Ather Energy

1. History of the company

The story of Ather Energy began in 2013 when two IIT Madras students, Tarun Mehta and Swapnil Jain, set out to revolutionize electric vehicles (EVs) in India.

Initially exploring energy solutions like battery swapping, the company was named as Ather Energy as the initial focus was on developing an alternative energy solution that was cheaper and more efficient than ICE vehicles. They soon realised the core problem was poorly designed electric vehicles.

This led them to a bold decision: rather than just making batteries, they would create India’s first smart electric scooter.

In December 2014, Flipkart founders Sachin Bansal and Binny Bansal invested $1 million as seed capital. Sachin Bansal and Binny Bansal expressed positive sentiments towards the company and showed an inclination towards energy-efficient vehicles.

Inspired by Tesla, they aimed to build a scooter better than petrol vehicles, both in performance and design.

So in 2016, Ather introduced the S340, a breakthrough with a touchscreen dashboard and connected features at a technology conference Surge in Bengaluru, which was the first step towards transforming India’s E2W market into a smart and sustainable mobility ecosystem.

But building an EV from scratch in India was no small feat. They faced significant challenges, especially when it came to sourcing quality parts from local vendors who weren’t equipped to meet Ather’s high standards - causing delays in production.

But the turning point came when Hero MotoCorp invested ₹205 crores, providing the capital and industry connections required to scale.

So in 2018, Ather launched the Ather 450, India’s fastest electric scooter at the time.

In December 2019, Ather Energy signed an MoU with the Government of Tamil Nadu to set up a 400,000-square-foot manufacturing plant for electrical vehicles in Hosur. The invested amount will be around ₹635 crore.

By 2021, thanks to cost-cutting measures and strategic partnerships with industry giants like Hero, Ather was finally able to achieve positive gross margins.

Ather wasn’t content with just being another scooter company—they wanted to change the game entirely. They introduced industry-first features like the Ather Grid, a fast-charging network, and their proprietary AtherStack software, offering over-the-air updates, ride statistics, and cloud integration.

In 2024, they launched the ‘Rizta’ series, targeting the family scooter market with features like 56L of storage space and an industry-first traction control system.

Source: https://growthx.club/blog/ather-energy-business-model

Tarun Mehta

Tarun is the co-founder and CEO of Ather. Mehta is an IIT Madras alumnus who has completed a dual degree in engineering design before starting as a deputy manager at Ashok Leyland. He eventually decided to find Ather. Mehta interned at Mercedes Benz and BHEL during his college days.

Swapnil Jain

Swapnil Jail is the co-founder of Ather. He is also an alumnus of IIT Madras and has completed his integrated Master of Technology in Engineering Design. After completing a brief internship at General Motors and BHEL, Swapnil decided to find Ather with his college friend Tarun.

Source: Ather Story: Founders | Business Model | Logo | Tagline

2. History of EV vehicles in India with a focus on 2W:

Efforts for introducing electric two-wheelers started in India in the 1990s. Companies like Bajaj

Auto, Scooters India Ltd. and Hero Motor Corporation etc. developed electric two-wheelers. The Ministry of New and Renewable Energy (MNRE) offered subsidy on electric vehicles during 2010-12. However, such efforts did not sustain and the sales of electric vehicles dropped significantly once subsidy was withdrawn.

After the launch of the FAME scheme, many new electric two-wheeler manufacturers have emerged and even the established ones have joined the race. Start-up companies such as Ather Energy, Okinawa, Pure EV and Ampere Vehicles etc. have established EV 2/3 wheeler manufacturing capacities and plan to expand them further. Ola has announced an ambitious plan for manufacturing and companies such as Hero Electric and Bajaj Auto etc. have also set up manufacturing facilities for the electric 2/3 wheelers.

