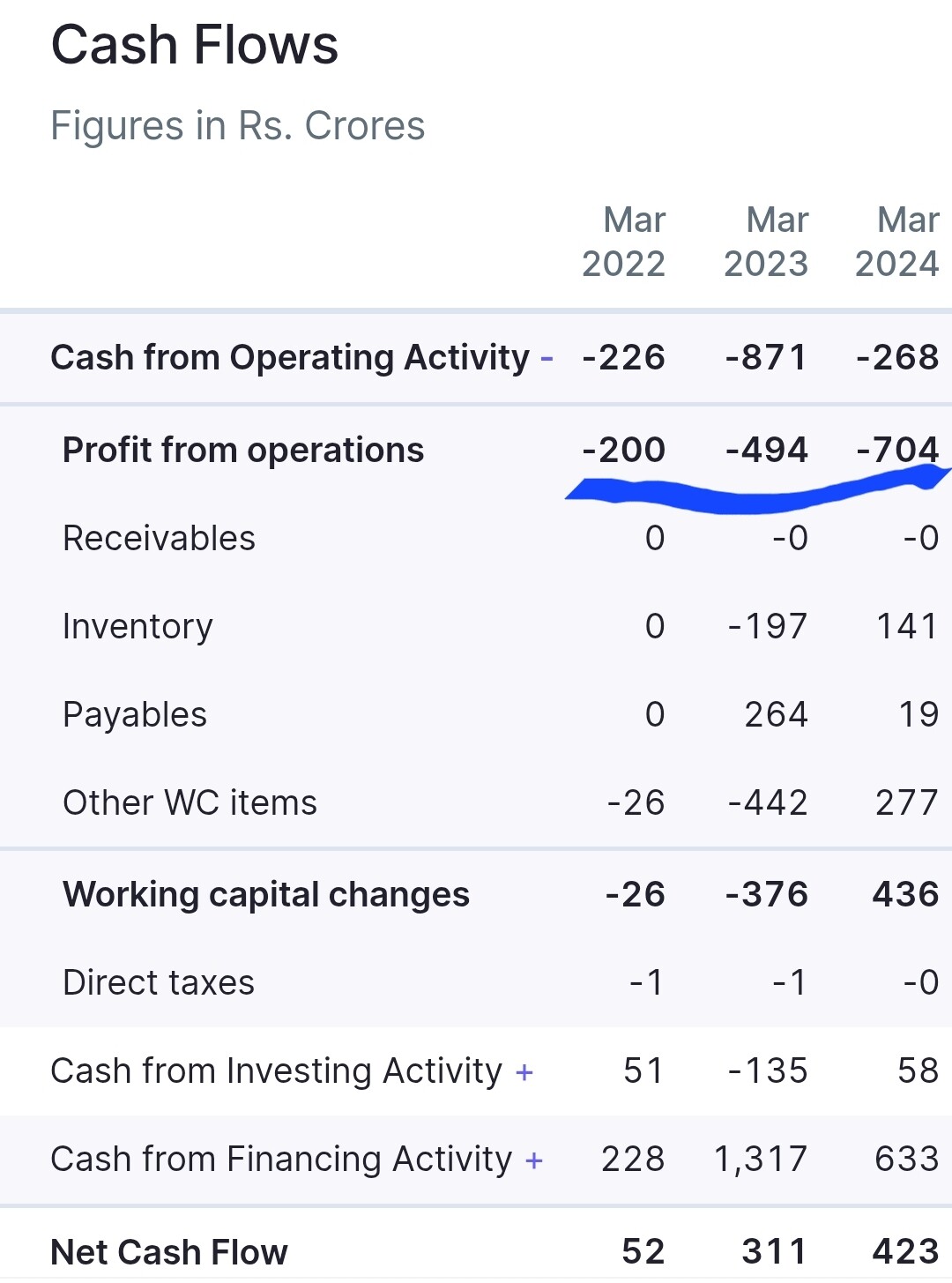

Are they expecting to generate positive profit from operations anytime soon?

