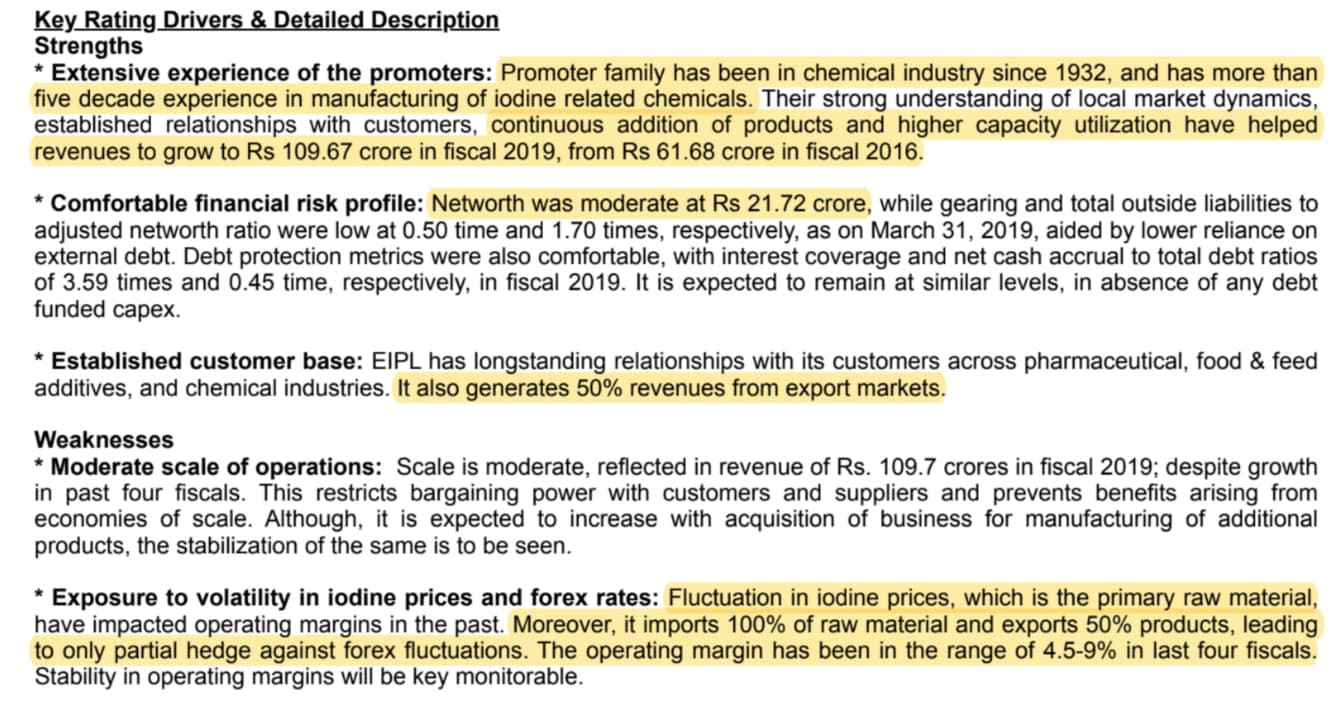

http://www.icra.in/Files/Reports/Rationale/Anuh%20Pharma%20-R-31082016.pdf

Surprisingly the stock has been doing decently in the recent past moving from Rs170 to Rs230 despite bad 1Q and ratings downgrade

http://www.icra.in/Files/Reports/Rationale/Anuh%20Pharma%20-R-31082016.pdf

Surprisingly the stock has been doing decently in the recent past moving from Rs170 to Rs230 despite bad 1Q and ratings downgrade

Looks like this thread has been inactive for very long.

Now that all regulatory issues has been cleared for the company, can the senior members of this thread provide some insight into the current position and future prospects of the company. Requesting the regular followers of the company to provide the current updates, pls. Thanks…

technically , i see something very interesting shaping up in the monthly charts in this scrip…

if anyone still tracks this company , please post some updates and present state of business

If anyone is still tracking this company? How is this shaping up in comparison to Granules, Aarti, Solara etc? I think they have recently finished some capex (?) And revenue should starting coming in for the next 4-6 quaters?

Researchers in England say they have the first evidence that a drug can improve COVID-19 survival: A cheap, widely available steroid reduced deaths by up to one third in severely ill hospitalized patients.

