I believe company is standing at a very interesting point due to 2 reasons:

In next 8 months, PCMC project will become operational. Once that WTE plant is operational, Antony will get into an exclusive league. Their credentials will be at par with only few other players in India. Their willingness to have such similar projects will also move up.

This new COO, Mr. Mahendra, is very interesting. His credentials are impressive. Whether he will propel growth in the MSW processing, or will help company get into other waste processing needs to be seen.

I would be happy if instead of making 25% revenue growth, they focus on high engineering projects like processing.

So we need to wait to see how the plant operates in first couple of years, while the mgmt has said that they will reach the peak performance within first year of operations, we need to take that (optimistic) guidance with a pinch of salt. Only then we will know if this project will be value accretive or destructive.

On the other point, I also have been curious to know how the company will diversify. The company had mentioned once in the past that the board is looking at multiple areas, the construction debris management is probably the first of such steps.

Ketan, while waste mgmt. has no easy answers, I don’t know whether WTE is the real solution or not. But I can tell you that I visited the Kanjurmarg facility of Antony and it is quite surprising the kind of work they are doing.

The problem that company cites many a times for not having similar facility in other large waste generating cities is the lack of large land parcels which the municipal authorities need to provide.

Segregation at home has to start, by force or by choice.

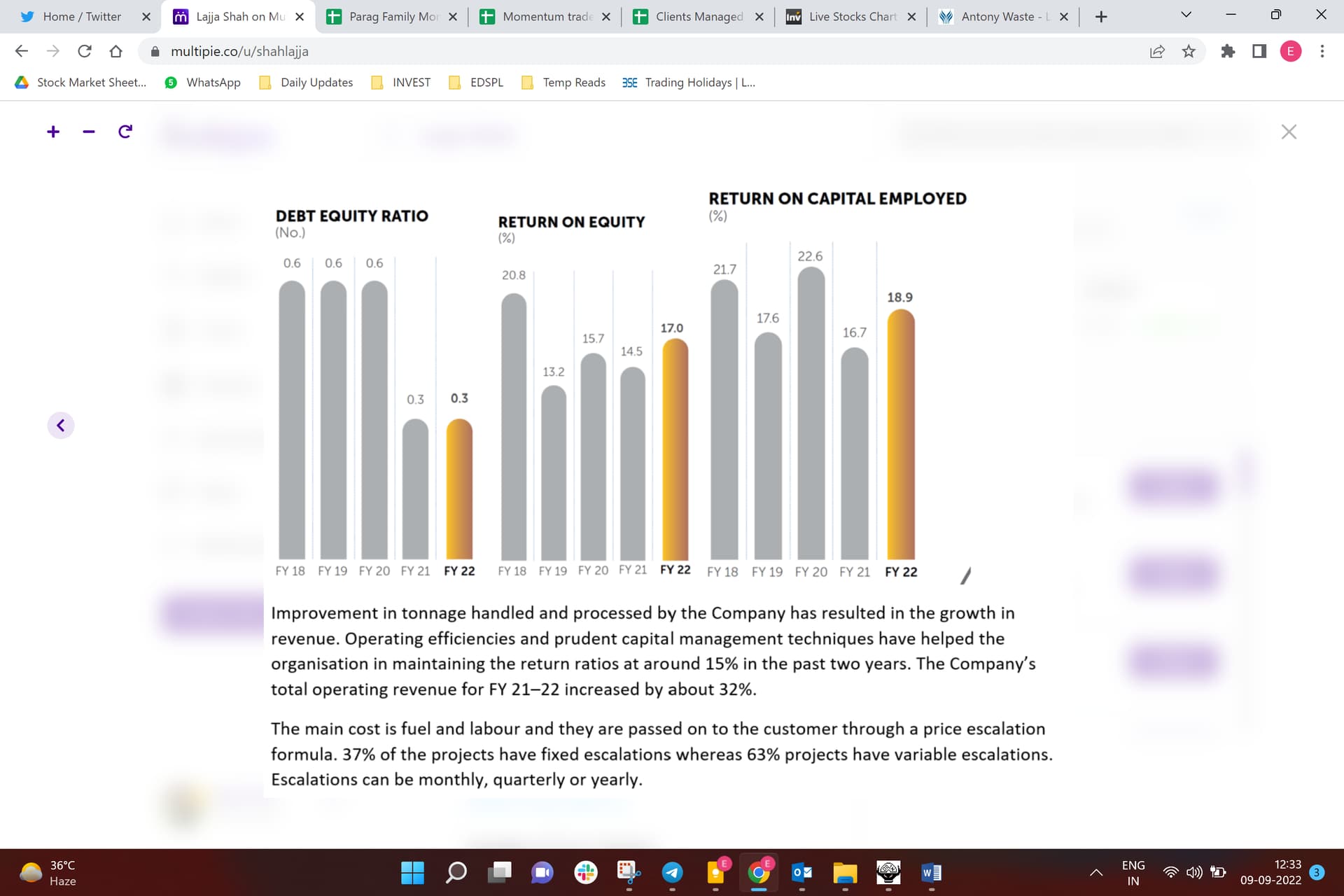

Honestly, I dont know if 12 is the right PE…I just assumed it for estimating purpose. However, for a company having returns (RoE/ROCE) comparable to Anotny, I’d expect higher PE.