Source: Niti Aayog

1. Sales growth of 2W vs 4W EVs:

Rise in 2w ownership for personal mobility:

Source: Niti Aayog

2W sales trend:

Expected EV penetration by vehicle class:

Reasons for low penetration:

Expected growth of E2W:

Sales growth of EVs across vehicle class:

3. Current landscape of EV market in India (all categories):

Currently we can see a lot of consolidation in the 2w EV market especially after reduction of government incentives, bold startups such as Simple energy,an Indian electric vehicle startup founded in 2019, released its first mass-market motorcycle, the Simple ONE, in 2021. However, deliveries were delayed to June 2022 and then again to January 2023. Deliveries to customers finally began in June 2023, and to date, Simple Energy has sold 639 units.

Even though they have managed to raise $20mn in seed funding, it is not sufficient at all considering Ather has raised total equity funding of $502 million in 19 rounds and is further proposed to raise money in its upcoming IPO.

Many e2W OEMs such as Ampere, Benling, Bgauss, Hero Electric, Joy, Komaki, Pure EV and Revolt wrongly claimed benefits under the FAME-II scheme in violation of the local sourcing requirements and engaged in rampant imports of vehicle parts. Thus they were asked to return the benefits claimed under the scheme. Due to stringent requirements for local sourcing of components, many of these OEMs have been blacklisted from all central schemes, making them ineligible for the PLI scheme and consequently less competitive in the market.

Source: Antique Stock Broking

Reasons for low penetration of EV in 4W:

Source: Bain Research

1. Small insights into global EV market

Global 2w EV sales breakup:

Globally EV sales are slowing, Tesla in its concall highlighted how competitive the EV market has become with the entry of chinese EV makers. Also Hybrid vehicles are getting more acceptance from customers and legacy auto makers are launching more hybrid models.

Source: Tesla Concall

Source: Goldman Sachs

4. How is an EV different from an ICE vehicle?

1. Power Delivery and Acceleration:

Internal Combustion Engine (ICE) Vehicles: ICE vehicles have long been the backbone of personal transportation, characterized by their internal combustion engines fueled by gasoline or diesel. These engines offer a broad spectrum of power outputs, ranging from economical options to high-performance models. The power delivery of ICE vehicles is characterized by gear shifts and engine RPMs, providing drivers with a familiar and dynamic driving experience. Acceleration is influenced by factors such as engine displacement and turbocharging.

Electric Vehicles (EVs): EVs offer an entirely different paradigm of power delivery due to their electric motors. Instantaneous torque delivery is a hallmark of EVs, resulting in swift and seamless acceleration from a standstill. Unlike ICE vehicles, EVs have a linear power delivery, eliminating the need for gear shifts. This translates into a smooth and exhilarating driving experience. As a result, EVs can often achieve impressive acceleration figures, making them competitive even in high-performance categories.

2. Performance Metrics:

Internal Combustion Engine (ICE) Vehicles: ICE vehicles have diverse performance metrics, including horsepower (hp) and torque (lb-ft). These metrics define the engine’s power output and its ability to generate rotational force. High-performance ICE vehicles often boast high horsepower figures to achieve impressive top speeds and acceleration.

Electric Vehicles (EVs): EVs are characterized by their power output in kilowatts (kW) rather than traditional measures like horsepower. While direct comparisons between kW and hp can be complex due to differences in power delivery, many modern EVs exhibit robust power figures. The instant torque delivery of electric motors contributes to brisk acceleration, which often outpaces equivalent ICE models.

3. Driving Experience:

Internal Combustion Engine (ICE) Vehicles: ICE vehicles provide a dynamic driving experience that enthusiasts have cherished for decades. The rumble of an internal combustion engine, gear shifts, and the connection between the throttle and engine RPMs contribute to a sensory driving experience that is deeply ingrained in automotive culture.

Electric Vehicles (EVs): EVs offer a futuristic driving experience characterized by quietness and seamless power delivery. The absence of engine noise, coupled with the immediate torque response, creates a unique driving sensation. Many EVs feature regenerative braking, which can provide additional control and energy recapture during deceleration.

4. Top Speed and High-Performance Models:

Internal Combustion Engine (ICE) Vehicles: Historically, high-performance ICE vehicles have dominated the realm of top speeds. Supercharged and turbocharged engines have pushed the boundaries of speed, leading to the creation of iconic sports and supercar models.