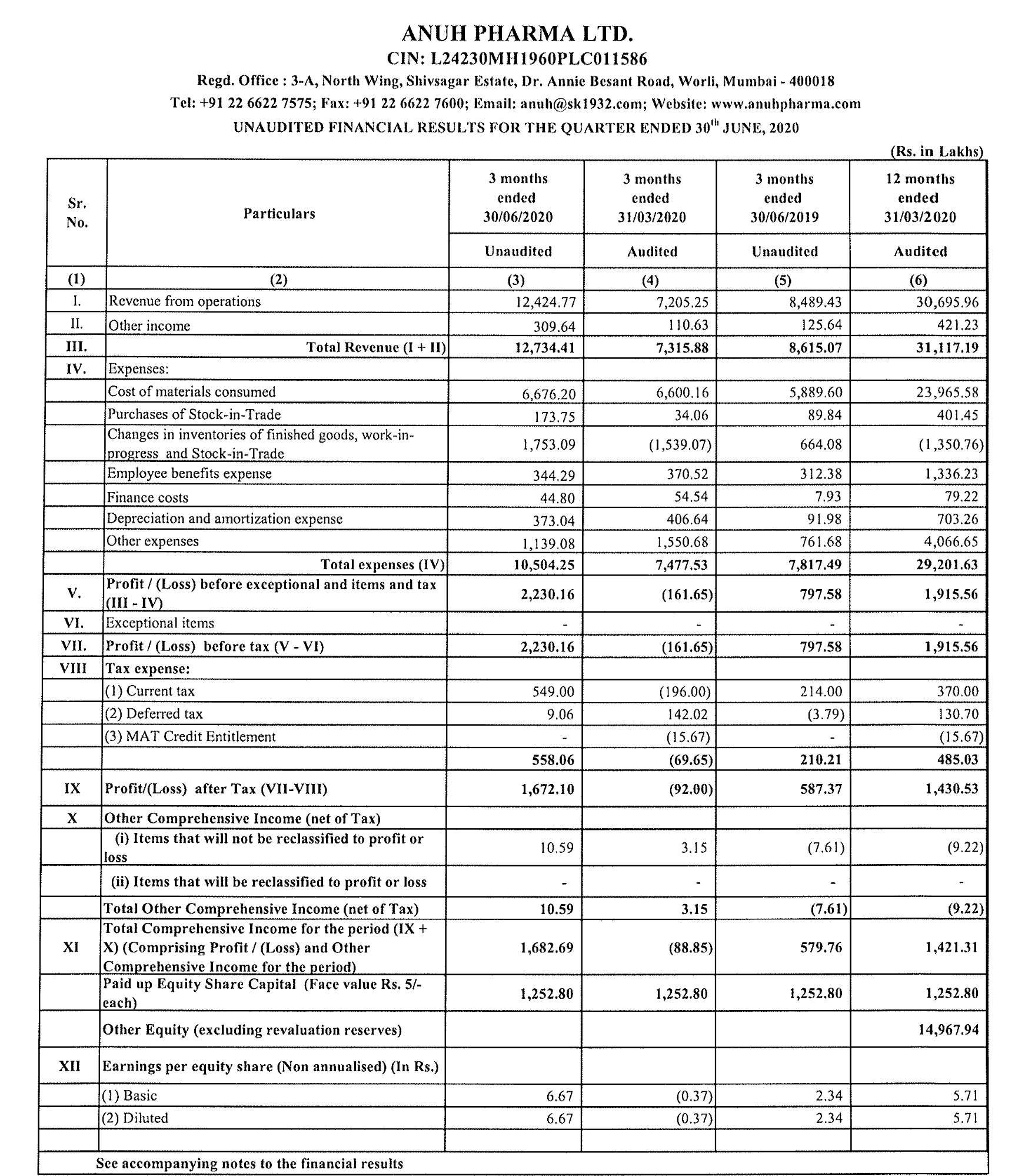

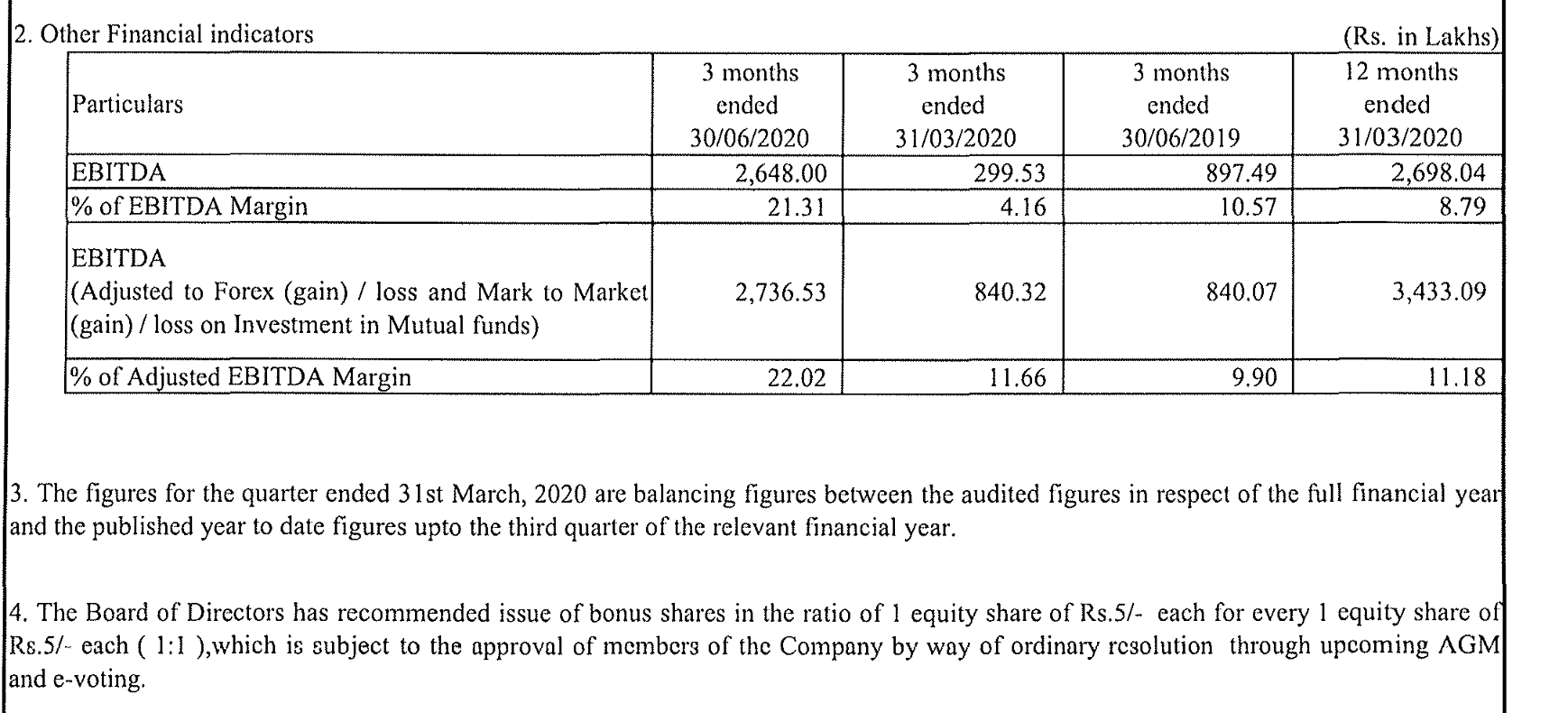

Excellent results this qtr with margin improvement…with 1:1 bonus announced…

EBITDA margin improved to 22% from 10% last yr…

Hi, just want to check if anyone has received