I am not holding any position.

Ather stock analysis report by Hdfc securities

HDFC_Securities_Initiating_Coverage_on_Ather_Energ_250616_191937.pdf (1.5 MB)

1 Like

Smaller EV players nearly wiped out as FAME-II crackdown triggers sales collapse

1 Like

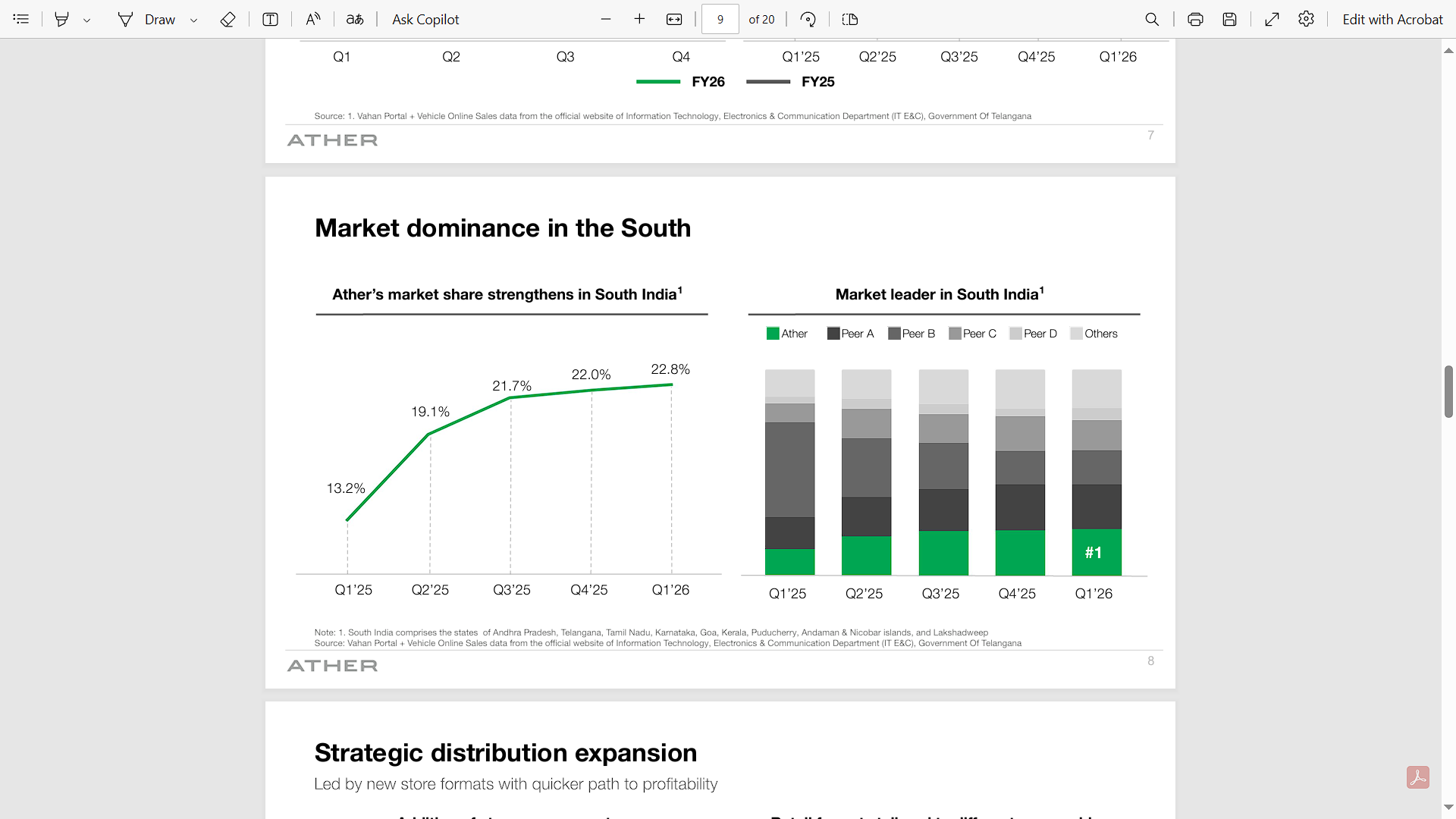

So Ather overtook Ola to grab no. 3, is it the first time?

