Few important extracts on product mix Q1 FY 20 call

What largely explains higher EBITDA per tonne in gas division

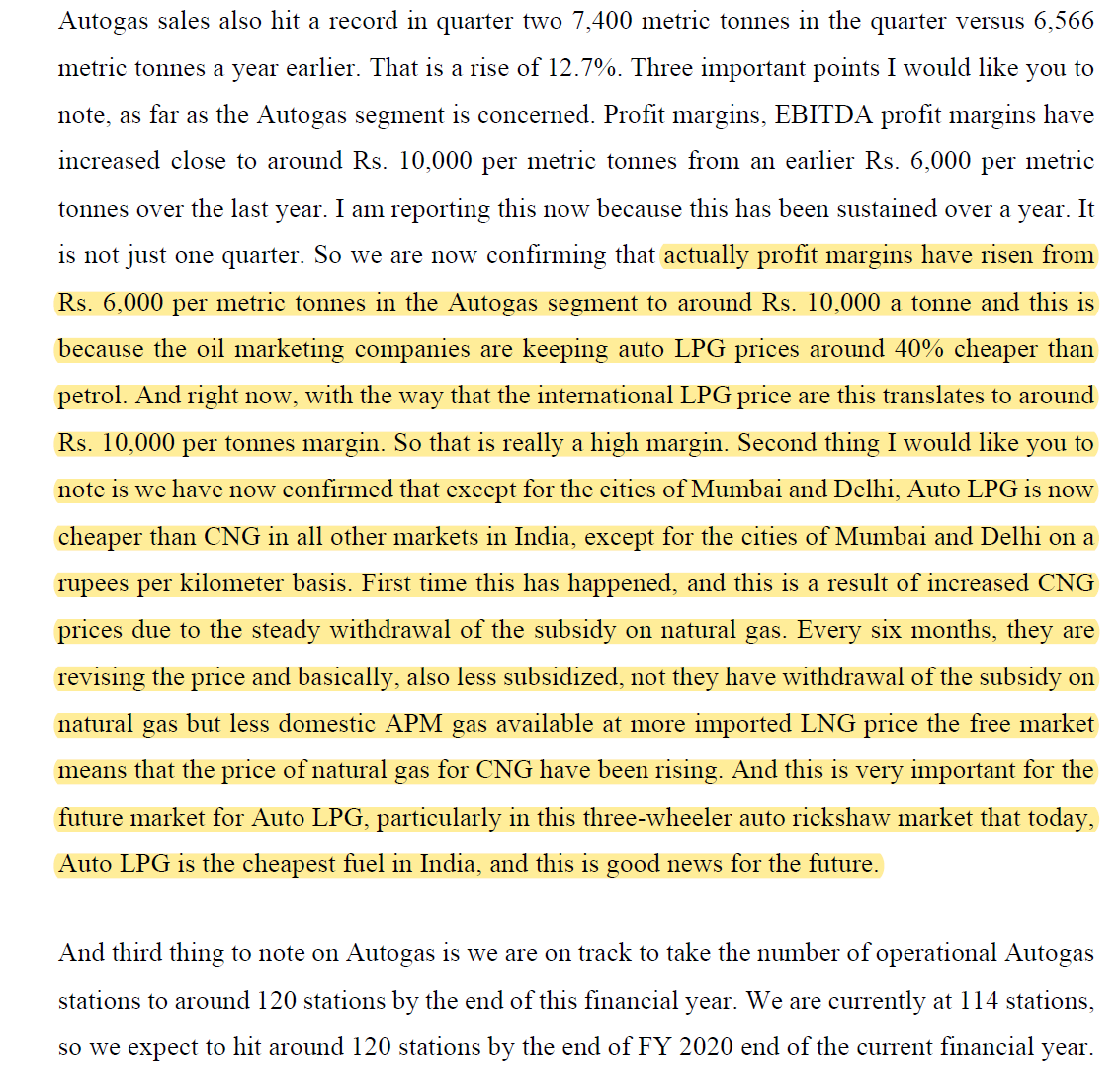

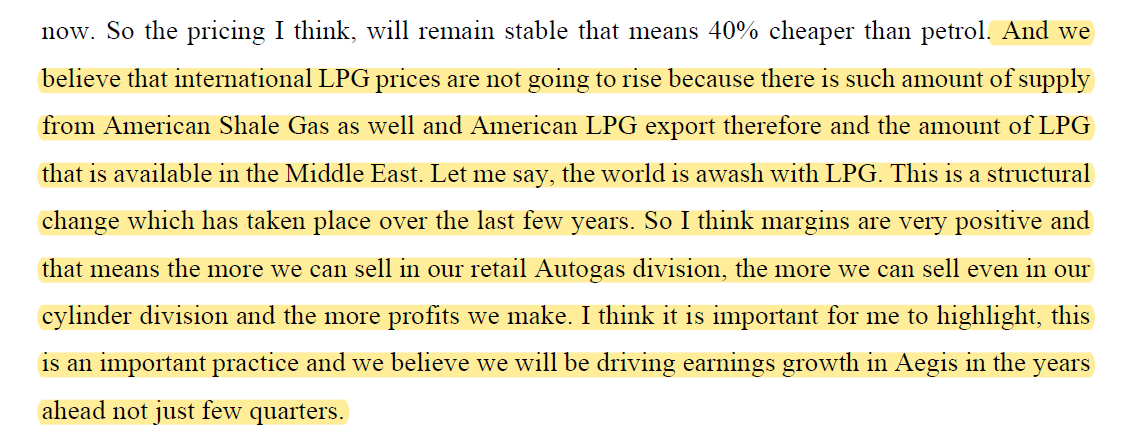

Auto gas (Q2 FY 20 call)

Few important extracts on product mix Q1 FY 20 call

What largely explains higher EBITDA per tonne in gas division

Auto gas (Q2 FY 20 call)

Since yesterday I have been spending more time on past data and annual reports. Thought of doing that as we did used to own some qty of aegis in earlier years but had sold out due to volatility in earnings or something. So was trying to understand the journey etc.

First thing to note is the huge change in valuations and returns post 2014 - stock was just 15-20 Rs even in late 2014 despite 10x growth in revenues over last 5 years and then the stock got re-rated and price multiplied over 20 times while the operating profits went 3x!

