Market also does have the similar views, hence the cheap valuation…But as a long term investor i believe that none of the municipalities would ever like the citizen to suffer…If they delay/withhold the payments, none of the companies would come forward to accept the MSWM contract… Here downside is limited, growth potential is huge…

Stock is available cheap due to.working with government. Govt can delay payment making difficult for comapny. Govt generally is in financial trouble. It spends more than it earns.

Also expansion means good deal of capex. First you spend on plant and then staff and other things. After that you will get payment. Company has no pricing.power.

If there is dispute, payment.will be cut and in worse case contract will be terminated.

every business has its own merits and demerits. as long as debtor days within expected perimeter I believe there is no threat for payments, and as government is pushing more towards swatch bharath, digital India and with this initiatives in mind, it is fair assumption to accept that company would receive on time payments. In a country like India, we should definitely agree that garbage is mandatory collection and never hold for a reason, and runs 24*7, and government does holds on it shoulders, in a broader way it plays the pollical dynamics.

Isn’t their revenue stream diversified with multiple municipal contracts? Also would the switching costs be high for a municipality if the existing WMC is doing a decent job?

Under swachh bharat mission 2.0, specific emphasis is on MSW. I believe some kind of dictate from the central govt will push all large MCs to go for privatization of C&T and processing on a fast track basis.

(Note: Fairly new investor without much accounting background. So please correct me if I made any mistake. Thank you)

Despite asking for dividend payout information in 3 con calls, the company has repeatedly said that it is considering it without giving any additional info.

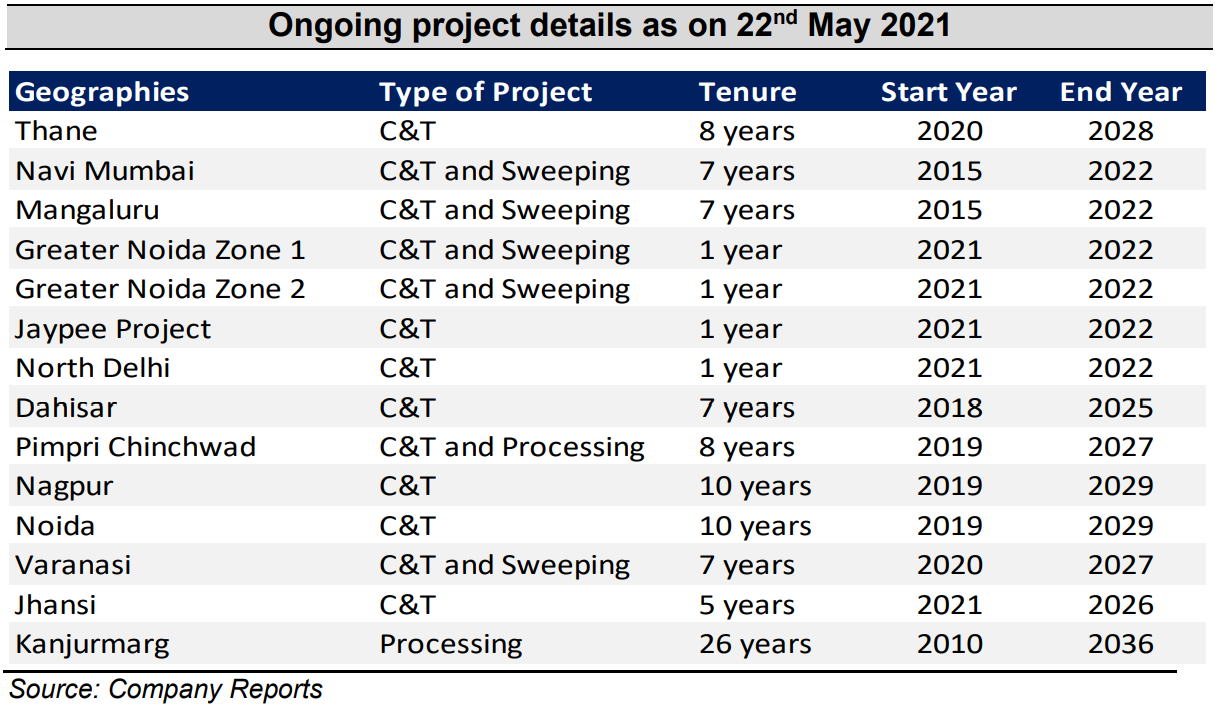

According to the company(mentioned in a concall), bidding typically starts after the allocation of the budget. Since 6 projects will complete their tenure this year, it will be interesting to see if the company wins these bids again. Since the company is aiming to only bid in areas with waste more than 200 TPD, most of the locations will qualify, where tenure will finish, the company is expected to win.