3 Likes

Anybody has information about the ownership of showrooms. Basically Company owned vs franchisee owned split

1 Like

Taken from Ather DHRP:

“The company has built a strong dealer network with 265 Experience Centers (ECs) across India as on December 31, 2024. They also have a dealer network present in Nepal and Sri Lanka with 5 and 10 ECs respectively. Out of this 280 ECs globally, 3 ECs are Company Owned Company Operated (COCO)”

3 Likes

Thesis

-

I expect 60% penetration of electric vehicles till CY 2035.

-

Ather Energy would be able to capture 20% market share of the total two-wheeler EV market.

-

Operating margins would increase on the back of higher utilization of current facilities, economies of scale, and the company switching to lower-cost tech like the shift from NMC to LFP battery technology. Also, the increase in revenue share from accessories and their software stack will contribute.

-

The competitive advantage of the business (moat) would be brand, higher quality product, charging network, and higher resale value of their vehicles — which they have been working on by not reducing the price of the product even when they benefit from supply. Their strategy is to create a new product as the cost of raw material and parts decreases

-

The company also has plans to export and enter the bike segment, but in the short to medium term, their focus is not here.

Anti Thesis / Key Risks

Increase in GST before the industry stabilizes – Currently, an EV and an entry-level scooter cost the same, but we have to keep in mind the fact that EVs are only charged 5% GST, and ICE vehicles are charged 28%. An increase in GST before a substantial decrease in the cost of EVs could hinder growth.

Supply Chain Risk – The majority of key parts of an electric vehicle are still supplied from China — tech like batteries and motors, rare earth magnets. Ather Energy is working on an asset-light model, so they do not have any plans to vertically integrate all these, which would make them dependent on Chinese suppliers until the Indian ecosystem develops. This would take time, given that these are complex tech and China also has an almost monopoly even on the raw materials of these parts, like rare earth minerals.

Hero MotoCorp holds a 30% stake in the company – This currently does not create any conflict because Hero is not as aggressive as other players in the EV space. Also, the majority of EVs being sold today are scooters, and Hero dominates in the bikes segment. But in the future, a conflict of interest can arise due to the increasing overall share of Ather or when they enter the bike segment.

Valuation

Ather Valuation 1.xlsx (18.7 KB)

I have attached the file in case someone wants to change the assumptions of EV penetration, margins, or market share, as the valuation is sensitive to these.

5 Likes

To my mind, extremely tough to make an DCF in a fast changing, fast growing sector. While it may give one a sense of direction, most assumptions will prove to be wrong by year 5. 60% penetration in 2W looks almost impossible. I guess the plateau happens at 35-50%.

Same for the rest of the assumptions.

Disc: Invested. Will track it year to year.

3 Likes

Thanks for the comment!

Just to clarify — my 60% EV penetration assumption is for Year 10, not Year 5.

And yes, this is definitely the most debatable assumption. Even HDFC Securities in their report expects only around 50% by FY39.

But I believe tech adoption is exponential, not linear. If EV prices stay in check — as I mentioned in the risks — and costs keep falling, 60% penetration is possible over the next decade.

Disc: Not invested (yet).

1 Like

No, I got that about 60% in Y10. My point was limited to saying that calculating even 5 years out in a rapidly changing tech field is tough.

So a DCF can be a more of a guiding light than anything that will give some level of certainty. I have always viewed DCF as good for a FMCG, Utility type of company that’s a mature company in a mature field.