I think TRs, IT raid and Waste Management sector is a factor for 12 P/E. Also that this is a B2G primarily isnt an attractive proposition.

But I have always liked what Jose said during the IPO interview. Municipal waste is an area that cant be deferred. Cities are competing to win the Swachta survekshan every year. The focus on this will only increase going forward

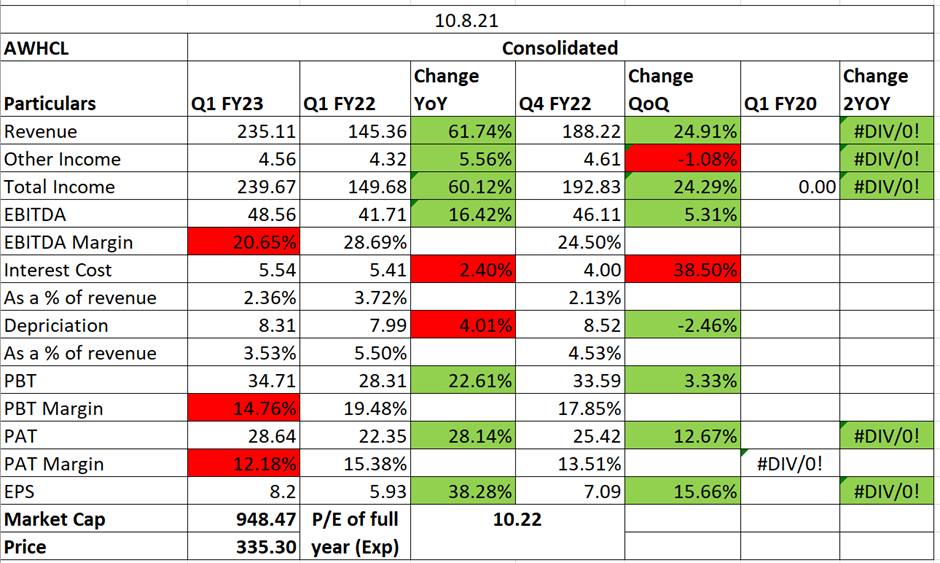

AWHCL Q1 FY23 Result Update!!!

Looking at margin expansion and increase in business verticals. Instead of just being a municipal waste management entity, also looking to go into Vehicle Scrappage and Construction Debris Processing.

