User collection model even in my Locality.

Added in maintenance bill.

Disc : not invested

Nikhil, date on the circular seems to be July 2022. How anyone can issue a letter using a later date? I am curious to know. Thanks,

Disc - invested

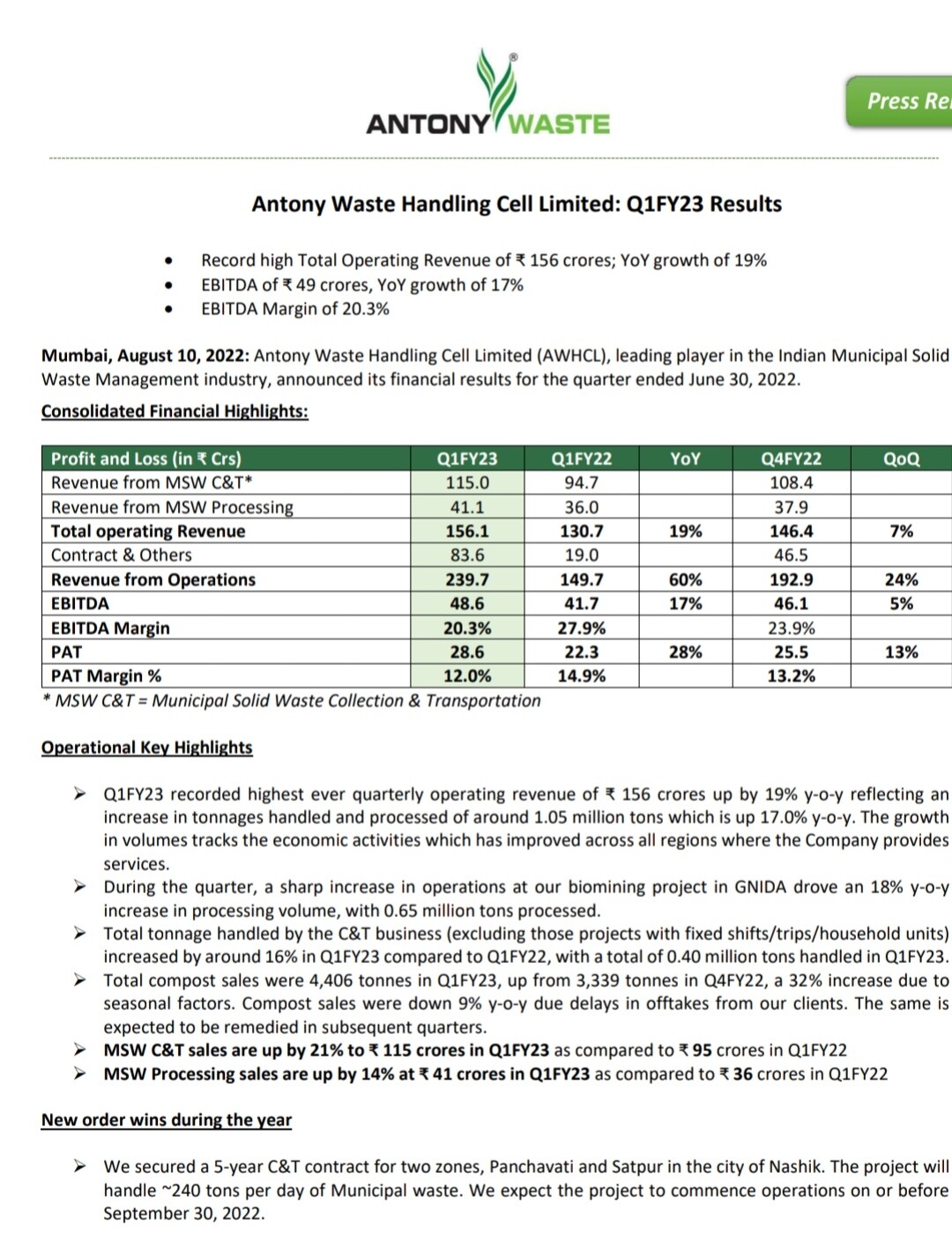

Result looks reasonable but again the trade recievables looks like a concern. Overall cashflow above 100 cr even with high provisions for tade recievables.

