In Q3FY23 concall, managememt mentioned they don’t plan to take the gearing ratio above 4-5x, which stand at around 2x now. So, it seems they’ll not raise capital for next 3-4 years, growing at 30%.

Growth continues

1 Like

Agreed, but when this growth will pay back?

This one is going to test patience.

P/B of 3.9x does not leave any room for valuation expansion.

However, ROA of >8% is tremendous coupled with AUM growth.

1 Like

Question on Succession planning

None of my family members want to join the business after me, So the board will identify and select a professional, it will be professionally run and, I would be only an investor after I exit.

Could succession plan be a potential reason for the long consolidation and downtrend in this stock? There has been a change in leadership with Mr. P Balaji joining as MD and the promoter, Mr. Anandhan has elevated himself as a chairman, however the market does not seem to be convinced with succession plan.

The financials have only grown from good to great and current valuation of 4x book does not look exorbitant for a company that delivers ~8% ROA and ~16% ROE and has ~1.1x leverage, coupled with ~30% AUM growth visibility for the next few years, along with <1% NPAs. Yields are great too and CoF is decent compared to other HFCs. NIM is fantastic.

Is Geographical concentration a concern? The leadership is quite clear that they do not want to grow PAN India and want to go deeper into existing geographies (TN, AP and KA) and only grow into adjacencies (OR, MH and CH).

Is the market discounting the possibility of a M&A (Chola?) or equity dilution by the PE players in series of blocks in near team?

I’m quite curious and keen to learn what others see in Aptus in terms of valuations and future growth potential and what are the potential risks? (Over and above what is covered in this fantastic thread)

6 Likes

One question , Is not it a sin business to charge 17% on home loan for economically weaker section for a token size of less than 10 lakh fund ? What do you think ? Feel free to flag it and get deleted by mods.

Aptus housing book yield in closer to 14%, adding LAP and business loans which are higher yield bring the overall yield to 17%. There are some companies that charge even 20+% for housing like SRG housing. These are priced for the potential riskiness of the book. You can ask these Affordable housing companies have very good credit quality and their historical loan loss also low, so they should charge much less. But for every Aptus, Aavas, Home First, we have some many companies struggling in this space like Manappuram, Muthoot, Motilal Osiwal, Ujjivan. Look for the NPAs of the housing book of these companies. And there are lot of companies which does not survive.

But they cannot charge less even if they wish. For a HFC that deals with larger ticket, higher quality customers, credit rating companies are comfortable in letting leverage to inch up to 7-8 times, so they are getting low cost of funds and with higher leverage they can work with thinner NIM and still get a better RoE but for are AHFC they are still looking for a leverage of 4-5, some they have to work with much higher NIM to at least match same RoE. If they try to reduce further, business will not make any money, so companies will stop doing this line of business and EWS have to get money from local lenders and people are still charging 36% at least for these segments.

So 36% vs 17% - not a sin

6 Likes

Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/e6a8ba6a-4c28-4750-bcbd-6f321ba200ae.pdf

1 Like

Aptus continued with their growth trend (28% loan book growth, 23% in disbursement, 26% in interest income and 20% in PAT). They were facing some headwinds in Tamil Nadu due to higher attrition, where growth rates came down to 13% (vs 35%+ in other states). This problem seems to be normalizing now and they plan to maintain 25% loan book growth and add 30-35 branches annually (current branch count is 250). Concall notes below.

