Antony Waste Handling - It is the business of waste management

3 broad business areas : -

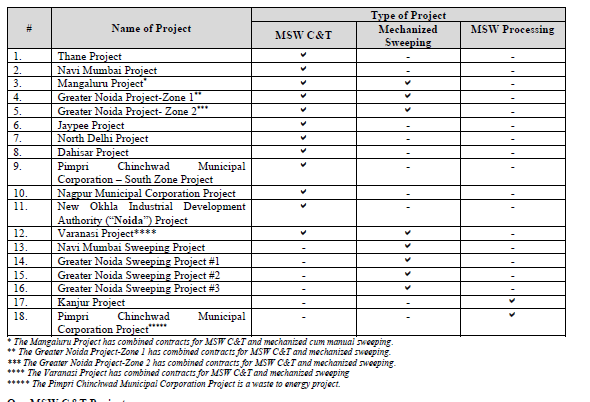

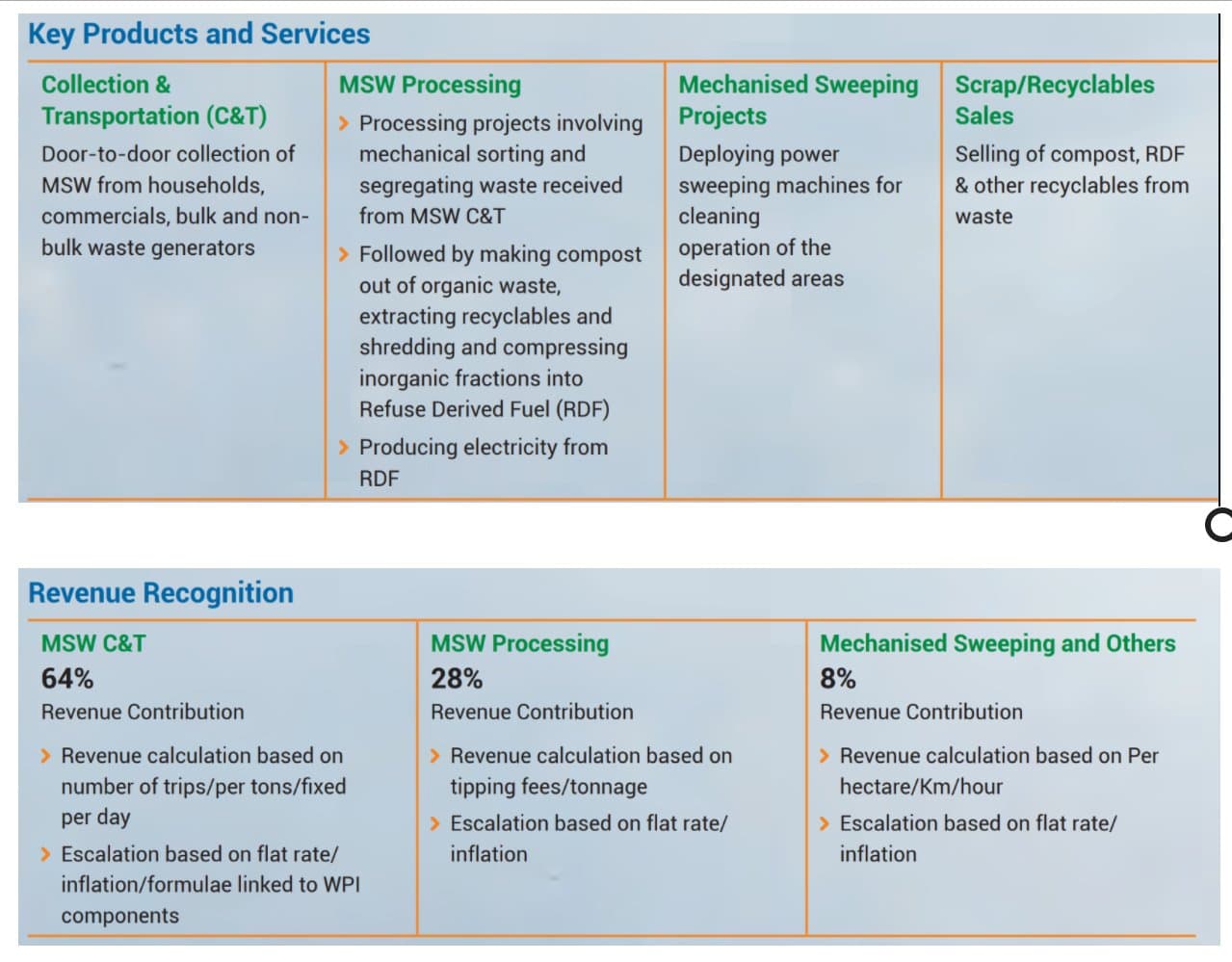

1. Municipal solid waste and collection process: These contracts are given by municipal authority and only have tenure of 7 to 10 years. The municipalities invite tenders for either the whole of the city or parts of the city. Currently we have 12 such ongoing projects in the service