Electric Vehicles (EVs): The rise of high-performance EVs challenges the notion of speed. The instant torque delivery of electric motors contributes to rapid acceleration, enabling many EVs to achieve impressive top speeds. Electric hypercars and performance-focused EV models have showcased the potential of electric propulsion in achieving remarkable speeds.

5. Adaptability and Customization:

Internal Combustion Engine (ICE) Vehicles: ICE vehicles are renowned for their adaptability and customizability. Enthusiasts can modify engines, exhaust systems, and suspension components to tailor the driving experience to their preferences. The aftermarket industry for ICE vehicles is vast and diverse.

Electric Vehicles (EVs): While customization options for EVs are growing, they are not as extensive as those for ICE vehicles. Modifications often focus on software updates, battery management, and performance tuning. However, the growing interest in EVs is likely to spur the development of a more robust aftermarket ecosystem.

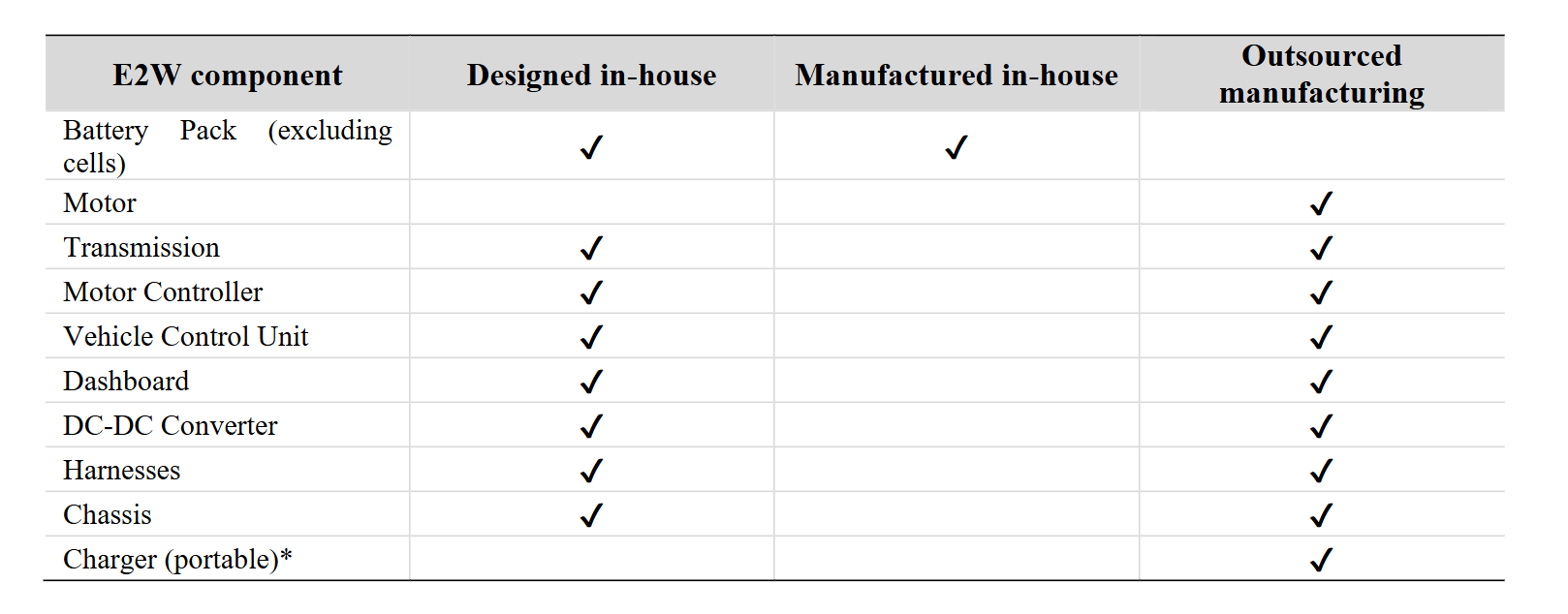

- What’s the difference between EV and ICE vehicle manufacturing?

