A smaller company, Urban Enviro Waste Management, is listed in the SME space in June…could use it as a peer to compare. It may not be an a-2-a comparison, but a rough reference nonetheless.

5 Likes

I had already analysed this one. Please refer to the earlier post.

2 Likes

In my Aug’22 post I was expecting the price to double in 4 years, price then was around 325. From that time there has been over 50% price appreciation to cmp of 500+.

Considering H1 results, and expecting the company to post similar performance in H2, there could be a 20%+ growth in profit from FY23 level. And assuming the PE level to be similar as now, that doubling of price from Aug’22 levels could be achieved by May’24 itself. But if there are negative surprises, like higher receivables, or write offs, or any technical issues wrt to WTE plant hampering its ramp up, or any other unpleasant development, the price will correct, and will follow the earnings trajectory.

Disc: invested, biased.

9 Likes

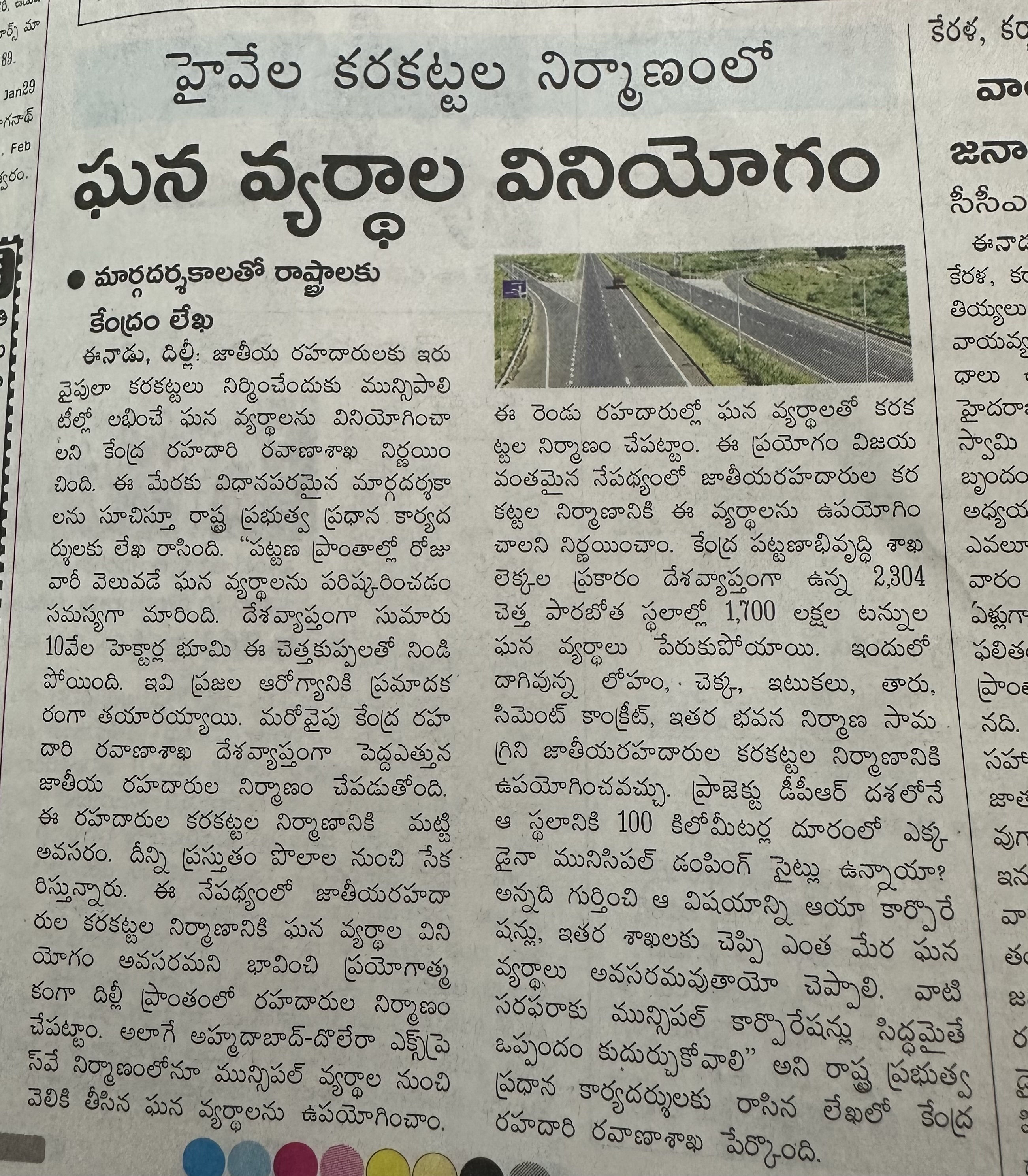

Centre paves way for using inert waste material in building highways

The company has a huge runway for growth. They mentioned in their concall that they will commence the C&D project and announce their vehicle scrappage facility at the end of this FY.