2. MSW processing projects:

The work involves composting, recycling, shredding, and compressing of the waste into refuse derived

fuel, as required. Currently, we have two large ongoing projects. Normally tenure of

such processing contracts are longer, which is around 21 to 25 years. One of our

processing projects is located at Kanjurmarg, Mumbai, which has a concession period

till 2036 and the second one at Pimpri Chinchwad has a concession agreement till

2040

3. The third business is contract and other service:

which involves mechanized road

sweeping with the use of power sweeping machines, manpower, comprehensive

maintenance, consumables, safe disposal of waste, requirements of completion of the

cleaning operation of the designated area

We have four such ongoing projects with an average outstanding duration of accounts for at least seven years.

They have revenue insights for the next 7-10 years, with a price escalation clause depending on inflation index

Good amount of disclosures and decent insights from management of business metrics

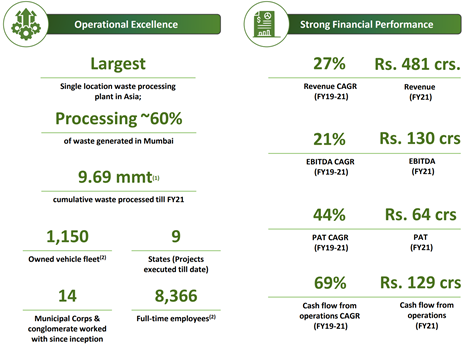

Market Size : Earning Transcript

"Now I will briefly share few highlights on the Indian MSW service industry. The industry

size is estimated to be Rupees 50 billion. Increasing population with higher urbanization

would lead to higher per capita waste generation in India. Urbanization coupled with

changing lifestyle patterns, increasing disposable incomes, have paved way for

consumerism and have also contributed to higher waste generation in urban India. Over last

few years along with Urbanization, we have also seen our industry leaning more towards

technological changes like mechanized primary waste collection & sweeping, GPS-enabled

vehicle and RFID-enabled bin tracking system etc. to bring in more efficiency and

transparency. This augurs well for a technology driven MSW service player like us.