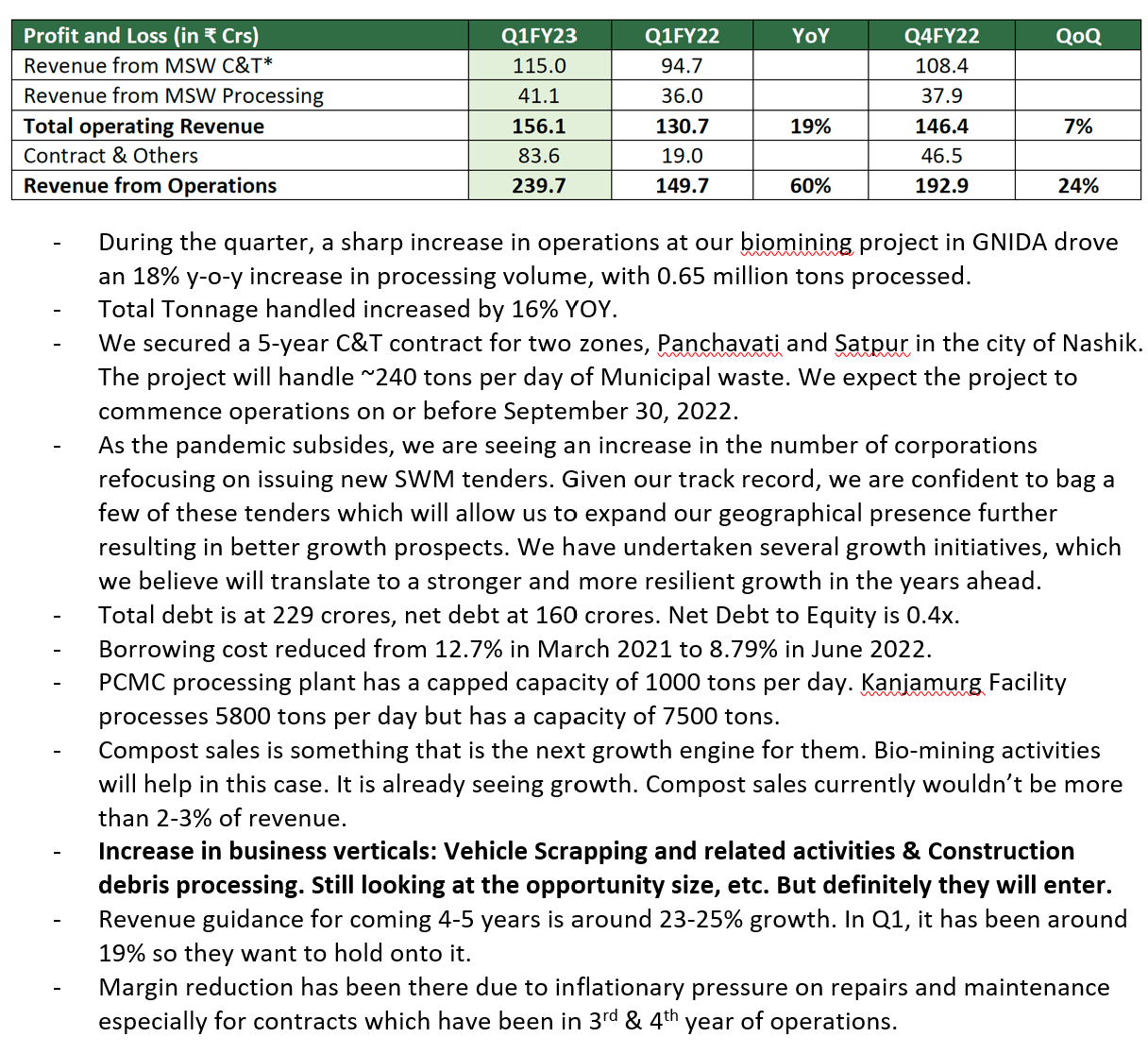

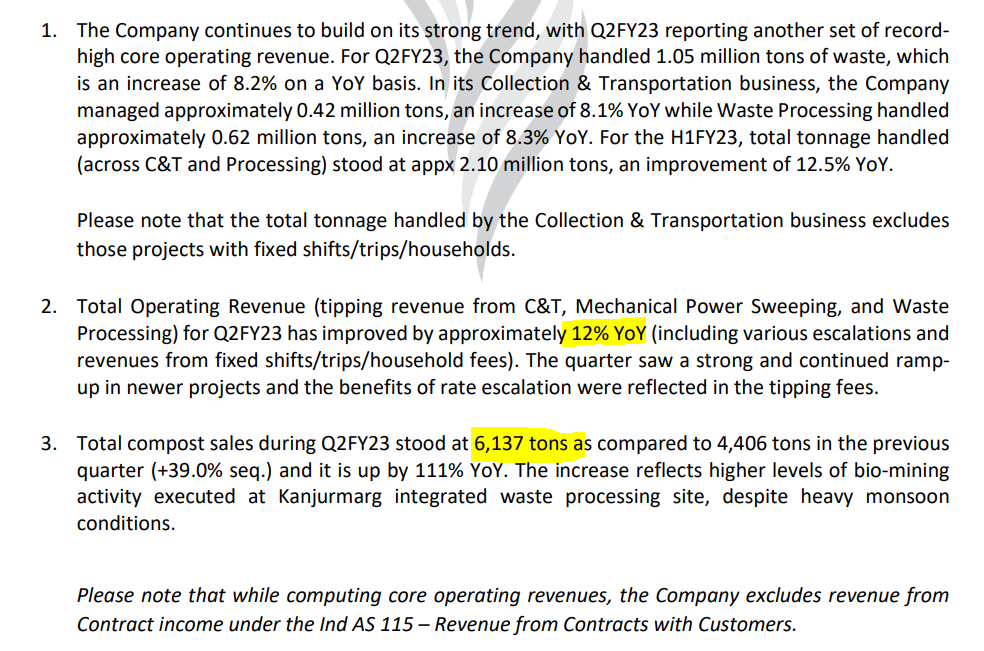

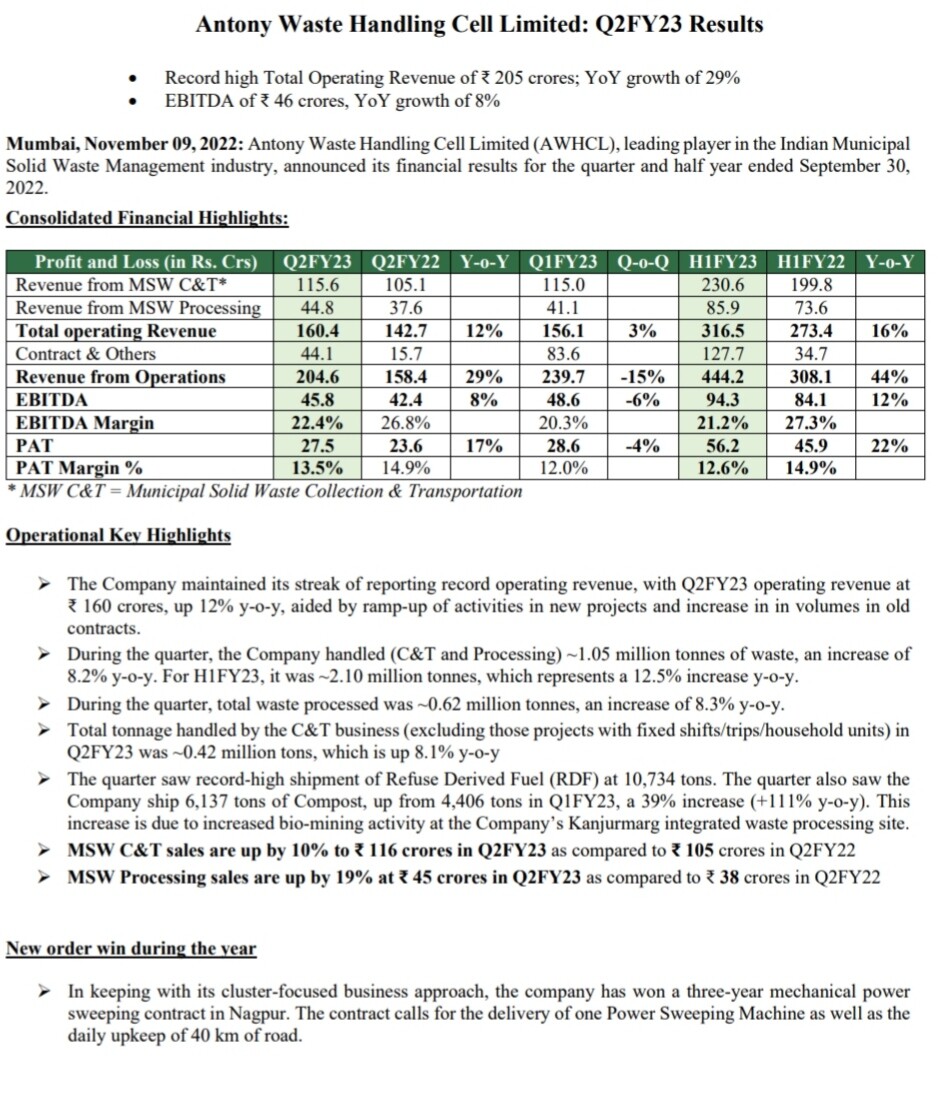

mentioned 12% upscale combining revenues from MSW and C&T, MSW processing. estimating an operating revenue projection is about 142.7 Cr + 12% ( 142.7 ) = 159.74 Cr. In the above, 142.7 Cr is the revenue share in Q2FY22 for MSW and C&T, MSW processing. Further, 6137 tons of compost and shipment of RDF (10,734 tons) could fetch another 10 Cr. Addition to this, other contract would fetch 20 Cr approx. So, total revenue expectation would be in range of (160 cr + 10 Cr + 20 Cr ) 180 Cr to 190 Cr, this way it fell sequentially unless they mention any non-recurring credits to other revenues.

it is posted that operating revenue is 160 cr odd and the contract, other revenues added 40 cr odd, which becomes total revnues to 200 crore+.

Excellent numbers from co, although sequentially total revenues shows declining trend but, this could be ignored as Q1 received one off exceptional other income.