the bonus share in their demat account?

I haven’t received yetstrong text

Same here haven’t received the bonus share in my demat account…

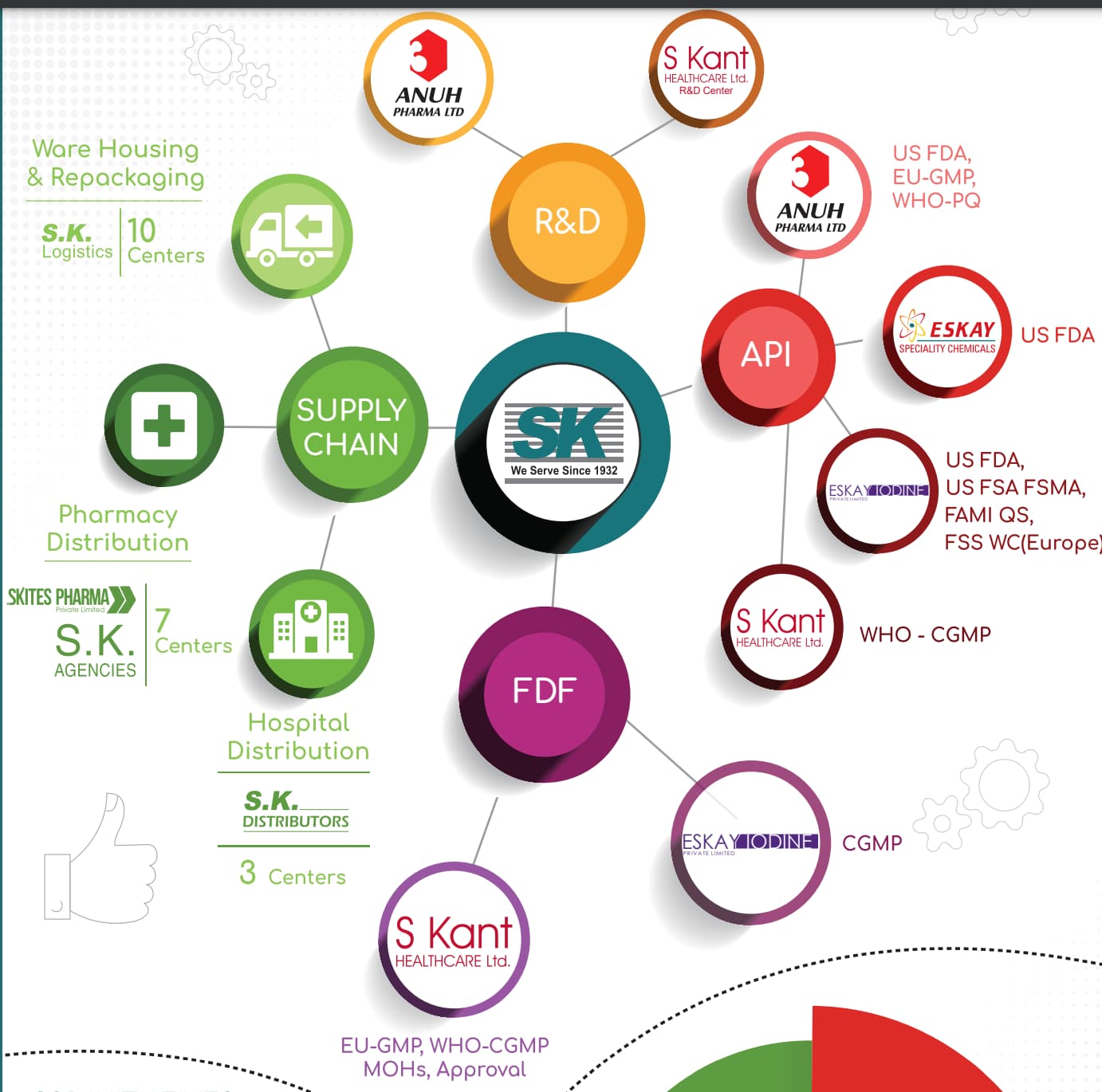

I am sharing my work on entities related to the Anuh Pharma group.