Powertrain: The most significant difference is that EVs use electric motors and batteries to power their wheels, while ICE vehicles use an internal combustion engine that runs on gasoline, diesel, or another fuel. As a result, EVs have fewer moving parts, and the powertrain is more compact and easier to manufacture.

Battery production: EVs require a large battery to store and provide energy to the electric motor. Battery production is a complex and costly process, which involves sourcing and processing rare earth metals, manufacturing and assembling battery cells, and testing and validating the battery’s performance and safety.

Lightweight materials: EVs need to be lightweight to maximize their range and performance. Automakers are using lightweight materials, such as aluminum, carbon fiber, and composite plastics, to reduce the weight of EVs while maintaining their structural integrity and safety.

Software integration: EVs require advanced software systems to manage the battery, powertrain, and other components. Automakers need to integrate software and hardware seamlessly to ensure that the vehicle performs as expected and meets safety and regulatory requirements.

Auto ancillaries catering to EV parts:

List of Key EV components:

Listed Auto Ancillaries supplying key EV components:

1. Battery Cell:

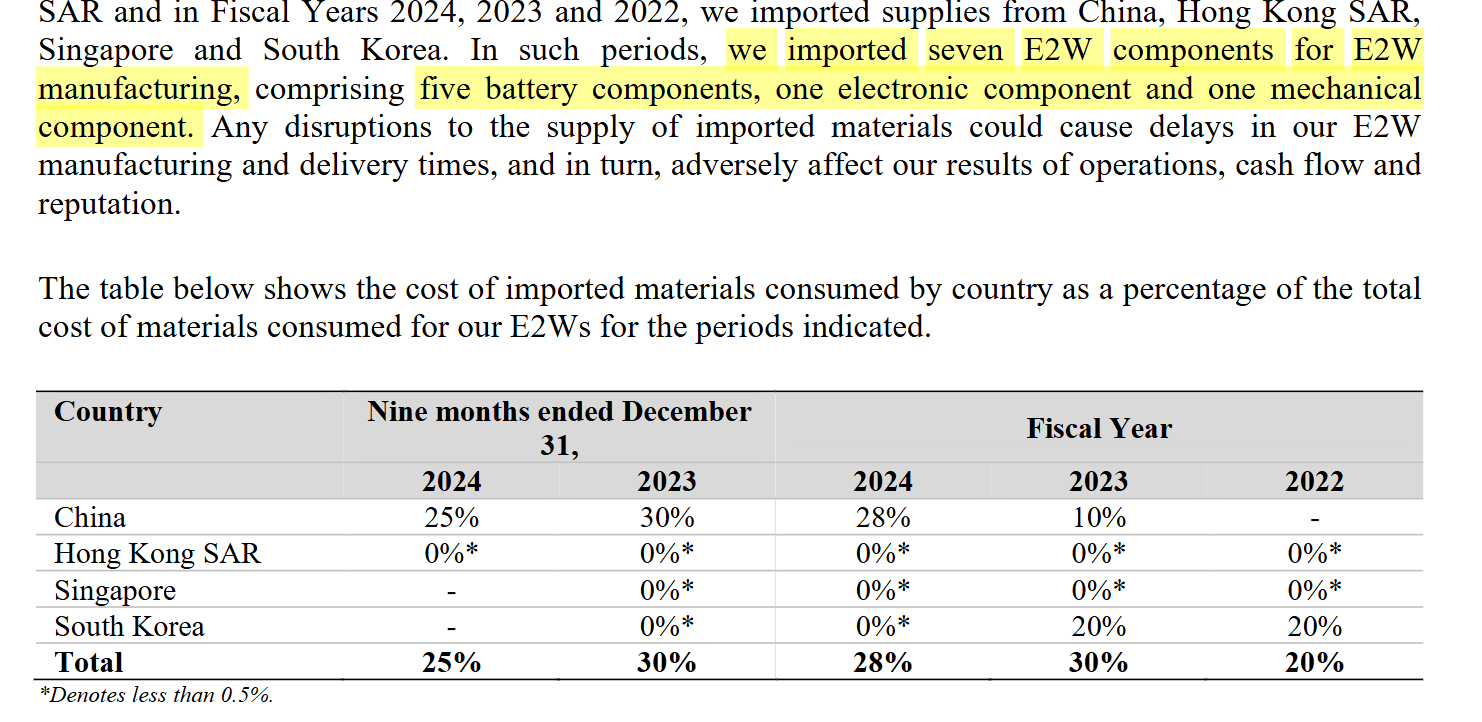

Currently Ather is completely dependent on China for lithium ion cells, it also has no plans to backward integrate into this category.