With respect to fuel pricing, the company stated that they and other bidders are asking for municipalities to make sure that they price it on monthly basis. So at least this problem will not be present in future projects.

Watched a couple of videos on Waste management in the US (like this How Trash Makes Money In The U.S. - YouTube), this made me realise the potential in the Indian market and the major point that was said repeatedly was “If done correctly then it is a successful business”. So when the company was asked about the tech uses technological solutions, they stated that they have been using modern tech solutions used in the US (composting unit) and Europe(RFID Tags). Based on this and other statements, it is sufficient to say that the company will do whatever it can to reduce the expenses.

Disc: Not invested (waiting for final assessment by Income Tax Dept on the raid conducted to make final decision)

It looks like a great opportunity, industry has tailwinds, growth looks good, company is taking smart decisions in mitigating risk of defaults choosing rich municipalties (which is the only biggest risk in this sector). Management looks competitive having enormous experience in the sector (looked at some of their videos floating on youtube).

The only problem I see is most of the players in this space are not publicly listed. This leaves me in the dark to compare Antony’s financials with other players(to compare operational excellence). Although plainly looking at the financials, margins looks fairly good.

Disc… Not invested, but tracking with interest (might be biased).

I think the company mentioned in last concall that most of the projects expiring this year have been further extended for another year or two. They say this usually happens with Municipalities since the new tender rollout is not expedited and it’s a challenge for them to change the waste handler.

I don’t think the IT raid was a big deal to be very honest. But this is a very subjective opinion.

I am a fairly new and young individual making small steps into investing. I am trying to investigate this company and am failing to understand the reasons for this stock to be trading at such low valuations.

Hope that I do not come across as someone who did not do my research.

Here are my thoughts:

The company deals only with municipalities (which is as good as the government that will never default) and most of them are 5-7 year contracts(long term visibility), maintaining an OPM of ~25%, growing at 20-25% YOY and the major factors that could impact their margins are the labor costs and the fuel prices but they mentioned in their concalls that they can appeal to the municipalities for most of the contracts (though the payout would be delayed). Considering the scope of penetration potential, more and more cities privatizing their waste management and the government’s initiatives, all the trends suggest that there would be only a pull up in this market.

I agree that there are a few private players that AWHCL is competing with that are doing well but am I missing any key risks that are involved that the valuations are so low? Are there any other trends that could disrupt this trend of privatizing waste management?

The reason why companies dealing with Govt trade at low valuation are

Corruption & low bargaining power

Once one municipal corporation blacklist you for some vague reason … ability to get business from other Govt entities is very difficult

Receivables - It takes a long time to receive money and on top of it often suppliers have write off some amount in most orders … so often Real profitability of an order is known a much later stage

Antony needs to diversify its customer base to get in more corporates so that he can sustain business in long run to get higher multiple .

That said … if they manage their show well … you may not have much downside from current level .

Yes, Ramky Enviro is much bigger than Antony, Ramky is also into many other areas like industrial waste, bio/medical waste, construction & demolition waste, etc. in addition to municipal solid waste. their ARs for the the past few years is available on their website, https://ramkyenviroengineers.com/investor/

Regarding the PCMC WTE project, assuming 65% PLF (11.5MW peak capacity), and tariff of Rs. 5 per unit, I expect the power generation to fetch topline of INR 32-34Cr. per annum.

However, we dont have many successful WTE projects in the country, and I consider this project somewhat risky.

In your calculation kindly include tipping fee also which will continue even post commissioning of WTE. Rough estimate is revenue of ~60-65 crs per annum from FY24.

WTE is the only way forward. It is impossible to have projects like Kanjurmarg since the land requirement is very high. More so, waste is India is very concentrate in terms of organic waste, all thanks to rag pickers. And this organic waste is good for burning post basic screening.

What we need are some tough measures from the central govt for waste mgmt… Like in SBM1, focus was on collections, SBM 2 is expected to provide fillip to processing.

Yes, other revenue will be the tipping fee…Rs. 500 per ton times 1000 tons per day, so about Rs. 18Cr per annum…my estimate of total revenue for the project is 50cr (18Cr+32Cr). This could be conservative. There could be some escalations (for fuel or manpower) in the future years, but that will add only to the handling/processing scope, dont expect any change in the revenue for power generation, this will be based purely on how much higher PLF the WTE plant is able to achieve.

The MSW in India is high in moisture content because of lack of segregation at source…which is not good for WTE projects.

For Antony, what I am curious to know is what areas will they venture into…in addition to the C&T and MSW processing, for additional revenue streams.