FY24Q2

- They increased SME loan rates by 50 bps in September 2023 and NIM growth trajectory will continue in next few quarters

- There was some attrition in Tamil Nadu at branch manager level which has affected growth (13% in TN vs 35%+ in other states). This problem has reduced recently and they are confident of reviving growth rates to 25% in FY24

- Growth strategy is always to go deep into a state and when going to a new state, start with places at border of the state nearby where they already have operations, and expand in a contiguous manner

- Always recruit local people for expansion

- Borrowing cost of NBFC is 25-50 bps higher than HFC (current borrowing cost is 8.25-8.3% for HFC)

- Will maintain spread of 8.5-9%

- Intend to add 30-35 branches annually

- Total pre-closures: 8% (5.5% from customer funds + 2.5% BT-out). According to my calculations, repayment/loanbook is 16% annually in normal times (e.g. Canfin) which translates to 4% quarterly. It becomes a problem when this increases to 20%. For Aptus, current quarterly number is around 4% which is fine

Disclosure: Invested (position size here, no transactions in last-30 days)

7 Likes

I was little surprised when management said the cost of funds for NBFC is only 25-50 bps higher. I kind of expected at least 100-150 bps. 26% per cent of overall consolidated borrowing is from NHB and HFC borrowing is 84% of overall borrowing, so 31% of HFC borrowings comes from NHB which is a much lower rate. Whereas NBFC does not have access to NHB and all 100% is at market rate. This feels like NCD and bank borrowing rate of HFC is higher than borrowing rate of NBFC

1 Like

Thanks for the Q2 FY 24 summary, Harsh.

One minor correction, though. I was on the Q2 concall of Aptus and the management (Mr. P Balaji, CEO) guided for 30% AUM growth, not 25%. (Sounds optimistic, given their H1 numbers, but that’s what they guided)

Aptus has grown AUM for H1 FY 24 (Q1 + Q2) by 13% over March '23 AUM and for them to achieve 30% AUM growth for FY24, then need to deliver 15% AUM growth in H2 (Q3 + Q4) over Sept, '23 AUM. (Quite reasonable, given that Q3 and Q4 are seasonally a shade better)

Also, given that bulk of branch additions for FY 24 have already been done in H1 (around ~25 branches already opened in H1 out of ~35 to be opened), the guidance seems palpable.

Q2 Con call excerpt of Aptus below:

P.S. - I was also on the Q2 call of Aavas and their management has guided for 20-25% AUM growth and the management of Home First guided for 30% AUM growth for coming 2-3 years.

