I realize that I wasn’t clear enough, thanks for pointing it out. I will go back to the unit economics of Ashiana and try to explain my thought process. The core business model of Ashiana is similar to a processing company where they buy land and turn it into a building and sell it (youtube playlist explaining their model). The management has previously stated that in order to generate ~20% growth, inventories should be liquidated in a 5-7 year timeframe.

In order to analyze Ashiana, these are the factors I generally look at:

Bookings along with the booking value (giving us the average realization)

Construction or delivery

Pre-tax cash flow (tells us if money from current booking is enough to construct)

The cyclicality of this business is clear from the above (look at bookings volume). FY14 was the peak booking of the last cycle (22.13 lakh sq.ft), which was when the real-estate entered into an oversupply situation. The oversupply seems to have bottomed out in FY18, since then bookings are going up for Ashiana and this is consistent with other listed real-estate companies. I have done some work on past real-estate cycles (eg: the 1997 peak of Indian real estate) and realised that the peak of bookings (in sq.ft) is generally twice of the previous peak (give or take 25%, its not exact science though!). Over the very long term, price of real-estate goes up by 1-2% over inflation (this is valid globally). In India, realizations bottomed out somewhere in FY19 (for most listed developers). We can have a ballpark estimate for growth in realization (as 6% GDP growth + 4% inflation ~ 10%). This is my mental model.

Now for Ashiana, in the current ongoing projects out of 31.17 lakh sq.ft, 19.35 lakh sq.ft has been booked leaving ~11.82 lakh sq.ft of unsold area. For finished projects, 6.84 lakh sq.ft of property is to be sold (this is ready to move inventory). Future planned projects have saleable area of 60.76 lakh sq.ft. And then the company has 67.88 lakh sq.ft of land which will be turned into property at some point. This means they have a total saleable area of 11.82+6.84+60.76+67.88 ~ 147.3 lakh sq.ft. This is the supply scenario. Does this make sense? (numbers are provided in the latest presentation)

For realization, prices peaked out in FY16 at 3293 which was recently crossed. Long term growth in price realizations in India has been ~10%. In order to be conservative (given how much excess inventory exists in certain parts of India), I took realizations as 4000/sq.ft in 2025. I might be wrong in my assumptions though!

Thank you for the detailed explanation. For some reason, the above investor presentation link did not completely load for me and I missed the information on the final slides (got it from bse now).

But that helped in getting your indepth analysis which helps me understand the business! Thanks again

To be bullish on Ashiana, you have to be bullish on the micro market in which Ashiana Operates. 60%+ of Ashiana future and current projects are in very niche micro markets.

First make a case on why people will buy houses in those micro markets

I was able to only attend part of the conference call, here are my notes. I will update it once the conference call transcript is available

Ashiana Amantran cancellation of 41 flats which are still in the system will be recorded in Q2FY21; July and August good months for booking

July has been a good month across all properties; see good overall traction in bookings; Needs to be seen if the booking are because of pent-up demand? Management sense: Compression in interest rates favors consumers; 3% rental yield (± 50 bps) in most of the projects

Q2 booking will be better than Q1; Ramp up of construction in months to come, delivery might be a little delayed

Receivables not alarming according to management

o Maintenance segment: particularly for people who do not stay at the property, so receivables can be a little stretched because of that and they pay when they visit

o When delivery letter is issued and last 4-5% of payments is pending, sometimes that gets delayed

Ashiana town: July and August continue to be good. This year will be better than last year

Cash situation will improve in Q3 (maybe suboptimal in Q2), optimistic on the cashflow front

New launches: Vrinda graden phase 5 in process, Nirmay: second block will be launched this quarter, more launches in different phases of different projects later this year; New lauches for FY21: ~1mn sq.ft

Bhiwadi & Jaipur area: Economic activities are coming back to normal, in Jaipur where tourism and jewelry parts a large part of the economy are constrained. In Bhiwadi, auto manufacturing activities started coming back in July

EMI scheme: no 10:90 scheme for Ashiana; Focus on schemes which give upfront cash

Direct sales: Got into it more because of compulsion

Still looking for senior citizen project for Chennai

I thought to chime in though I don’t own any stock in Ashiana nor do I intend to.

I am an investor in Ashiana properties in Bhiwadi for over 6 years. Pre covid the occupancy rates from a rental perspective were quite high and Ashiana is looked as up market as per the standards there. Rentals have grown but is nothing in absolute terms compared to say Gurgaon which is a 45 min drive away. Folks in middle income group have started staying in Bhiwadi even though their offices are in Gurgaon.

The industrial belt including auto companies and glass companies like Saint Gobain is what drives occupancy.

I dont think property prices have appreciated much. I have not kept track of it. But for me rental income has increased almost 100%.

