Haha, I don’t know if it’s a typo or intentionally trying to deceive investors by Urban Enviro.

As per the Explanation for the Key Performance Indicators in their prospectus, Debt to equity ratio is calculated by dividing the debt (i.e., borrowings (current and non-current) and current maturities of long-term-borrowings) by total equity (which includes issued capital and all other equity reserves)

That should come out as 0.4 in the case of Antony.

They have been meeting up with investors more lately.

…

11 April - Kanjurmarg project site

25 April - Kanjurmarg project site

25 May - Virtual one on one

12 June - Kanjurmarg project site

14 June - Kanjurmarg project site

19 June - Virtual one on one

Co is conducted an investor meet today; Pursuant to Regulation 30 (6) of the SEBI Listing Regulations, we wish to inform that the officials of

the Company will be attending the meeting with Investors/Analysts (Participants) at Kanjurmarg

project site on Thursday, June 22, 2023.

And it appears that they are able to impress the investors with business and subsequently investor has increased his stake.

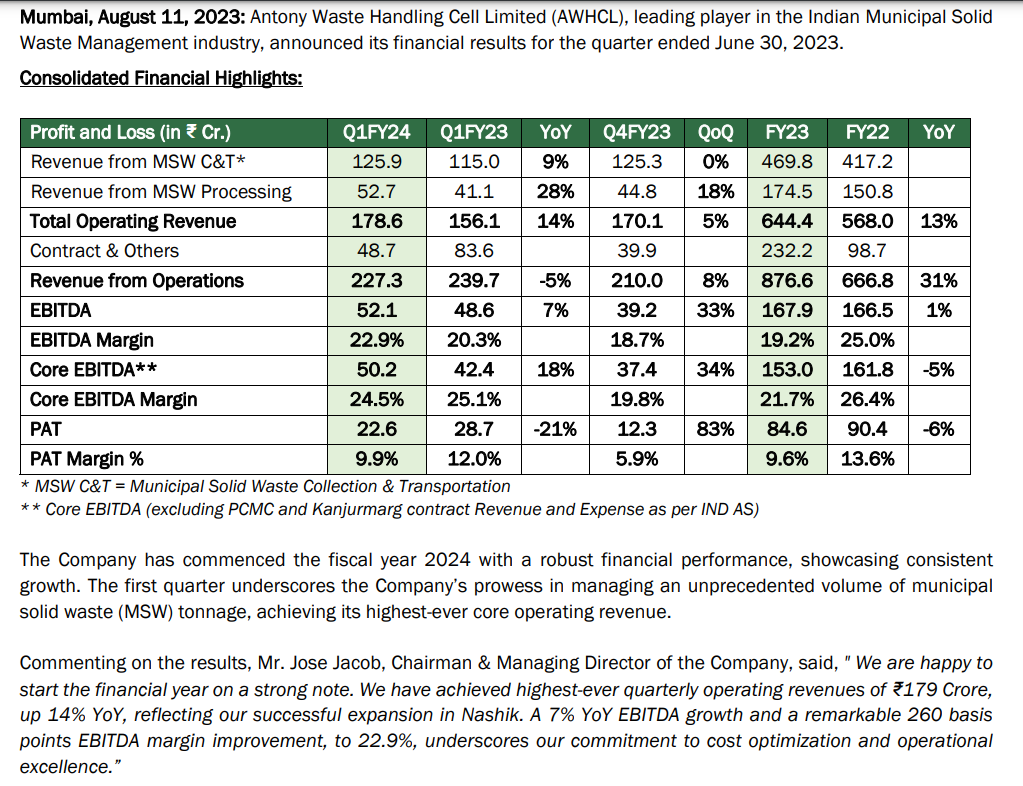

Record High Total MSW Handled: The total tonnage handled for Q1FY24 stood at ~1.20 million tonnes representing a remarkable growth of ~14% compared to the previous year. This success can be attributed to the full-scale implementation of operations at the recently acquired contracts, ramping up our existing Collection & Transportation (C&T) sites and the increased tonnage processed at the Waste Processing Operations. In the C&T business segment for Q1FY24, the Company effectively handled ~0.45 million tonnes, reflecting a growth of ~11% compared to the previous year. Additionally, the Waste Processing business expertly managed ~0.75 million tonnes, demonstrating a growth of ~16% compared to the previous year. It is important to note that the tonnage handled by the C&T business excludes projects that are billed based on fixed shifts, trips, or household counts.

Highest ever quarterly Core Operating Revenue: In terms of Total Core Operating Revenue, which includes tipping revenue from C&T, Waste Processing, and Mechanical Power Sweeping operations, the Company witnessed a significant improvement of ~15% in Q1FY24 compared to last year taking into account various escalations

on tipping fees and revenues from fixed shifts, trips, and household fees.

Record Breaking Sales of Refuse Derived Fuel (RDF): Furthermore, the quarter saw a remarkable achievement with record-breaking sales of Refuse Derived Fuel (RDF). The total RDF sales reached ~27,720 tonnes, a substantial increase compared to ~4,417 tonnes in the same period last year and ~19,226 tonnes in Q4’23.