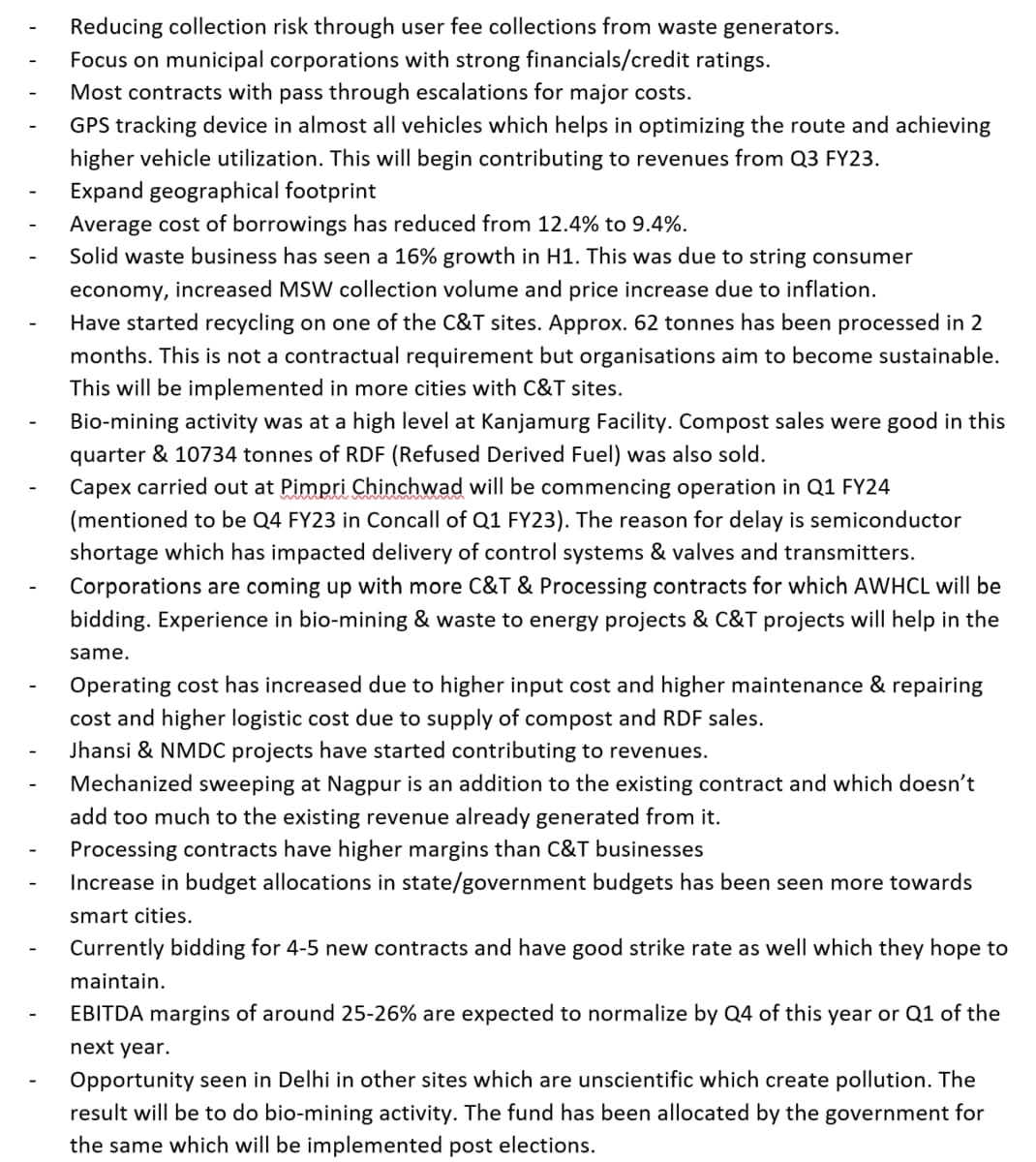

-Reducing collection risk through user fee collections from waste generators.

-Focus on municipal corporations with strong financials/credit ratings.

-Most contracts with pass through escalations for major costs.

-GPS tracking device in almost all vehicles which helps in optimizing the route and achieving higher vehicle utilization. This will begin contributing to revenues from Q3 FY23.

-Expand geographical footprint

-Corporations are coming up with more C&T & Processing contracts. Currently bidding for 4-5 contracts.

-EBITDA margins of around 25-26% are expected to normalize by Q4 of this year or Q1 of the next year.

-Opportunity for expansion seen in Delhi for Bio-Mining Activity.

No update on diversification of businesses which was mentioned Q1: Hazardous Waste Management, Vehicle Scrappage, Construction Debris Processing

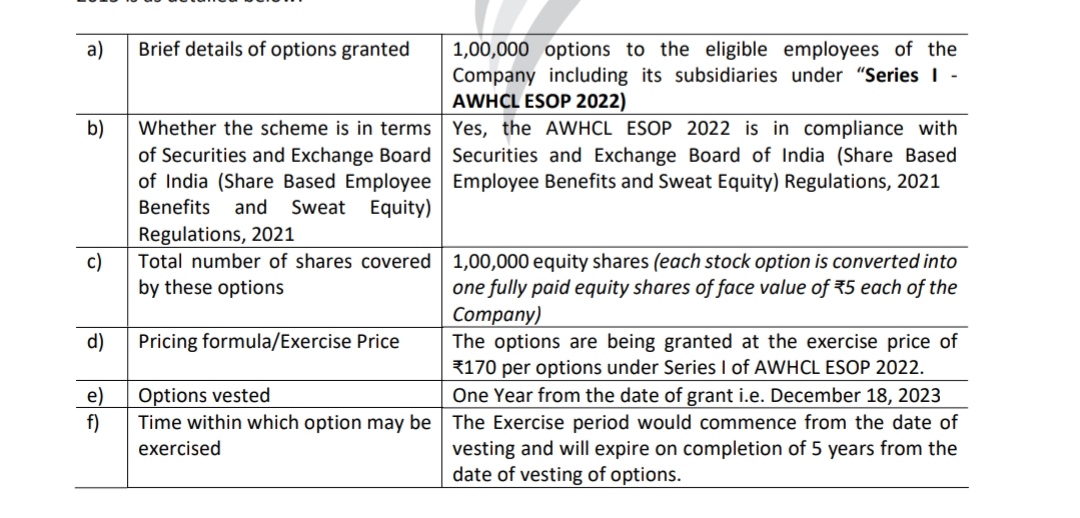

Grant of 100000 issues awarded at price of 170 Rs/- , would result in 100000*170=1.7 cr additional employee expenses this quarter. this result in margin shrinkage this time again.

