What’s this!

Are they getting into music production?

Seems like a gimmick.

Need to focus much more on Core business.

Awaiting results.

Anyone has access to Distribution numbers for AS in their states of operation?

How many retailers they go to each month from how many distributors?

Hi Guys,

What does it meant by this paragraph on page 11. Is it saying that volumes are low in North East Region. So profit will be low in upcoming results?

https://nsearchives.nseindia.com/corporate/ANNAPURNA_10022024123443_Intimation_SE_PB_ASL.pdf

It is just grammatically incorrect sentence. What they mean to say is that as a company majority of their operations and hence revenue is being driven by the North-East region of India, and they think that the profits are inadequate. The sentence should read:

“The company is regularly making profit. However, presently our volume of operations are limited to North East Indian States only. Because of the limited span of our operations, our profits seem inadequate.”

Point 2 suggests the measures that the company is taking to improve the span of their operations via geographical expansion and diversification, and, increase the utilization of their production facilities.

Point 3 is forward looking statement, which signifies that because of the steps mentioned in point 2, they are confident of posting better than previous fiscal’s results.

6 Likes

Positive development

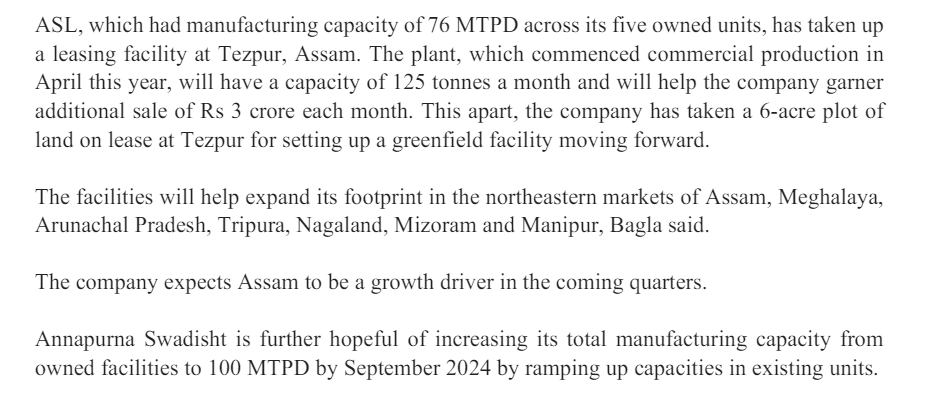

Annapurna has accquired a 6 acre plot in Tezpur, Assam on a lease basis for a greenfield manufacturing facility to expand its footprint in the North-East market.

https://nsearchives.nseindia.com/corporate/ANNAPURNA_19032024142232_Intimation_SE_PR_ASL.pdf

2 Likes

Positive development

Annapurna has entered into the edible oil business via acquisition of Arati brand. Hopefully this would also provide with backward integration with consumption of oil manufactured in-house, increasing margins.

Press release: https://nsearchives.nseindia.com/corporate/ANNAPURNA_27032024133842_Intimation_SE_PR_ASL.pdf

1 Like

The edible oil business is mustard oil. 60% of the crushed seed will go into making oil cakes that would be sold as cattle feed to farmers. The mustard oil will be sold through Annapurna’s own and Arati’s current distribution channel and would fetch 5-6 cr per month in revenue. I dont think it would be used in-house.

1 Like

This is a double edged sword. Edible oil business is highly competitive in nature and margins are generally in single digit. Look at Adani Wilmar or Patanjali’s edible oil business. I consider this as a case of “di-worsification”. Only time will tell how company uses this.

2 Likes

Commencement of production facility at Tezpur to serve the northeast market having a potential to add 3 Cr monthly revenue.

1 Like

The arihant capital interaction is out : https://www.youtube.com/watch?v=FKiEB78ieKA

2 Likes

The managment looks confident on their growth and doubling their topline in next FY and then growing it at 50% for FY26-27

The acquistion gives them a hedge from their core business and also a commodity play on the increasing consumption of mustard oil in the west bengal and nearby regions

The fory into new geographies is the main driver for growth as penetrating depper into the same market will not reward them that much like north east and extended parts of UP

Idk but I found the mangment less proffessional and a bit weak on the numbers that they had to recall otherwise the company looks good with a huge market potential

And at last they are trying to put food items which are sold through the non branded labels and pack them and sell it in a more sophisticated manner to target the rural and semi rural popultion of india

3 Likes

Some notes from the Arihant Capital meeting:

- Recently acquired a company which is primarily in the business of selling mustard oil. Can scale the existing business from 130 Cr to 190 Cr. Asset value is 27-28 Cr. The entire acquisition has been done on asset value.

- As on date products are being sold in West Bengal, Assam, Jharkhand, UP, Bihar and Orissa.

- 10 categories of products and 75 SKUs. 11 if you count mustard oil after acquisition of RR Proteins.

- Total production capacity stands at 76 MTPA per day.

- Margins have expanded due to economies of scale and better utilization of logistics due to the company entering into weight heavy products.

- In the process of implementing their own ERP system.

- Plans underway to expand into central and northern India, starting with Uttar Pradesh.

- Recently acquired a 5 acre plot in Tezpur, Assam

- Why acquired an edible oil company - Preference for mustard oil in India is growing, brand loyalty in West Bengal. Will be margin acretive, as the edible oil is a heavier product, so optimized logistics will come into play. Will also benefit the company because of the better reach in the region. The acquisition has been done on asset value. The cherry on cake is the market already created by the brand. Co is expecting better uptake after revamping the packaging and pricing. Annapurna will be taking over the 20 Cr worth of debt from RR Proteins.

