What other company is giving you an roa of 8% and roe of 16%+ with a gearing of just over 1x, while growing over 20% yoy? when gearing tends towards 3-4x roe will easily surpass 20% while roa remains relatively stable at 5-6%.

Hey guys just a quick question, I was going through the transcript for Q4 FY24, and when it comes to the Asset Quality Part, what does Mr. Balaji mean by “Undrawn Sanctions”?

Few of my takeaways from Q1 FY25 of Aptus Value Housing Finance

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲:

Aptus Value Housing Finance demonstrated strong performance in Q1 FY25, with 27% YoY AUM growth to Rs. 9,072 crores and 21% PAT growth to Rs. 172 crores. The company maintains a positive outlook on growth opportunities in Tier 2-4 cities, driven by low mortgage penetration and significant housing shortage. Management expressed confidence in achieving their 30% disbursement growth guidance for FY25.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

Geographic expansion: Opening 40 new branches in FY25, including in new states like Maharashtra and Odisha.

Technology adoption: Implemented a mobile-first lead management system to improve efficiency and productivity.

Digital channels: Increased focus on customer referral app, construction ecosystem app, and social media channels for lead generation.

Productivity enhancement: Rationalization of collection team and focus on improving per-employee productivity.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

Increasing penetration in existing geographies

Contiguous expansion into new states

Focus on digital channels for lead generation

Emphasis on productivity and cost efficiency

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

Low mortgage penetration in Tier 2-4 cities

Significant housing shortage in target markets

Government initiatives supporting affordable housing sector

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

Potential cyclicality in affordable housing segment

Rising interest rates impacting borrowing costs

Competition from other players in the affordable housing finance space

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Concern: Slowdown in Tamil Nadu growth

Response: Management acknowledged issues but expects 20% growth in FY25 with corrective measures in place

Concern: Rising 30+ DPD

Response: Attributed to seasonality and elections; expect improvement in coming quarters

Concern: NIM compression

Response: Expect 10-15 bps NIM compression due to rising borrowing costs

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

Aptus faces competition from other affordable housing finance companies and small finance banks targeting similar customer segments in Tier 2-4 cities.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

30% overall disbursement growth for FY25

20% disbursement growth in Tamil Nadu

Credit cost guidance of 0.3-0.35% for FY25

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

The company maintains a strong capital position with a net worth of Rs. 3,800 crores. No specific capital raising plans were discussed, indicating sufficient capital for near-term growth.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Opportunities:

Large addressable market in underserved segments

Expansion into new geographies

Leveraging technology for improved efficiency

Risks:

Potential asset quality deterioration in economic downturn

Increased competition in affordable housing finance

Regulatory changes impacting business model

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐥𝐢𝐦𝐚𝐭𝐞:

The company benefits from priority sector classification for housing finance. Management mentioned adapting to recent RBI circulars on disbursement practices.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

The management indicated strong on-ground demand for both home loans and small business loans in their target markets.

Hi just started tracking Aptus. Quick question to those who are invested. Is there a risk to capital raising especially from NHB refinancing. The management mentioned there is an audit that is done by the NHB team every year to determine how much capital can be provided to Aptus.

Also Westbridge capital (promoter) has been offloading its stake. Is that a concern?

@Pulak I think the overhang due to the mentioned large investor sell off is bringing down the price. This generally happens with all IPOs 2-3 years into the listing. Early PE investors sell their stake.

Another reason for weakness is sector sentiment. NBFCs and all banks are going through this because the banks are going through slow deposit growth phase. I am not sure if you had followed this whole discussion on people moving from term deposits to equities. If banks face this pressure they are going to cut down on their lending to NBFCs. Aptus borrows from banks and the exposure is probably 15-20%. There was a news article as well on this issue, just google it.

Lastly, I can see concerns in unsecured lending (microfinance) as NPAs are slowly rising and RBI issued a circular few weeks back on microfinance. Though this should not apply to Aptus as much because its dominantly a HFC. Their SME financing is also collateralized probably as I remember they mentioned LTV on these loans of 42% (need to check again this).

I think once the market sentiment improves its going to be a clear value buy, aptus at 300 is super cheap. They are growing AUM at 30%.

Thanks @Shivam_Jindal for the detailed response. You are right in highlighting why the stock price has been correcting. I agree with you on the same. I am not so much focused on the stock price as long Aptus is not short on liquidity

My question was whether Aptus is likely to face any liquidity crunch as banks and nhb are big sources of capital. While Aptus is well capitalised at the moment I understand nhb refinancing happens every year after an audit exercise by the nhb team. Would that be seen as a risk going forward. It may not be so.