2 Likes

Please provide any link for this type of research report if possible.thank you

1 Like

What I like is that there is revenue visibility due to the long term nature of the contracts. But…due to the customer profile there is a risk of collections which could hit the earnings and cash flows.

4 Likes

there is an article published in media and it mentions that central has issued a guidelines to states in india for using municipal solid waste in the construction of highways;

3 Likes

Stocks had a breakout (Yesterday) from the above high of 532 made on 13 Nov 2023, Not let’s see if stock sustain above its support level of 473

2 Likes

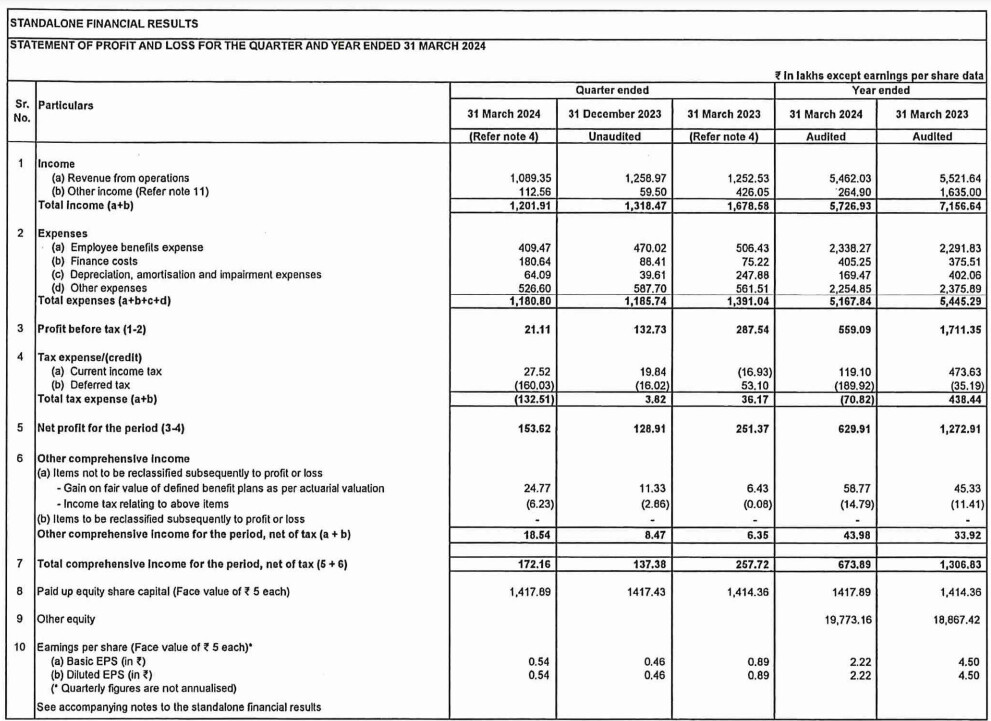

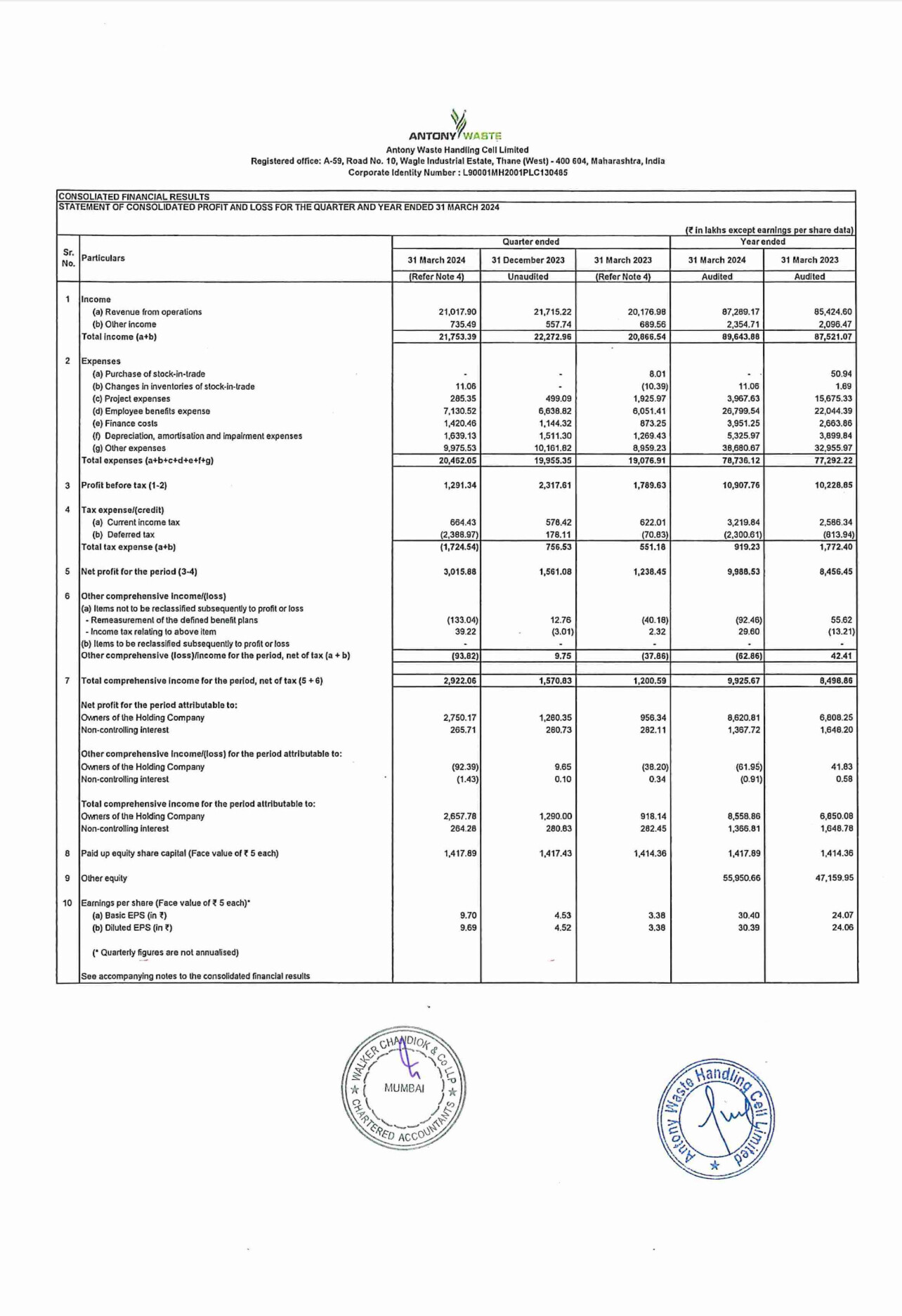

Any reason for such a big fall? Results were not that bad

I had made some errors in understanding Q2 numbers, one was not taking note of the revenues due to some escalations which were billed in Q2 for previous period, other was lower tax rate. This quarter the finance charges increased and also higher depreciation due to PCMC WTE project commissioning. There is a possibility of FY24 revenues being flat or slightly higher (approx. 5% growth v/s FY23). Net profit could be flat.

The mgmt is expecting a 22-24% revenue growth for FY25 (C&D revenues will come in FY25). A PE of 20 looks reasonable, not cheap, but not expensive either.

I am positive on the company as they are striving to diversify revenue from non-MSW business, C&D and vehicle scrappage. However, for me, the B2G nature remains a significant risk.

Disc: invested

9 Likes