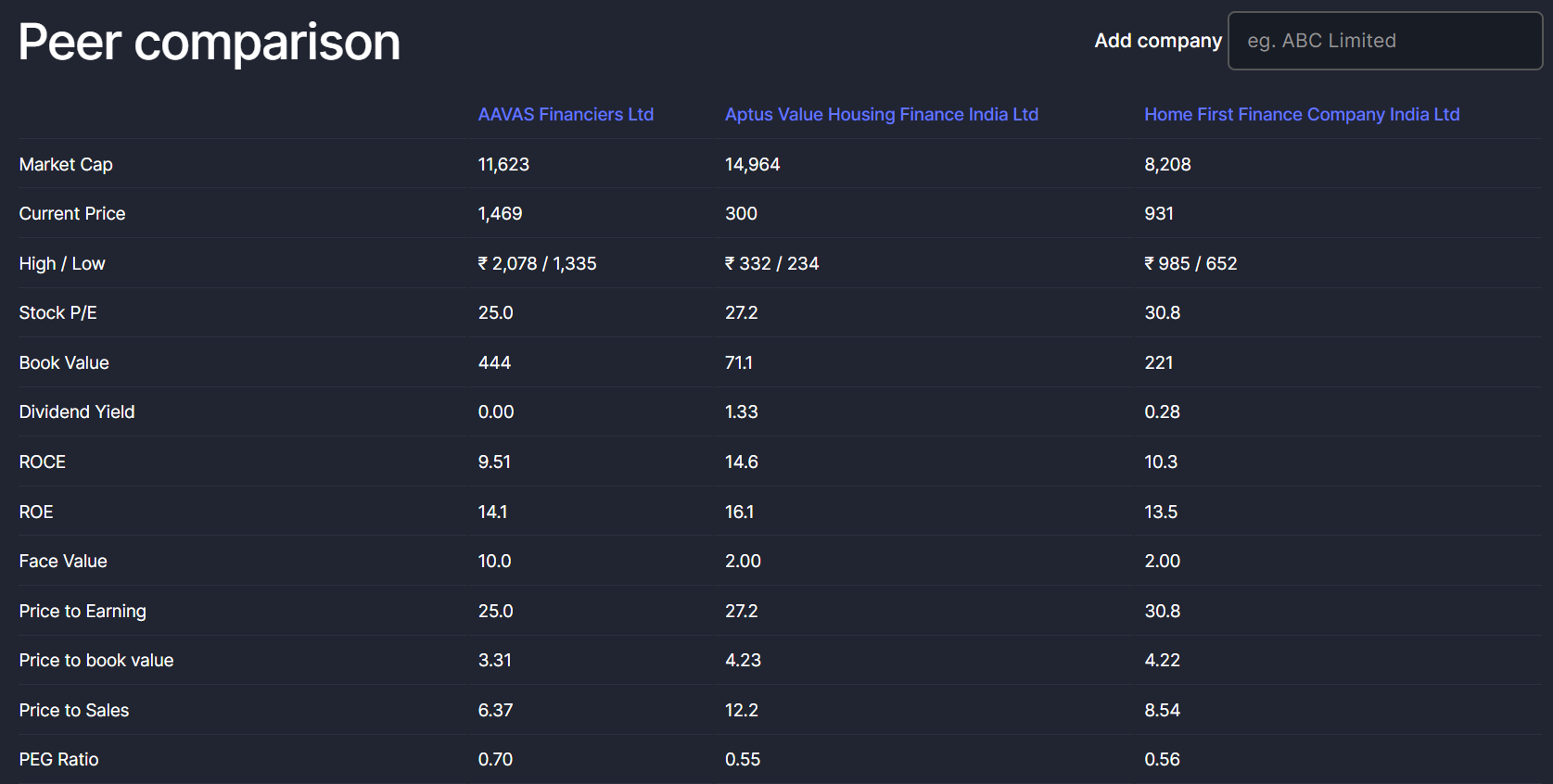

This is perhaps why Aavas is now trading at 3.31 times book, while Aptus and Home First are trading at 4.23 and 4.22 times book respectively.

Aside form these points, here are few aspects that are noteworthy for Aptus:

Aptus enjoys superior margins compared to Aavas and Home first due to its lower leverage (1.1 D/E) and thereby lower interest costs

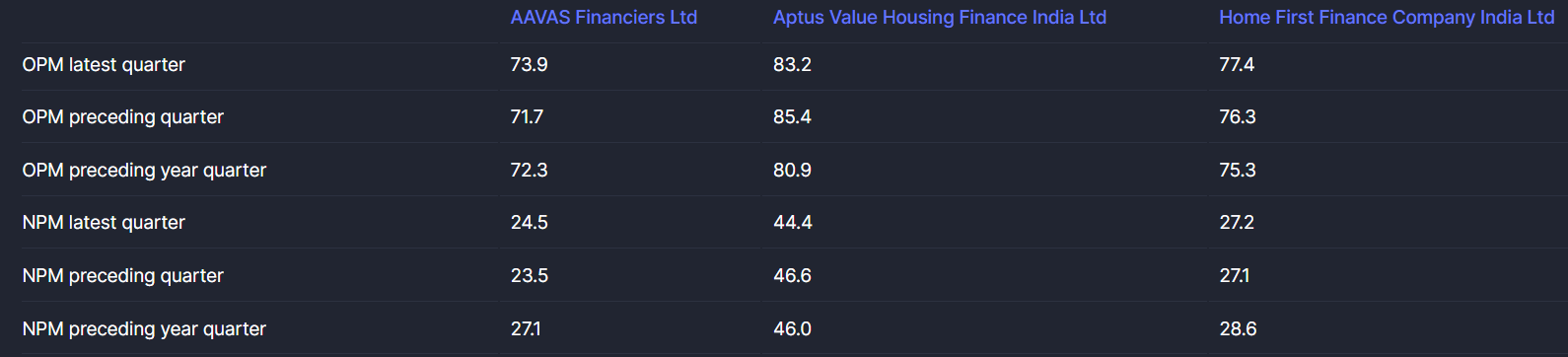

Leading to almost 2x PAT margins for Aptus (44% PAT Margins for Aptus!, compared to 24% and 27% for Aavas and Home First)

