I have been a long time holder in this stock and will vouch that the promoters are only interested in making a fortune for their close family members …every 5 years they give bonus but other than that they have too much value unlocking possible but are reluctant to do that since they want to play under the hood. Many representations were sent to get themselves listed on NSE but they were least bothered.

Anuh Pharma came up with another good set of results, with sales growing by 24% and EPS doubling. They are now guiding for 16% CAGR in their sales for next 5-years. I am sharing notes from their recent presentation.

FY24Q3

Planning to invest 20 Cr in existing site in FY25 for capacity enhancing by 70 KL

Focusing on deeper penetration in European markets

Added CEP for Ambroxol HCL (expected CEP for Allopurinol and Sulfadoxine)

Got Approval of Isoniazid from WHO PQ (TB product)

New product launches: Vildagliptin, Acebrophylline, Amodiquine, Moxifloxacin and Allopurinol. Expected to contribute 50 cr. in FY25

R&D pipeline: 6 new products in next 9 months

Guidance: 16% CAGR for next 5 years

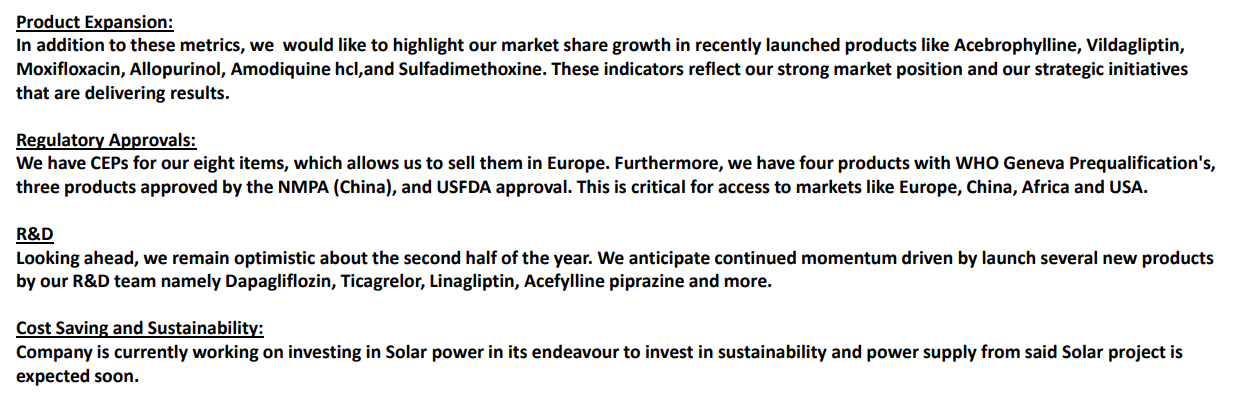

Investing in solar power

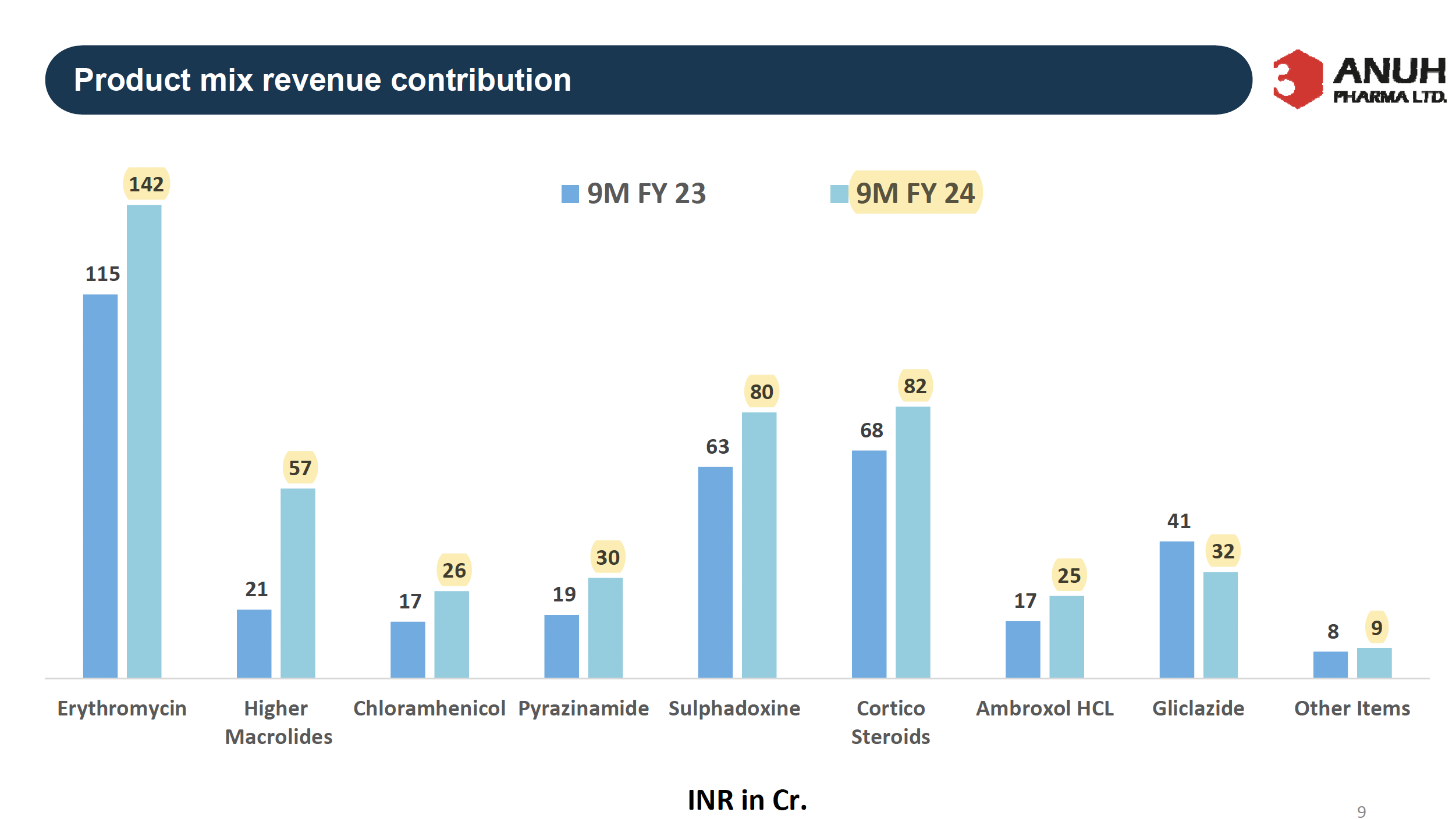

Product mix: most growth was driven by acute portfolio

Hi, any insights on how they will achieve 16% CAGR since no new CAPEX is there in balance sheet, also Q1 results are miss when sector overall is doing good

New Plant commissioned.

Plant - 3

In this regard, please take note that the new Plant is expected to be operational by December 2024,

and this will increase existing overall operational capacity by 400 MT/Annum.

Production capacity:

Existing production capacity (approx): 1800 Metric Tons Per Annum

Total production capacity after API-3 (approx): 2200 Metric Tons Per Annum

At the new Plant, the Company will install 53 KL Reactor Capacity.

Ref:

Disc: Restarted Tracking as this came up in one of my screens, 0.5% of PF. No investor presentations after Feb 2024.