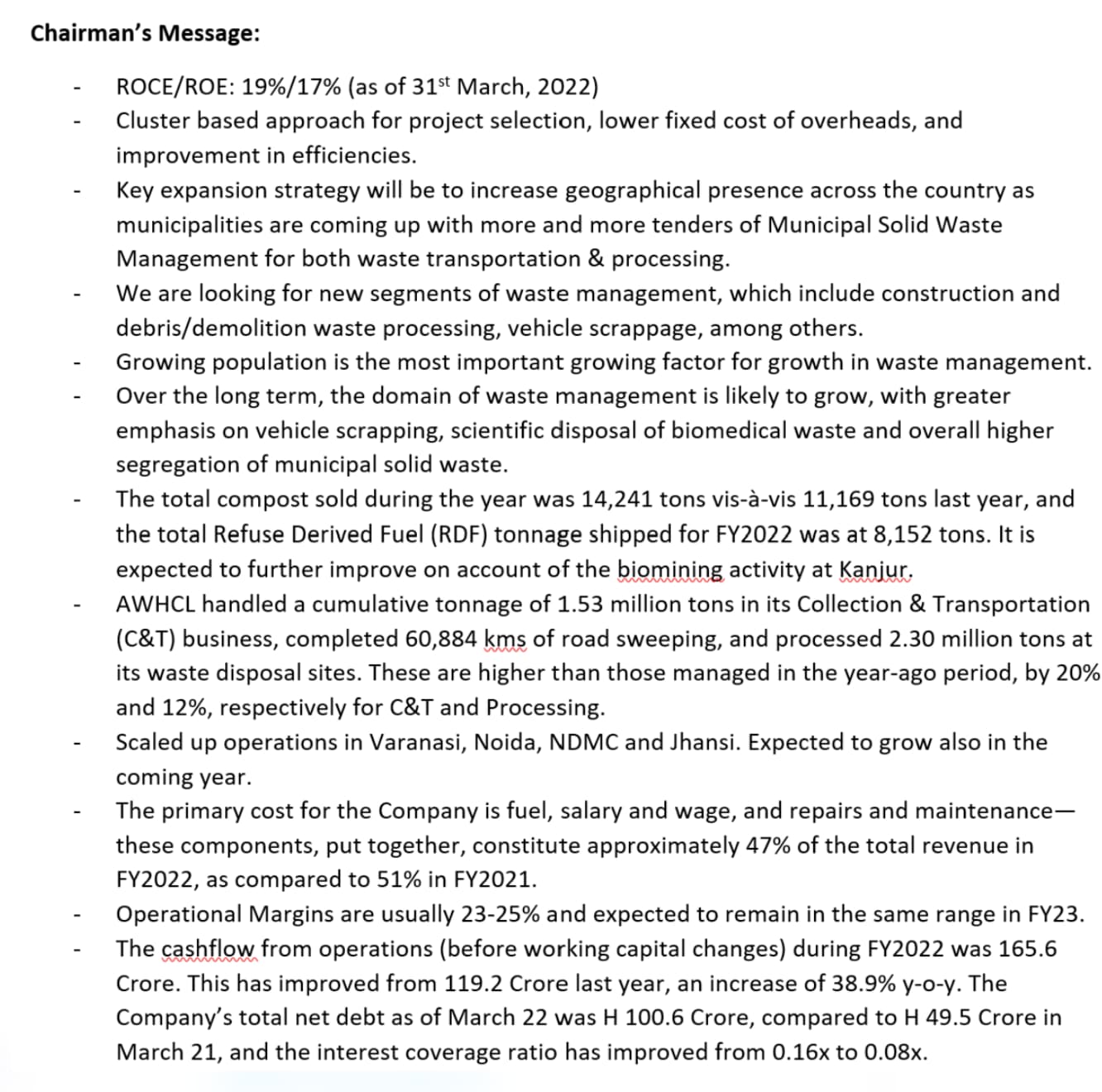

Our solid waste business has been strong for the first six months of the year, we recorded a 16% growth in operating revenue of Rs.316 Crores due to a strong consumer economy, commercial collection, MSW landfill volume and inflation aided price increase.

Activities at our recently bagged sites have shown rapid growth and are ramping up at a good pace.

During the quarter we have kick started our recycling business in one of the sites from where we collect MSW. This is not our contractual requirement but in line with organization’s aim of sustainability and working in the forefront of creating a circular economy. In this we will segregate the recyclables from the waste collected before sending the same across to the designated landfill site. This will help us generate revenue from the recyclables that we would segregated in this process. This is our first project and based on the satisfactory performance confirmed by approximate 62 tonnes being recycled in two months. We now plan to implement similar activities in all cities where the company has C&T operations.

your company has secured a three year mechanical power sweeping contract in Nagpur as part of cluster-focused business strategy. The contract calls for supply of one power sweeping machine and daily maintenance of 40 kilometers of road. We already have a C&T business in the City of Nagpur so bagging additional project helps us leverage on our existing setup and exploit our product lineup.

This follows the recently bagged five year C&T contract for two zones in Nashik namely at Panchvati and Satpur. We have completed the entire vehicle mobilization and the project will begin contributing to our revenues in Q3 FY2023. Every day we estimate that we will handle approximately 240 tonnes of municipal solid waste from this project.

