Ashiana Housing FY 19 AR Notes

Focus on being cash surplus, reducing area construction and increasing bookings helped the company in becoming cash surplus this year. Management’s commentary was very positive for FY 2019-20 on the back of good sales in FY19. They plan to launch new projects aggressively in FY20 and plan to double the sales in FY20 to 20 lac sq. ft. (they use to do these kind of numbers pre 2015). Trying to create a Niche in a Commodity Market through Kid Centric Homes, new focus area after Senior Care homes. Focusing on employee training really tells about the culture management wants to create.

Key points in AR.

- Our revenue from operations include: a) Revenue from completed projects (residential/commercial); b) Revenue from other real estate operations include maintenance and hospitality services Revenue from Operations increased by Rs. 2,341 lakhs or 7.64% from Rs. 30,637 lakhs in FY18 to Rs. 32,978 lakhs in FY 19.

Out of this, revenue from completed projects increased from Rs. 26,225 Lakhs (FY18) to Rs. 28,138 Lakhs (FY19), an increase of 7%. Increase in revenue was attributable to higher deliveries (9.44 lakhs sq.ft in FY19 vs 8.91 lakhs sq.ft in FY18)

Revenue from maintenance & hospitality increased from Rs. 4,412 Lakhs in FY18 to Rs. 4,841 Lakhs in FY19, an increase of 9.72%. - Partnership Income: There was a decrease of Rs. 719.34 Lakhs or 48.13% from Rs. 1,494.58 Lakhs in FY18 to Rs. 775.24 Lakhs in FY19. Decline in partnership income mainly attributable to lower deliveries. (2.34 lakhs sq.ft in FY19 vs 3.78 lakhs sq.ft in FY18).

- PBT decreased from Rs. 4,874 Lakhs to Rs. 2,395 Lakhs due to lower gross margin (resulting from mix of projects in AHL), lower Income from Partnership (due to lower deliveries) and increase in costs like Selling and Finance costs.

- Collection for the year improved to Rs. 29,236 Lakhs [AHL: Rs. 21,493 Lakhs and Partnerships: Rs. 7,743 Lakhs] from Rs. 26,895 Lakhs [AHL: Rs. 18,753 Lakhs and Partnerships: Rs. 8,142 Lakhs] for FY18, a rise of 8.70% primarily due to higher booking.

- During FY19, the company delivered and recognised revenue of Ashiana Dwarka (Ph-II) in Jodhpur, Gulmohar Gardens (Ph-VII) and Vrinda Gardens (Ph-IIIA) in Jaipur, Ashiana Surbhi (Ph-V), Ashiana Tarang (Ph-I) in Bhiwadi. Area delivered for revenue recognition was 9.44 lakhs sq. ft. in AHL and 2.34 lakhs sq. ft. in Partnerships.

- We have an ambition to double our sales to more than 20 lac square feet in the forthcoming year.

- 2019-20 will be launch heavy year with several new projects lined up across most of our markets. We have several new project launches in the forthcoming year in Jaipur, Jamshedpur and Kolkata. Besides, we also have launches of new phases of existing projects.

- Kid Centric Homes - Trying to create a Niche in a Commodity Market.

‘Kid Centric Homes’ can provide solution where the infrastructure, facilities and management of the project create an environment that ensures holistic development of children of all ages inside the project itself. 3 of our projects are Kids Centric, i.e. Ashiana Umang, Jaipur, Ashiana Town Bhiwadi and Ashiana Anmol, Gurgaon. - Recognised by the Track2Realty wherein Ashiana was recognised as the Number one caring brand in north India.

- The company has acquired a land parcel measuring 6.67 acres situated at Village Shri Kishanpura, Jagatpura, Tehsil Sanganer, Dist. Jaipur, Rajasthan. Ashiana is proposing to develop a Comfort Homes project which will have a saleable area of approximately 6.15 lakhs sq. ft.