Started reading about the company quite recently. Most of the revenues and project of the company are form municipalities means government. It is never a good idea to be in business with government as a lot of tender competitions, subsidies, corruption etc. comes to play. But will it play out in this case I’m not sure. I think the industry, company is set for exponential growth but my only problem is the one I mentioned. Can anyone who is tracking the co. and industry tell their insights and perspectives please?

8 Likes

The company is FCF negative… any comments on this? ROE is good at 15% but FCF negative makes me a bit apprehensive.

1 Like

During a period of higher capex, FCF will look negative, that is the case for most small cap companies. I think OCF to ebitda is a better metric suggesting whether the company is able to recover money from its day to day operations, and a 5 year average of 95-100% pre tax suggest a very good operating business

5 Likes

Anyone following this company, the results were posted yesterday and they don’t look that good. Sales is reducing quarter or quarter. Profit margins are also reducing. This year the performance dropped compared to last year.

Disclaimer: Invested.

3 Likes

Thank you for sharing

Nothing extraordinary, still a subpar operating performance compared to previous FY, compare the PBT.

Bottom-line gets beefed up by Deferred tax Assets, which is not a given in every quarter

5 Likes

Result looksling good just because of negative income tax

3 Likes

True. Can anybody help me with this? In their business update, they mentioned that their operating revenue grew by 14% this quarter, but according to the results, it’s barely 5%. Similarly, for the entire FY24, the business update claims a 17% growth in operating revenue, but the financial statements show it’s barely 2%.

4 Likes