Just to add to what Nalini shared, they have recently hired Mr. Sanjay Kumar as head of operations, who wast earlier cluster head for instant noodles Wai Wai and before that with Nestle, handling four instant noodle (MAGGI) manufacturing lines having capacity of 150 tonnes per day.

3 Likes

Personally, this does not inspire confidence, not that it is uncommon, it is common AFAIK with FMCG businesses, but this could also mean such KMP may again move if a more lucrative offer is made from other companies, even back to home, so to speak, just like in IT.

And for the stipulated time period, if any changes are made, and there is visibility of such changes in the business, if the important personnel leave, the company will replace them with available talent, and can build on the already established processes and go forward.

Not invested, been following the posts for a few days, just saying.

2 Likes

RAVI SARDA (CFO) SOLD 100000 shares, value Rs. 3.057 cr (Rs. 305.7 / share) through Market Sale.

Does not sound good.

Disclosure: invested.

1 Like

Just noticed that the buyer is marque investor Ajay Upadhyay in Annapurna Swadisht who bought 175500 shares.

Resignation by Rahul Surekha- President Operation

https://nsearchives.nseindia.com/corporate/ANNAPURNA_08122023185008_Intimation_to_SE_resignation_Rahul_Sureka.pdf

Question for those who are holding.

Is there a path to 10x EPS in the next 5 years? What are the general expectations here?

Market size is limitless, but distribution & advertising will be critical.

Keenly interested in the company, wish to learn more.

A quick answer without the arithmetic of FA:

The path is well established with ample opportunities. Right now, they are into snacks and fast food (newly introduced) categories:

- Western snacks - chips, rice puff based, cakes

- Indian snacks - namkeens

- Simple drinks - glucose based

- Noodles, biscuits

The potential options from here seems to be the following:

- Indian snacks - Increase the spectrum of namkeen offerings

- Indian sweets - Playing on the turf of Bikaji, Haldirams and Snactac (Reliance Retail)

- Indian pickles

- Different ethnic foods - Tomato ketchup (keeping it neutal since I do not know where it originated), Chinese foods - soya sauce, schezwan sauce etc., Mexican foods - salsa (big opportunity South America’s taste palette matches Indian taste palette), American - mayo, cheese blends, Italian - pasta etc.

- Daily consumables - Bread and buns via contract manufacturing

- Drinks - low-cost energy drinks on the lines of Varun Beverages’ Sting, fruit juices

See all this getting played out in Reliance Retail’s Snactac brand. BTW, I have not seen Reliance selling their products in small shops. It is exclusive to Jiomart and Reliance Retail.

Geographical distribution

Right now, they are primarily located in eastern India, and in the process of expanding into north and north-western states like UP (recently contracted Gopal Foods, Mathura to manufacture snacks for them), Delhi and parts of eastern Rajasthan (to keep distribution competitive). Thus, just from the geographical distribution perspective, the company presents an opportunity that is only going to grow bigger from here-on.

Management

- The management seems to be of high quality and so far, has walked the talk.

- Given their size, they are already having some names from the giants like Nestle, Parle, etc. on their payroll. That means the management has challenges to keep them engaged and are conscious about the quality of talent walking in the door. Also, not shying from hiring senior management from good companies shows they want to grow smoothly yet aggressively.

Disclosure: Invested

5 Likes

Thank you, @Parakh

The product mix is clear & easy to understand. It’s a blend of a Maggie Noodles, Balaji Wafers, and Haldiram Namkeen, if you may.

The positives that I see are:

-

Built distribution in the East, where no one else has been successful. IF they’ve addressed this unaddressable market, and captured it, then the’ve planted the flag where others haven’t and may not even try to.

-

Size - due to their comparatively smaller size, they’re quicker in implementing changes and taking decisions.

Major challenges:

-

Product Mix: They aren’t namkeen only, noodles only, chips only, and moving forward, Chinese foods, breads, juices & drinks only. This is like Maggie launching a Chings sauce, or Chings launching a Haldiram namkeen, or Haldiram getting into Paper Boat Juices. They’re all of this. Are they spreading themselves too thin?

-

Advertising: As they venture into organised & controlled markets, they’re up against the big boys. ATL/BTL and all the other retail jargon will come into play. They cannot out-advertise, they cannot out-distribute in these areas, so how they get an edge remains to be learned. And, they have to do this across multiple product verticals.