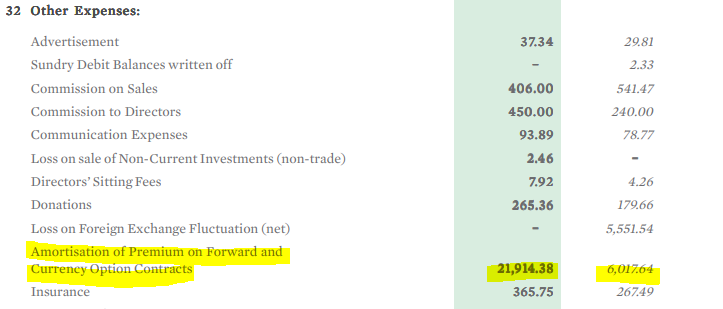

The financials of the company were hit between 2011-13 due to some forex hits etc and as I went deeper there were complex things like premium on options etc of large amounts.

It would be good to understand this pain period as it was the growth phase for the company. Will they face similar issues again this time and why not?

Also, looking at such winners, I keep asking - 1. what are the learnings for us to repeat and catch such winners early

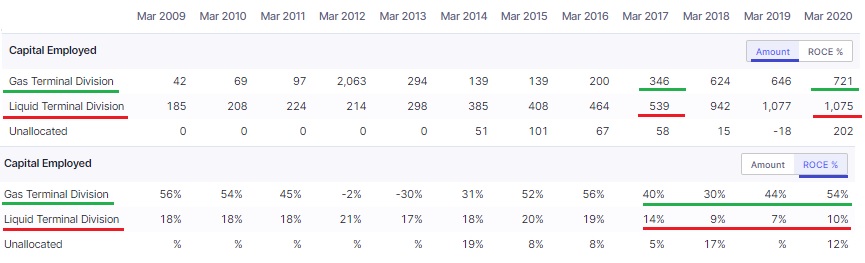

Regarding Liquid Terminal Division…

A quick look at ‘Product Segment’ feature of screener.in says, Liquid business segment has subpar RoCE. More capital has been employed in low RoCE Liquid than Gas.

Curious - Is the RoCE suppressed currently and expected to drastically improve (for Liquid)? A “cash cow”?