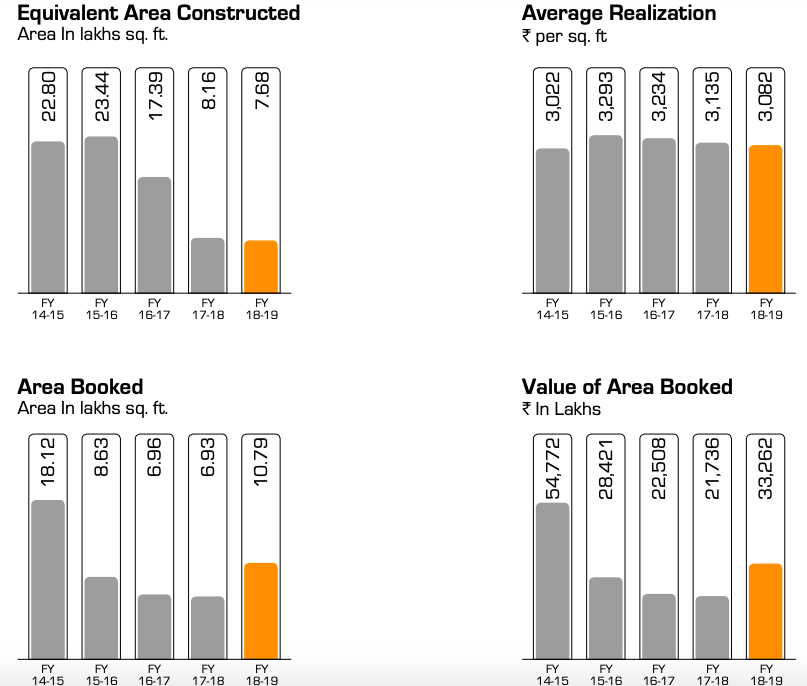

- With the sector showing gradual cyclical upturn, we also witnessed improvement in our booking to 10.79 lakhs sq. ft. in FY19 vs 6.93 lakhs sq. ft in FY18. The growth was secular as we saw improvement across all our markets vis a vis previous year, barring Lavasa (Pune).

- In terms of the execution, we recorded an EAC (Equivalent Area Constructed) of 7.68 lakhs sq. ft. (AHL: 5.31 lakhs sq. ft. and Partnerships: 2.37 lakhs square feet)

- Operational Cash Flows, turned positive and improved vis a vis last year due to better collections resulting from higher booking. (Positive at Rs. 16.41 Crores in FY19 versus Negative of Rs. 20.21 Crores in FY18).

- New projects lined up for fresh launches include Ashiana Sehar and Ashiana Aditya (Jamshedpur), Ashiana Daksh, Ashiana Amantaran and Gulmohar Gardens Extension (Jaipur) and Ashiana Maitri and Ashiana Nitya (Kolkata).

- Plan to launch new phases in Ashiana Shubham (Chennai), Ashiana Tarang and Ashiana Nirmay (Bhiwadi), Vrinda Gardens and Gulmohar Gardens (Jaipur) and Ashiana Dwarka(Jodhpur) and Utsav, Lavasa (post completion of Construction).

- Our major markets are Jaipur, Bhiwadi, Gurgaon and Chennai. In Jaipur market there is less oversupply. Unsold inventory has stabilised and is gradually being absorbed. Our outlook for Jaipur market is very positive and we expect to continue doing well in Jaipur market in future.

- In Chennai, overall market remained tough. Markets are stable with high unsold inventory, though the supply seems to be cooling down and demand showing hint of recovery. Since for us, we launched a senior living project, which is a specialised niche, we have done much better than our expectations. We have already sold the first phase of the entire project there.

- Gurgaon, markets are oversupplied and relatively priced higher. We will shortly commence deliveries in Phase 1 of our project Ashiana Anmol on Sohna Road, South of Gurgaon.

- Another significant development during the year was the initiatives we took for growth of our Human Capital, like 23 days orientation programme for new joinees in sales, creation of Job Score Cards, Performance Management (Talent Review and Management Conversations) etc.

- IFC will invest total Rs. 150 cr (40%) with returns linked to specific projects. The first tranche of funding i.e. Rs. 18.74 Crs has already been received for Ashiana Daksh, a Comfort Homes project in Jaipur which will be launched in FY20.

- The average realisation price has remained under pressure for the last 2 years. The average realization has declined by 1.70%, Rs. 3,082 per sq.ft. in FY19 vs Rs 3,135 per sq.ft. in FY18. We have not taken any headline drop in prices in any of our projects. The marginal decline in average realization price is attributable to the following reasons: • Benefit of GST input credit passed onto customers was higher vis a vis benefit received by the company Customised payment solutions in select ready to move projects resulting in indirect discounting on prices • Inability to significantly increase prices across projects due to ongoing sectoral slowdown • Interest subvention being offered in Bhiwadi projects and • Change in project mix.

- The GST council had decided that all new regular projects launched after April 1 would attract and levy a charge of 5% of GST to buyers. For affordable housing units, rate was slashed to 1% from 8% earlier. However, the builders would not be eligible to avail input tax credit. This would result in blockage of credit and an increase in cost, adversely impacting the margin of builders. For ongoing projects, the government allowed developers an option to continue under the old GST regime. In our case, we have opted for the old GST scheme in all our projects which were ongoing as on 1st April’19 and continuing with the GST benefit/discount we were earlier passing onto our customers. We have not seen any adverse impact on our sales as a result of this.