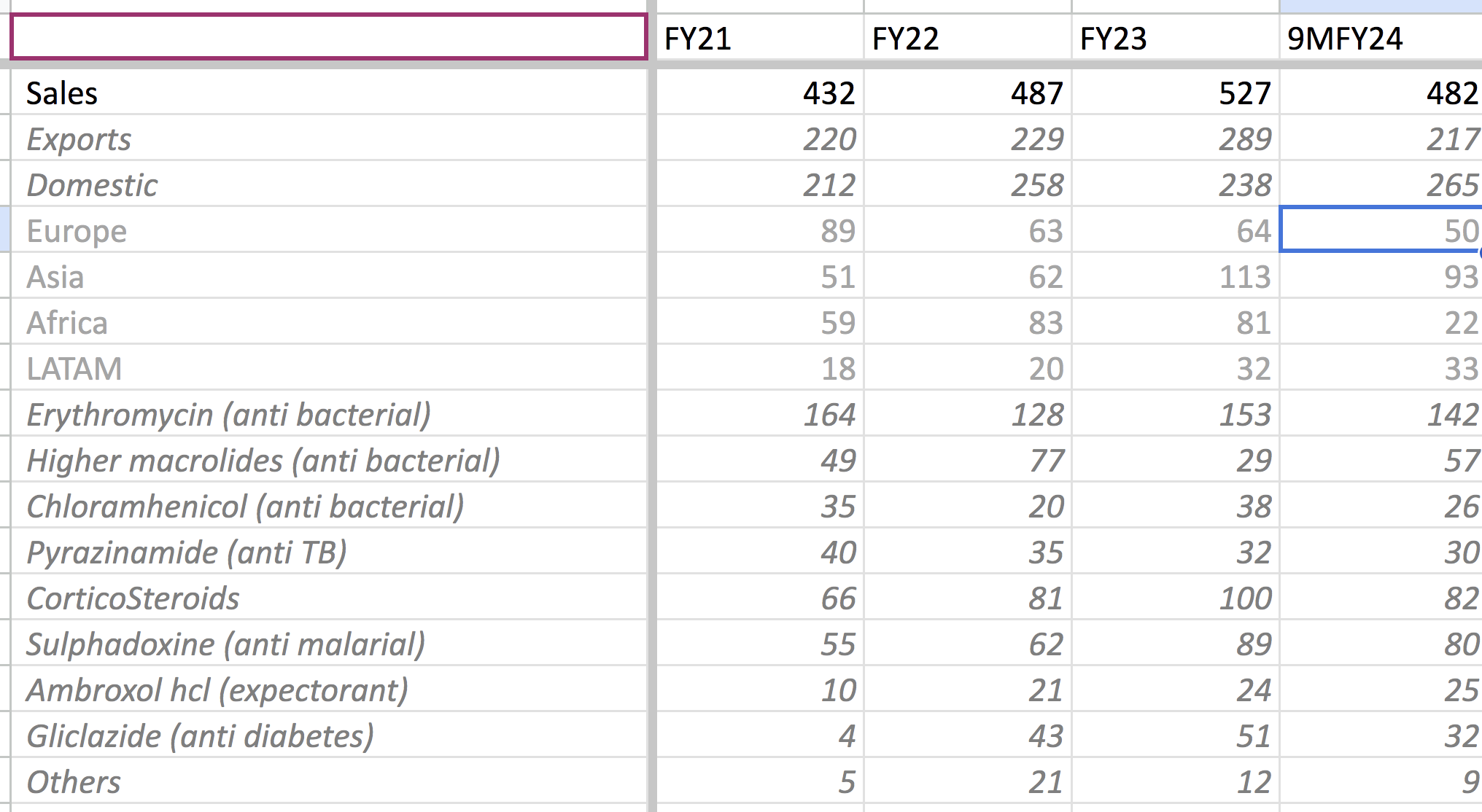

Last 3 years, stock price is lagging behind profit growth, but overall in line with profit growth, Positive Operating cash flow in the last 3 financial years. ROE is improving, dividend payout of 20.9%

Anuh pharma came with a presentation after a year. They have commercialized their new capacity which now stands at 2200 MTPA. They seem to be getting more registrations in Europe which can hopefully drive margin improvement in the future. My presentation notes below

FY25Q2

H1FY25 exports were largely driven by Africa and ROW markets, Europe saw decline

Erythromycin drove growth

Capex of 20 cr. increased capacity from 1800 MTPA to 2200 MTPA (commercialized in November 2024)

New approvals: CEP from EDQM for Allopurinol (Anti gout)

Registrations: CEPs: 8, WHO Geneva Prequalifications: 4, NMPA (China): 3

Market share gains in recently launched products like Acebrophylline, Vildagliptin, Moxifloxacin, Allopurinol, Amodiquine hcl,and Sulfadimethoxine

Expect continued momentum driven by launch of new products like Dapagliflozin, Ticagrelor, Linagliptin, Acefylline piprazine, etc.

