. This was compounded by ill-tempered and ill-mannered responses by the owner.

So, now all the EV scooter makers fight on an even field.

Disclaimer: Bought a small number in the Mahoorat trading of the 21st Oct.

I think the ICE vs EV debate is old now especially in two wheelers. The scooter market is already at 20%+ penetration and will likely be 50%+ by the end of this decade. And the scooters are themselves taking away share from motorcycles.

This is simply because the TCO of EV scooter vs ICE scooter has become a no-brainer (payback period of 1-2 years).

Only question is which player will end-up taking the lion share here?

I personally don’t think you can evaluate new-age disruptive sectors on conventional metrics.. the industry itself is growing at 30-40% CAGR and you’re still looking at EBITDA positivity? In any such scenario, you first capture the market and then focus on cost optimization..my hunch is Ather will end the year at -10 to -15% EBITDA margins.. tbh that’s pretty decent given EL platform will have lower BOM costs

Tarun has clarified this multiple times.. Hero and Ather serve very separate segments of consumers so far.. so a merger isn’t on the cards yet. And if it maybe tomorrow - no sensible person would dilute the brand equity of Ather? It will continue to exist as a separate subsidiary

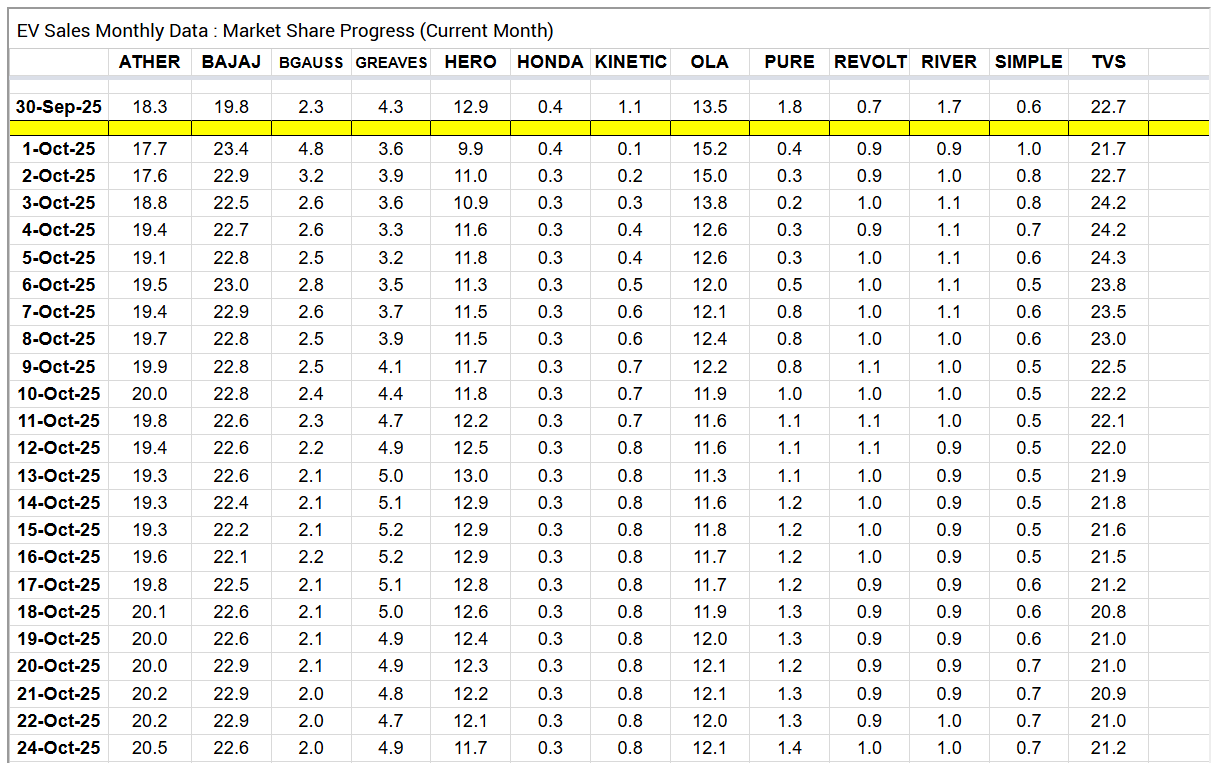

They also have 40% higher sales in October 2025 so far (leading indicator)

Valid question - but from even the recent interviews of Tarun, the spark is clearly alive.. it’s not just the equity stake.. it’s just energy as an industry which is just undergoing a dynamic shift

Hero motocorp is the largest manufacturer in the world. Access to tech, cash and network is not a problem at all.

