Mr Anandan did an interview with Money Purse in Telugu in Aug 21,

Here’s the transcript of the same.

Overview of Aptus -

Provide home loans to retail (largely from lower/middle income) who are self-employed staying in lower tier towns, loan size - 5L -25L

Avg loan - 9L, avg EMI - Rs 12500.

The loan is provided mostly for building a house on customer-owned land (Self Construction) in tier 3,4.

Banks/Large HFCs are present in the higher loans segment and metros/towns but not present in the affordable segment. They don’t service Tier3/4 towns. They avoid this segment as they cannot service last mile customers i.e. go to customers’ homes, do not lend to people who are new to credit (no cibil) and can’t lend without proofs like IT returns and bank statements.

The above borrowers who are not serviced by the big players we are servicing.

There is a perception that lending to lower strata is high risk and high bad debt, hence big players stay away. If we can find borrowers while doing well for themselves in their businesses but are avoided by other financiers as they are not accessible then lending to such borrowers is a lucrative opportunity.

It is important to provide loans to such borrowers as no other bank/HFC will approach the person and building a home is important for low/middle-income borrowers. People in medium to high income, the accessibility for house loans is easier and even if the requirement for a loan is not there, the big HFC/banks will be approaching you by calls/SMS/branches.

Aptus Business Model is 100% in-house - from sourcing loans, credit underwriting, legal, valuation of homes, and collection.

With 2000 staff and 90 branches, 150 in head office, remaining 1850 in 90 branches with separate persons for sales, credit disbursal, legal and collection all working under branch manager.

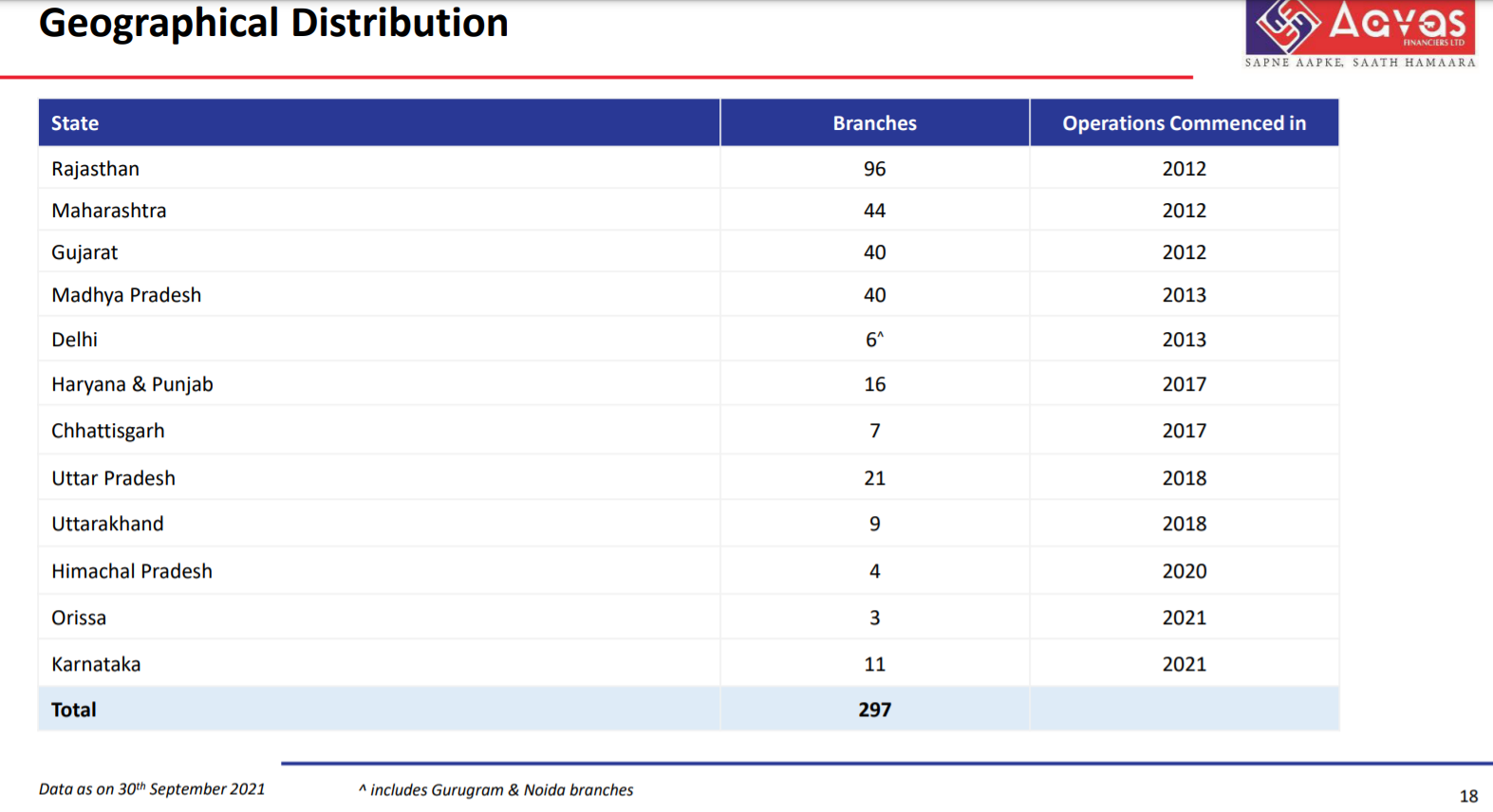

Every 80-100 km we have branches, planning to expand more.

