Network Effect in this case means, that you have comfort in knowing you have bought right product.

Consumer version of no one is fired for buying IBM.

Network Effect in this case means, that you have comfort in knowing you have bought right product.

Consumer version of no one is fired for buying IBM.

With Price/Sales being @ 11, how do we see the current valuation? as there was a lot of a debate around it recently for IPO bound Lenskart.

Ather is yet to be PAN India player, scope and scale is huge , At Current Expansion phase this company can be 75k+ cr mcap company in 3 to 4 years.

Tarun has patience, he will do things in sustainable way

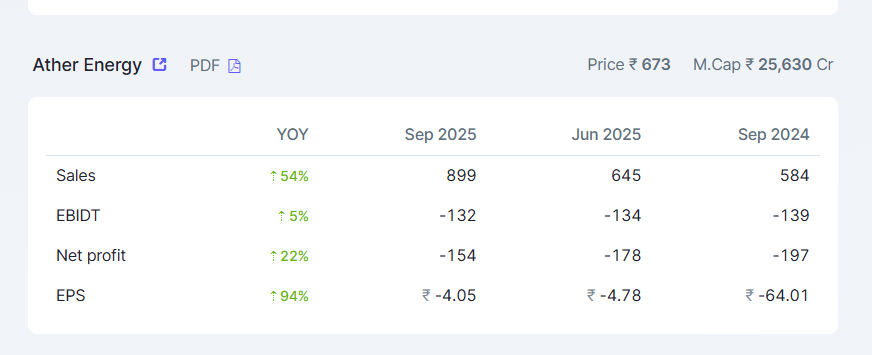

Revenue up 54% YoY, loss narrows

Price/sales now at 8 as per current FY performance and path to profitability appears quicker than expected due to Ola’s operational issues… strong runway to growth for long term