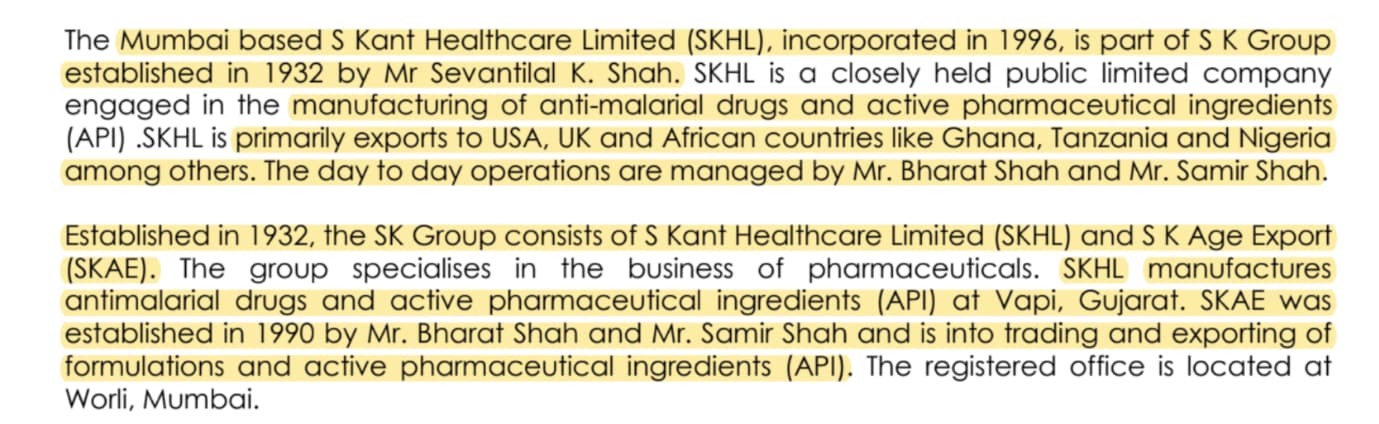

The 4 main group cos operating in pharma sector are Anuh Pharma (listed co), Eskay Iodine (operates in iodine based APIs), S Kant Healthcare (formulations business in Africa), and Eskay Speciality (specialty chemical business).