-

E-commerce: I read that they’re also focusing on D2C with Amazon / Flipkart. Is this smart or a distraction, given the tall task they’ve setup for themselves?

I like the underdog story, and root for it, but is this biting a lot more than they can chew?

They will need to raise a LOT of funds. Will need a clear product introduction strategy (cannot bring in bread + juice + Chinese, etc etc all together), will need team divisions and/or clear milestone based plans regarding e-comm/retail, and they will need some celebrity brand ambassadors who will help establish a footing in the controlled markets.

Having said this, they’ve raised funds from some astute and visionary early-stage investors. Ajay Upadhyay is no rookie, and no fool.

So, there must be something cooking that public shareholders are not privy to, as yet?

4 Likes

Product categories:

So, the options mentioned are a figment of my imagination, and not any commitment from the management. What path the management takes, needs to be seen. But any arithmetic we do to calculate the projections, may benefit from some variations introduced on the basis of future potential optionalities.

Funds:

Yes, they would need funds and in the current environment that should not be too difficult for them, given their area of operation, record of growth and profitability.

Are they spreading themselves too thin:

May be not. While I do not have any background in food manufacturing, but my understanding is that once a food’s recipe has been understood and finalized, it from there-on a matter of manufacturing it (some tweaking may be required depending upon raw materials) and distributing it. Since they can leverage their existing distribution network, it should work out for them. Depending upon the products they may select different distributors. Plus, they are leveraging a mix of their own plants and contract manufacturing. They currently have 6 manufacturing locations per their website out of which manufacturing unit 6 is Gopal Foods of Mathura with the biggest capacity and Annapurna has an exclusive manufacturing contract with them, although the exact capacity exclusive to Annapurna has not been disclosed.

Advertising and going against big boys:

The major selling points for them is their taste selection done to suit the taste palette of the region and the smaller ticket size that helps people try out their offerings. This also helps in impulsive buying, like buying a Rs. 5 namkeen packet to go with a Rs. 10 tea.

Another thing is that they offer a smaller unit to a distributor, making it economical for the distributor to deal with them, compared to the bigger players like Balaji or Pepsico. I am attaching a video in which Mr. Ritesh Shaw mentions this. So, dealing with Annapurna is better in two terms - unit economy and working cycle for a distributor. This further percolates to retailer level.

As far as advertising is concerned, I do not have much to contribute. But, from my experience, I have bought almost every brand of namkeen and snacks either because I wanted to try them out or have already tried them in the past like Bikano, Snactac, Crax, Uncle chips (didn’t knew at the time of buying that they have been taken over by Pepsico) etc. without seeing any advertisements of these brands. I think people are now open to try various brands irrespective of the fact whether they have appeared on TV at primetime or not.

E-Commerce:

I searched for “Olonkar” brand of oil and for Gohona Bori on Amazon and Flipkart, but was not able to find anything. Maybe it is a work in progress.

I have a couple of queries that I will drop to their investor relations team and will update you guys here.

5 Likes

Not so much a figment of imagination, they have a lot of those live already → https://www.annapurnasnacks.in/our-products

I couldn’t find them on Amazon, but was surprised to see a different Annapurna brand in a similar product line → Listing …so it seems this other Annapurna has a lot of products already listed. Whenever Annapurna Swadisht lists, it’ll have a tall task in differentiating from this other brand. This is a big red flag, as it’s going to create a lot of confusion for customers.

–

While the future is ahead of them, there is a lot they need to figure out. I don’t think it’s going to be plain sailing, and I don’t think they have a clear path & plan of action, at least it hasn’t come across in any of the material I’ve read/watched.

I hope there is an underlying plan of execution for the near future.

Disc: Invested, hopeful, not biased.

1 Like

After the company got listed, I was not able to find any presence of “olonkar” brand on online retail platforms. However I was able to get a whatsapp number to order “Gohona Bori”. However on the price front it seems like a mismatch to other products that it sells. The minimum order for delivery was 5 Jars (6 pieces in a jar). And price per jar was Rs.90. Now after one year, I do see some of their low ticket size products available in small kirana shops. However, I would seriously not compare the products to the established brands like Haldiram, Maggi etc. Annapurna Swadisht products are quite inferior. And there is high competition with local unlisted players.