Regards

Harshit Goel

Disclosure: Invested

This is a snippet from annual report of the company. For the first time in recent years Area Booked is more than Area Constructed leading to positive cash flows for the company. And this Area Booked number is expected to double in FY20.

Regards

Harshit

Hi Harshit,

I find the business format of this Housing company to be much better than most others. It has a good brand building as well. But due to recent course of events, Demon, GST, RERA the builders are facing a major liquidity crunch. I am sure our company will get over it in the due course.

But, for the first time in more than a decade the interest coverage ratio, which I find to be a very important metric for housing companies, for Ashiana Housing is appearing to be unmanageable. After, March 2017 balance sheet, the borrowings have only ballooned. Apparently, Demon took a heavy toll on liquidity. Borrowings almost doubled from 89Cr at end of F.Y.2016-17 to 165 at end of F.Y.2018-19, in two years time.

I think this may cause a drag on the share price. Only making it more attractive for retail investors.

Please comment on this situation.

Thank You.

Hi Amit.

They increased the borrowings for purchase of land and also because of the slowdown they were not able to sell much. They had negative operating cashflows in 2017-18 due to fall in collections, which turned positive in FY 2018-19. Yes these things do have negative impact on valuations of the company. This was one of the reasons that stock did not perform well in the past 2-3 years where other good realty companies like Godrej Prop, Oberoi Realty, Kolte Patil did quite good.

Also the Q1 results were a bit disappointing in the sense that Area Booked was around 3.54 lac square feet. Management guided for 20 lac sq ft in Annual Report 2019, so in Q1 it was a bit on the lower side. On the Q1 con call management said that they should easily achieve around 17 lac sq ft for FY20 and they aspire to do 20 lac sq ft for FY20.

Regards

Harshit

Company launched two project in december one in Jamshedpur and sold area of 3.54 Lac Sq ft and second one in Jaipur and sold area of 3.75 lac Sq ft whereas total area sold in last two quarters is 6 lacs . Good Launched by the company. Management guided for 20 lac sq ft in 2019-20 looks now easily possible.

disclosure Invested

Ashiana Housing Q3FY20 Concall Summary

Business Update

- Area booked in Q3FY20 was 9.78 lakh Sq foot vs 2.55 lakh sq foot in Q3FY19 due to new launches in Jaipur, Bhiwadi and Jamshedpur

Participants

• Marshmallow Capital

• Multi Act Equity

• SBI Mutual Fund

QnA

- The new projects at Jaipur have done well because of recalibrated pricing, designs and also due to a better location

- Some price increases can gradually happen but price increases seen during the past in the boom period are difficult

- Q4 will see one new launch and be better than Q1&Q2 combined

- The managements comfort on cash flows have increased and thus now will be signing more new projects as certainty on cash flow is now there

- Expecting FY 21 & 22 to be also good considering newer launches to be done

- Not expecting significant profitability in FY21 as well. It should be a reported loss

- Total debt on the books is Rs 121 crores including debentures issued to IFC for the Ashiana Daksh project

- The management expects to make some announcements on land purchases in the next 12 months

- Expecting a decline in FY21 over the FY20 numbers in terms of sq foot launches. Launches in FY21 will be closer to 1.5 million sq foot versus 2 million in FY20

- The Pune launch is expected in Q1 FY22

- Continuing with some experiments across projects to improve the sales velocity

- Have deployed only Rs 18 crores from IFC partnership in the Ashiana Daksh project

- The margins have come off because land prices were locked in 4 years ago and prices haven’t increased since then while construction cost has been going up

- No plans of raising equity capital at this point of time with valuations which are not justified

- The affordability index of customers today is significantly higher than what it was five years ago

- Land pricing can only change when the cycles turn

- Not using IRR as a benchmark for measuring return but instead using economic profit on a company level to measure profitability

- The cost of funds currently are 10.5% and new funding is happening at 11-12%

- With RERA cannot take more than 10% at the time of booking

- The balance cash collections on ongoing projects is around Rs 400 crores and the timeline on this is the next 24 months

Based on the consolidated balance sheet numbers of Dec 2019, the net current assets (Inventory+Cash+Other Current Assets- Debt- Current Liabilities) is around Rs 60 per share. At market price of Rs 45, the market is saying that the company is worth more dead than alive.

Will Ashiana survive the downturn and be stronger 5-7 years later ? I think that probability is quite good.

The inventory might have to be marked down, considering the impact of Covid-19.

