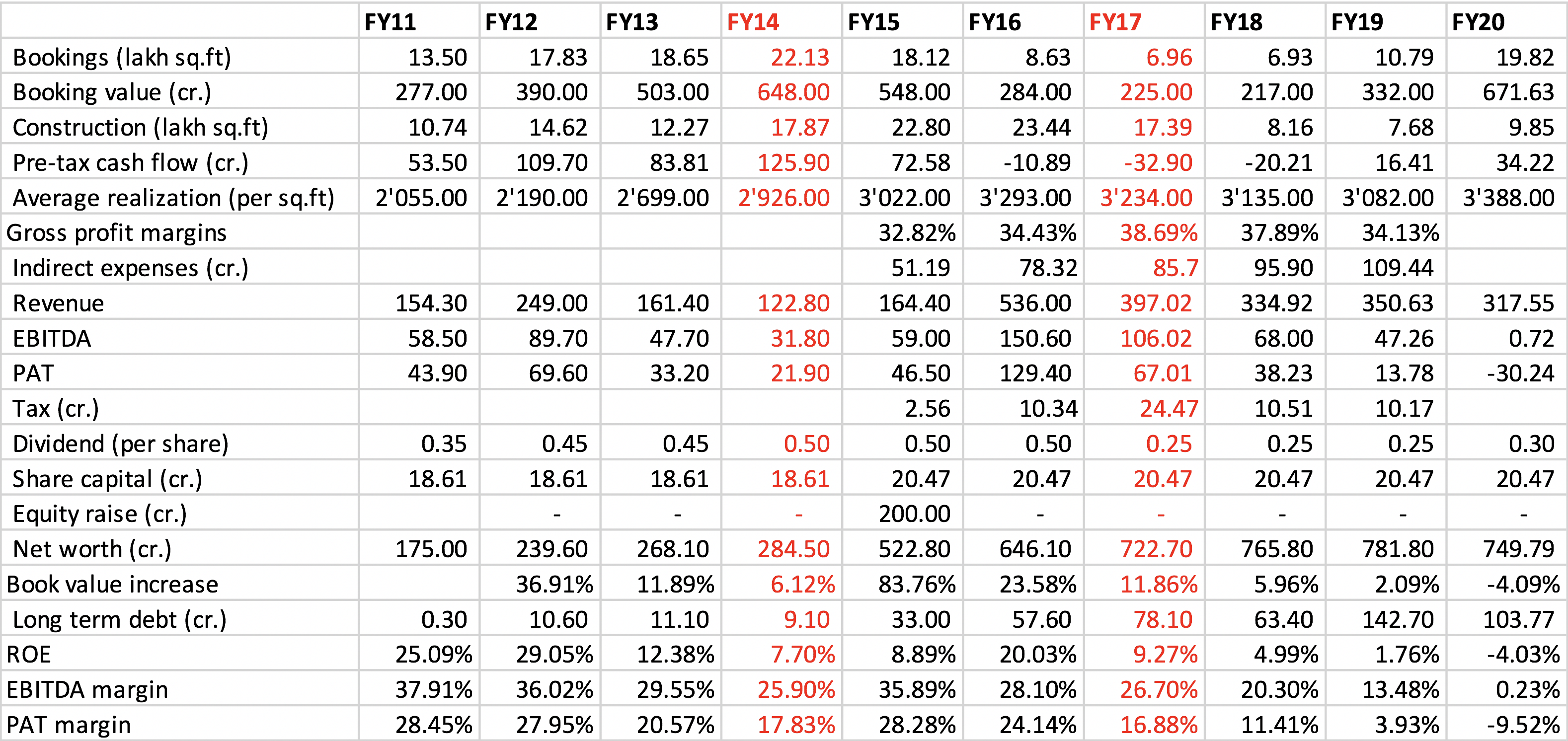

In this post, I will try to illustrate the real-estate cycle through Ashiana Housing. The figure below shows detailed financials since FY2011

As shown in the previous post, the Indian residential real-estate cycle peaked around 2013-14 period. Ashiana’s booking also peaked around the same time at 22.13 lakh sq.ft in FY14 and went down to 6.93 in FY18. Since then, booking volume has picked up and the company managed to get close to its FY14 numbers. Other listed players have reported improving sales number in the last 2 years, which hints that the cycle might have bottomed out.