Quite Naturally Aptus has high ROAs to boast, compared to its peers: (Almost 2x ROAs)

Also, such high PAT margins and ROAs for Aptus, will lead to accelerated retained earnings and book value growth for Aptus (Unless they don’t have high dividend payout rates - Right now Aptus has 20% div payout rates, Home first has 10% and Aavas pays zero dividend).

Management is quite seasoned and the market opportunity is huge. Interesting times ahead!

Disclosure: Invested. Potentially biased.

8 Likes

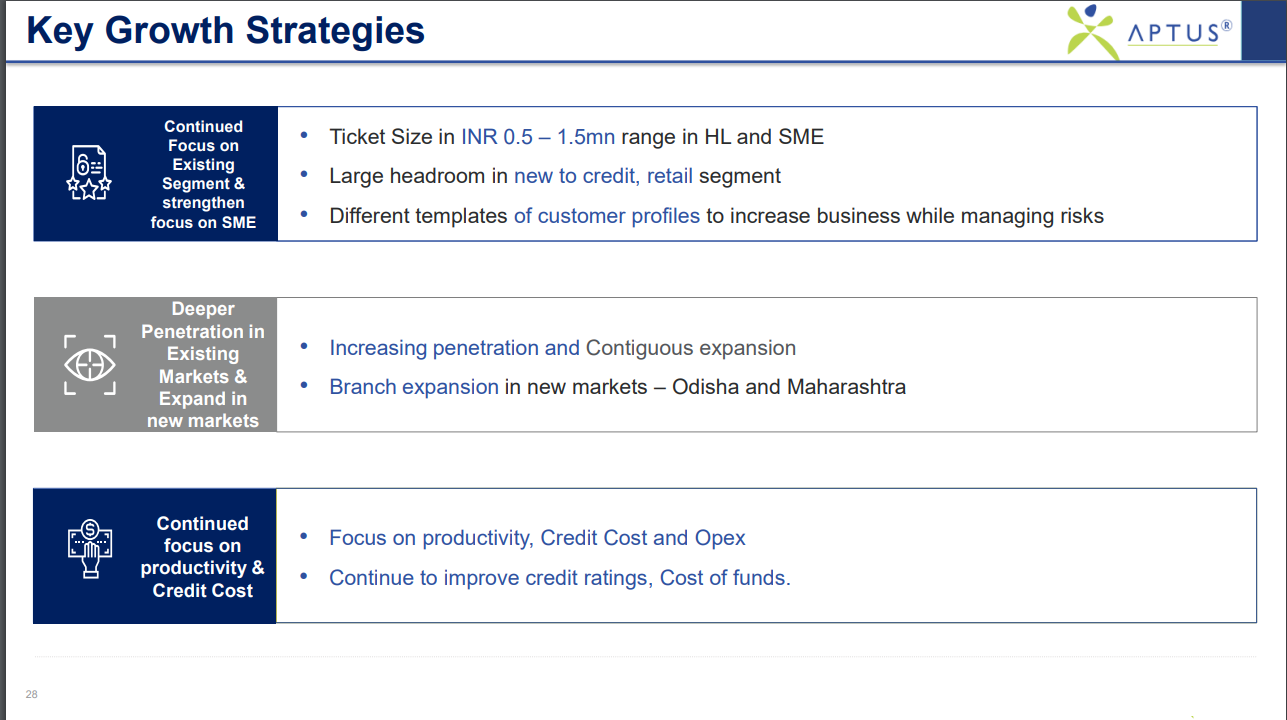

Growth Strategies

- Increasing penetration and contiguous expansion: The company aims to expand its reach in existing markets while simultaneously entering new markets like Odisha and Maharashtra.