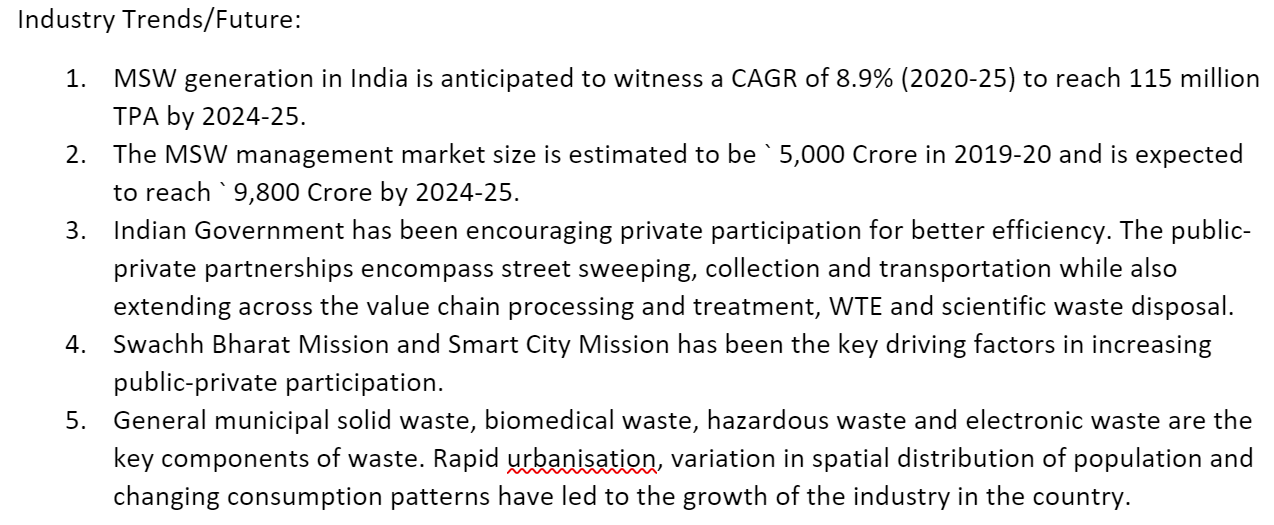

Various initiatives taken by our government like Swachh Bharat Mission, to keep India clean and focusing on hygiene has led to a multifold increase in the spending on solid waste management by various municipal corporations. This initiation has taken a new shape in this budget with an allocation of more than Rs. 1.4 lakh crores over a period of next 5 years towards Urban Swachh Bharat Mission 2.0. This is expected to drive the Indian MSW industry towards a more efficient Collection, Transportation and Processing of Solid Waste. MSW generation is expected to grow at a CAGR of ~9% from 2020 to 115 Million TPA by Fiscal 2025. The MSW Management market which is currently estimated at Rupees 5,000 crores in FY2020 and is expected to reach around Rupees 9,800 crores by FY2025 -a CAGR growth of 14.4%."

Management : Overall management appears to be transparent and giving good disclosures on the website

Risks -

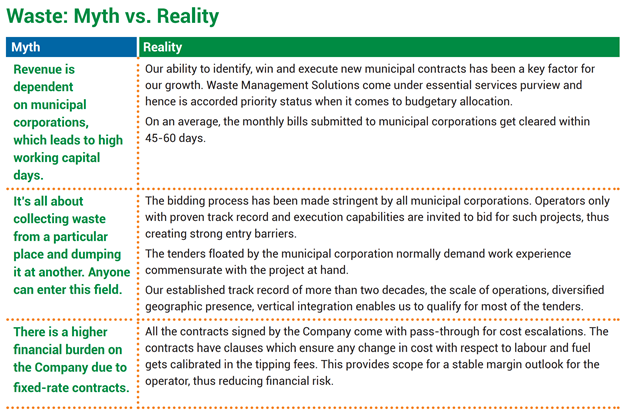

All the revenue is coming from Municipalities that means heavy dependence on government.

They did initial projects in Delhi, but haven’t been able to drive penetration in Delhi

At the moment, heavy subsidies from Government, but what happens when subsidy ends

Opportunities -

Waste generation is going to increase multi fold and Antony is one of major players in the market

Swach Bharat Abhiyan, there is line of sight in to continuous funding by the government

can drive penetration in to other markets and with smart cities coming in to picture waste management is going to be one of the key factors

Please share your thoughts

Disclosure : I am invested

In terms of business opportunity, India generates ~2 lac tons of waste per day of which only close to 50% is processed. So there is enough waste that still needs processing.

Waste generation is directly linked to wealth of any nation.

Apart from the 5000 crs of municipal solid waste (MSW) industry, there is another 2500 crs of industrial waste + medical waste + e-waste industry. Very rough estimates suggest doubling of both these industries over next 5 years.

Competition - Antony waste mentions many competitors in the RHP, but apart from Antony, Ramki and BVG, other players are either regional or very small. Essel (another name mentioned as a competitor) is under severe financial stress and the MC’s that they are serving are looking for alternatives.

Run way for growth - not only waste generation is increasing per day, but MC’s also need to clean the closed dump yards by using biomining landfilling. This is a huge opportunity and only large and existing players will get to play this game.

Specifics on Antony

C&T - Currently company has 12 such contracts. Varanasi project is still to show in no’s. Apart from that company has bidded for 6-7 new projects, and expect 1-2 project wins. These wins will ensure revenue continuity in the years to come.

Processing project -

A. Kanjurmarg project is operational for last 10 years and has another ~15 years of life. Plant is supposed to process 7500 TPD of waste at its peak. There is a glide path for company to reach to that level. Till FY19, they were processing 3000 TPD. In FY20, it increased to 5000 TPD and due to that we can see growth in processing income. Over next 2-3 years, they will reach to 7500 TPD of capacity.

B. PCMC project - This project entails an investment of 240 crs and is supposed to become operational by FY23. It is a 14 MW waste to energy project.

C. The bigger opportunity size - Mumbai has 3 dumping sites namely Devnar, Gorai and Mulund. Mulund and Gorai are closed for dumping. Devnar is the only site where waste is getting dumped without any processing. Mumbai generates 7500 WTD every day and of that ~70% is getting processed at Kanjurmarg. Plan is to move the entire processing to Kanjurmarg and then process the already dumped waste of Devnar. While I don’t have any details of this business opportunity, but Devnar is Asia’s oldest dumping site with waste mountains of 48-68 meters height.

