Urban enviro prospectus is released. The IPO is over subscribed by 200x!

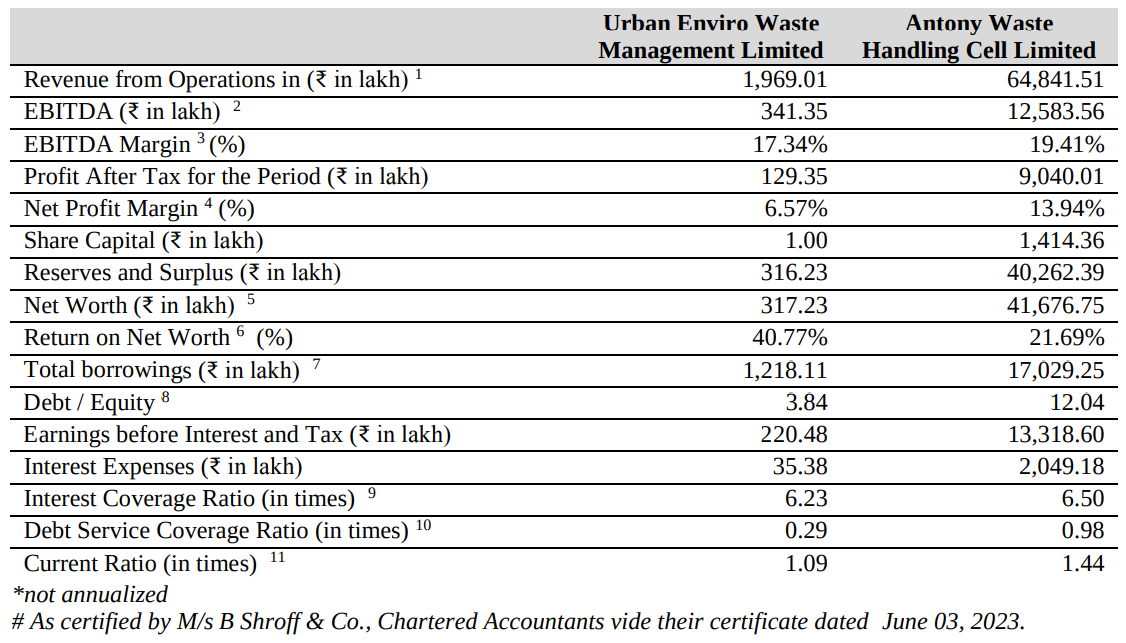

Did a cursory look at the numbers and compared with Antony’s (trendlyne). A few points (as on Dec 2022):

- Their receivables are quite high (473.32 L) which is higher than shareholder equity (423 L)

- Debt to equity is 2.86 (Antony Waste has 0.7)

- Current ratio: 1.05 (Antony 1.3)

- Interest coverage: 2.48 (Antony - 6.3)

- PE Ratio (at issue price of 100): 20+ (Antony - 10.5)

- EBITA margin: 18.75% (Antony - 19.62, note that historically it was 25-30)

They took on large debt in 2021-22. Haven’t dug through on what they deployed the proceeds into.

The prospectus also has a comparison with their peer - Antony. Am a bit confused on Debt to Equity computation on how it is 12x as against 0.7 in trendlyne and screener.in,

Looking at numbers, I see that AWHCL is a better valuation with only risk being the receivables (which is very likely same case in urban enviro). Not sure what else is being priced by the market.

Disc: Have tracking position. Might add more if nothing else holds against Antony.