They are largely into commodity APIs, their model is invest in capacity, then debottleck for a very long time, and only increase capacity sporadically. As their main end markets are unregulated or India, it requires lesser maintenance capex. They have always had the highest fixed asset turns, however their margins are also much lower than regulated API cos.

They are now increasing capacity more regularly as seen in the 22% capacity increase in 2024. Maybe management is becoming more growth focused.

Disclosure: Invested (no transactions in last-30 days)

Anuh Pharma is finally getting their sales growth back, due to pricing pressure, margins were impacted in FY25. Adding my recent notes on the co:

03.01.2025 ICRA

Revised outlook from Stable to Positive (A-) due to improved revenue outlook driven by capacity enhancements and launch of new products

400 MT capacity enhancement in FY24, increased further to 2,200 MT from 1,800 MT in FY25, funded through internal accruals

Capacity: 2200 MT (1900 APIs + 300 intermediates)

Reported a marginal YoY decline in growth in H1FY25 due to declining realisations and a shift in sales volume for regulatory markets (which typically fetch higher realisations) to H2 FY2025

Expect pickup in demand for high-margin products in H2 FY2025

Erythromycin and its salts ~32-33% of revenues

Obtained CEP for gliclazide and azithromycin from European Directorate for Quality Medicine (EDQM)

Development stage: Ticagrelor, Dapagliflozin, Empagliflozin, Bilastine HCI, Pyronaridine Tetraphosphate and Vonoprazon Fumarate are at the development stage

FY25Q4

Lower EBITDA margin reflecting the impact of external market and cost factors during the earlier part of the year

Plan to expand intermediate manufacturing capacity by 300 MTPA in FY26

Expects 15-16% CAGR growth

Customer base increased from 698 to 737, export customers increased from 260 to 304

Manufacture 40 APIs, 6 introduced in FY25. Expect to add 5-6 new products in FY26

Received CEP for Ambroxol HCL (expectorant cum mucolytic agent)

Product under development: Ethambutol, Sulfadimethoxine Sodium Antibiotic

Disclosure: Invested (no transactions in last-30 days)

Sir, Do you see anything weird in the management? Gaurav Shah and Bipin Shah has been taking 100% salary hikes since last 2 year. Moreover their companies are also purchasing and payment of money where the KMPs are directors?

Although they are doing well, still stock has not been making a move. Is there anything that you can shed light or am I panicking without any issues?

thanks in advance

Disc: Have positions before Bonus share was issued, 1% of my PF

Strong revenue growth (35%; 44% YOY domestic; 26% YOY exports) due to increased customer reach, market penetration, and product portfolio

Capacity increased to 2400 MTPA (vs 2200 MTPA)

Faced input cost pressures, building process efficiencies and product mix change to higher margin products to restore margins

In exports, top-5 customer contribution increased to 55% (vs 32% in Q1FY25). EU contribution increased to 35% of exports (vs 22% in Q1FY25)

Erythromycin increased to 63.63 cr. (vs 41.31 cr.; 54% increase); other items also increased to 34.66 cr. (vs 10.73 cr.)

FY26Q2

Lower margins due to lower sales of certain high-margin products, expect strong margin recovery in H2FY26

Increased effluent treatment capacity from 100 kl/day to 150 kl/day

Commissioned solar power

Advancing CDMO opportunities

Promoter shareholding increased from 69.91% in June 2025 to 71.82% in September 2025

New products added to future pipeline:

o Piperaquine Phosphate (Anti.Malarial)

o Dapagliflozin Amorphous (Anti Diabetic)

o Pretomanid (Anti TB)

o Bedaquiline Fumarate (Anti TB)

Disclosure: Invested (bought shares in last-30 days)