MSW C&T project side: we have 13 ongoing projects. Our MSW C&T business volumes increased by 8.12% year-on-year to 0.42 million tonnes in Q2 FY2023.

MSW processing projects: the total tonnage processed during the quarter increased by 8.3% year-on-year to 0.62 million tonnes at our MSW processing projects which included Kanjurmarg, Pimpri Chinchwad, and Greater Noida bio-mining project.

Regarding our construction at Pimpri Chinchwad site we now anticipate that the project will begin in Q1 FY24 which was earlier planned to start on March 2023. The reason for these two months delay is due to the global semiconductor shortage which has impacted the delivery of distributed control system, control valve and transmitters.

The increase in core revenue was driven by contribution from newly bid contracts, general increase in volumes in existing C&T and processing contracts and also partially from the tipping fee increases which are built-in, in the contracts

Over last year we have made significant investments in our people including proactive wage adjustments and an improved benefit package and increased training. Leading repair cost and transport costs remain elevated, higher cost for parts, third party service are factors which we continue to watch.

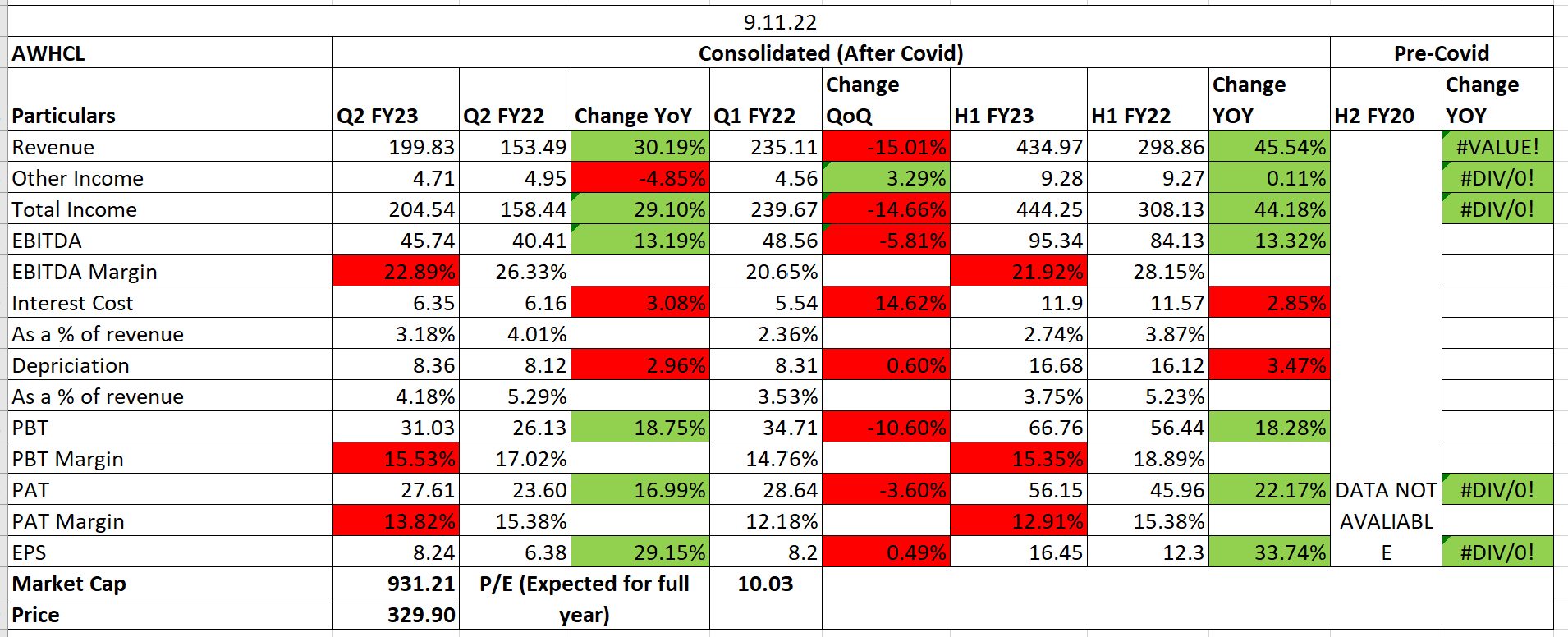

both Jhansi and NMDC have started the operations so if you look at on a sequential basis that decline in revenue is primarily due to Rs.41 Crores of processing cost which is absent now so that is one of the key reasons why you are seeing a fall in my revenue which is offset by an incremental revenue which has come from a core revenue section so both on Jhansi and NMDC the core revenues have started kicking in.

if you want to include all the receivables in the financial assets as well as the current and noncurrent receivables my total DSOs would be around 102 days as against maybe 92 days for this period last quarter. This includes certain receivables payable by the client at the end of the project life so going forward as a management practice we will start incorporating all the receivables current and noncurrent and even the money which is payable at the end of the project as a separate line item and we will disclose that separately

over the last couple of years we have seen slight bit of degrowth in the corporations’ spending patterns so this is as per the report that has been given out by the market research company so may be with newer policies of government spending increasing over the next couple of years we will again revisit this but this is just market report that we have got from the entity which we are sharing.

total receivables including trade and financials the total amount as of September stands at around Rs.200.08 Crores.