Any seniors can please have a look at the auditors remarks and give feed back please

Disl small tracking qty

Indeed. Out of the 91cr of profits, 47cr are stuck in receivables. Other interesting thing is 30cr spent on Project work. I wonder if its a new win or the WTE plant.

Hopefully more on this in the investor call.

Personally, I am not worried on the TR part since the management looks confident that Municipalities are focused on waste and the payments wont be delayed forever.

Disc - Invested

From the concall…

The company has ambitions to grow over 25% CAGR over the coming decade, and they are deliberating at the board level to enter other areas like bio waste, hazardous waste, waste water treatment, electronic waste, etc.

PCMC WTE project would operate at 60-65% PLF to start and in 4 months ramp up to 80-85% PLF.

New contract win in Nashik, https://archives.nseindia.com/corporate/AWHCL_27052022135728_AWHCLMaterialSubUpdateNashikProject.pdf

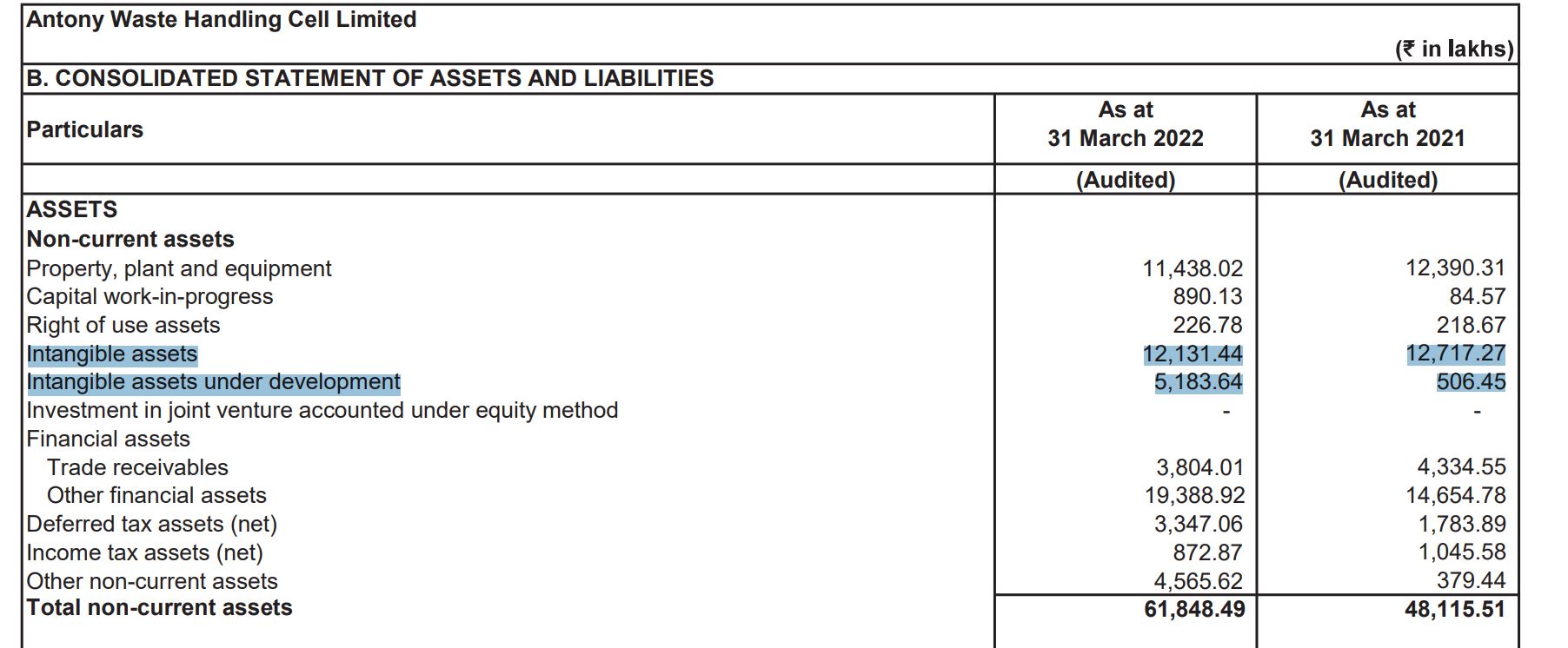

Did u notice in balance sheet under PPE purchase 110 cr but whereas no addition in fixed asset where it is gone