Eskay Iodine

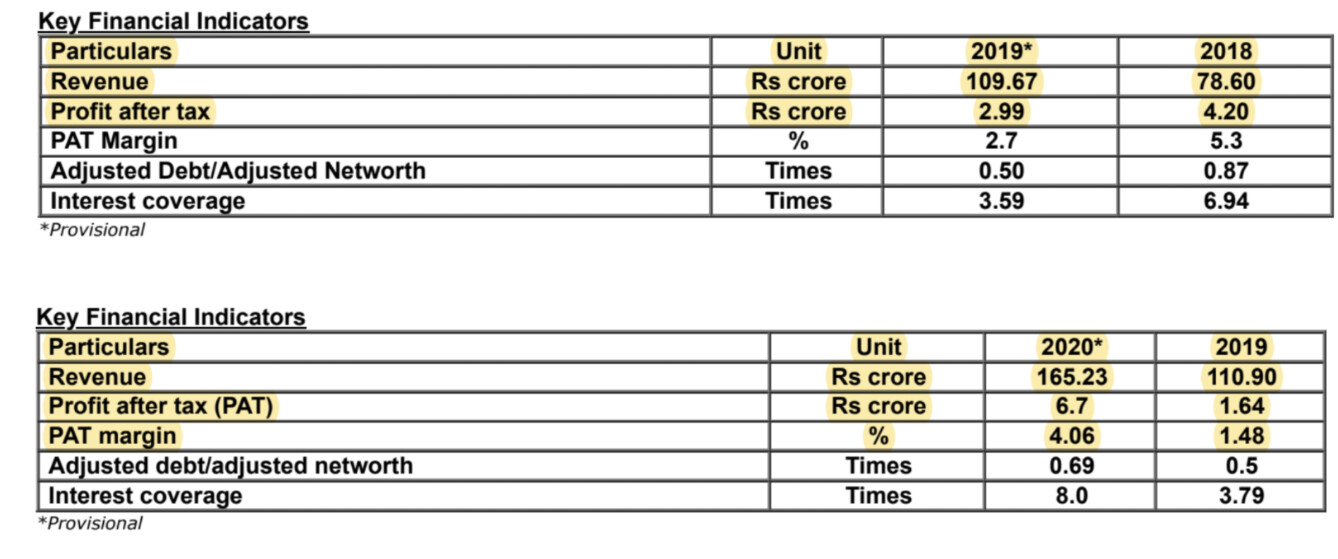

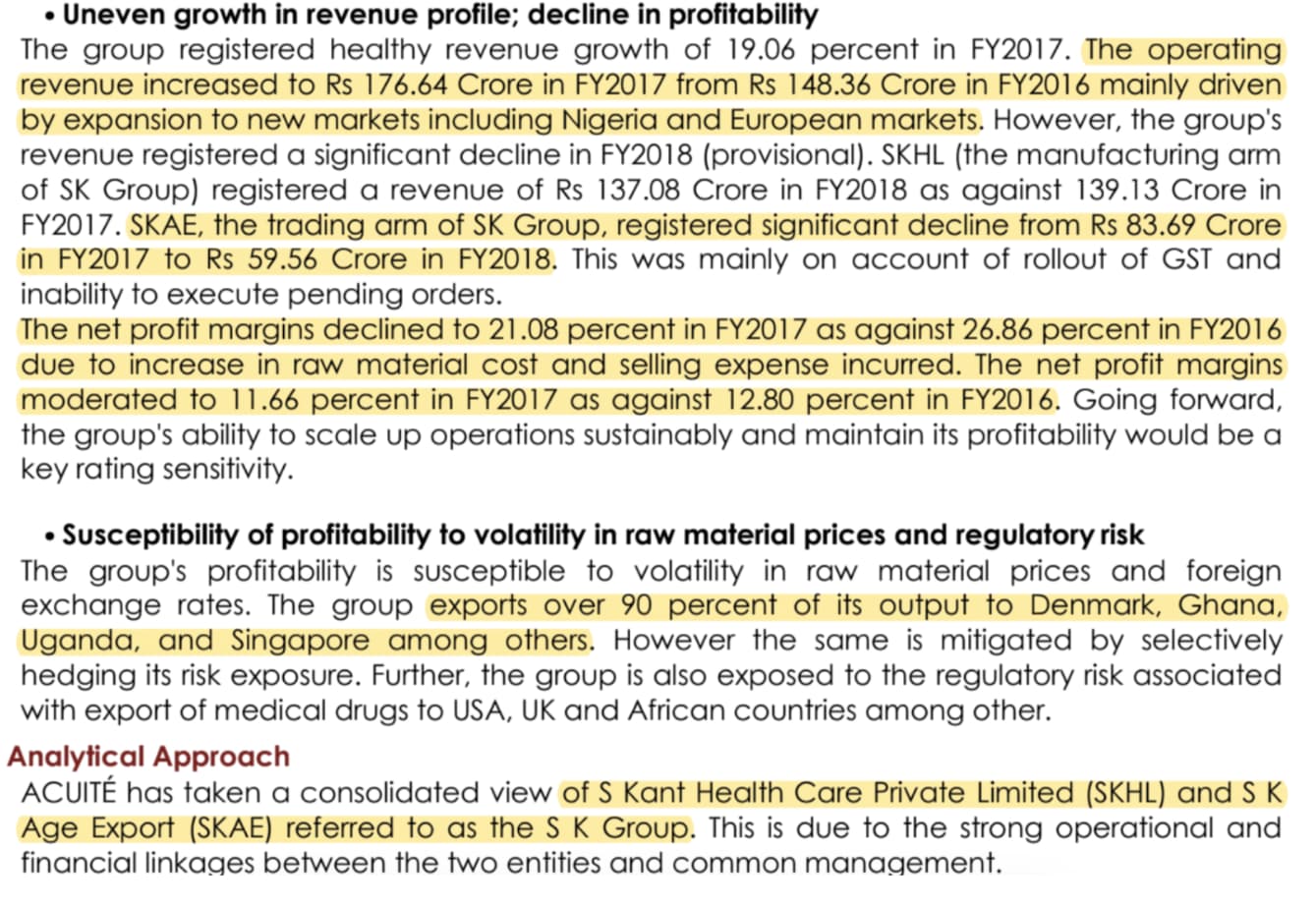

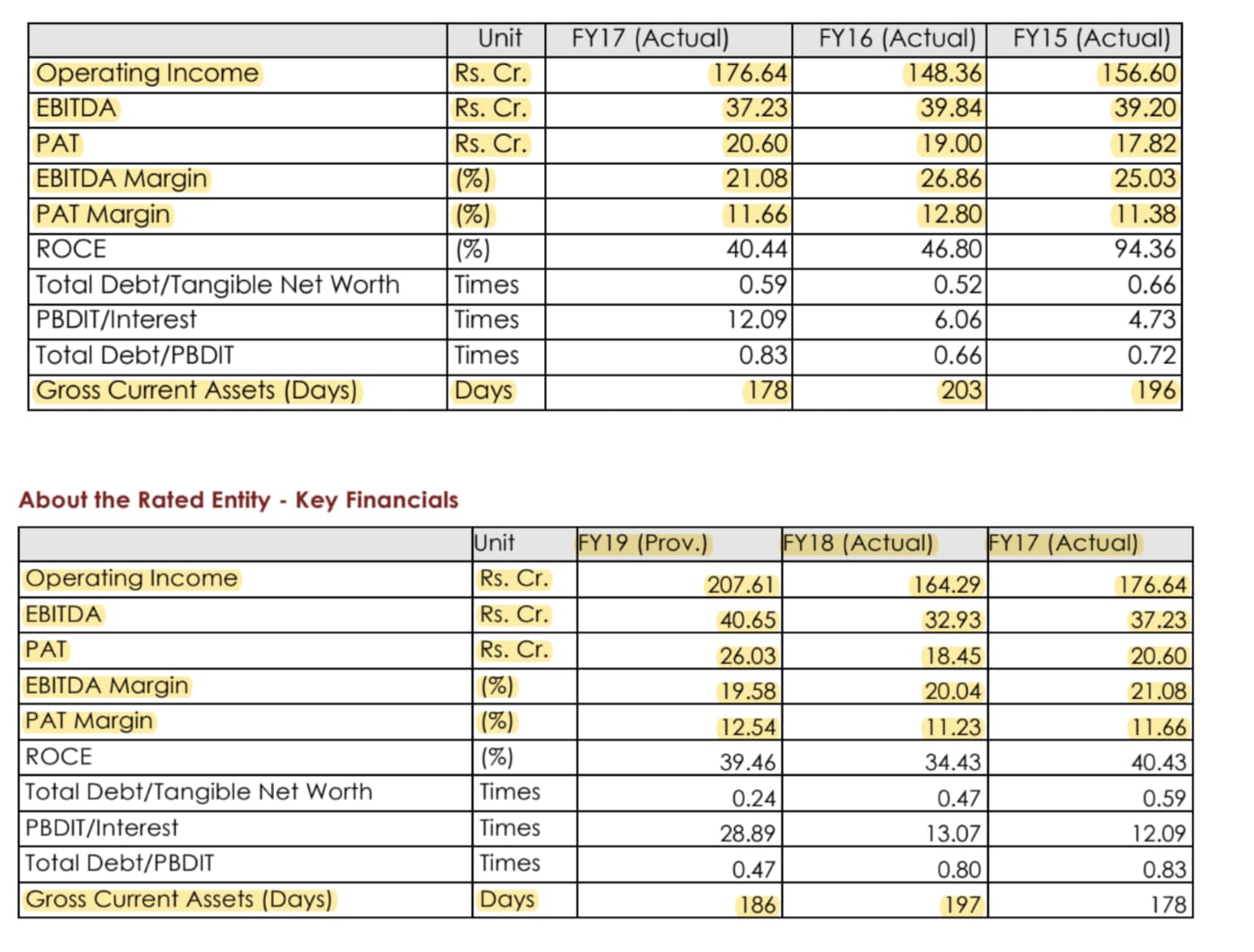

S Kant Healthcare

Eskay Speciality

Disclousure: Invested (position size here, bought shares in last-30 days)