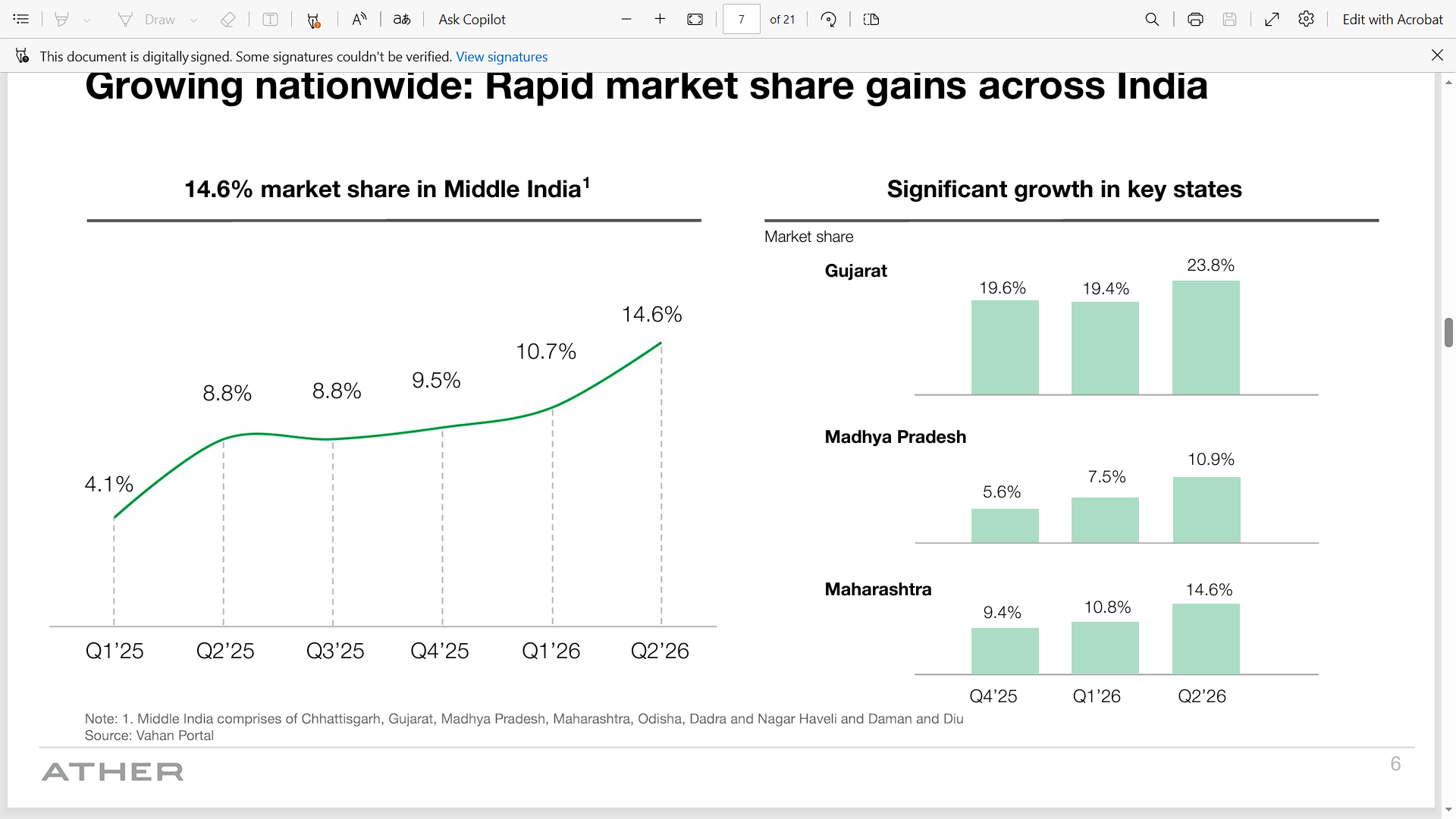

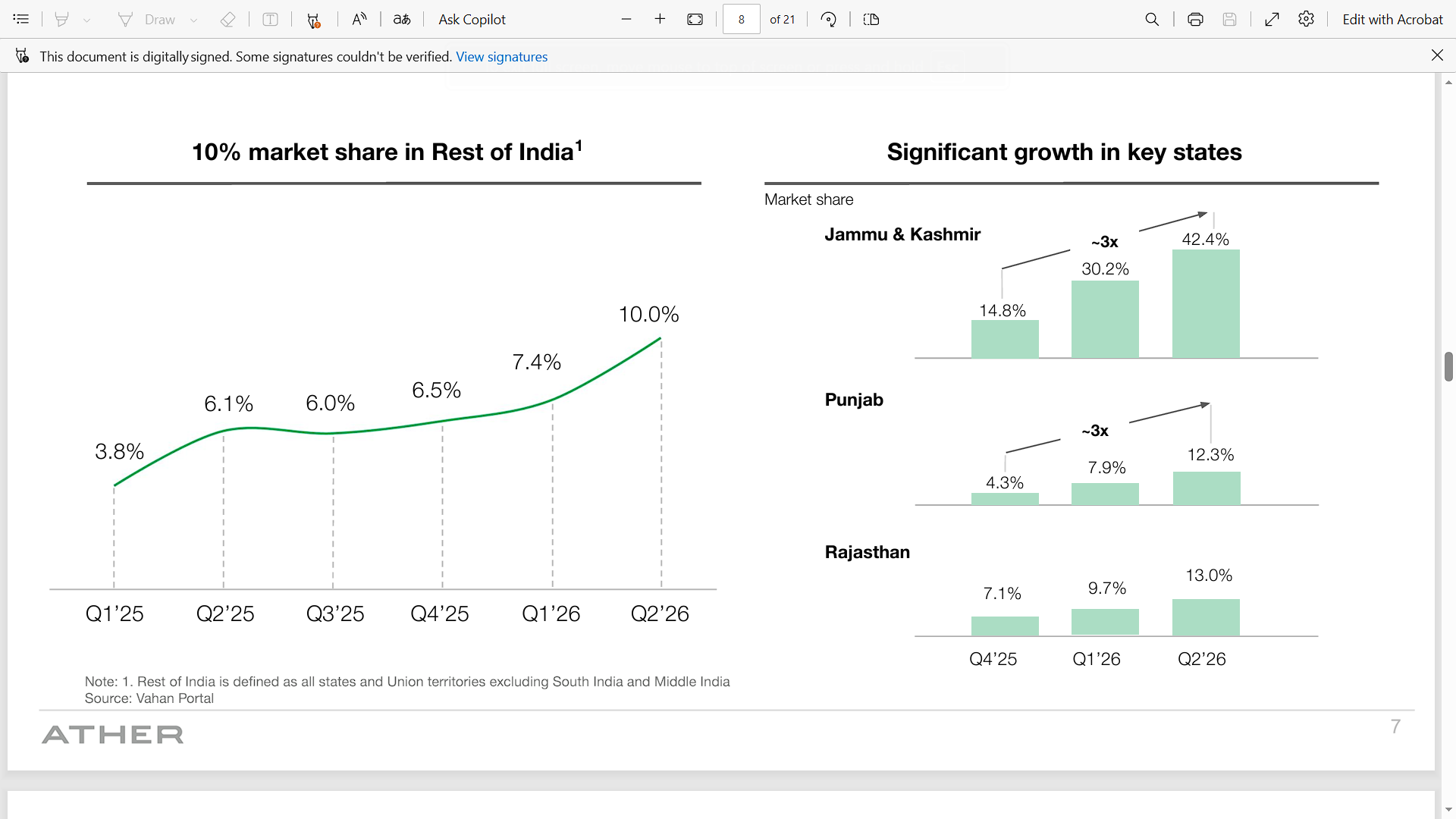