Technology partner

When Antony was making bid for Kanjurmarg project, they didn’t had the technology and the experience of processing. So they partnered with Lara of Brazil. Lara gave the technology and Antony made the investments. Currently in this project, Antony holds 63% and rest is with Lara. As per the original contract, Antony’s stake in this project will increase to 73% without any consideration. As per my understanding, Kanjurmarg is the most profitable project for the company. So increased stake will reduce the profit not attributable to the company.

Due to the % equity increase, company’s stake in PCMC project will also increase. It is very difficult to predict the profitability of this project currently, but I believe it should be similar to that of Kanjurmarg project.

Accounting under INDAS

Due to INDAS, accounting is slightly tricky here. One can see 3 kind of assets in the balance sheet.

Tangible assets - My under understanding is that these are the vehicles owned and deployed by the company in C&T projects.

Intangible assets - This is capex incurred by the company for processing projects where no revenue assurance is there.

Service concession agreements - This is capex incurred by the company for processing projects where revenue assurance is there.

Unresolved issues

Project cost and revenue - There is project cost and project revenue (project cost + 10%) in the P&L. I don’t understand whether this is actually cash flow or just an entry required as per INDAS.

Long overdue receivables - Company has long overdues worth ~35 crs from a south India based MC. No visibility regarding the recovery of this amount.

Other income - There is a large interest income whereas corresponding bank balance is not there. So how this income is coming.

I believe company has a long runway for growth. Competition is limited. Apart from the B2G risk, there is no other major risk that I can foresee.

Clearing an existing dump site of the waste - https://www.bseindia.com/xml-data/corpfiling/AttachLive/1005f7cb-97b5-462b-8cc8-79c74916cdfb.pdf… 23.75 cr of annual order, 2 years period… Neither the amount nor the period is relevant… what is relevant is that this is first such project won by the company. There are dump sites which are closed now but over a period of time as the city limits have stretched, these sites are now near to city limits and due to that, commercial value of these plots have gone up. Only way to make these sites functional is to remove the garbage dump.

I had mentioned about Devnar which is Asia’s biggest dump yard and needs to be managed properly by going garbage management. This opportunity is worth thousands of crore.

AWHCL has formed a good base post IPO. 50EMA has been acting as a decent support. It has formed a cup and handle pattern and breakout will be above 375-380.