We go to the borrowers’ business place and check who in the borrowers’ family are earning members, we sit for a few hours and check how many customers the borrower is having, how much and what stock is present in conducting the business of the borrower. Monthly bills related to purchases by the borrower to conduct his business, if they are present, we will collect such information as that gives us an idea of how much business the borrower is doing. We also spent time at the current home of the borrower as well, what type of vehicle they own 2/3/4 wheeler. How many children do they have? what school do children go to? what is the electricity bill? to understand the standard of living? who all are earning and dependent members? Location of property?

Prefer to lend if the land is already owned by the borrower, for an average construction cost of 12L we provide a loan of 8-9L. The total value of the property comes to 12L(land)+12L(construction). At 8L, we have enough margin of safety, and one of the reasons why we have low NPA.

75 out of 100, Emi gets cleared by bank debit/cheques/nach. 20 need to be collected by cash.

5 have an issue in paying EMI. In this situation, we can enforce legal means, we initiate legal means, not with the intention to repossess the property but to bring the borrower to the table and make him clear pending dues. 4 out of 5 usually clear their Emi at this juncture. 1 however goes to NPA. but in the entire 10 years, we have to date auctioned off not more than 15 properties.

Reason for low auctioning - we try to educate the defaulting borrower that there is more loss in auctioning property as auction means u will not get the market price of the house. also, we include neighbors/friends and relatives as a last resort to sell the property at market price and repay the loan.

Talks about IT - there are around 300 collection staff, as MD from my system, I can track all 300 collections, and see who all customers he has met, and how much km he has traveled by tracking via an app.

We try to keep operating expenses low. one example is creating a pre-defined route for the field team for customer visits.

Documentation is done in the local language, not English, and staff are all locally hired.

Try to have customer complaints in app/branch and proper redressal system with escalations from branch manager up till myself (MD).

Building a good relationship with customers is very important in this business, doing good to them helps us as it creates more value by them referring their friends/relatives also to Aptus for loan requirements.

Talks about assets quality and loan growth despite Marco headwinds (covid 1,2) and issues faced by HFCs like dewan.

Question on Business Loans

Business Loans is LAP; business loan customers’ profile is different from house loan customers’ profile.

Home Loans at 14% and Business Loans at 21%, blend 17-17.5%

Business Loans avg 7L, around 5-15L disbursals.

21% looks optically high but talks about competitions like 5-star finance, SCUF, Muthoot and manapurram all charge over 21% around 24-27%

Only Fullerton and HDB charge around 18-21%.

Also talks about Aavas, tell that we have business loans in our book which increased our blended yield higher than pure play HFC like Aavas. resulting in higher Roa.

Question on High Equity base

IPO proceeds increased equity further, not leveraging equity by taking additional debt -

Reason - 500 cr from IPO came only at 3-4% dilution, however not required in the next two to three years, but still listed.

Being unlisted for 10 years to a listed company now, there is higher respect for being listed by banks, rating agencies, Mutual Funds, Insurance, and Foreign institutions. We can diversify funding sources. A listed co can also attract good talent.

With higher equity (500 cr from IPO) and lower gearing, there is now scope for a rating upgrade. cost of funds will come down by 1-1.5% if an upgrade happens.

Insurance companies have mandate to only lend to the highest rated nbfc, and when we get an upgrade we get to diversify our liability base which will also help in reducing COF.

Even though ROE comes down due to equity raise, COF reduction will compensate for the ROE drop.

Question on TAT as HomeFirst does in 48hr.

We use technology only when we feel relevant,

Tech used on customer acquisition, customer service, underwriting, collection, dashboard, AI analytics, and cheque bounce forecasting.

For salaried class providing loans via online using bank statements can result in lower tat and customer prefer faster TAT, but in our business, from the time customer application, we can provide sanction in 4-5 days. however, we spend the next 7-8 days doing due diligence starting with a visit to the sub registrar’s office for land documents, legal team will check the land records and create the mortgage, checking for existing encumbrance.

Documents to be collected from Govt. offices and doing due diligence on this will take time. Talks about how each state they are in, the quality of sub-registrar offices and land records, and sale deeds are different, so can’t paint all with one brush. First, the Govt. should push the land ownership online, then we can leverage technology. as of the date it’s not there hence will take additional days to do our checks and only after due diligence is completed will disbursement happen.

Question on Geographical expansion and why avoid Kerala?

I love Keralites, was also on board in manapurram,

but we avoid Kerala as there many local banks like Dhan Lakshmi, federal, south Indian as well biggest gold loans Muthoot and Manapurram who have HFC companies in them. plus, Kerala as a state the demand for housing is fully met by all the existing players. we will relook at the Kerala opportunity at later date.

Do not believe in an all india company tomorrow, with 190 branches you can have 5-10 branches in all states, but we would prefer to be no 1 a geography and then only expand. We would like to grow more in AP, TS, and KA. we are also looking at 3 more states in MH, CH, and OR as they are adjacencies to our existing states. prefer to have deeper penetration than expansive reach.

Question on why should investors invest in aptus?

We are a High-quality co that can deliver consistent growth for long periods of time and will continue to have good asset quality with low NPA.

We have a high level of productivity leading to low operating costs. all resulting in higher ROA, and high ROE.

We are having good corp governance, very transparent, 0 related party, 0 unrelated diversification, Big 4 auditors, broad is very experienced and diversified.

Our market is still underserved and good runway to grow, we understand this business and have a management team to execute and deliver.

Question on Succession planning

None of my family members want to join the business after me, So the board will identify and select a professional, it will be professionally run and, I would be only an investor after I exit.

Youtube Link: APTUS "0" Bad Debt ఎలా Maintain చేయ్యగలుగుతుంది? Grow అవ్వడానికి ఉన్న Scope గురించి తెలుసుకోండి - YouTube