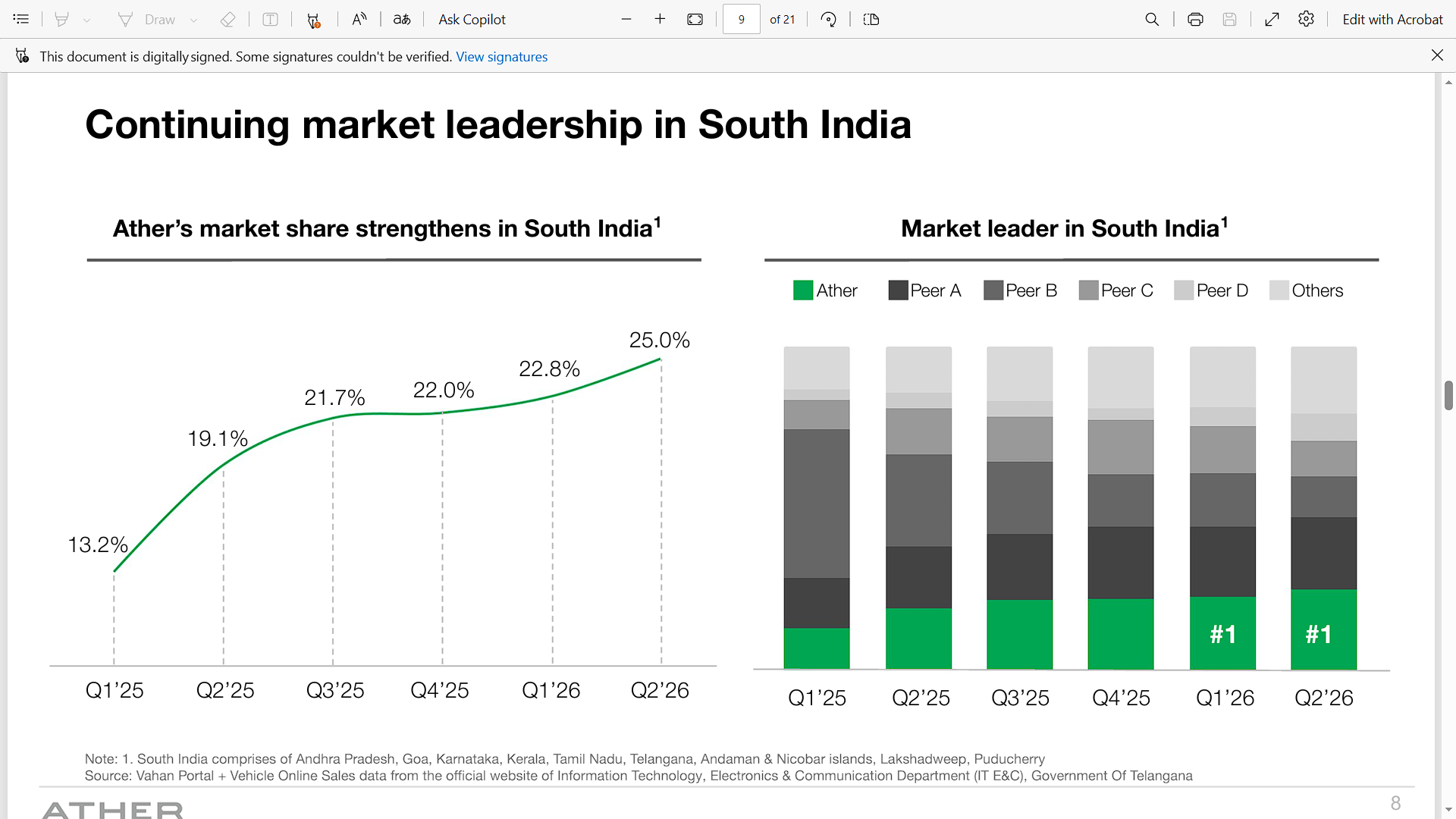

Others may post the results. I am more interested in MS across states.