What is your conclusion from above analyis of group cos business. Are you trying to say company might not focus much on listed business and launch more products in unlisted group cos - Any kind of overlapping products between listed Anuh Pharma and other unlisted cos?

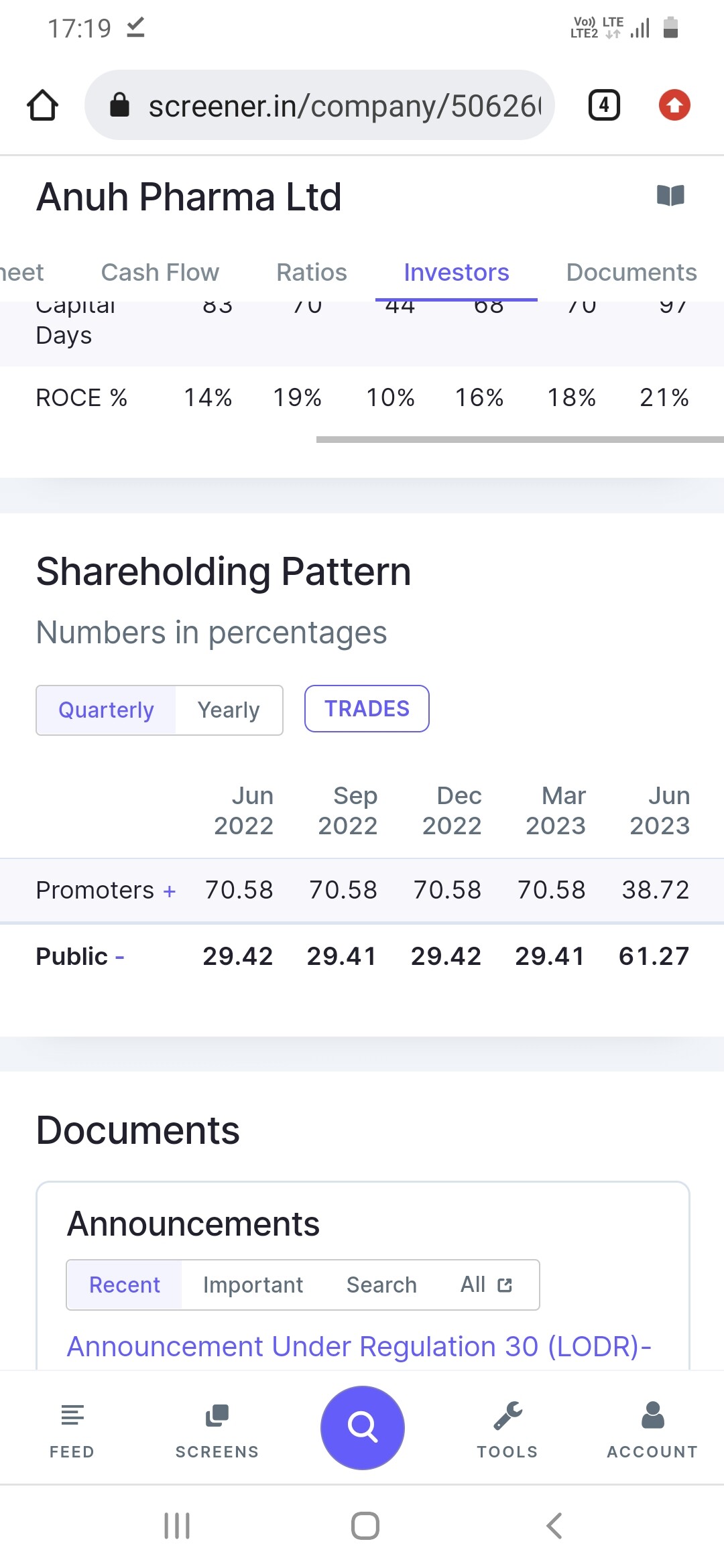

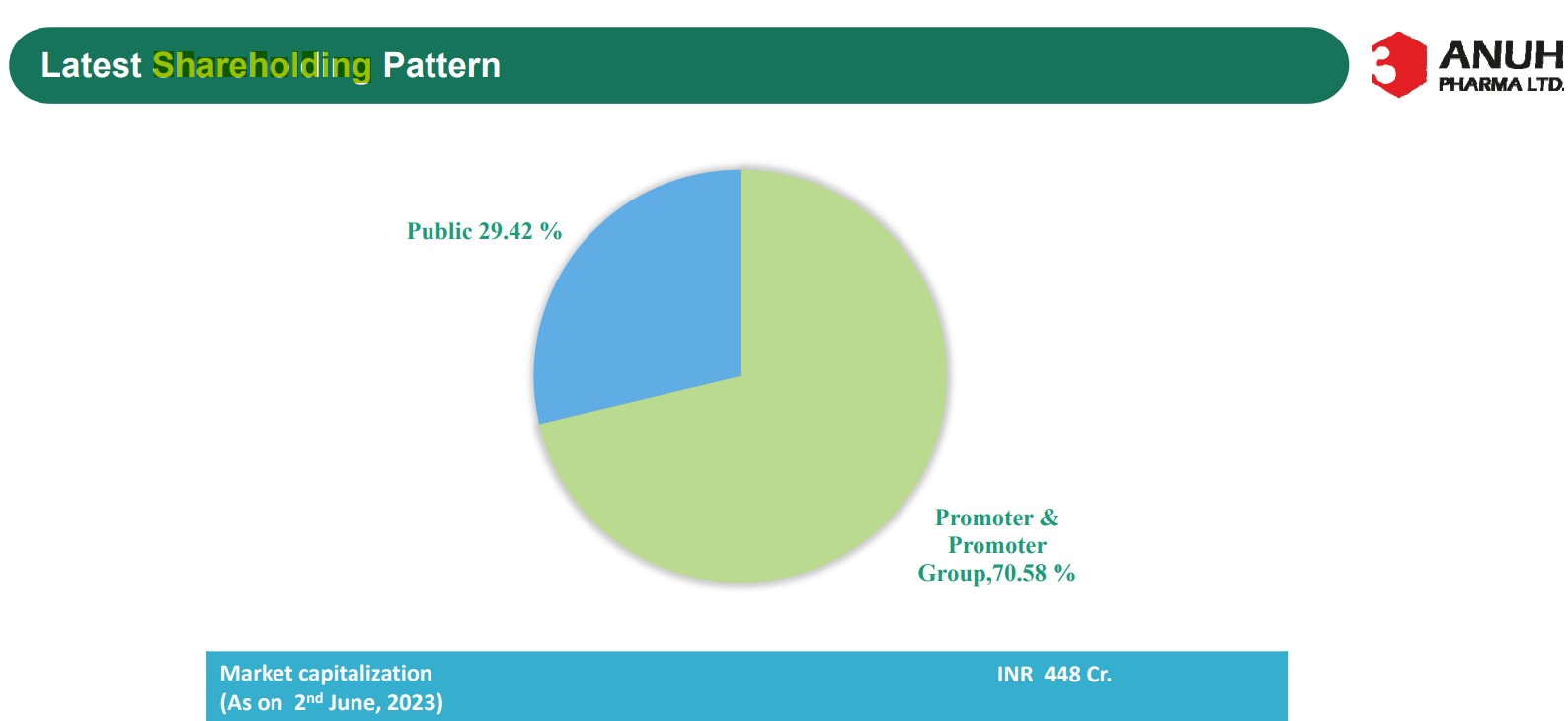

Appreciate that you are sharing your research on Anuh pharma! I was also looking into this company and it looks attractive, however while looking through Screeners i noticed that the promoter holding has changed dramatically in june quarter, from 70.58 it has come down to 38.72