Vida is already breathing on Athers neck and will be profitable thanks to Hero motocorps’ ecosystem.

For how long can Ather keep burning cash? Where will it keep getting cash from if it keeps posting losses? New age or not, cash is king.

Hero motocorp is sitting on 30% holding. Currently, hero is fighting ev race with 2 horses without brand dilution for Ather. If Vida wins, Ather can be acquired at a later date at a cheaper value where patents and tech are more valuable. If Ather wins, Vida can be merged with Ather and Hero still stays in the race. Its a win win.

Disc: not invest in Ather but following to see how Hero plays the game.

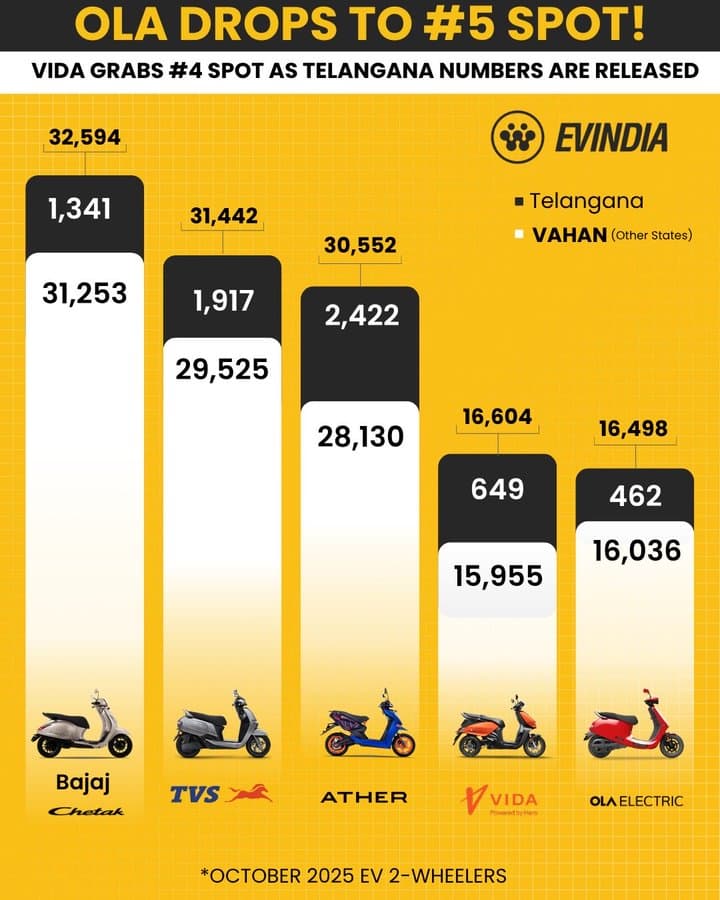

Offtopic: Ola was always a Lost cause because Bhavish is to narcissist for his or the company’s wellbeing. Ola desperately needs a partner/ investor to reign in Bhavish’s musings and steady the ship. OLAs latest diversification is a silent surrender in tje EV space in my opinion.

You are free to be bearish - when the tap turns positive, negative flows will be erased in no time.

There is no such tech that they can buy off. India is the most mature ev-2W market. No tier-1 engineer / designer / product guy wants to work for Hero Moto, but they all want to work for Ather.

Ather has continually increased market share over the last few months. It was placed no 4/5 a year back. Its solid no.3 today. Hero has gained at expense of Ola/Other smaller players. There is no one to gain market share from this point. TVS/BAJAJ keep fighting for 1-2.

Unless this changes significantly, these market shares will likely remain stable for now.

Remember a year back, Ather did not have stores across the entire East/North. Now they are building stores fast. In the south, they have a 35% MS. It is also impossible for Hero to buy out and delist the company. Shareholders won’t agree.

Ather is very close to becoming the top player. The difference in the top three is less than 5% now. Given that Ather has a superior product, I feel it should get to the number 1 spot soon.

I guess the difference lies in the distribution network. A combo of store expansions and increasing customer confidence, the brand shall gain better visibility, triggering a network effect.

Probably what you mean is “positive feedback loop” or “virtuous cycle” of growth?

In the strict tech sense, a network effect means the product becomes more valuable to each user as more people use it (like telephones, social networks, or payment platforms). An EV 2-wheeler doesn’t really have that. Your scooter doesn’t work better just because your neighbor bought one too.