Thanks for sharing an early draft of the slides, Dhwanil. I have not been able to contribute much to this deep dive but have been keeping up with this thread + the presentation. My key takeaway from the presentation is:

Aegis has competitive advantage both in terms of the cost of the terminals it puts up (350cr for the kandla terminal vs 800cr for the Adani terminal) and also in terms of the static capacity turns. There are several reasons for the asset turns advantages mentioned in the deck and the thread:

I hope we can address in the Q&A section why competitors find it difficult to replicate aegis’s success. Can the Adani port not install the same larger in-tank pumps and also work 24x7? Also IIUC that port is deep water port as well. Lastly it would also be good to know if there are any insights on why setup cost or capex (per unit of static capacity) for the Aegis ports are much lower than competitors (this would essentially be another factor for higher ROCEs).

Static Capacity: 30,000 TPA

Throughput Capacity: 1.4 MMTPA

Turns: 46

Project Cost: INR 400 Crores

Port: Krishnapatnam

Reiterates the competitive capex cost of Kandla for Aegis. Assuming above project is using the latest technology and 46 is still the max turns they can achieve, it makes Aegis turns even more impressive.

https://www.pngrb.gov.in/pdf/public-notice/comt6.pdf

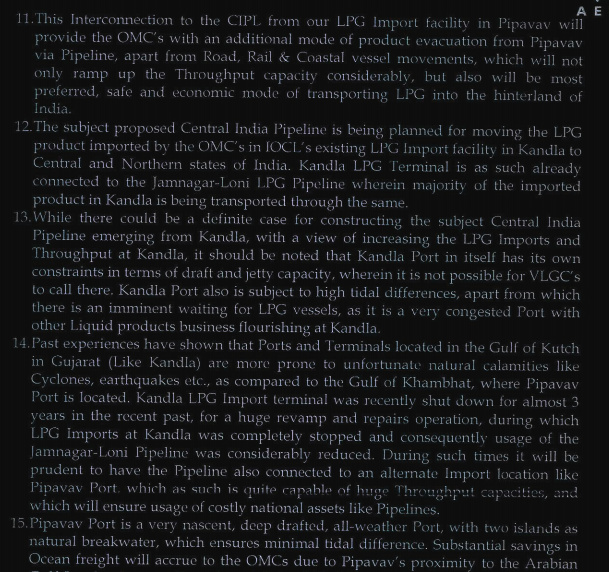

Aegis themselves had highlighted a higher natural calamity risk to Kandla compared to Pipavav. Above commentary was made when they requested PNGRB to consider connecting Pipavav to Kandla-Gorakhpur pipeline (CIPL) as a fallback terminal.

Good Presentation from IOC Chief Manager (LPG-Operations)

Great presentation by VP team! Would have loved to contribute more, but occupied with job.

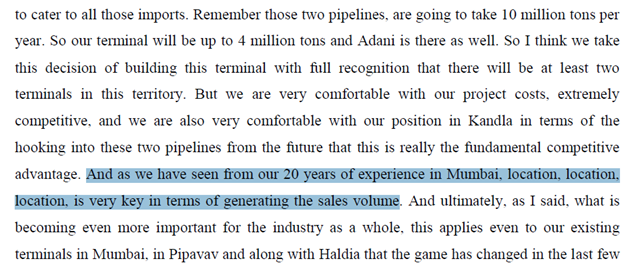

Important to track developments on Aegis Kandla (key to increase in throughput) and Adani Mundra terminal.