So good results beyond their base in the south. This means they have capability to maintain this 15-17% market share for a longer period of time.

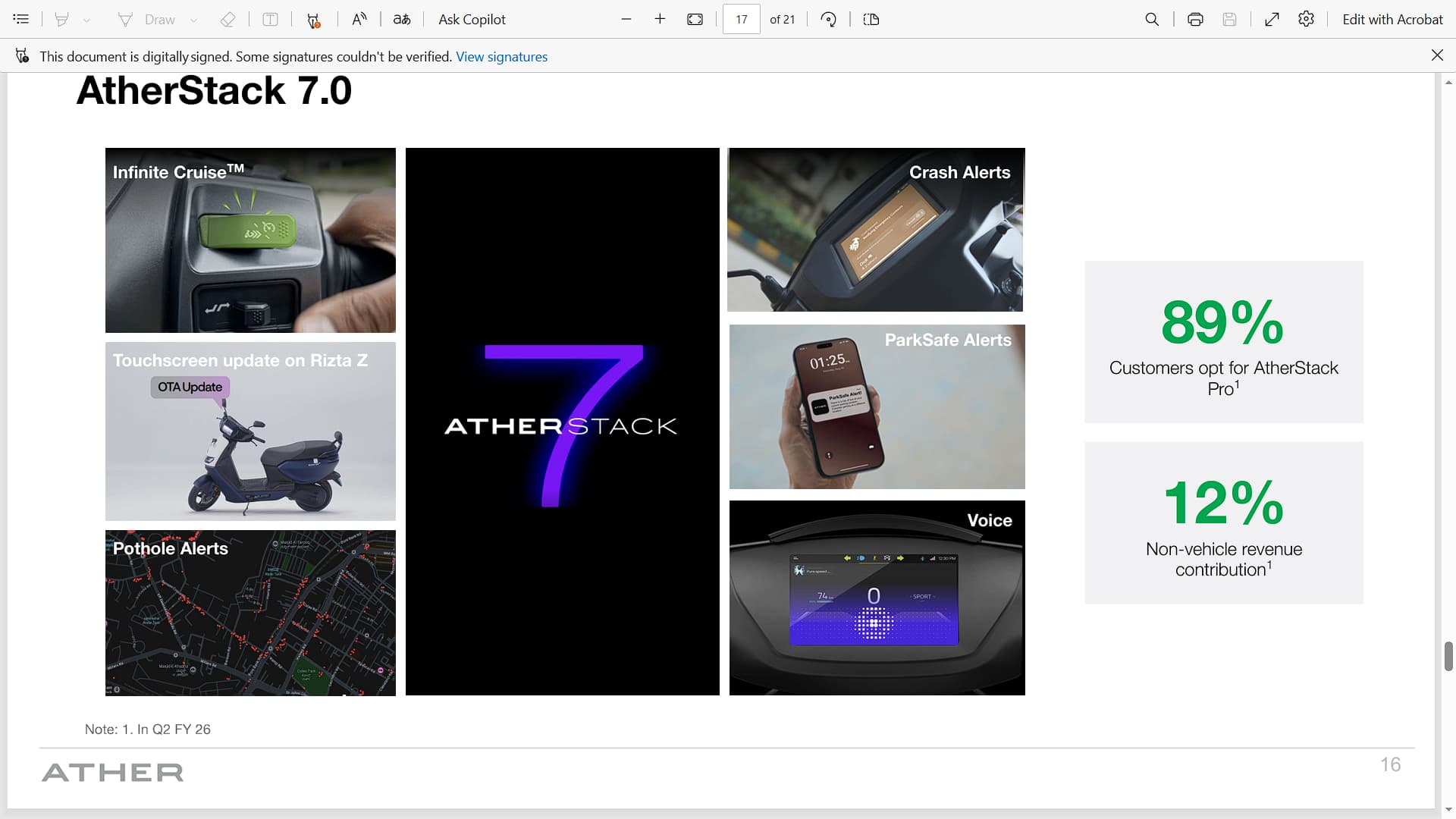

And major area where in future they can make good margins is the software stack.

Next moniterable would be Editda Neutral. Guess it would take one more year.