Currently only Ola is planning to backward integrate and Ather has signed a collaboration agreement with Amara Raja to de-risk themselves.

Exide Industries also plans to commercialize its phase 1 lithium ion cell project in FY25.

2. Power Electronics, Motor, BMS and Power converters:

Sterling Tools: It is the largest MCU manufacturer for EV Industry in India. It has plans to expand its EV portfolio.

Sandhar Tech: It has started manufacturing DC-DC converters, battery chargers and monitor controllers. It aims to cover almost the entire value chain for EV market.

Varroc Engineering:

Its current EV portfolio:

It also plans to cover the entire value chain for EV products.

Shriram Pistons:

It has acquired EMFI and plans to manufacture motor and motor controllers. It also has signed a technical collaboration agreement with Wuxi Lingbo for Controllers and Shenzhen Greatland Electrics for all kinds of Motors.

Uno Minda:

It aims to cover the entire electronics value chain and increase its EV kit value.

Entered into a Technology License Agreement (TLA) with StarCharge Energy to manufacture wall-mounted AC chargers for EVs.TLA with Suzhou Inovance for manufacturing high-voltage EV products.

Minda Corporation:

It has a similar strategy of increasing EV kit value. Its EV components include:

Bosch:

It offers powertrain solutions for electric vehicles and also manufactures motors. It does not give a break up of its EV business so it is difficult to understand its product portfolio for EV.

Steel Strips Wheels Ltd:

It has announced a JV with Israel’s Redler Technologies and plans to enter into the motor controller business.

Steel Strip Wheels to set up EV joint venture with Israel’s Redler Technologies (moneycontrol.com)

Exicom:

It manufactures AC charges as well as DC chargers.

It also supplies power convertors for fast charging applications to Ather energy and Hero Motor.

Servotech:

It basically supplies DC chargers, its business majorly comprises B2G contracts.

Sona Comstar:

It is one of the most dominant suppliers of EV components and is a major supplier to Tesla too.

3. Chassis and Body:

Ask Automotive:

The company has 11 new programs under development in the EV sector.

Sansera Engineering and Endurance Tech: They are into small Aluminium Die-cast components for EV applications.

Alicon Castalloy:

They supply many critical parts to Ather.

Craftsman Automation:

Benefiting from EV tailwinds as it is a leader in precision manufacturing in high pressure aluminum die casting.

Source: Valuepickr

Demand and Supply Economics:

1. Where are parts produced:

Local Sourcing of 99% parts except lithium ion cells makes makes them eligible for government subsidies and lowers their costs as well.

2. Where is max demand from:

Ather has recently started to expand internationally, it also wants to become a pan - India player and thus has expanded to 154 cities with 208 experience centers. Currently it derives 68% of sales from South India which should reduce when their new stores become mature.

3. Where is max supply from:

It has plans to commence phase 1 production from its Aurangabad plant by 2027, further reducing its logistic costs.

4. Are costs going up or down?

Battery pack comprises about ⅓ cost of a scooter. Currently Global Battery prices are expected to further go down.

Ather has managed to reduce costs through better sourcing and higher scale and its COGS per unit has reduced.

5. Are there any bottlenecks?

It has certain bottlenecks with respect to certain parts where it is reliant on a single supplier.

5. Ather Energy Past and Current Performance (Products and Key Points):

Current Product Portfolio of Ather:

Ather Accessories:

Ather Pro pack and connect subscription:

Ather Fast Chargers:

Ather Energy has transitioned its Ather Grid fast charging network from a free service to a paid one. This marks a significant shift for the company, which previously offered free charging to encourage EV adoption. Despite the change, Ather Grid remains the largest fast charging network in India with 1973 chargers nationwide, aiming to address range anxiety concerns for new EV owners.