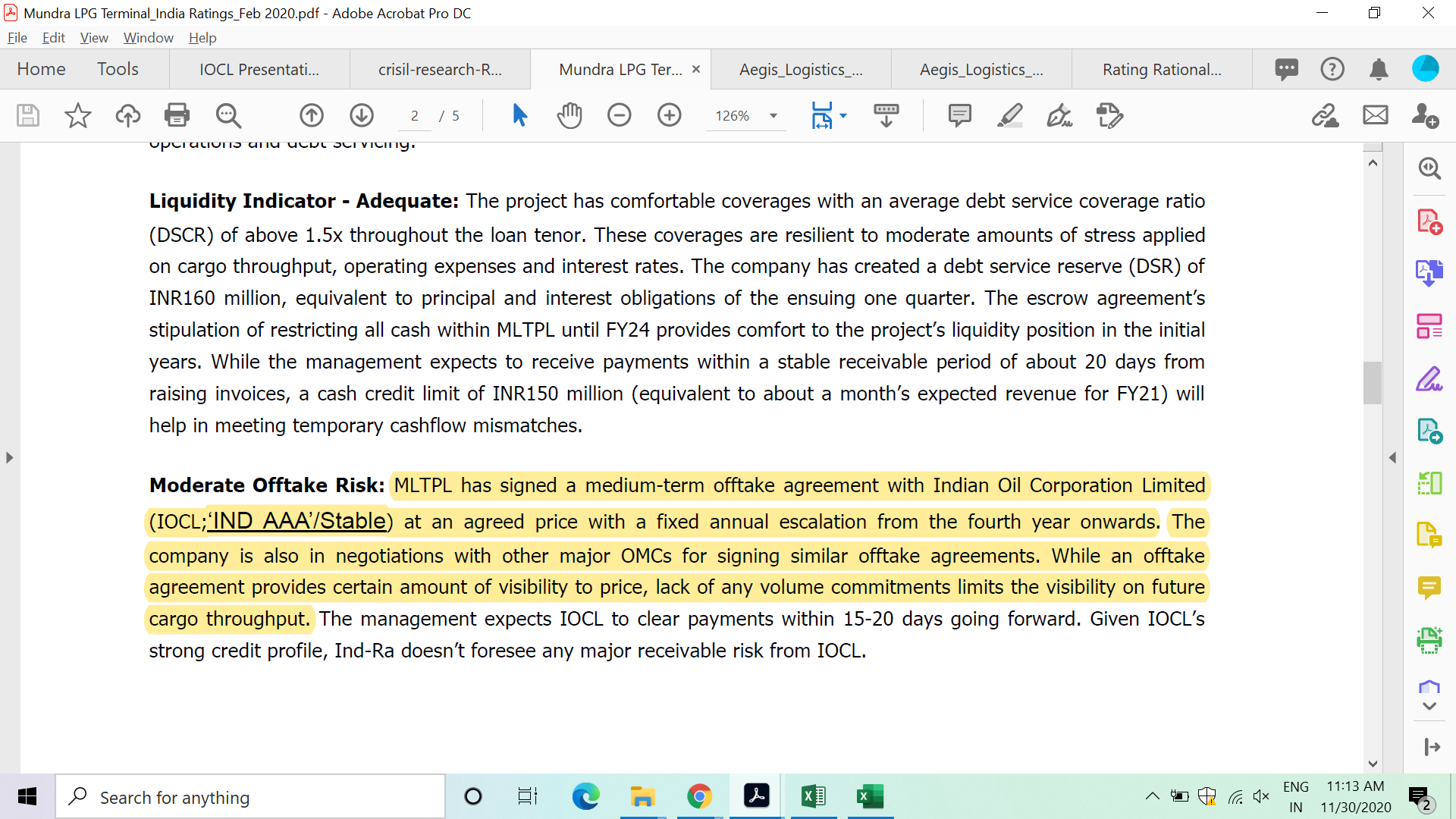

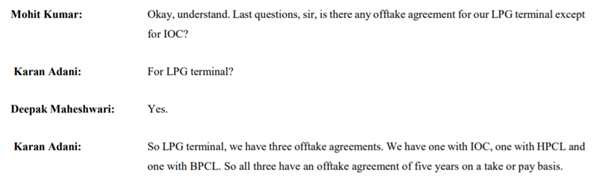

Adani’s have already signed three offtake agreements for their Mundra LPG terminal - one each with IOC, HPCL ad BPCL- for a period of 5 years on a take or pay basis. Expected utilisation at the terminal is c. 1.8 mmt for FY 21 (of the capacity of 3.2mmt).

Q2 FY 21 call

Q4 FY 20 call

Normally, going through Aegis past data and even Adani’s LPG terminal’s rating report, OMCs sign MoU with LPG terminal and these agreements are not take or pay is what I understand.

Also, till the data of publishing of this rating report (Feb 2020), Adani had offtake agreement only with IOC. May be they added two more clients later.

For me, the biggest growth driver and most attractive part in the thesis of Aegis is the LPG terminal segment and the growth drivers associated with it. Below are the volume, revenue and EBITDA (estimates factoring management’s indication of EBITDA in the segment being 1,000 per tonne):

The throughput volumes in the segment have grown by 37% CAGR over FY15 - FY20.