Recently did a plant vist of Hosur Facility.

4.2 lakh annual capacity.

Factory is not fully automated.

Place is owned by TVS Logistics.

Sambhajinagar factory will be 100 acre facility , initial 5 lakh capacity will be on 50 acre.

R&D is working on EL Platform scooters and Bikes 125-135 cc

EL Platform launch in 2026 prices will be close to 1lakh , company will not compromise on quality and reduce price.

Focus will be on quality

This is a tweet.

Ather Energy – The Growth Engine, Explained - Most investors still look at Ather through the old lens: premium EV brand, early adopters, high burn. - That lens is outdated. - What’s unfolding now is a classic execution-led scale-up, where multiple levers are starting to reinforce each other. Let’s break it down, step by step. ![]() The real inflection started with distribution, not demand - For a long time, Ather’s constraint wasn’t product or consumer interest. - It was reach. That changed over the last year.

The real inflection started with distribution, not demand - For a long time, Ather’s constraint wasn’t product or consumer interest. - It was reach. That changed over the last year. ![]() Retail footprint more than doubled in under 12 months

Retail footprint more than doubled in under 12 months ![]() Stores scaled from ~250 to ~550

Stores scaled from ~250 to ~550 ![]() Expansion followed portfolio readiness, not the other way around - Once distribution scaled, market share didn’t need discounts or push marketing, it followed naturally. - That’s why recent gains look structural, not seasonal.

Expansion followed portfolio readiness, not the other way around - Once distribution scaled, market share didn’t need discounts or push marketing, it followed naturally. - That’s why recent gains look structural, not seasonal. ![]() Rizta wasn’t a cheaper scooter, it was a market unlock - Rizta is frequently misread as a mass product. - Its real role was different:

Rizta wasn’t a cheaper scooter, it was a market unlock - Rizta is frequently misread as a mass product. - Its real role was different: ![]() Address family and mainstream use cases

Address family and mainstream use cases ![]() Unlock non South markets

Unlock non South markets ![]() Do it without breaking pricing discipline The result:

Do it without breaking pricing discipline The result: ![]() Gujarat moved from ~5% to ~25% market share

Gujarat moved from ~5% to ~25% market share ![]() Maharashtra & Madhya Pradesh started delivering real volumes - This wasn’t brand dilution. - It was addressable market expansion.

Maharashtra & Madhya Pradesh started delivering real volumes - This wasn’t brand dilution. - It was addressable market expansion. ![]() Premium is a lazy label - Ather’s strategy isn’t about staying premium for its own sake. - It’s about riding India’s upgrade cycle. - Data supports this:

Premium is a lazy label - Ather’s strategy isn’t about staying premium for its own sake. - It’s about riding India’s upgrade cycle. - Data supports this: ![]() 125cc scooters are the fastest growing ICE segment

125cc scooters are the fastest growing ICE segment ![]() EV demand is strongest above ₹1 lakh - That’s why Ather sustains a 15 to 25% pricing premium, even while expanding rapidly. - Not because it refuses to go mass. - Because the mass itself is upgrading.

EV demand is strongest above ₹1 lakh - That’s why Ather sustains a 15 to 25% pricing premium, even while expanding rapidly. - Not because it refuses to go mass. - Because the mass itself is upgrading. ![]() Scale is now flowing into the P&L - This is where narratives turn into numbers.

Scale is now flowing into the P&L - This is where narratives turn into numbers. ![]() Volume growth: ~100% YoY in Q1, ~60% in Q2

Volume growth: ~100% YoY in Q1, ~60% in Q2 ![]() Revenue scaled from ₹408 Cr (FY22) to ₹1,543 Cr annualized run rate (Q2 FY26)

Revenue scaled from ₹408 Cr (FY22) to ₹1,543 Cr annualized run rate (Q2 FY26) ![]() Gross margins expanded to ~22% - Importantly, margins improved despite subsidy noise, pointing to genuine unit-economics improvement.

Gross margins expanded to ~22% - Importantly, margins improved despite subsidy noise, pointing to genuine unit-economics improvement. ![]() Profitability is being built the right way - Ather’s path to profitability doesn’t hinge on one future launch. - Two engines are already at work: Engine 1 – Unit Economics

Profitability is being built the right way - Ather’s path to profitability doesn’t hinge on one future launch. - Two engines are already at work: Engine 1 – Unit Economics ![]() 6 to 9% annual cost reduction

6 to 9% annual cost reduction ![]() Engineering led margin expansion Engine 2 – Operating Leverage

Engineering led margin expansion Engine 2 – Operating Leverage ![]() Volumes compounding

Volumes compounding ![]() Fixed costs largely in place

Fixed costs largely in place ![]() EBITDA losses already in single digits - The upcoming EL platform is upside, not a rescue lever. - That distinction matters.