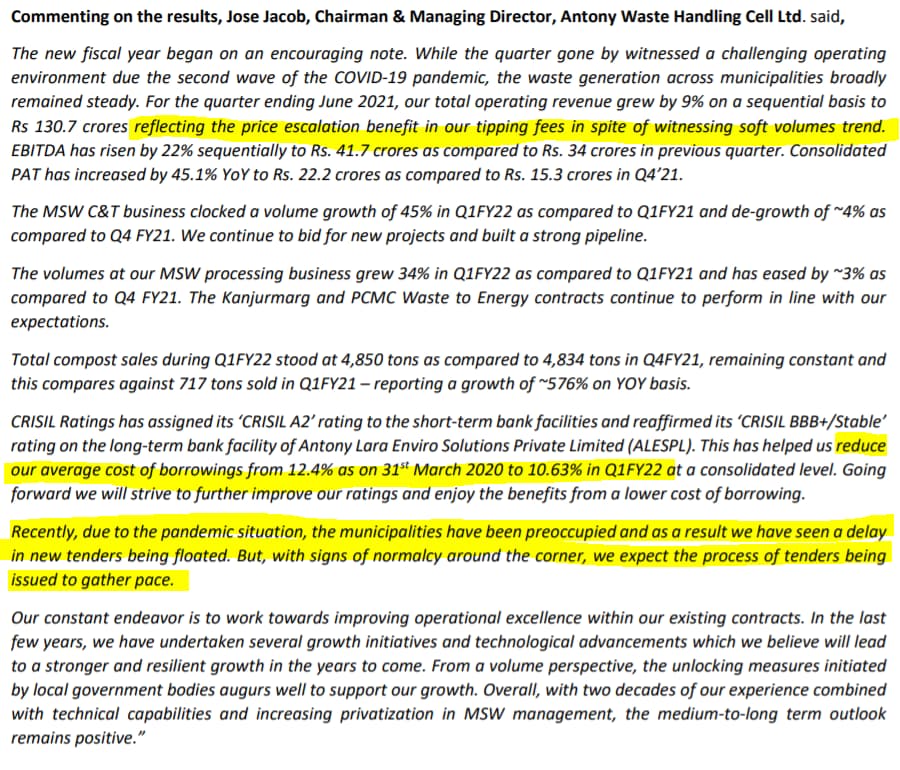

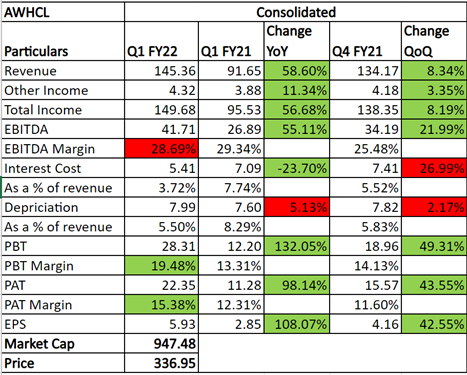

Operating revenue up 9% qoq.

C&T vol degrew 4%, but revenue up 15%. Benefit of price escalation and scale up of Varanasi project.

Processing vol degrew 3% and sales dipped 4%

Margins improved in this quarter at 27.9%. The range has been 28-30% historically. So there is room for improvement as tonnage goes up.

We could see some contract wins in coming quarters.

Q1FY22 Concall notes

Highest ever Q revenue, EBITDA, NP even in a challenging quarter of second wave

Softness on volumes on qoq. Witnessing recovery in vol.

Price escalation benefit accrued in Q1. 65% of projects saw price escalation in Q1. The remaining will be done in coming quarters. Fuel contributes 19% of costs. Now we make it a point that escalation should be monthly. If its quarterly/semi-annual/annual the corporation should take average of the period instead of end of period. This is to cover cases where fuel prices goes up in between and then comes down at end of period.

C&T- 13 ongoing projects. Continue to add projects and bidding pipeline

Processing- Kanjurmarg and PCMC ongoing. Qoq volume drop of 3%. Performing as per expectation. WTE project at PCMC is WIP, started in Mar21 and commissioning on or before Mar 2023.

Projects-

• Varanasi operational 60%. Employee cost has increased because of this and DA increase

• Bio-mining in Greater Noida. Commercial operation in mid Sept 2021. Bio-mining has 2-2.5 years contract. Kanjurmarg has given us big experience. We were the first to get such experience. Lot of bids coming up. We take a call based on our parameters. It takes 3-6 months for MC to go from design stage to award state. This year COVID disrupted the things incl financials. Margins are between C&T and Processing, more towards processing side.

• Mangalore contract Expiring Feb 22. It contributes 6% of the topline. Mangalore stands 1st in Karnataka in Swachh Bharat survey. Landfill is not in our scope and is not being handled well. We have managed C&T in a very good way

• Nagpur is fully operational since dec 2019.

• Thane running beyond end date. Contract extended by 4-5 months. Once COVID situation improves, contracts will come for renewal

Increased compost capacity and there is good demand

Total debt 145cr. Borrowing cost has come down after rating upgrade by 2 notches in single quarter. Looking at further improvement in cost of borrowing. Banks don’t look at waste handling, road repair etc as good models because there are delays in payments from customers. But our track record and balance sheet has given confidence to banks.

Municipalities prioritized payments to essential services and DSO reduced from 71 to 56 yoy. These are the best DSO days that company has seen. Historically it averages between 65-70 days and we build that in our systems. This will normalize to pre-COVID levels.

Having executed a complex project like Kanjurmarg, can we execute next such project without JV partner? We can execute without partner. Waste processing has different tech. Depending on requirements, we will have to evaluate

Any new tenders/ progress? In last 4 months we have seen a flow of contracts and have tendered for 6, of which 3 are C&T and 3 are for processing. Still in discussion. North Delhi is one of them- Landfill. C&T tender in Pune. Swach Bharat has brought awareness in Municipal top bosses. Every municipal corporation wants to perform. They want good players. We as a company are in a right spot.

Dividend policy will be finalized and approved soon.

On number of projects we were 2010=10, 2015=15, 2021=16. Why havent we grown fast on this? When can we hit say 30 number? In past, the kind of contracts were in very small sizes. Tambaram, Jaipur etc were small size contracts and tonnage was less than 100-150Tonnes. These have higher fixed costs and we were not in a sweet spot. Now we are looking at large cities, which are also financially better off. We are seeing large size and complexity tenders coming out. Now entire city, or half city are being given as contracts. So sizes have grown. There will be a gradual increase in projects.