Ather Neighbourhood chargers:

Key Performance Highlights:

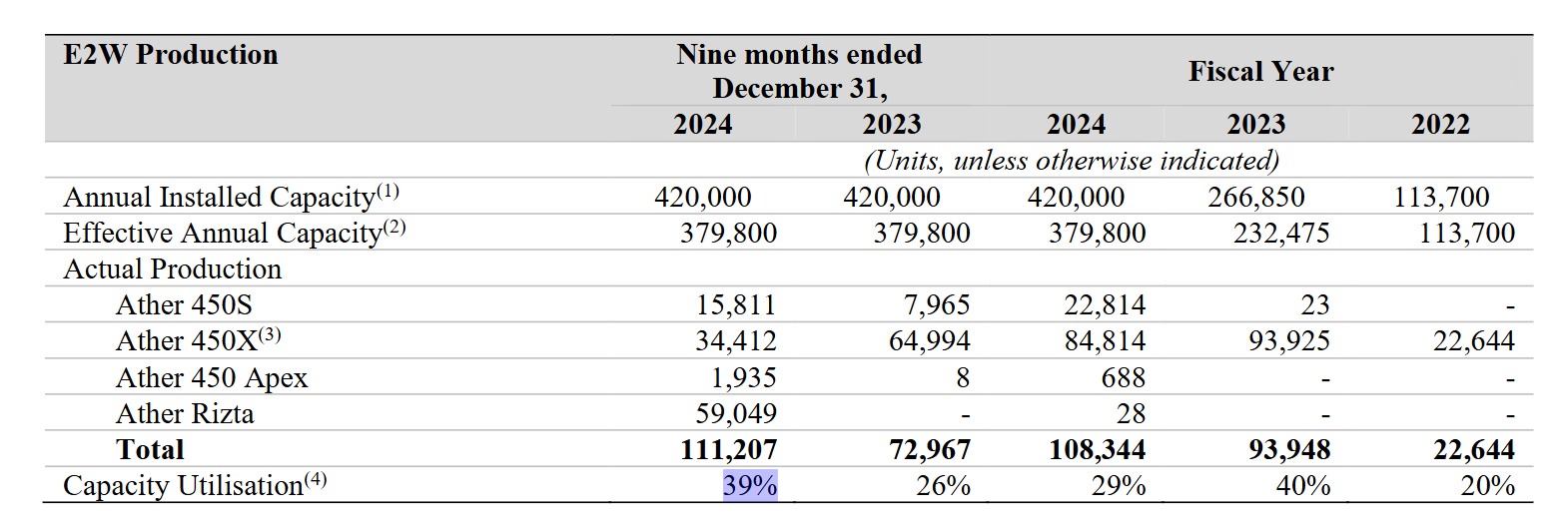

Ather’s market share growth has been sustained, but the recent reduction in government subsidies has slowed its sales momentum and decreased revenue per unit. The introduction of the Rizta model could further lower revenue per unit. Ather’s low capacity utilization of 29% presents an opportunity for significant operating leverage as it scales up its sales.

6. Ather Energy future plans (motorcycles?):

Scooters:

Ather Energy’s DRHP outlines plans for a new, more affordable scooter positioned below the Rizta. Leveraging their brand recognition and economies of scale. My guess is that it would be a sub 1 lakh Rs mass market model. They would utilize their new Factory 3.0 expected to commence production by 2027 equipped with enhanced automation to manufacture them.

Motorcycles:

Currently ICE motorcycles have higher sales than scooters, thus there is a lot of opportunity to capture with currently very few EV motorcycles in the Indian market.

Ather is planning to introduce EVs targeting the mass market premium range from 125 cc to 300cc on the zenith platform.

New Battery platform:

Ather Energy is developing a new battery platform to reduce costs and mitigate risks associated with rare earth materials used in traditional permanent magnets.