- Focus on productivity, credit cost, and operating expenses: The company is committed to improving operational efficiency and reducing credit costs, with a specific emphasis on enhancing credit ratings and lowering the cost of funds.

- Target ticket sizes in the range of INR 0.5 to 1.5 million for home loans (HL) and small and medium-sized enterprises (SME). This approach provides a broader customer base, with ample room for growth in new-to-credit customers within the retail segment.

- Utilizing various customer profiles and templates to increase business while effectively managing risks. This strategy allows for diversification and flexibility in reaching a wider range of customers.

Please watcth recent interview of Sumeet Nagar on ndtv in the programme Talking Point about Aptus

4 Likes

I just listened to their Q32024 Call. Good numbers overall. I would like to understand 2 things if anyone can clarity phase -

(1) How come their capital Adequacy is so high? 70%. Does that mean they achieved this growth mainly through internal accrual? Their borrowing is so low compared to Equity.

(2) is MD Balaji a relative of Mr. Anandan or a professional hire? I am trying to understand what stake MD has in the Bank?

Answers to your questions:

-

Capital adequacy is super high because they raised a fair chunk of capital during ipo. Debt/equity was also < 1 at the time of IPO. CAR is reducing quarter on quarter as the company is leveraging and will likely move towards 25% at a 4-5x leverage. Aptus is super profitable with 8% roa and 17%+ roe which result in high internal accruals as a result the decline in car and roa is slow (a great problem to have!) and roe is increasing slowly. In order to speed up this process they have started paying dividends (because the raised too much during ipo, when markets were buoyant).

-

No, Balaji is not a relative of Mr. Anandan. He is a very early employee and was brought on board as CFO. Recently promoted to MD, he is super competent.

Disclosure: 25% of portfolio.

8 Likes

Very good response. Thank you for the clarification.

1 Like

The Malabar strategy for Aptus resembles a niche industry segment, buoyed by long-term secular growth and favorable tailwinds, with a nuanced consideration of interest rate impacts.

Within the affordable housing segment, there exists a notably limited penetration, offering a substantial runway for growth. Aptus stands out as a prominent player in this arena, benefiting from enduring tailwinds.

While interest rate tightening may have some impact on the housing finance segment, its effects are primarily limited to new flows and incremental borrowing. Effective management of assets and liabilities can mitigate these effects considerably. Although there is an undeniable impact, it remains relatively modest.

Moreover, there are additional levers at play, including operational expenditure management and asset quality control. Within the affordable housing sector, companies like Aptus possess sufficient resilience to navigate and absorb minimal interest rate hikes more adeptly than larger players with shorter asset durations.

3 Likes

Hi, Harsh Bhai, how do you value Aptus Home First Finance for valuation? Which method do you prefer to use?

Aptus continues to do very well, growing AUM by 29% in FY24 while maintaining 8%+ ROAs. They are confident of growing AUM by 30% in FY25. Concall notes from last couple of calls below.

FY24Q3

- Central audit employees reduced sequentially because there was a reclassification from central audit to head office (HO/operations)

- Opex will continue to be in the 2.7-2.75% range

- Have started booking some LAP loans in NBFC which was earlier getting booked in housing finance entity

- Reduced fixed loan borrowing because they envisage reduction in rates (so tactical in nature)

FY24Q4

- 30% growth in FY25

- Sequential decrease in # sales employees is due to attrition at lower employee grades

- Maintain 1-1.5 months of disbursements as cash equivalent

- Want to take leverage to 5x (equity / advances: 0.2)

Hard to say, at these high growth rates with such unit economics, they can even trade at 10x PB assuming they can maintain this combination of growth, profitability and asset quality. I am not really modeling an exit valuation yet, just seeing the picture unfold slowly.

Disclosure: Invested (position size here, no transactions in last-30 days)

2 Likes