Fair point! anyone who’s attending cc please ask about this disparity

2 Likes

The company has guided that they will grow at 20% over the next 2 years with ~22% operating margins.

My expectation is that the company will probably achieve the above guidance, but the PAT could be flat in FY25 due to higher tax.

The future revenue streams look interesting

- vehicle scaping+tyre recycling (almost a done deal)

- battery recycling (started work )

- rPET project with a major FMCG player

The last couple of days gave a good entry point.

The B2G nature of the business however is a big risk.

Disc: Invested

5 Likes

Financial Performance:

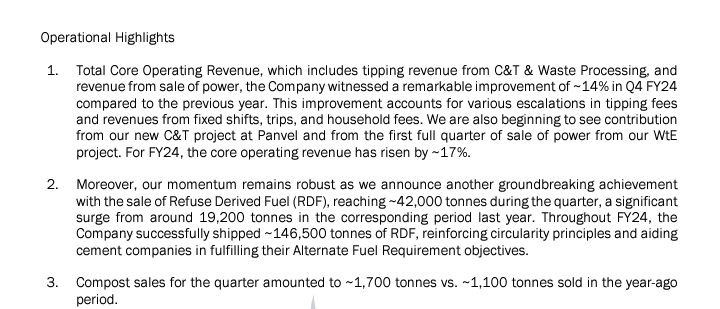

- Core operating revenue increased by 19% in FY '24.

- Total operating revenue excluding contract revenue stood at INR 829 crores, reflecting a 21% year-over-year growth.

- Core EBITDA amounted to INR 198 crores, showing a 29% year-over-year growth.

- Core EBITDA margin was 23%.

- Debt stood at INR 414.6 crores with a net debt of INR 343 crores.

- Weighted cost of debt for the group is around 8.5%.

Operational Performance:

- Managed 1.14 million tons of waste in the quarter, a 10% year-on-year increase.

- Successfully commissioned the 14 megawatts waste-to-energy plant in Pimpri-Chinchwad.

- Achieved a plant load factor of approximately 71% during the initial quarter of operation.

- Generated over 37 million green units of electricity.

- Record RDF sale of 1.47 lakh tons.

- Sold around 10,000 tons of compost during FY '24.

New Projects and Contracts:

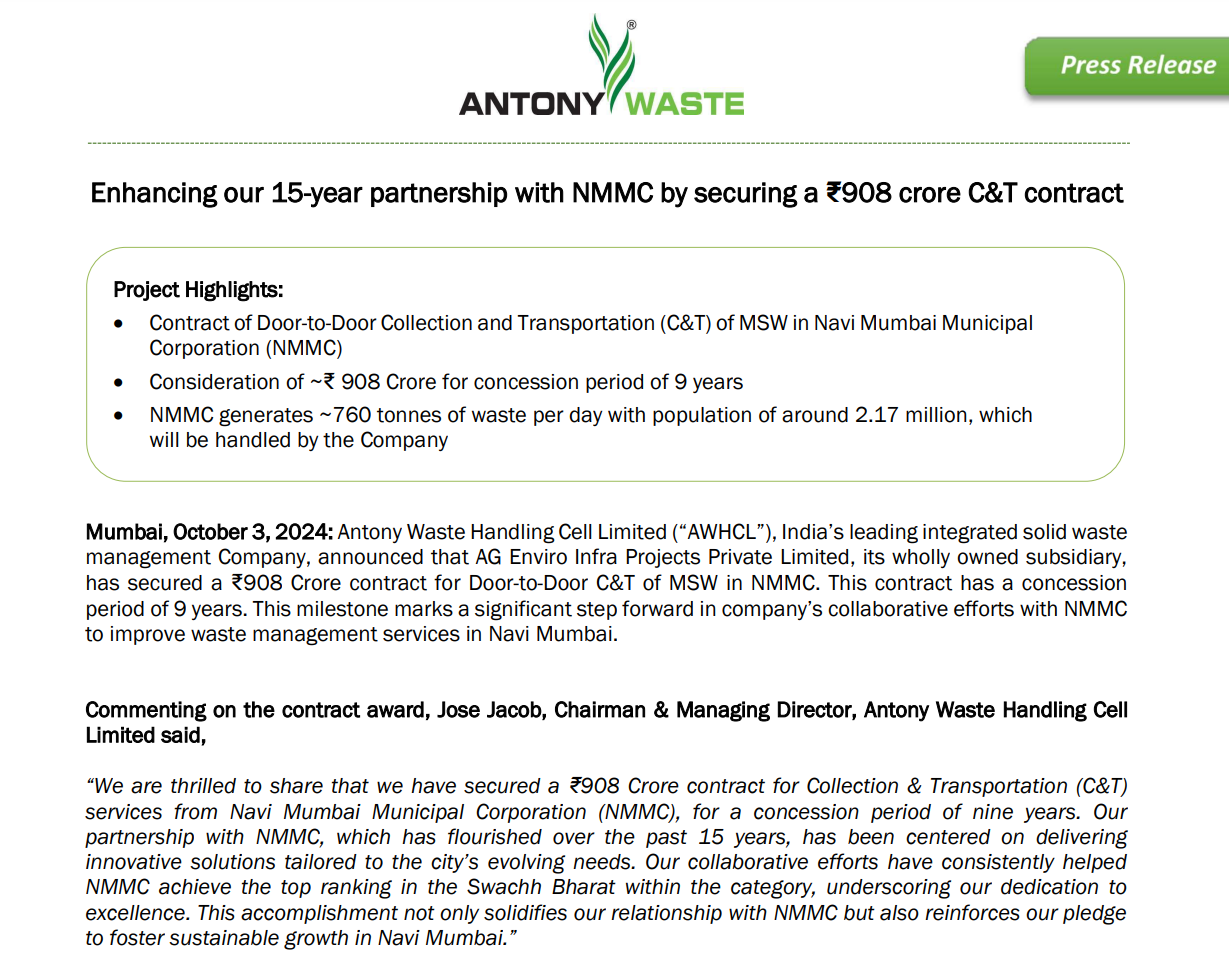

- Secured a contract worth approximately INR 386 crores for collection and transportation projects in Panvel Municipal Corporation.

- Secured a biomining contract in CIDCO valued at approximately INR 77 crores.

- Working on a vehicle scrapping business starting with cars and trucks.

- Exploring the possibility of entering the 2-wheeler vehicle scrapping segment.

- Planning capex for potential projects at the Kanjurmarg site.

Regulatory Environment:

- Following EPR norms for recycling PET bottles.

- Vehicle scrapping regulations mandate scrapping of vehicles after 10-15 years depending on fuel type.

- In discussions with BMC for potential capex at the Kanjurmarg site.

Future Outlook:

- Expecting a 20% CAGR in revenue over the next 2 years.

- Anticipating revenue growth from waste-to-energy projects, construction and debris processing, and new contracts.

- Margin guidance in the range of 22% to 24%.

- Focus on environmental sustainability and innovation for future growth.