Not invested, tracking.

2 Likes

Gone through above comments. It was really helpful.

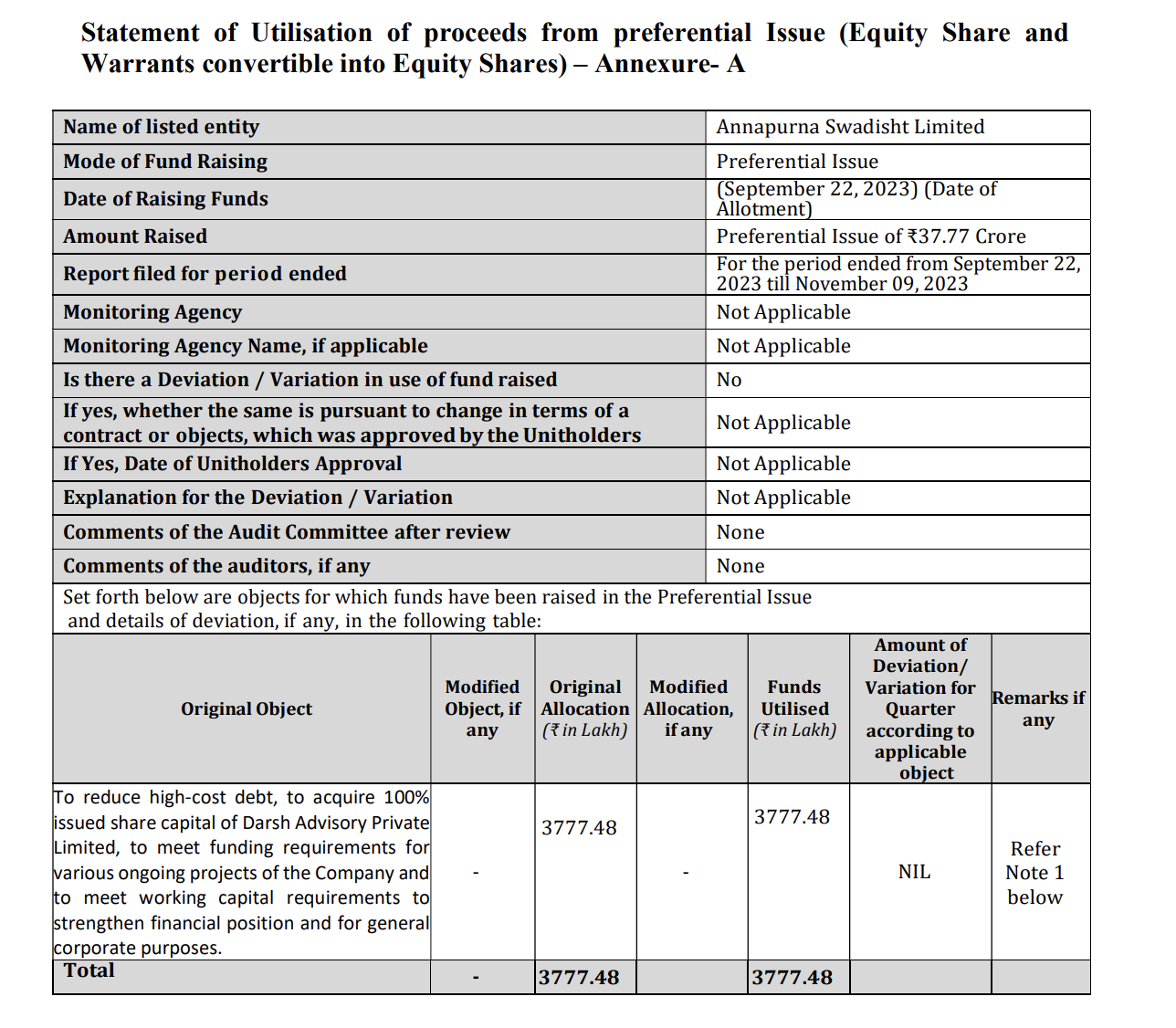

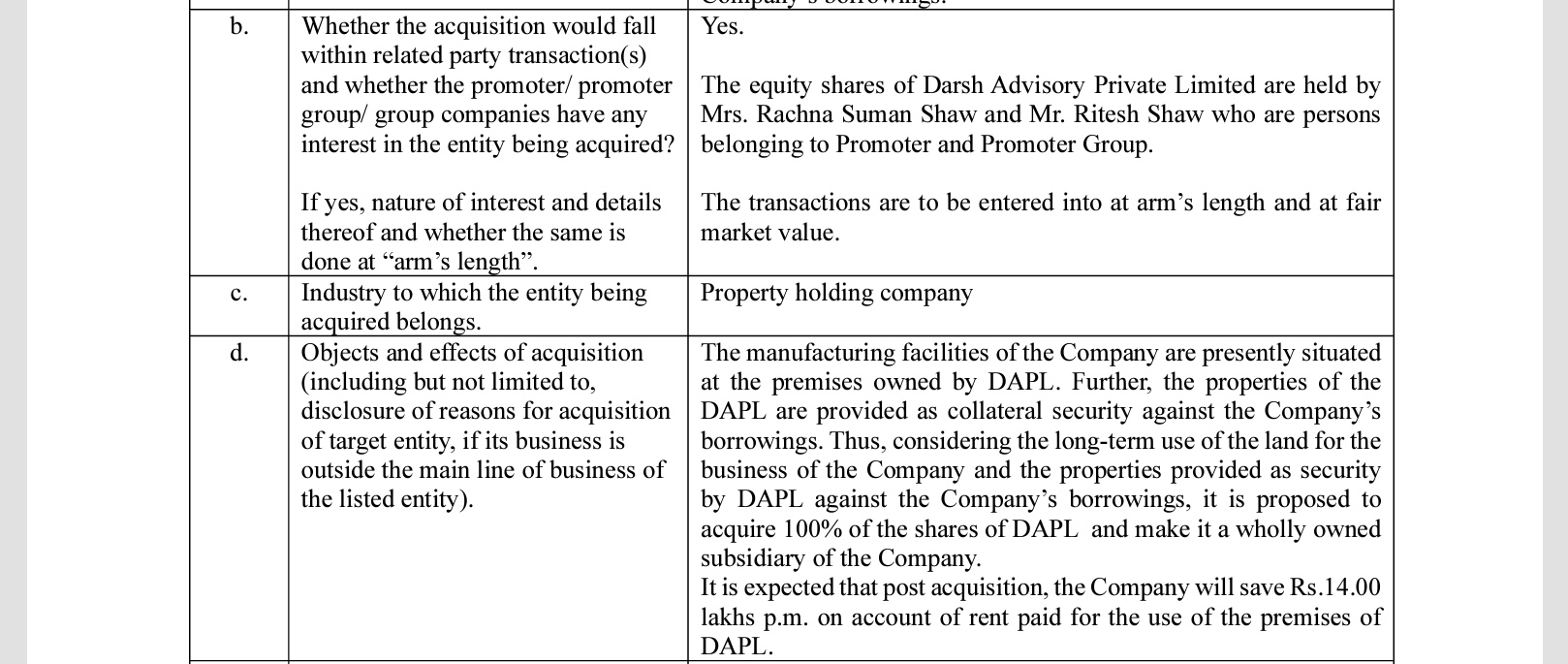

@Chethan_Ck @Moonrise @Rezang_La Do you guys know why they are acquiring 100% of Darsh Advisory Private given they have common director Shreeram Bagla and business is not similar to Annapurna?

Also how much are they paying to acquire this company? It may be a very naive question but still want to know.

DAPL was owned by the promoter, Mr. Ritesh Shaw; the rationale for the acquisition was duly disclosed at that time. Hope this helps.

FundRaise 1.pdf (647.6 KB)

3 Likes

@Rezang_La Thanks for the quick reply. Somehow missed this entire page while understanding about the company.

1 Like

It’s a positive move.

Assets are being built.

Is the Cream Roll a recent addition or has it been around for a while?

Per the wayback machine (internet archive), cream roll was available as far back as May 30, 2023. Although, the price since then seems to have been increased from Rs. 5 to Rs. 10

2 Likes

Disclosure: Invested

1 Like

Can someone help me find the Google Finance tracker symbol for Annapurna?

Tried everything - can’t find it.

1 Like

I think they have not included the SME feed into their data. Annauprna, Dentalkart, Alphalogic Industries, Inflame Appliances, Robu are some of the names that I tried and are not coming up.