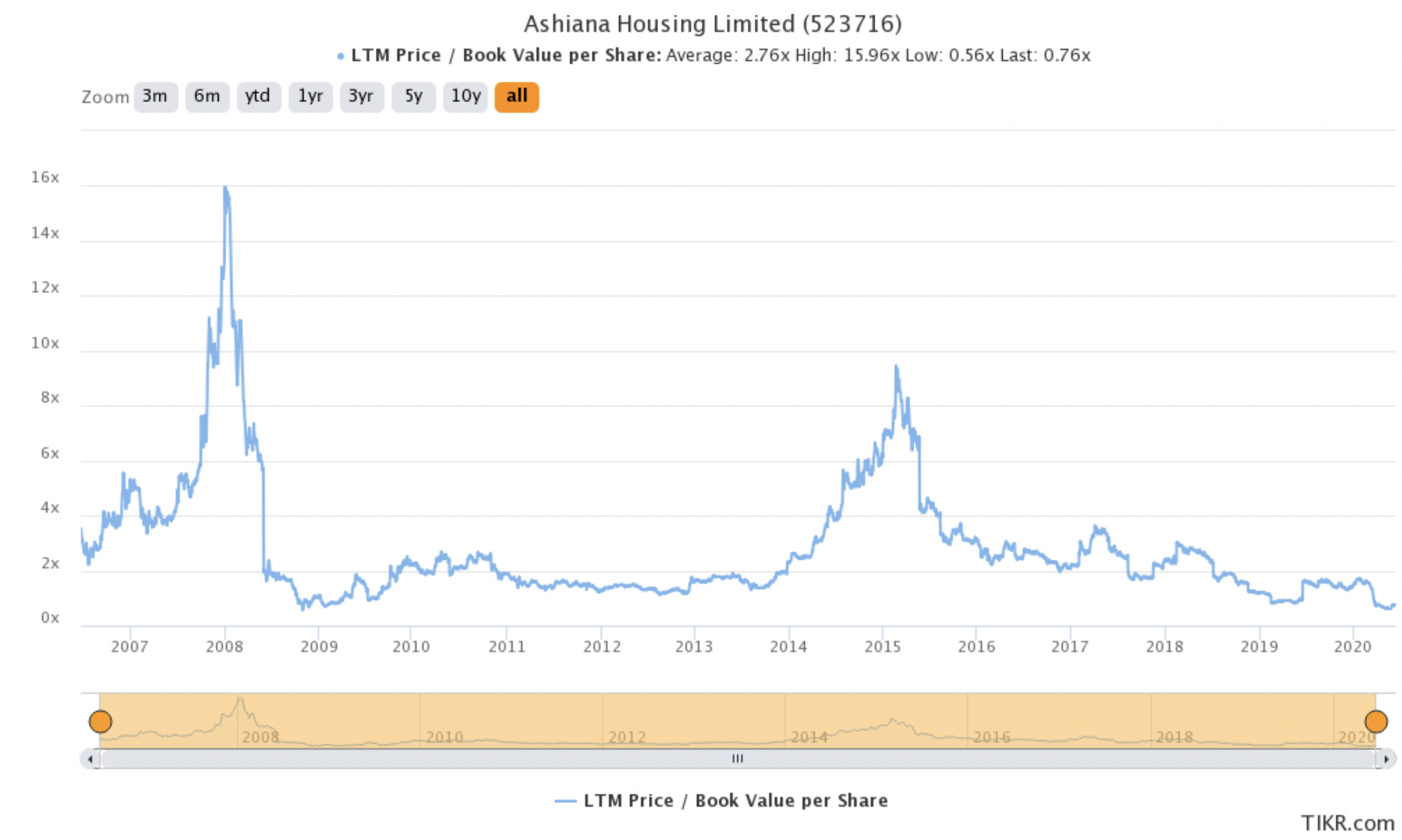

Book value can be a considered as a proxy to the current value of land and inventory. How has market price moved relative to their book value over time? (taken from tikr)

We can clearly see that market went a bit haywire in 2008 boom, and again in 2015 period (Ashiana housing thread is a very good illustration of the same). This shows how cyclical valuations (or market sentiments) are. Over the past 15 years, we have clearly seen two large bull markets in Ashiana where market was willing to pay upto 10x its book value. The next question is what is the appropriate P/B for such a business? Let me try to give my spin.

In FY10, Ashiana’s book value was ~130 cr. This has increased to ~750 cr. in FY20 (CAGR growth of 19%). For achieving this growth, company has taken ~95 cr. of debt, raised equity of 200 cr. in FY15 and given back dividends of ~80 cr. (excluding taxes). If we include taxes paid on dividends, the IRR numbers are 12-15%. Now we also know that the inventory and land costs stated on the balance sheet are historical numbers, their actual values might differ (are probably higher given inflation). In essence, the long term ROEs of the company is probably close to 15% which means at a risk free rate of 6%, this should be valued close to 2-3x its book value (if we do not assume growth). Market has valued it anywhere between 0.6x to 10x in the past.

What about now?

I did detailed valuation work here. The company sold flats worth 671 cr. in FY20, has land and inventory worth >1000 cr. all of which are available at a market cap of 630 cr.

Now the question is:

- Will real-estate cycle recover (given the current down cycle has already been for 5 years)?

- If it does, can management execute as they operate only in niche geographies (large inventory in Bhiwadi which is an auto-hub) and in niche sectors (senior citizen, trying to grow into family friendly housing)?

If the answer to the above is yes, it is a no-brainer 3-5x. What’s the downside? The current inventory is close to the market capitalization, they have an unlevered balance sheet (low bankruptcy risk). Only cycle has to turn.

Disclosure: Invested (latest position size here)