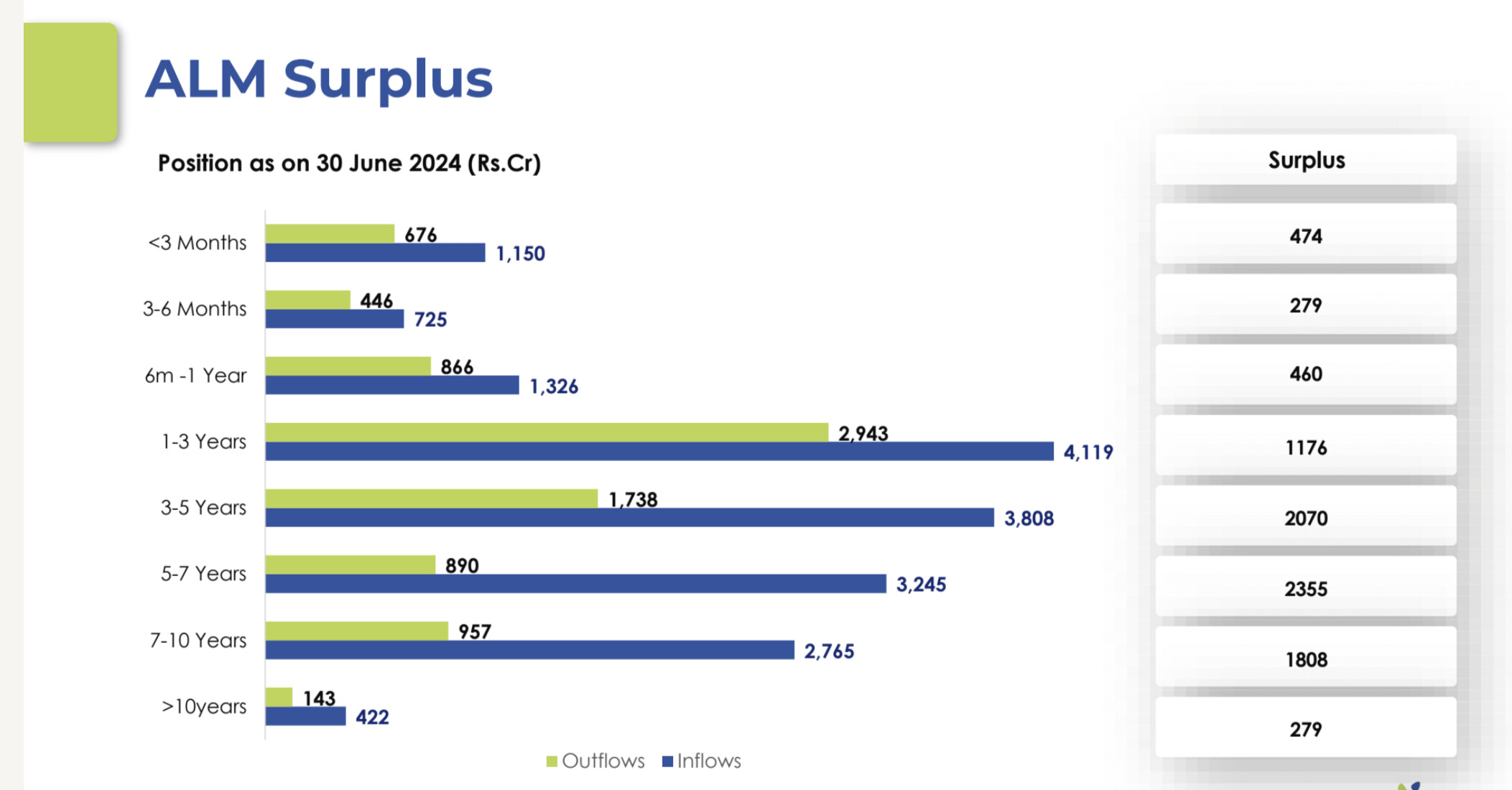

Hi Pulak, their capital adequacy is 71.8%, its so high that they have been paying very high dividends to bring it down which improves ROE. Look at their ALM slide, there is surplus in every timeframe, so there is no concern on liquidity at all.

Thanks much @harsh.beria93 . Looks well covered. Let’s hope their expansion into new states is measured and develops well.

They have indicated they want to dominate the regional markets they are in and not stretch themselves across the country chasing growth, which is reassuring.