What is intangible assets 50 cr

Non curent trade recievables 38 cr apart from current trade recievables

Auditors comment

) Auditor’s Qualification on the Internal Financial Controls relating to above matters:

In our opinion, according to the information and explanations given to us and based on our audit, the following material weakness have been

identified in the operating effectiveness of the Holding

internal financial controls with reference to financial statements as at 31

March 2022

Matter II a. (i) (a) :The Holding

internal financial control system with respect to determination of expected credit losses on trade

receivables, were not operating effectively, which could lead to a potential material misstatement in the carrying amount of trade receivables,

recognition of loss allowances and its consequential impact on the earnings, reserves and related disclosures in the consolidated financial

statements

A material

is a deficiency, or a combination of deficiencies, in internal financial controls with reference to financial statements,

such that there is a reasonable possibility that a material misstatement of the Holding

annual financial statements will not be

prevented or detected on a timely basis.

We have considered the material weakness identified and reported above in determining the nature, timing, and extent of audit tests applied

in our audit of the consolidated financial statements of the Group as at and for the year ended 31 March 2022, and the material weakness

have affected our opinion on the consolidated financial statements of the Group and we have issued a qualified opinion on the consolidated

Anybody can please shed some light.

The simple meaning is Auditor is not believing in Management ability to collect receivables on time + also believes receivables are overstated as there are disputes over invoicing with their customers

The real issue is Management is not able to counter auditors by showing collection process ( SOP) or past collection track record . In such circumstance management should have taken partial provision of disputed receivables .

Though Business is doing fine and has lot of potential . For me this was NO GO …

Discl . Exited stock with Minor profits ( It is was small tracking position )

Trying to understand this sudden spurt under intangible assets. Anyone?

Discl : Exited my small stake today.

It could be detailed in the AR and it could be related to the vehicles for the New Delhi project. They did explain this capex in the concall, but I am not that clear TBH

The auditor qualification is there since 2013, so that means it’s an inherent risk in the business. Will have to understand the Intangible Assets part

Can we calculate how much of this year’s revenue was contributed due to the increase in fuel Prices?

Do you have data what kind of write off of receivables they had since 2013 as percentage of sales ?? This will help in deciding how much weight we need to give to both management confidence and auditors qualification …

ab3c3327-f004-4b70-aa98-d55bc15d45c2.pdf (695.1 KB)

Business update

as it is mentioned 26% up scale including revenues from MSW and C&T, MSW processing, the estimated projection could be 130.7 Cr + 26% ( 130.7 ) = 163.7 Cr.

130.7 Cr is the revenue share in Q1FY22 for MSW and C&T, MSW processing . And consider the remaining portion for contract and compost sales may fetch another 15 to 18 Cr. Total estimated would be 175 to 185Cr approx.

I feel, sequentially it will below to Q4 revenues but, however it is good to see that Q1 cycle posted a great set of numbers. Q1 for Anthony is cyclic in nature, as reason dry waste tonnage volumes are low compared to wet waste. Waiting to see Q2 run rate, and I’m sure we witness spike in tonnage volumes further.

I was mentally comparing Antony with Krsnaa Diagnostics today for the only reason that they both derive most of their revenues from B2G contracts, there is of course no other overlap in both the business. So when I look at both the companies, the market is valuing Krsnaa better than Antony even though Antony has better RoE and RoCE.

And another thought that stuck me was the recent events of Krsnaa wrt the income tax search. I saw some commentary hinting that you could not win business without “blessings and prasad”, so was wondering would that be true for Antony as well. And if yes, at some point in future the similar events could unfold in case of Antony too.

Thinking what to do.

Disclaimer: Invested

Antony had an income tax search last year.

Yeah, but that was due to one of their vendor evading GST and such. Antony directly had nothing to do with it.

What could be the risks to the revenue growth aspirations?