12 Likes

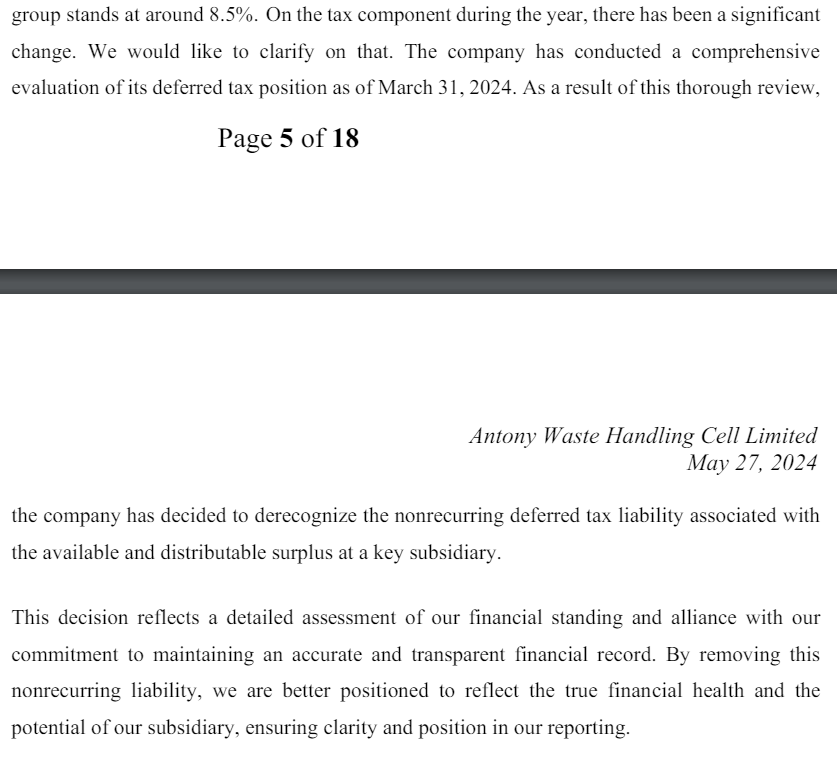

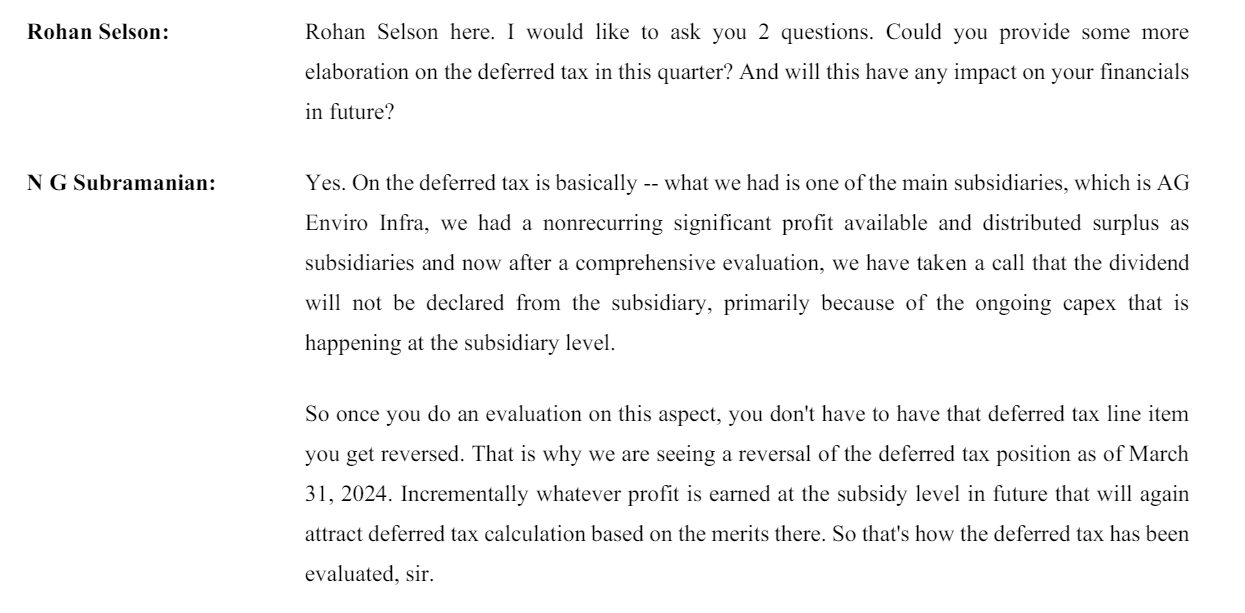

Likely Deducted from Deferred Tax Asset. Company had paid extra tax in the past, they’re deducting it now.

1 Like

Deferred tax liability in one of the subsidiary (AG Enviro Infra) was written off. This was also discussed in detail in concall.

2 Likes

This Company Manages Nearly 90% Of Mumbai’s Municipal Waste This Company Manages Nearly 90% Of Mumbai's Municipal Waste - Forbes India

7 Likes

The company has posted their Q1 business update. They are growing on all parameters. RDF and Compost sales seem to be the growth drivers. Clearly, the company is the most important player in waste processing. With increasing urbanisation and growing need for waste processing, they could continue to witness high growth

6 Likes

RDF and Compost cannot be growth drivers in my opinion. They form very small % of the total revenue, about 2% or thereabouts. We need to look out for the big movers like WTE plant, C&D, these have started contributing and these are large projects. Other revenue driver will be their vehicle recycling and tyre recycling projects. And any new revenue streams that they can add which is non-municipal, these will be value creators.

The stock has run in the recent past, though not very expensive, but moved ahead faster than earnings growth.

Disc: Invested

10 Likes

Results are not bad QoQ if you account for differed tax credit last quarter. PBT has doubled from 12.9Cr to 25.5Cr. Major hit YoY had been on EBITDA margins. There is significant deterioration there. There has been a significant run up recently. Need to wait for management commentary on margin contraction.