Never heard of a bank or NBFC paying dividend to bring down their capital adequacy ratio and I don’t think that’s the case here. If they had too much capital they won’t be borrowing from the market (at a higher rate) while paying dividends from retained earnings. It’s a bad capital allocation. Why not lend excess capital which if done well can be ROE accretive? Or even better, do a buyback that tends to be more shareholder friendly than paying dividends.

One should look at other plausible explanations. I can offer a few without being sure of any but it can be always very instructive to look at such practices from several angles in a bull market.

For example company has not been paying any dividend until couple of years ago and for a profitable company it always raises flags with potential investors. So they started paying 15-16% (by no means very high) dividend which is surely healthy. It could be just coincidence but since they started paying dividend there has been significant increase in both DII and FII holding.

Company’s stock prices has been depressed in this scorching bull market and for many promoters and executives it can be source of stress. I won’t be surprised if they announced a QIP.

Also biggest risk with financial institutes is quality of their disclosures. For an auto company you can do several checks outside their books. For a financial company you just rely on their reporting. My rule of thumb in a bull market is to take all the numbers with a pinch of salt.

I think it’s the case with all the AHFCs like Aavas also.

Though it’s not a good practice to compare on a PE basis, they have been derated from PE around 40 to 25 currently.

None of the AHFCs have shown any price appreciation during this bull run.

Sooner or later they have to show the price appreciation reflecting the AUM growth.

In my view Avvas Financier’s poor stock performance has been mainly because of high valuations. Until 2 years ago stock used to trade at 6 times book which was clearly excessive given 13-14% ROE of the business. Stock has been in time correction.

Clearly the market is less generous to NBFCs on valuations following RBI’s restrictive policies and higher cost of funds. And none of these small-mid caps NBFCs, Aptus or Avaas, are posting spectacular numbers on your typical parameters such as ROE, NIM, AUM growth etc.

A sane investor will ask as to why they should buy an NBFC at 3-4x book for 14% ROE when they get 16-17% ROE from many dividend paying large private banks current valued at 2 times book.

We’ll have to wait till interest rate cuts and some easing in RBI’s restrictions to see some action in stock prices of these NBFCs.

Actually Aptus is not great in capital allocation. 1st they raised fresh capital in IPO rather than doing only stake offloading even though their CRAR is crazy high. 2nd, after raising fresh money at high valuation and giving 40% of profit as dividend as if they do not need money.

By giving higher dividend, they themselves are proving capital raise is wrong decision

I disagree that they might go for QIP. Capital is raised in two ways - debt and equity. Debt/equity ratio is generally over 3x for most lenders but it is < 2x for Aptus. This is also the reason they are comfortable in paying dividends as they have adequate equity buffer. Their target from here would be raise more debt from banks/NHBs instead of raising equity.

@Pulak I see your concern on NHB refinancing. But from what I understand it shouldn’t be a problem for them to secure it this year too. The government is very supportive of financing affordable housing. It was mentioned multiple times in speeches and even in “Final Budget key note”.

Besides their ratings are not bad, look at the credit report. Care assigns AAA to most secure lenders and AA is second to that. Read their rationale behind it.

Yes there are concerns about self-employed borrowers who experience uncertainty in their cash flows, however I personally would take this much risk willingly, particularly given their LTV doesn’t go beyond 50% and avg LTV of whole portfolio is ~40% as most of the portfolio is for HFC where LTVs are <40%. Secondly, SMEs are expected to do good in coming years as government is strongly pushing for them, if you have noticed in this budget too there was a scheme for bank guarantees from their side for SME loans.

As far as geographical diversification goes, they have done pretty good so far and going forward their Karnataka allocation is gonna increase as this region AUM is growing at over 30% vs their traditionally dominant region Tamil Nadu which might be growing at 10-15%.

I didn’t say they will go for QIP. My statement was “I won’t be surprised if they announced a QIP”. So it’s just a speculation and there is nothing to disagree with :). In stock market one thing I have learnt, the hard way, is never to be sure of one’s opinion and be ready for surprises.

Paying Dividend is another way of bumping up the RoE nos with a few bps. So, the payout made from the Reserves decreases the Overall Book Value/Networth of the company which in turn increases the RoE %.

This logic makes sense for a company clocking decent growth (though less than its potential) but still managing to stick around a 17-18% RoE numbers. Cause when a company grows at 25-30% and they fail to show the similar kind of growth in subsequent years, its RoE decreases.

So, paying dividend is an easy way to keep the Networth under check and maintain a consistent RoE.