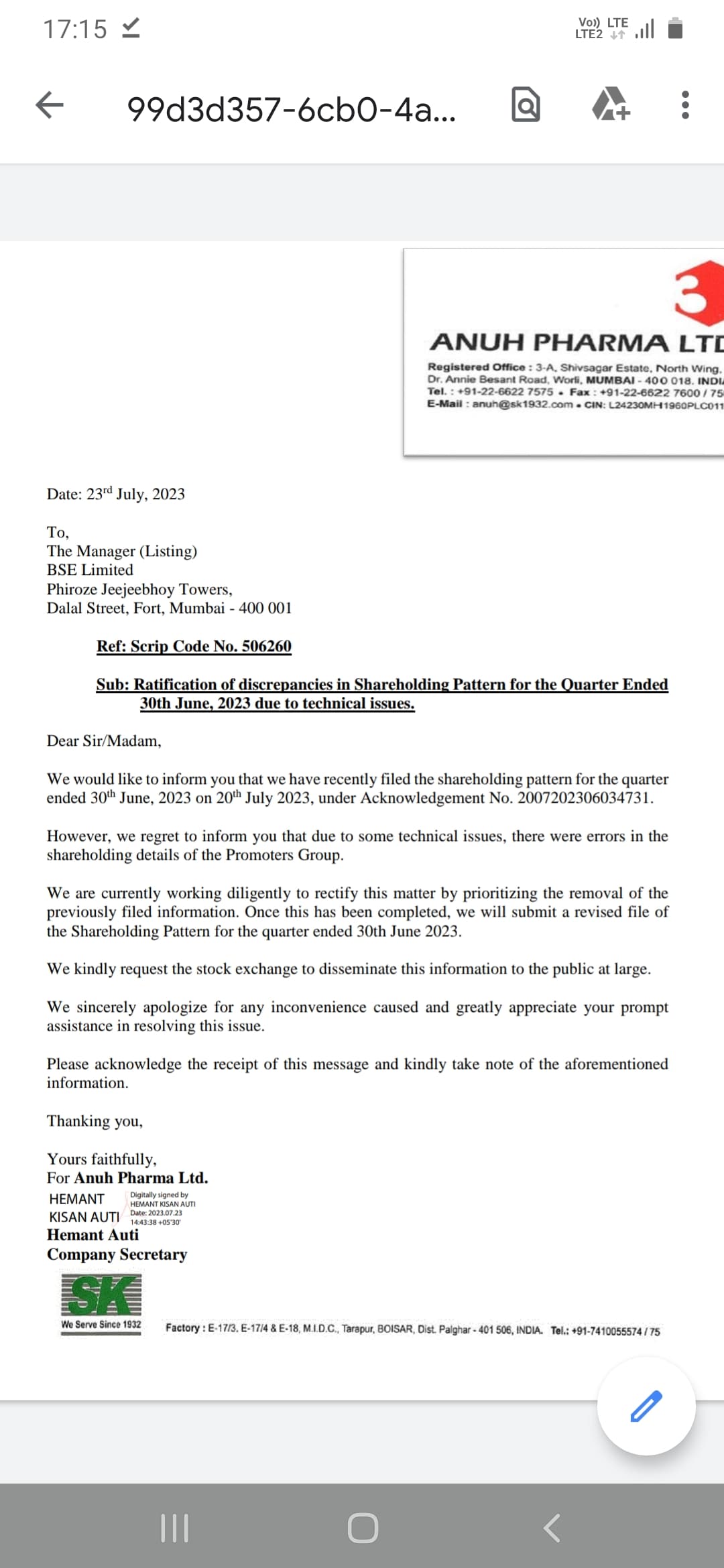

Good find. The reason is below as many wanted to reclassify from promoter to public. You can see the exchange information here.

Now one thing I wonder is how the share holder information as of March 23 reporting them as promoter and June they became public. Based on above exchange filing both Dec 22 and March 23 also should reflect the change.

Any thoughts @harsh.beria93 ?

4 names which are mentioned hardly owns any shares of the company…

few big names are not there in promoter caregory? I wonder what is the reason for that?

@harsh.beria93 or many other senior members can check and update

There can be 2 reasons

Either there is some error from bse side and it should be rectified in couple of days or

There is some reclassification of promoter group and few promoters may have been reclassified and shifted to public category…but such big quantities reclassified as non promoter i feel chances are rare

Anuh Pharma largely focuses on API, wherea other group companies are more focused on other segments (like Eskay Iodine on iodine intermediates, S Kant Healthcare on formulations, and Eskay Speciality on specialty chemicals).

63rd Annual General Meeting (AGM) of the members of Anuh Pharma Limited will be held on Friday, the 18th day of August, 2023, at 4:30 PM, Hall of Harmony, Nehru Centre, Dr. Annie Besant Road, Worli, Mumbai - 400018

If anyone is attending please post the updates here

I have started some high level analysis of the company once @harsh.beria93 started sharing the updates. But, I am still not feeling confidence with the management to scale the operation like they usually suggest in all forums.

Below are some of points which making me cautious to invest:

If anyone planning to invest in the company, please go through at least couple of con-calls to really know more about the management and style of working.

I still feel current valuation which company is trading may not have much steam till management able to meet walk the talk. Hoping management to have more con-calls so that MF houses start tracking this counters to really see value in this counter.

Happy Investing,

Karthik

Disclosure: Not having any exposure to this counter. Started tracking this due to Pharma upcycles and lower PE.

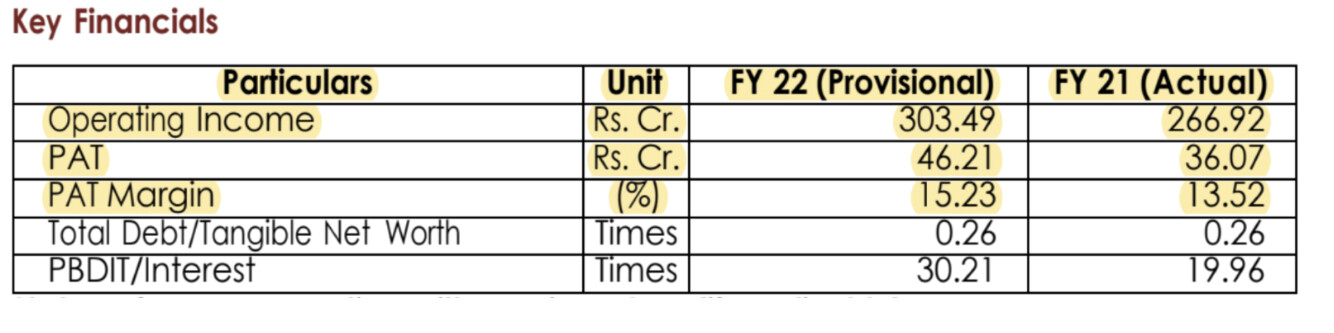

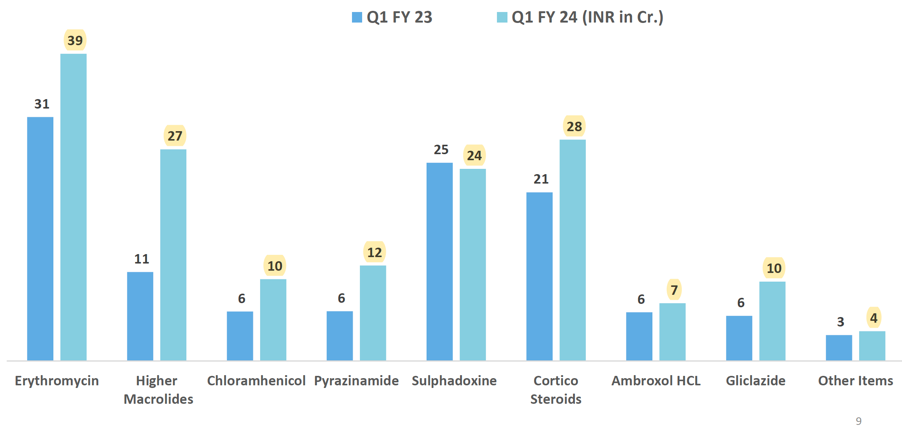

Company came out with a very good quarter, they have increased capacity and got new registrations in EU. I have highlighted key developments from their presentation.

FY24Q1

Disclosure: Invested (position size here, no transactions in last-30 days)