EBITDA losses already in single digits - The upcoming EL platform is upside, not a rescue lever. - That distinction matters. ![]() The flywheel is now visible - Distribution → Market share → Pricing power → Margins → Operating leverage. - Each lever strengthens the next. - This is no longer an EV adoption story. - It’s a scaling business model story.

The flywheel is now visible - Distribution → Market share → Pricing power → Margins → Operating leverage. - Each lever strengthens the next. - This is no longer an EV adoption story. - It’s a scaling business model story. ![]() Investor Compass Takeaway - Ather has crossed the hardest phase.

Investor Compass Takeaway - Ather has crossed the hardest phase. ![]() Product risk is behind

Product risk is behind ![]() Distribution is scaling

Distribution is scaling ![]() Pricing power is intact

Pricing power is intact ![]() Operating leverage is visible - What remains is execution compounding, quarter after quarter. - That’s usually when perception changes, slowly at first, then all at once. No Buy/Sell recommendation #StocksInFocus #StocksToWatch #atherenergy #ather #EV

Operating leverage is visible - What remains is execution compounding, quarter after quarter. - That’s usually when perception changes, slowly at first, then all at once. No Buy/Sell recommendation #StocksInFocus #StocksToWatch #atherenergy #ather #EV

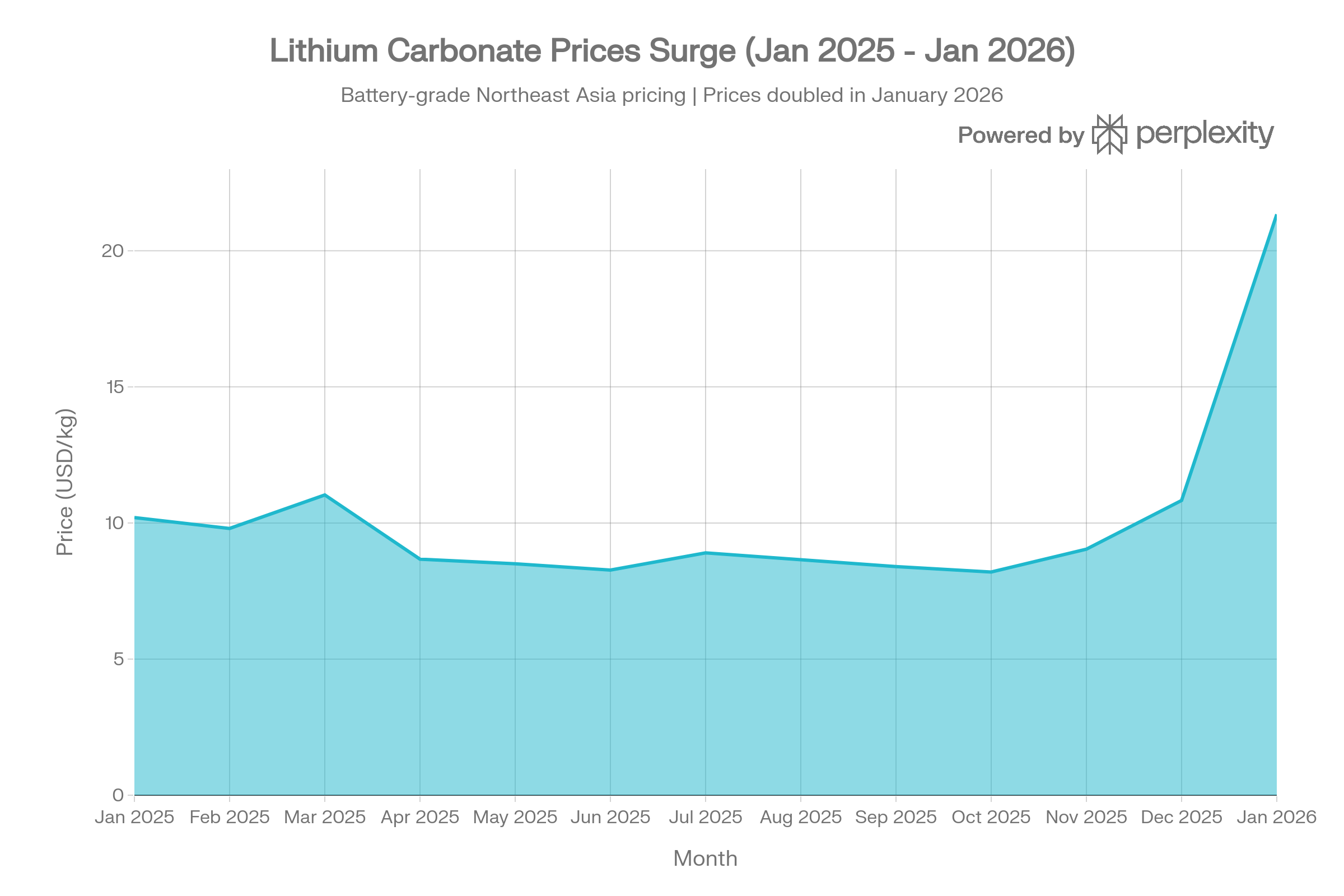

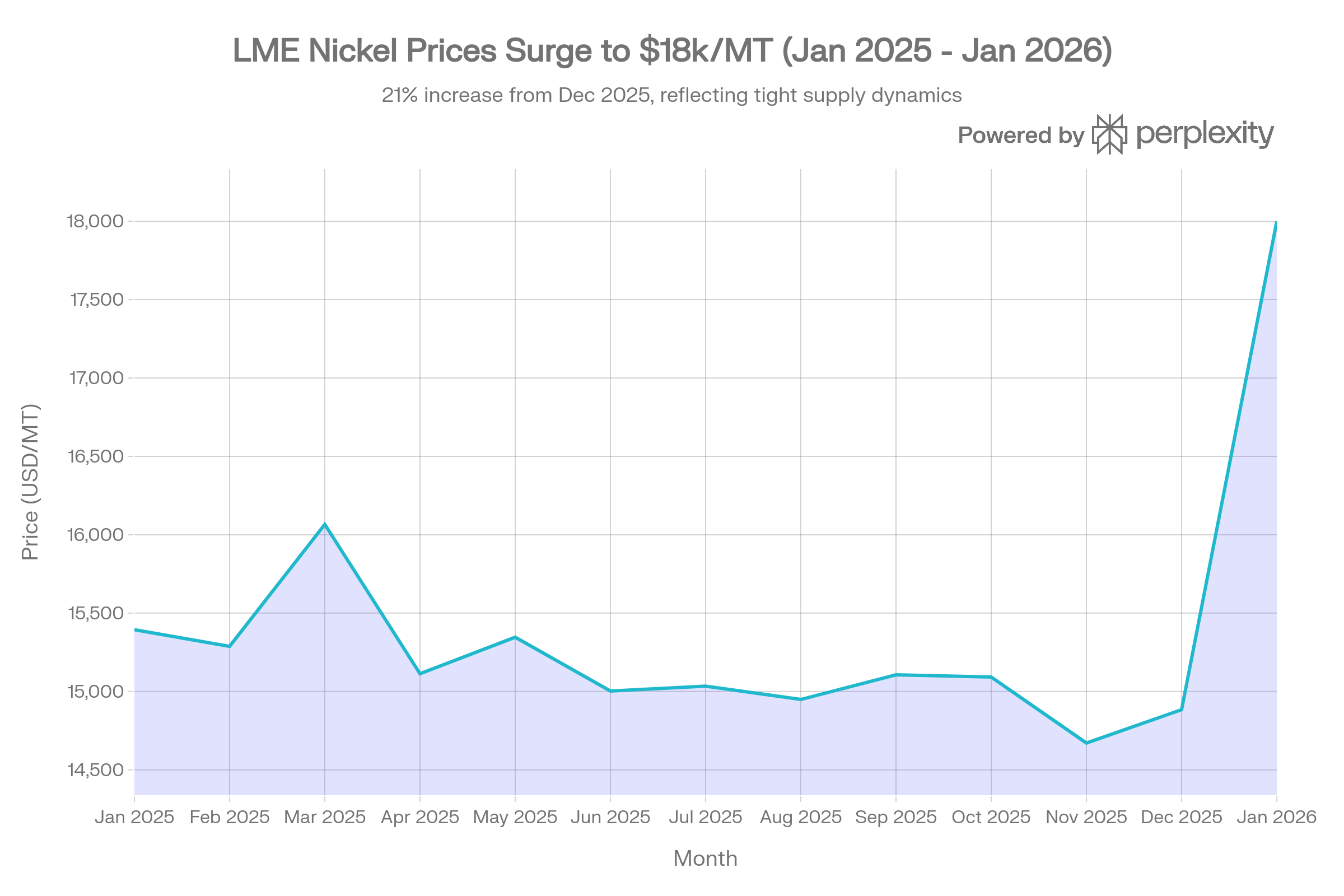

After USA attack on Venezuala , China too is playing it’s card and prices of Lithium and Nickle have risen sharply .