CWIP in the financial assets partly refer to assets that have been procured and deployed for the Nashik C&T contract because these are not transferable to the corporation at the end of the project life and also present capex that we have incurred and we are ongoing at our waste to energy project and the Kanjurmarg site wherein these are used for generating RDF and compost which are not transferable to the corporation so those capex are sitting at my CWIP in my financial assets today.

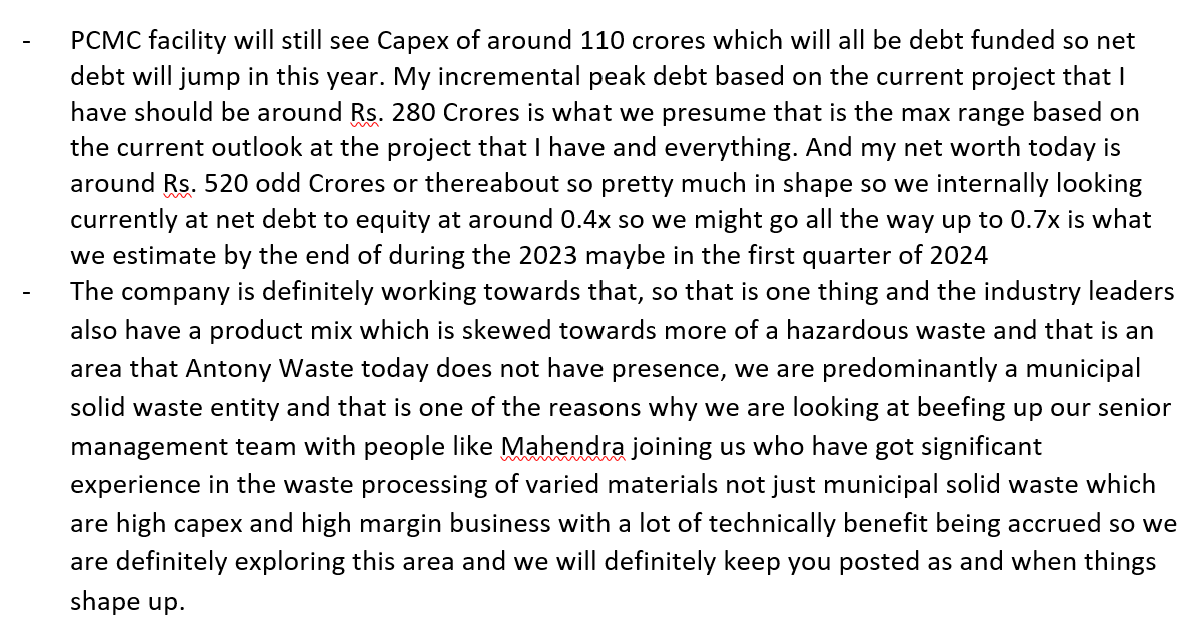

For the Pune project we are estimating an incremental capex of Rs.67 Crores. This bulk of it this will be spent in Q3 and Q4 and may be part of it will be in Q1 based on the independent engineer’s certification but Rs.67 Crores is what we expect at the waste energy plant to be done. At the Kanjurmarg site we are looking at our incremental capex of around Rs.12 Crores for the second half of the current financial year. We do not see any incremental capex at our collection and transportation businesses. If at all it is there is going to be in the tune of around Rs.1.5 Crores to Rs.3 Crores but that is depending upon the tonnage improvement that is likely to happen. As of now it is not happening so maybe we will defer this to the next financial year.

Jhansi is fully ramped up. NDMC and Nashik will be rolling out in the benefit zone.

NDMC by itself we will say Rs.100 Crores annualize revenue I would say that I would be looking at least four months of revenue coming in the current financial year and Jhansi is not a very significant in that time so that is anyway going on and that would not have any dent. Nashik the size you mentioned is 240 tonnes project so that again will not move the needle significantly but gets adds to the total.

What happens is the contract revenue component reflects the capex that I am doing and there is a contract clause which is related to that which you are right to quantify that so once the revenue is out, once contract revenue and the contract cost is out that get replaced with two streams of revenue, one is my tipping fee and the other is the sale of power so that gets added into my topline and the proportionate cost operating cost will sit in my operating cost line.

we are seeing a significant amount of cost that is sitting today as part of the transportation cost which we had to incur because of setting up the entire linkage systems and the segregation part of work so we have opexed all of that during the quarter and may be some of the cost will sit in the current quarter so the benefit of better realization and the margins flow through is likely to happen by Q4 of the current year and the Q1 of the next year. This being the monsoon we were not able to have a better margin play over here because the moisture levels are high and it is always difficult to work in monsoon conditions when we do bio-mining.