2 Likes

I have seen such Rosy picture being painted for CNG 10 years back. Today, when I see results of MARUTI and HYUNDAI, Petrol/Diesel is still at about 60% or close. I do not believe in such predictions as they ignore real life problems at ground level. But having said that, EV penetration might grow little faster than CNG!!!

2 Likes

Just go to Vahan dashboard and see the growth of CNG and Petrol/CNG vehicles over the last few years. Obviously, the government will always give overly optimistic targets, but the fact is that CNG consumption and growth in CNG vehicles have grown faster than petrol and diesel.

3 Likes

Pretty much metric to track here will be the performance in West and North India.

Keep inching up market share in South

Rest the EL models and wider footprint and lower COP should get this to breakeven.

2 Likes

Ather Community Event on 30th Aug , is any analyst attending ?

Is the date confirmed? I do not see any offical communication from the company yet other than management mentioned that during Q1 earnings call.

1 Like

According to their latest investor presentation dated 4th August 2025, Ather currently operates around 446 stores/experience centres across India.

While they haven’t disclosed a clear split between company-owned and dealer-operated outlets, given Ather’s asset-light model, it’s likely that the vast majority are dealer-run—apart from a few legacy centres the company had set up in its early years

2 Likes

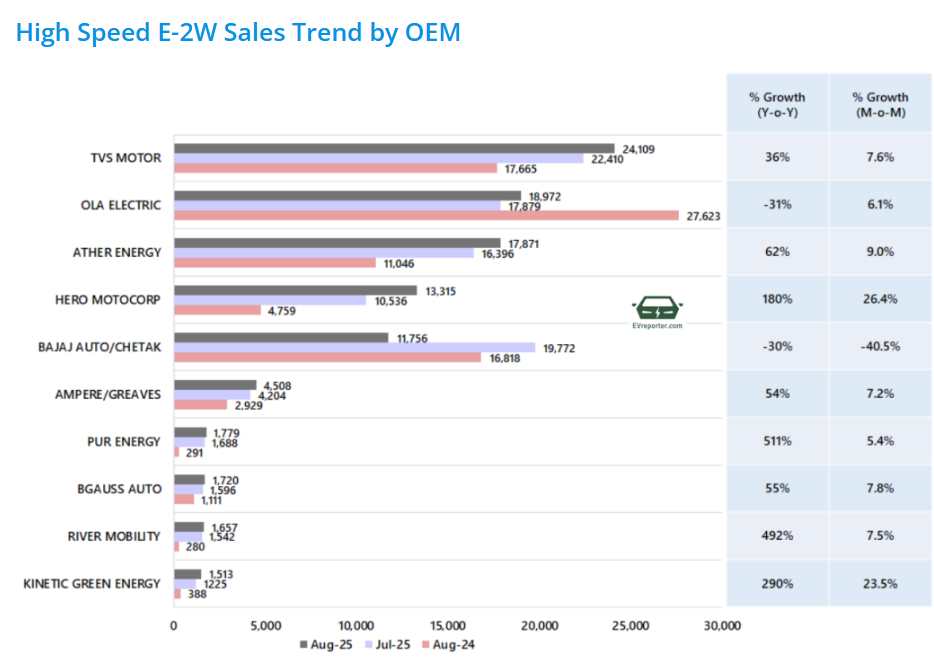

Looking at the August sales of 2W EV, Ather and Hero are in similar terms.

Hero holds 40% stake in Ather, Hero also has its own EV Fleet - Vida which is doing pretty well.

What would be the way forward for Hero? Lessen the stake in Ather and pump money back in Vida?

Take major ownership in Ather and help them decrease the RM costs?

Keeping 2 entities helps in market share and dominance, but should be in 2 different segments which is not the case right now.

5 Likes

Could be the case of oppo/vivo. Keep two separate business as rivals and let customers choose?

Disc: tracking EV segment with no position

2 Likes