This will hurt gross margins of all EV’s. What will be the degree of margin reduction needs to be asked in the next concal to the management.

And what’s the plan to mitigate this problem.

What is cooking in Ather?

ABU DHABI INVESTMENT AUTHORITY

Bought 352,817 of

Ather Energy Ltd. ( Block Deal on BSE, 11 Feb 2026 )

ICICI PRUDENTIAL MUTUAL FUND

Bought 563,380 of

Ather Energy Ltd. ( Block Deal on BSE, 11 Feb 2026 )

ICICI PRUDENTIAL MUTUAL FUND

Bought 563,381 of

Ather Energy Ltd. ( Block Deal on NSE, 11 Feb 2026 )

MORGAN STANLEY ASIA SINGAPORE PTE

Bought 602,883 of

Ather Energy Ltd. ( Block Deal on NSE, 11 Feb 2026 )

ADITYA BIRLA SUN LIFE MUTUAL FUND

Bought 704,226 of

Ather Energy Ltd. ( Block Deal on NSE, 11 Feb 2026 )

SOCIETE GENERALE

Bought 352,115 of

Ather Energy Ltd. ( Block Deal on BSE, 11 Feb 2026 )

Disclosure: Invested in the stock, could be biased. Added the new video link.

This video looks to be private.

Possible to share few key points if you have access to this. TIA.

Edited the new video link, take a look at the post again.

The month also saw a surge in demand ahead of the Centre’s PM E-DRIVE subsidy deadline.

According to registration data from the government’s Vahan portal, total electric two-wheeler registrations stood at 1,39,238 units during the month.

According to registration data from the government’s Vahan portal, total electric two-wheeler registrations stood at 1,39,238 units during the month. TVS Motor led with 38,007 units, translating to a 27.3 percent market share. On a quarter-to-date (Q4 FY26) basis, the company maintained its lead with 34,885 units and a 27.9 percent share.

Bajaj Auto ranked second with 33,447 registrations, accounting for 24 percent of the market, supported by continued demand for its Chetak electric scooter. Ather Energy followed in third place with 26,151 units and an 18.8 percent share, driven by steady volumes from its 450 series and from its family scooter Rizta .

Hero MotoCorp’s electric mobility brand Vida secured the fourth position with 15,683 registrations and an 11.3 percent market share, reflecting gradual scale-up and wider availability across cities.

Ola Electric recorded 6,381 units in March, with its market share at 4.6 percent, placing it fifth in the market.

Among other players, Ampere registered 5,378 units with a 3.9 percent share, while River recorded 3,135 units (2.3 percent). BGauss reported 2,296 units, accounting for 1.6 percent of the market. Pure EV and other smaller manufacturers together contributed limited volumes, with Pure EV at 259 units and a 0.2 percent share.

The “Others” category, comprising multiple smaller and emerging manufacturers, accounted for 8,501 units, or 6.1 percent of total registrations during the month.

For a comparison, In February 2026, total electric two-wheeler registrations stood at 1,01,059 units. TVS Motor led with 29,231 units and a 28.9 percent market share, followed by Bajaj Auto at 22,942 units (22.7 percent) and Ather Energy at 18,726 units (18.5 percent). Vida recorded 11,356 units (11.2 percent), while Ampere and Ola Electric reported 4,203 units (4.2 percent) and 3,783 units (3.7 percent), respectively. River and BGauss registered 2,018 and 1,849 units, while smaller players together accounted for 5,521 units.

Disclaimer: Invested in Ather. Biased. No recommendation.

While Ola was shrinking stores to ~550, Ather went from 524 → 600 ECs and is targeting 1,100+ by March 2027.

Add the Rizta (60% of sales volume), the Ather Grid (4**,357** fast chargers), and a market share jump from 12.1% to 18.8% in just 4 quarters.

Ola had the head start. Ather had the discipline

Would Ola’s assertion of improvement in service benefit it?