3 Likes

Since 9 qtr, they post same revenue ±10%

Since 13 qtr, they post same PAT, ±10%

Price movement bcz of PE re rating…and budget announcement

7 Likes

That’s because they have had same revenue stream at same capacity for some time. YoY sales have doubled in 3 years.

They have been adding new vertical and have been in capex mode for past couple of years. Future will be better. Though I agree on the PE re rating part. Disc: invested and bias.

3 Likes

OPM is declining qoq yoy…

1 Like

I understand the concerns of the people in the forum- I share many of them.

But here’s what I think:

-

Competition like Urban Enviro seem good. But AWHCL is many times bigger, and has major Metros for it’s business.

-

Waste management seems linear- more fixed assets, more revenue. This alongside fairly stable but mildly volatile margins makes it seem like a bad business. But the scope for revenue growth is tremendous. Goverment risk is always there in India so I don’t agree with the regulatory risk that people are excessively worried about. It is a service business, with better margins than retail stores and restaurants.

-

Does seem to be undergoing small capex- always a good sign.

-

I don’t think WM business is a commodity. There is no raw material or fluctuations in revenue. Fixed costs are there, yes but that makes it more like a safe utility . The actual payment form governments might take time to arrive, but with such monopolies at hand, AWHCL should be considered very safe.

-

There is some decent scope for scale economies. And as they manage more waste, their operations will become streamlined, more so than other upstarts.

-

And the main thing is that professional waste management is such a new but essential service in India. It will grow by a lot this coming decade— to not have it grow means the death of all major metros.

Have you seen our streets, the dusty roads, the garbage dumps be it in Bangalore or the gigantic Delhi Garbage mountain?

9 Likes

Diesel for C&T is one of their biggest expense. They also have a heavy book from all the vehicles.

There was a default of payments from Mangalore MC, I couldn’t find much reports except AWHCL sending them a notice.

Not exactly a monopoly, but large a contractor. There are smaller players, all aren’t listed.

Safe - pollution laws can be tricky and they are making major investments in the Kanjurmarg plant. That could lead to growth from biomining and power generation.

My biggest concern is being B2G and the related problems that come with it. They do have a contract with one FMCG for EPR though. More businesses could branch out to contribution to profitability.

Disclosure: Invested for the long term,

6 Likes

AG Enviro Infra Projects Private Limited, a wholly owned subsidiary of AWHCL wins Collection & Transportation project in Navi Mumbai for a period of 9 years. Total estimated contract value is 908 crores over period of 9 years.

6 Likes

Yeah, its nice that they again won the contract. But, I’m not sure if there will be any incremental revenue since it was an ongoing contract. Its more like a renewal.

9 Likes

This not weak it is normal quarter with no one off incomes unlike last year .

The average QTR EPS is 4.5 Growing at low single digit YOY …

Annual EPS at 18 Gr with low single digit utility company getting revenue from Municipal corp ( low grade Govt entity below PSU , central and state ) should trade at low single digit PE … < 180 Rs

4 Likes

Hi All,

I hold Antony Waste & I got a question after listening to the last concall. The current ROCE is 14% & the management says it’s not going to increase due to the capital intensity of the business. ROE is around 16% & the management stated that it will come down to 9% levels. Management is guiding for ~25% growth in the topline & said that the OPM will stay around 23% over the next 3-4 years. Debt levels as per my understanding of the past & their future guidance, management is consecutive & thus, debt should remain low to nill. In that case, can we model it like below over the next 2 years? Due to the return ratios either staying stable or coming down & the very high dependence on the small governments, the business may not be able to command higher valuations unless the revenue mix tilts more towards higher margin projects (waste processing, vehicle scrapping, waste to energy, etc).

Revenue after 2 years at 25% cagr comes to ~1450 Cr.

EBITDA at 23% margin, comes to ~330 Cr.

Interest + Dep ~110 Cr.

PBT ~220

PAT ~154

EPS (provided same share count) ~54

PE remaining between 15-25:

15 PE: ~770

20 PE: ~1080

25 PE: ~1350

So questions :

- Does it make sense to have such businesses where the probability of better profitability, return ratios over 5 years is low, in our core portfolio?

- CnT business seems a commodity & can face steep competition even from small regional players then does the management have the capability to venture into the new value added areas?

- It seems that even valuation of sub 20 levels is not cheap for these businesses, what should be a good margin of safety?

Please reply as much as you all can to enlighten all of us. ![]()

4 Likes