Will start measuring net promoter score to understand how happy their clients are across projects

Ranked #1 brand in North India, #5 in India, #1 senior living brand (third consecutive time) by Track2Realty

Launched 4 greenfield projects (2 in Jaipur, 2 in Jamshedpur). No further greenfield projects in FY21

Debt as on FY20: 104.97 cr. (excluding IFC funding of 18.74cr.), Out of this 20.2 cr. is working capital debt. Cost of borrowing: 10.5%

Cash as on FY20: 154 cr. (4-5 cr. monthly expense)

Generated positive operational cashflow at 34.22 cr. in FY20 vs 16.41 cr. in FY19

90% of customer loans are from top 2 housing finance companies in India

Land bank: 86.82 acre, looking for land acquisition opportunities in Jaipur, Gurgaon, Pune, Chennai and Bhiwadi

Jaipur market is doing well, there was never oversupply problem here

Gurgaon and Bhiwadi markets are facing challenges, with sales in Sohna (Gurgaon) slow. Bhiwadi senior citizen living project is doing well

Ongoing projects: 31.17 lakh sq.ft saleable area out of which 19.35 lakh sq.ft has been booked

Lavasa (Pune) phase IV has been constructed, however sales is yet to be commenced pending OC approval

Projects launched in 2013 and 2015 have seen pricing impact, where they have unable to pass on inflation in construction costs to customers due to oversupply in market

Enquiries and site visits are back to pre-COVID levels, expect normalcy return in 2nd half of this fiscal

Number of permanent Employees: 524; Median salary: 3.47 lakhs; 9.18% increase in salary of employees other than managerial personnel; 7.1% including managerial personnel

Internship program from leading management institutes went well and has now been institutionalized.

Sold 1505 flats against a sales target of 1600

Advertising and business promotion expense: 28.28 cr. (vs 25.59 cr. in FY19)

Had to writedown 17.39 cr. selling expense whose corresponding revenue were not similar to the costs was incurred

Gross profits was lower at 23.51% vs 30%+ in previous years because of Sohna project (accounting for 47% revenues recognized) which had much lower gross margins

Partnership profit: 300/sq.ft (vs 331/sq.ft in FY19)

Total collection: 353.1 cr. vs 292.36 cr. in FY19

COVID impact:

o Project delays

o Demand contraction

o Supply contraction

o Continued consolidation towards reliable real-estate players with balance sheet strength

o Trying to manage cashflows properly

Site visits higher than pre-COVID levels, virtual visits going well and shortening buying cycle

Seeing substantial traction in conversions where bookings are happening with substantial payments

Ashiana not alone in demand revival; Lots of other developers also seeing traction in residential space, Possible reasons: low inflation in residential real-estate prices over past 5 years, low interest rates increases affordability;

Getting more sales in under construction property compared to ready to move property

Maintenance booking revenue: 4.5 cr./month (not for profit business)

Debt: 55 cr. in corporate balance sheet; 15-20 cr. in project level funding

Company has a business coach based out of Vancouver Canada, and they have also seen spike in residential real-estate demand across Canada

Govt extends several incentives including free Floor Space Index (FSI), concessional project finance, free of cost trunk infrastructure facilities, among others to push participation in Affordable Rental hsg scheme

Margins were under pressure this quarter due to lower revenues recognized due to lower delivery volumes; will achieve construction targets for FY21

Sales momentum has continued in Q3FY21 and pricing remains stable across markets; Proportion of sales has shifted towards home buyers from investors

July – September: Units booked were ~215 (1300 sq.ft average size); excluding cancellations in Amantran (H1FY21 ~80’000 sq.ft), bookings were closer to 2.8 lakh sq.ft this quarter

Bookings come back to 2mn sq.ft sales booking starting FY22

Have signed 3-4 term sheets for land transactions; With recent sales momentum, company is looking to take those land transactions through; Hoping to do 3 transactions this fiscal year (may spill out to April-May)

Lavasa sales have recovered, however will comment more on the Lavasa market after 1 quarter to see if the sales recovery is stable

Land available for future development: means they don’t have approval for launches

o Milakpur in Bhiwadi: Land is owned by Ashiana

o Ashiana Malhar in Pune: It’s a joint development project which is now fully funded (this quarter); This is Ashiana’s first project in Pune; major approvals have gone through and smaller ones remain; Launch will be in FY22

o Kolkata: Partly funded the land cost and rest is a structured transaction; Facing difficulty in getting project off ground in Kolkata; facing a tough time with approvals (don’t expect anything soon)

Vrinda garden has been the most slow selling project in Jaipur

Hoping to gain sales momentum in Anmol (Gurgaon) project

Currently preferring joint-development projects; actively looking for new partners

Currently not seeing inflation in raw material prices for construction compared to pre-covid level

Noida senior living project: Most complex market in terms of approval; Have signed a very early term sheet, want to get a senior living project started in Noida but struggling with getting around the maize of approvals and bureaucracy