- Co enjoys better margins because of indigeneous machines which can be modified per requirements in a shift’s time. Plus, the pricing structure makes their products competitive. It is easy to deal with the products that are available at prices which are multiples of 5.

5 Likes

If we assume the same growth in EPS next year too, then it’s trading at 20 one-year forward PE. But it’s an optimistic view.

After today’s correction, the stock is available at 35 current PE.

1 Like

There was a bulk deal in case of Annapurna Swadisht Ltd as per data below ( Courtesy: Trendlyne)

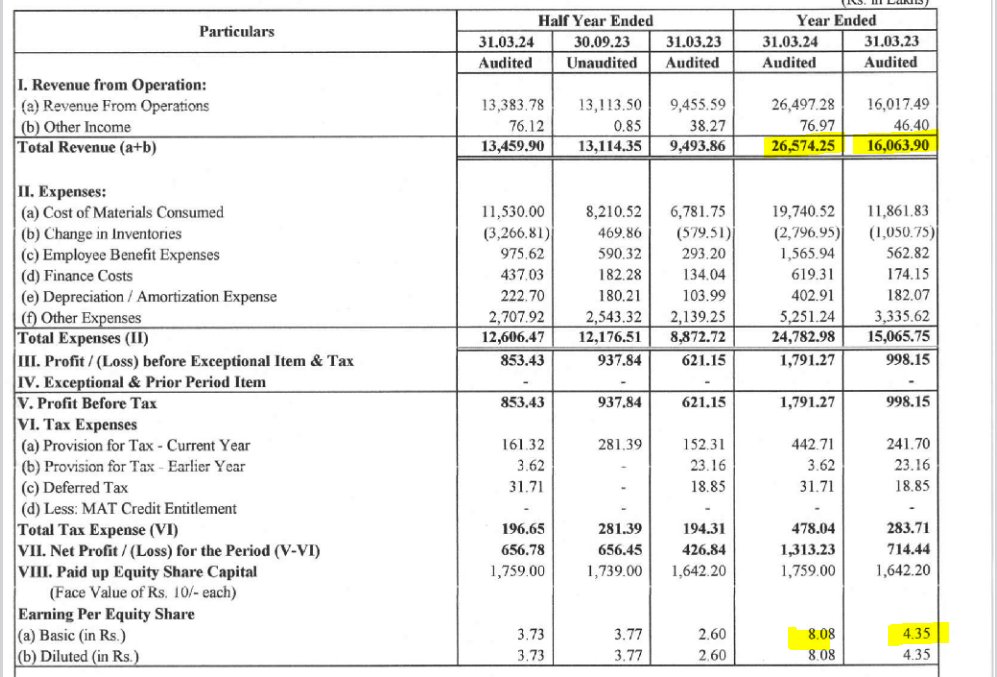

There was decay in profit in H2 comparison with H1, which may be ascribed to stangant sales in H2 comparion with H1, higher depreciation, employees cost, finance cost and other expenses. The increase in expenditure is quite normal for growing company.

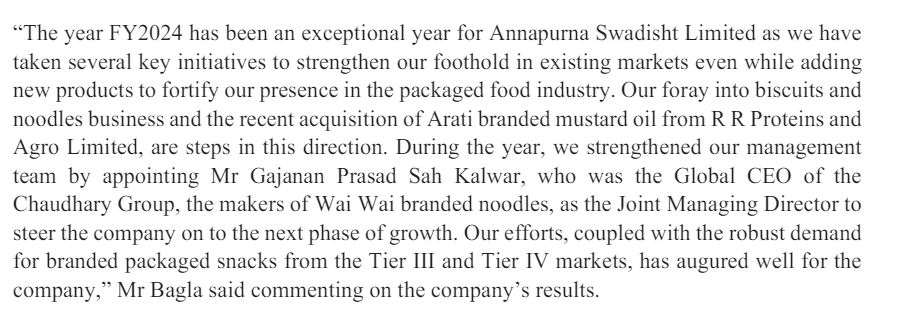

Company is roping in professional management team.

For long term company seems to be taking right steps in right diection. Following pressrelease from company may be referred:

The increasing SKUs, geography reach is mentioned in following part of press release of company:

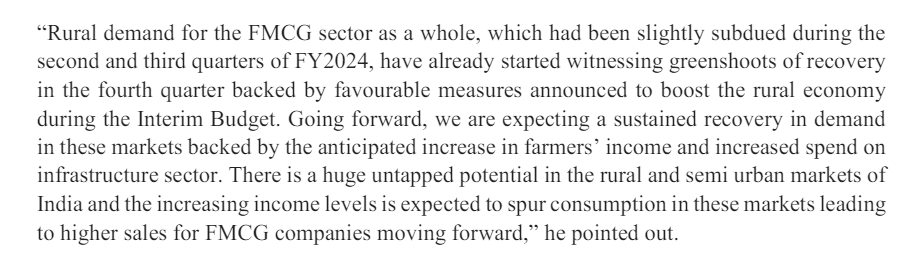

Comoany is envisaging demand recovery in coming months:

Complete press release are available at https://nsearchives.nseindia.com/corporate/ANNAPURNA_31052024140140_PRESS_RELEASE_ASL.pdf

Company is having market cap of Rs. 504 Cr. and having P/s ratio of 1.9.

Disclosure: Invested

4 Likes

That jump is due to listing of the shares. Pre-listing PE should not be looked at.

but the shares got listed in oct 2022. this jump is in august 2023?