In their last call the management said they can’t decide what they will do with the extra cash when their cash flow resumes. They can buy land parcels or they can go for buyback. I think if a company is selling at good valuations you buy it, even if it is your own. So I think that should be their prime choice. I don’t know what will happen.

Disclosure: entered the company @ 48/-

This will be series of post on residential real in general & ashiana housing investment thesis

Residential markets different vs GFC crisis, may bottom out by CY20 end

- The residential markets are much different vs the 2008-09 GFC crisis. We have buyers market now, demand is end user driven, FDI is largely non- residential, land prices are expected to correct further and developer’s margin has contracted. Govt support on affordable housing and CLSS scheme has aided demand. Though luxury and super luxury will see more delayed demand recovery. Interest rates are at all time low, LTV is conservative at 75-80% vs 95-105% during GFC crisis. NBFC crisis priced in.

- In Residential, we saw in the first quarter (1QCY20) that launches were down 3% and sales were down 29%. The market is much different now vs 2008-09. Today, the

- residential pain which has been continuing for the last five years is a lot more

- realistic. The nature of the market back in 2008 was a market driven by sellers.

Today, the residential market is already very buyer-driven. - Home loan rates back then were getting into the 9% to 10% mark. Today, the home

loan rate is in its early 7%. - Back then the markets were very, very driven by speculators and investors. Today, the speculators and investors have totally moved out. Resdential demand is very local in nature , back then it was FDI money which was fuelling prices and demand.

- After RERA, GST & demon 90% of competition has moved out. Those who have left have also become choosy after ILFS fiasco & now covid 19.

- Ready to move in will be preferred. The buyers would be all home buyers who are end users. For bigger size apartments of more than Rs 10mn, the troubles will continue. Developers

- who are able to offer the right price at the right size and right quality will obviously

- do well.

- In the wake of COVID-19 situation, price points are expected to soften for developers “desperate to sell”. However, this would again depend upon location and type/ segment of individual projects and the builder’s financial flexibility which will be demonstrated in its ability to hold on to the inventory in such times. Luxury projects which have shown lower sales growth are likely to be impacted more.

- Slowdown in the construction activity may result in weakened cash-flows for the companies in the short term. Consequently, companies with higher financial flexibility, stronger liquidity or having projects nearing completion or having longer moratorium period or having cash strap mechanism i.e. repayments linked to sales are better placed to tide over the uncertain market environment. However, in the long term, it would depend upon developer’s ability to improve collections.

-

- Disbursement of new loans/ refinancing risks have increased as housing finance companies, NBFCs and banks become more selective and tighten their disbursements criteria to developers. A large portion of funding requirements of the sector (customer advances) is met by NBFCs or HFCs who would also be highly selective in fresh disbursements. The uncertainty and slowdown in economic activity would have severe impact on new loans/ refinance to developers.

- “The 75 basis points’ cut (in repo rate) would give a big boost to credit appetite among new home buyers. The moratorium of three months on term loans, including home loans, would provide relief and enable companies to focus more on the operational requirement and recalibrate their business strategies,” said Kamal Khetan, chairman at Mumbai-based Sunteck Realty.

Disclosure: Invested and top 3 holding now after been out of this sector since start of my investing period.

From ashiana concall I could gather following relevant point

- [x] Labour has not migrated and we are ready for post lockdown enviro

- [x] We don’t wanna is forecast we don’t know

- [x] We will be conservative in near future

- [x] Not think buy back as a lot of it depends on how cf pan out in 3 4 months

- [x] We don’t know land price behaviour , stock price info is available we will look other options to allocate capital

- [x] We have large bank if sub etc not able to finance

- [x] Consolidation will accelerate with this event

- [x] Lot of migrate labour going back thesis they are not sure

- [x] Indian economy is not that bad effected as USA

- [x] Bhiwandi dependent on auto sector impact? Bhiwandi demand already minuscule and we have grown via gain in market share as competition has suffered more than us

- [x] Supply side is slow process in industry as need time to build but this issue has been of demand supply side and last cycle was supply side issue

- [ ] Fortunately we have been healthy in bad times

Disclosure: same as above

I must add they have no plans to add inventory in 2020-21. They will think about it in 2022, and that is the right decision. I think.