In cases where we bid but dont win the contract, what are the top reasons? There is competition from 2-3 quality players. Our strike rate has been pretty good. We have a firm pricing discipline. We have high overhead costs of employees etc so there is not much space left.

When can we see margins hitting 30% that we saw in FY20, what would cause that…what is the ceiling that we can get to? Product mix- processing gives higher margins. So it depends on that. 60 C&T-40 Processing is normal mix. This is expected to be in this range.

Geographical presence- South we are in Mangalore. Chennai – another bidder has taken the contract. If quality tenders come up that are drafted by top 4-5 consultants, we bid for those.

Municipalities have different approaches- whether to have 1 vendor or 2 to handle the waste.

Yet to see waste processing contracts getting renewed. The contracts are long duration so not seen a full cycle

Increase in JV stake will be completed by Sept 2021

As already highlighted in the forum, waste management industry is still in the nascent stages and company has great scopes going forward. I especially liked the Jhansi project which the company won in May’21 where capex is fully funded by Jhansi Nagar Nigam.

The Jhansi project and Bio mining project are expected to start generate revenues from Oct '21. Varansi C& T project is also expected to start generating revenue in Q3.

With all these projects contributing along with price escalation benefits will be very positive for the company.

The one thing that Iam still not able to understand is the company’s WTE project with capacity of 14 MW in Pimpri - Chinchawad. The project entails an investment of 246 crores and is expected to be up in next 2 years. On a random google search it is seen that many WTE projects have met with widespread opposition from people living in vicinity. Do you perceive any such kind of risks for this project?

As per care ratings dating Feb23,2021 project risk associated with WTE project is one of the key rating weakness.

“Since the project is a new venture for the company in this segment with no prior experience along with limited track record and viability of WTE projects in India, the company is exposed to project risk with respect to timely execution of the same within envisaged cost and timelines”. ( care ratings).

From what I understand these are incinerators which burn the waste to produce steam from which electricity is produced.

Power will be purchased by PCMC on net metering basis at the rate of Rs.5/unit. Further,the company will also generate revenue through tipping fees at Rs.502/tonne for collection of waste in the project.

Details of company’s projects as on Nov,2020

Source: IPO propectus

Disc: Not invested. tracking. trying to understand the risks associated with the WTE project.

Biggest risk in this industry i see is the dealing with governments as that might delay revenue and increase receivables.

But as they suggest they do keep focus on municipal corporations with strong finances and also carry out a viability analysis before entering a project.

As i see it Waste management is one of the core responsibilities of the Local municpal corporations.

Delayed payments could result in disruption of services and being a monopoloistic model I think the possibility of payments being deffered indefintely is minimal.

Also the lack of orgnaised players to replicate the model of Antony in a quick time gives them significant leverage .

They also seem to have already tied down the wealthiest corporations in long term contracts which I think is the biggest moat in the business. This has given them a significant first mover advantage and the increased Budgetary allocations for Cleaner cities gives them a clear headroom for growth.

WTE projects can be of different types. One of them is anaerobic which probably involves lot of bad smell in nearby areas. The PCMC project is inceneration based so should not see any oppositions. Good links to refer.

Management has clearly mentioned that waste management was given a priority during COVID and hence funds were released early. Below is the snippet. Payments will always be an issue in this business model but my guess is that payments will eventually come. Do check out the current ongoing litigations.

Sterling & Wilson has won a WTE (waste to energy) plant of 19.6 MW @ INR 1500 crs, which converts into INR 76 crs per MW. If we compare this to Antony’s project in PCMC (Pune), WTE project, that is close to INR 16-17 crs per MW. So which one is more accurate?

Request subject matter expert to kindly help.

I guess we should consider per annum revenue potential, here Sterling may be referring to the total revenue potential. WTE may not be a 1 year project.

Antony’s PCMC is for ~21 years.

Or

Since the project is in UK/Europe, it may not be appropriate to compare it with Antony’s contract which is from municipality .

Industry folks who have been tracking this player closely can correct me.

I was going through the AR and found contingent liabilities to be around 90% of total equity. It has a line item ‘Estimated amount of contracts remaining to be executed on capital account and not provided for (net of advance)’ which is of 311 crs. Can someone please help me understand what does this pertain to?