3-year plan (aim to get back to mid-term ROE)

o Focus Markets: Chennai, Bhiwadi, Gurgaon, Pune, Jaipur (smaller markets like Jodhpur and Jamshedpur may have 1-2 ongoing projects, however these are not big markets)

o Kind of projects: Senior living housing (Bhiwadi, Chennai; looking for something in Noida); also trying to build into comfort and kid-centric homes

o Long term realization growth: In-accordance with CPI growth (6-8%); Sales realizations have more or less doubled in similar sized projects over the last 12-13 years

o Senior living properties will drive overall profitability (less competitive space leading to less cyclicality in supply) – probably the top developer in India (definitely in top-3)

Access to capital is very limited to developers serving smaller markets (funding first goes to Mumbai developers followed by other metros, etc.). That’s why Jaipur didn’t have such an oversupply compared to Delhi NCR or Mumbai. Bhiwadi had oversupply because a lot of Delhi based developers who had access to funding went into Bhiwadi.

Future projects summary slide is generally for future units that will be constructed in a given project (which already has units constructed in the past)

Disclosure: Invested (position size same as before)

Thanks Harsh…The last time Ashiana Housing hit 2million sq ft. was in FY14. The market cap. at that time was about 3000cr (about 3.5x higher) and with 10% lower realizations. If they can hit that mark in terms of bookings again on a consistent basis, as guided by the management from FY 22 onwards, it will be interesting to see how the market reacts then. Especially with a way more consolidated industry structure, higher entry barriers and better access to low cost funds (through their partnership)

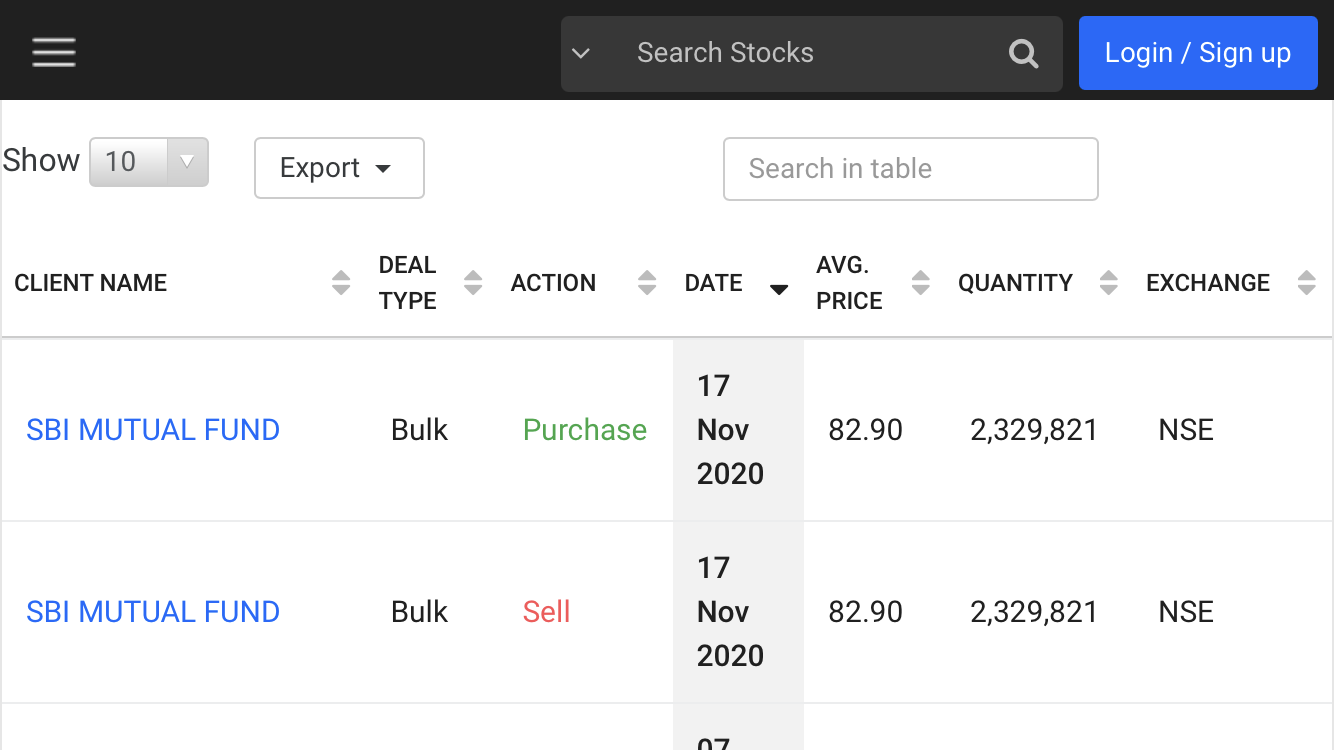

Bulk deal on 17th November. Can someone explain the rationale for buying and selling large quantities by a mutual fund on the same day at the same price?