Post completion of terminal at Kandla, capacities will expand from 5 million tonne to 9.2 million tonne and management has stated in its concalls that across all its terminals, they plan to debottleneck and increase the installed capacity further to 12 million tonne. In addition, management has stated their plans to set up another LPG terminal in South India over medium to long term.

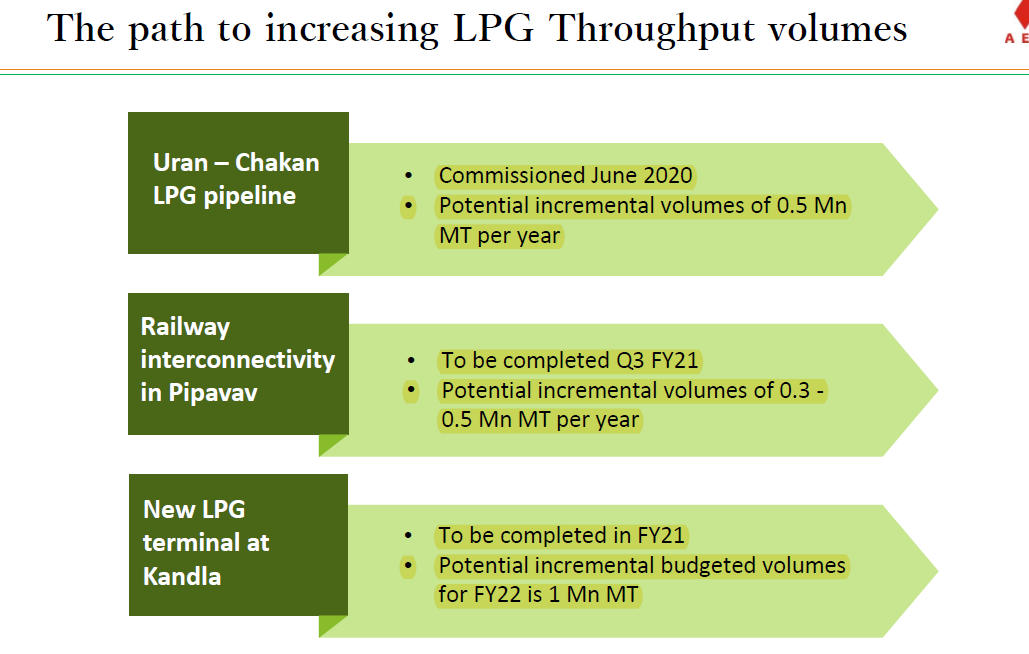

Now, let us do some maths for how volumes can pick up over the next few years. The following slide is form company’s Q4FY20 presentation:

FY22 will be an interesting year for the company. It will be first year when additional volumes from Uran - Chakan LPG pipeline (for Mumbai terminal) and railway gantry at Pipavav will contribute volumes for the full year (both to start ramping up volumes from H2FY21). Together with Kandla, additional volumes next year can be 1.7 - 2 million tonne and company can reach throughput volumes of 4.7 - 5 million tonne in FY22 from 3 million tonne in FY20.

Also, it is interesting to note that LPG imports have grown at 18% CAGR during FY09 - FY20 (source: Equirus report). Furthermore, it is a bit far stretch to imagine switch from LPG to PNG as cost of setting infrastructure in PNG is extremely high and it doesnt make economic sense to set them in tier 3 and tier 4 towns.

Another optionality can be the scale up of autogas stations (company plans to grow them from 115 to 200 in next five years), commercial and domestic LPG (by expanding distributorship and expanding to Tier 1, Tier 2 and Tier 3 towns and adding more LPG bottling plants).

Liquid terminal is a slow and steady grower for the company and grows at 5 - 10% per annum. The LPG sourcing business (in JV with Itochu) will be tender based and difficult to forecast.

The company throws out quite a bit of cash and despite its capex plans, it is expected to generate healthy free cash flow over the year. It is currently a net cash company (despite sharp jump in receivables as on March 31, 2020 due to covid which have come down in Q1FY21) despite significant expansions done by it over the past few years.

(Disclosure: Invested)

Some of the more top level questions that I have are:

a) Have we worked on how pricing scenario could impact LPG demand. For example Biden is expected to come hard on Fracking industry how do you see that change LPG demand. Also if LPG becomes expensive do you see a possibility of Reliance and Essar jumping back in the game?

b) The other interesting thing in entire LPG/CNG story is the cost in terms of kWh. So you take the calorific value and the best possible conversion from KG to kWh is almost 50% to 60% of that calorific value and see how the pricing works out. With the current solar auctions at below 2 Rs/kWh I don’t know how would the commercial use of CNG/LPG play out. Solar is expected to go down significantly from here as well.