From the last quarter conference call, I understood that although the sales in RDF are big, the EBIT level was not positive until last quarter. So mentioning the RDF record sales in the PPT would not contribute much to the EBIT or PAT. However, overall projections in waste handling are good, and a lot of recent developments in cards are expected to be launched sooner, and the investment from PE helps to understand the growth prospects. Overall, things are moving in the right direction, and if CO is able to complete pending receivables,it would be a very positive sign for all the investors.

The difference lies in the sector they are operating… while diagnostic services is something many can provide, the waste handling is very difficult work to manage and a tricky job … And somehow i feel they will find a way to fightback the systems to change and gain upperhand. The legal notice in manglore is the begining. The investment thesis itself is that the government systems are going to change because of forced transparency

Their Waste to energy plans are far bigger than Antony’s. They plant to start with plants around Mumbai first. Seems like they will start buying waste from AWHCL.

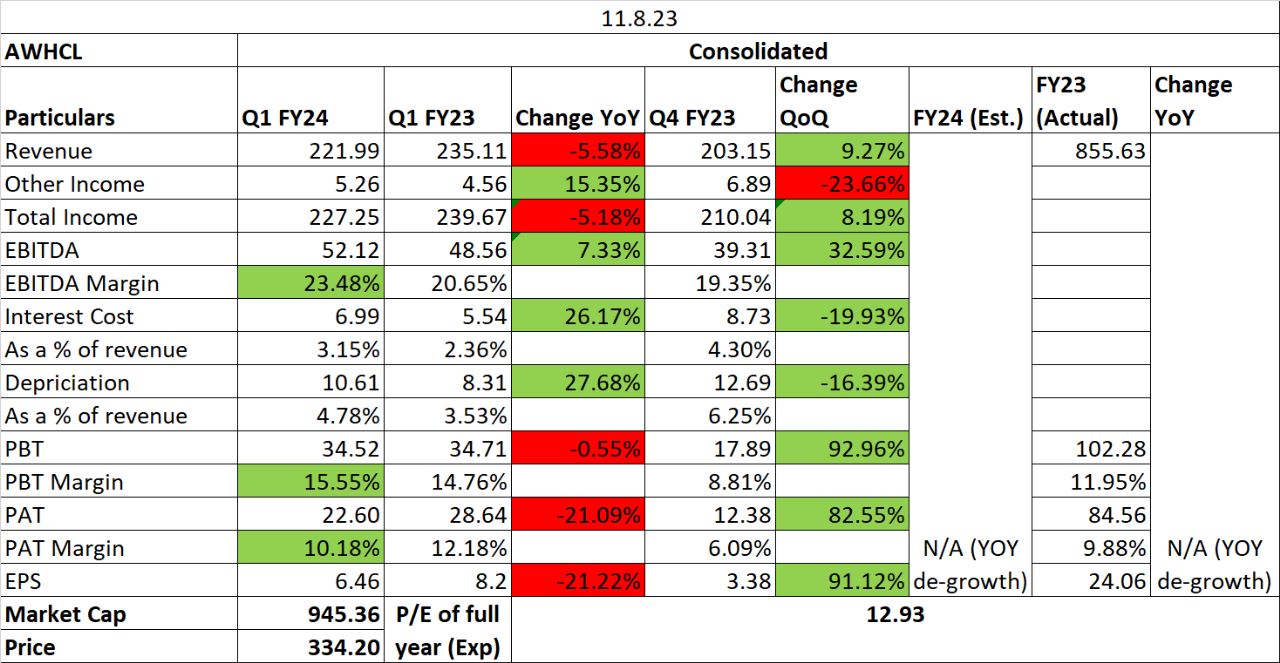

Results are good in comparison to the previous quarter, but Q1 is a slightly low volume quarter for the CO. Last year, it was good for the CO, as the escalations helped boost revenues. This time, without this escalation, the results are decent. For most of the other COs listed, Q2 is seasonally weak, but for Antony, Q2 is strong as increasing rainfall adds weight to solid waste overall, thus increasing tonnage costs.

Handled 1.2 million tons of waste in Q1 FY24, representing a 14% YoY increase.

Bid for a large C&T contract in North India and bio-mining tenders in South India, expecting positive outcomes.

Future Outlook: Revenue growth for FY24 is expected to be around 18% in core operations. Anticipates EBITDA margins of 23% to 25% going forward. Pimpri Chinchwad waste to energy plant will generate 65 cr revenues annually. Contract revenues are estimated to be around INR32 crores for the remaining three quarters of the year. Finance costs and depreciation expected to increase due to the waste-to-energy plant, starting from Q3 and Q4.

The concalls of this company are very detailed and the promoters always taking time to answer queries in a detailed manner. That shows a great amount of patience. In microcaps we need to bet on jockey.

In my view this can be a dark horse.

Although some negative are

B2G

Asset heavy

Declining margins.

Having a tracking position and watching it closely.

Can be a long term play till real growth comes in.

Management has capability to execute.