Investor presentation for q4 FY20

Here are my takeways from today’s call

|-|Anmol Gurgaon: Phase 2&3 will be launched only after completion of sale of finished inventory of Phase 1 (1.45 lakh sq.ft still left from finished inventory); Margin is half compared to other projects, will reduce consolidated margin if large sales occur within this project.

|-|Amantran Jaipur: 124 bookings were completed until 31st March 2020; Received 30-35 cancellations so far; Expect ~45 cancellations out of the 124 expression of interest. No other project seeing this cancellation trend (reason: launch was followed by COVID; bad timing)

|-|Vrinda garden Jaipur: Phase 3 has very limited stock right now, do not have smaller units (2 BHK)

|-|Chennai: Looking for 1 project launch for senior housing; their differentiation from local competitors is focus on senior citizen housing

|-|Bhiwadi: Market extremely slow

|-|Halol: Decided to exit the market; Took 5 cr. write-off in costs

|-|Virtual site visits started where manager shows the property on video call

|-|No clear trend observable in consumer behavior

|-|FY21Q1 (so far): ~50 bookings + ~50 cancellations (with 35 happening in Amantran project Jaipur); Single digit revenues (in cr.??)

|-|Pricing: Jamshedpur & Jaipur: No pricing pressure; Gurgaon, Bhiwadi: Pricing pressure (were already facing that pre-COVID)

|-|As of now, construction costs are stable

|-|Labor situation: Rajasthan: no worry; Chennai: labor supply crunch as a lot of labor left; Jamshedpur: saw some labor shortages (although Jharkhand has a lot of local labor as well which has helped curb the shortage)

|-|Kid-centric projects: Anmol, Bhiwadi & Jaipur. Long term plan is to position themselves as higher value offering, hence having higher margins. Currently, that’s not the case, it took them 14 years to charge premium pricing in senior housing|

|-|How will cash be used? Buyback: NO! Will look to hoard a bit of cash to make sure that liquidity is not an issue; Have prepaid 10 cr. in loans; 17 cr. of NCD will be repaid in July; Land markets are becoming very attractive; Evaluating Noida market for senior living housing as it can be a replacement for Bhiwadi (Noida is better value for seniors compared to Bhiwadi)

|-|Land transactions (Anmol, Tarang, Umang extension, Aditya, Amantran): lower gross profit margins because land price was locked in 2013-15 at high level; Long term gross margins ~ 30% across projects 3-years out (~ Rs. 1000 /sq.ft); Senior living will have higher gross margins

|-|Margin compression is period is over, going forward margins should expand (how COVID impacts is not well known)

|-|Overhead costs started ballooning because of increased marketing costs; Marketing expenses will be more controlled going forward

|-|No analyst day this year

Thanks for the great summary.

It is understandable that management continues to talk about what they know and what can be measured. But I honestly think they may be in denial. It is very naive of them to think that margins should expand and marketing costs will be more controlled.

The long term impact of COVID on the real estate market is a major overhang. From my current experience asking around in tier I/II cities, land prices haven’t dropped much because of the extremely slow velocity of sales. It is only when transaction volume picks up and the loam moratorium ends will we see what the real estate sector looks like.

What’s your valuation model tells about this company, is it good buy at this level? Please share your views on valuation

Valuation is very cheap, they sold flats worth 671.63 cr. this year, which will lead to profits of 100-130 cr. On a Mcap of 535 cr., this translates at 4-5 times of current year’s earnings.

I think the real question we should ask is what sales will be in 5 years, here is a hypothetical scenarios:

In five years, Ashiana is able to increase sales from 20 lakh sq.ft to 30 lakh sq.ft @price of Rs. 4000/sq.ft (this year’s realization was Rs. 3388/sq.ft). If it happens, revenues will be 1200 cr.; PAT margins have varied b/w 15-25% in the past with gross margins of >30%, a conservative PAT margin will be around 15%. PAT: 15%*1200 ~ 180 cr.

Now you can put your price multiple to come to your projections ![]()

Can someone help me understand the Operating Cash flows arrived at in the Investor Presentation? It says OCF has increased to 34 cr from 16 cr. Also there is a foot note which mentions the following -

Note: Cashflow From Operations before land acquisition reported above are different from the statutorily reported operating cashflows (as per Ind AS 7)

How do I arrive at these numbers from the Cashflow statement because it shows different values?

Can you help me understand the math here? Already 20 Lakh Sq ft has been booked at 3388/sqft this year right? I believe the total land parcel is 30 Lakh sq ft as of now. So that means we have 10 Lakh sq ft left to be booked. Now if they have sold 20 Lakh sqft this year alone, we can assume that they can sell off the rest of the 10 Lakh sqft within a year or two. From the QnA

The balance cash collections on ongoing projects is around Rs 400 crores and the timeline on this is the next 24 months

- Why did you assume 5 years for the remaining 10 L sqft? Am I missing something here?

- Shouldn’t 10 L sqft cost just 400 cr instead of 1200 cr in your assumptions?

Please let me know your thoughts.