The above is a presentation by Tony Seba to the GoI done very recently.

")

Recording of Team VP discussions on Aegis Logistics business on Nov 28th.

Have been receiving some questions/requests from well-meaning folks - for an update on recent announcements - the Aegis-Vopak 51:49 JV in particular - and how should/could one go about thinking through.

I am capturing below my interpretation of how things stand. If anything has changed in my view of the business/prospects since the time we actively collaborated/presented on Aegis.

Cons

Having said that (NOT easy to digest the above well), I do NOT see any other negatives, really (?) ![]()

Pros

Has the business/model become stronger/weaker?

To my mind the answer emphatically is - YES stronger.

Not only has this brought access/ strategic fit and technology/knowhow with a larger global player servicing large MNC customers in India, this deal ensures that important question’s answer for me - will it be able to keep increasing its distance with peers/competitors - again an emphatic yes.

Can they grow faster/bigger?

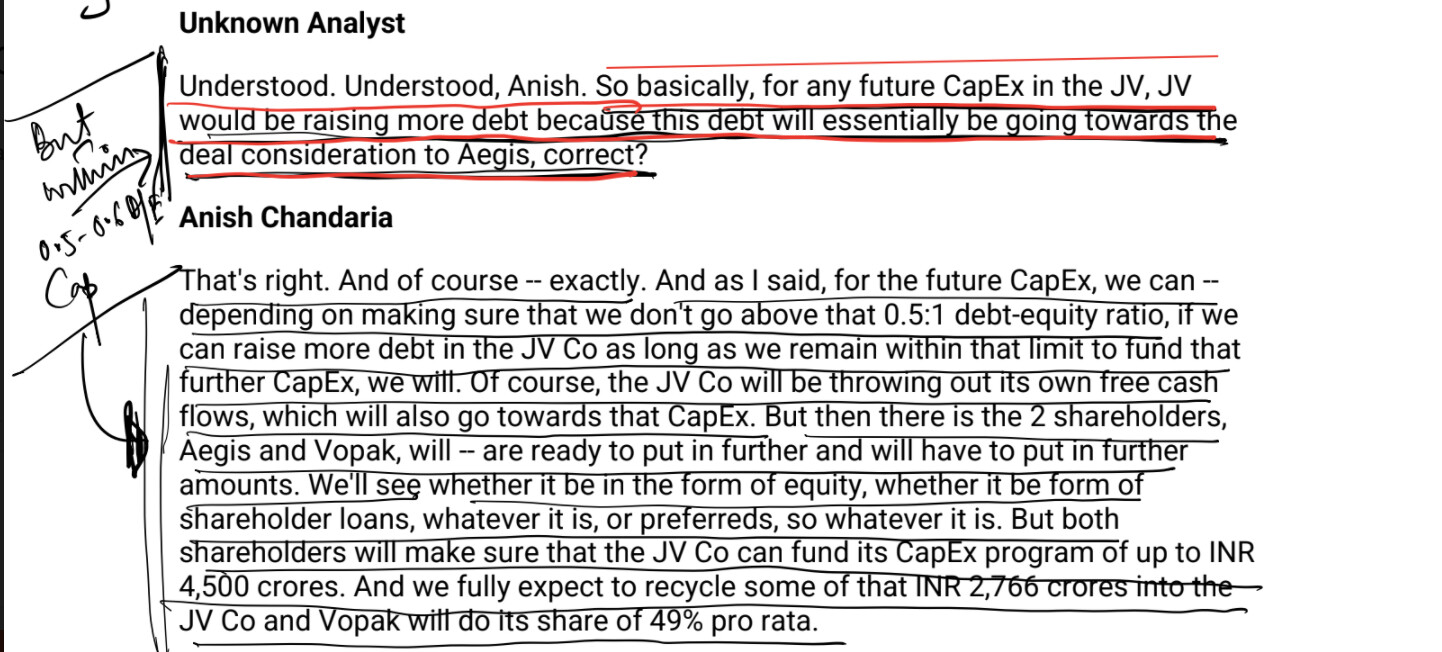

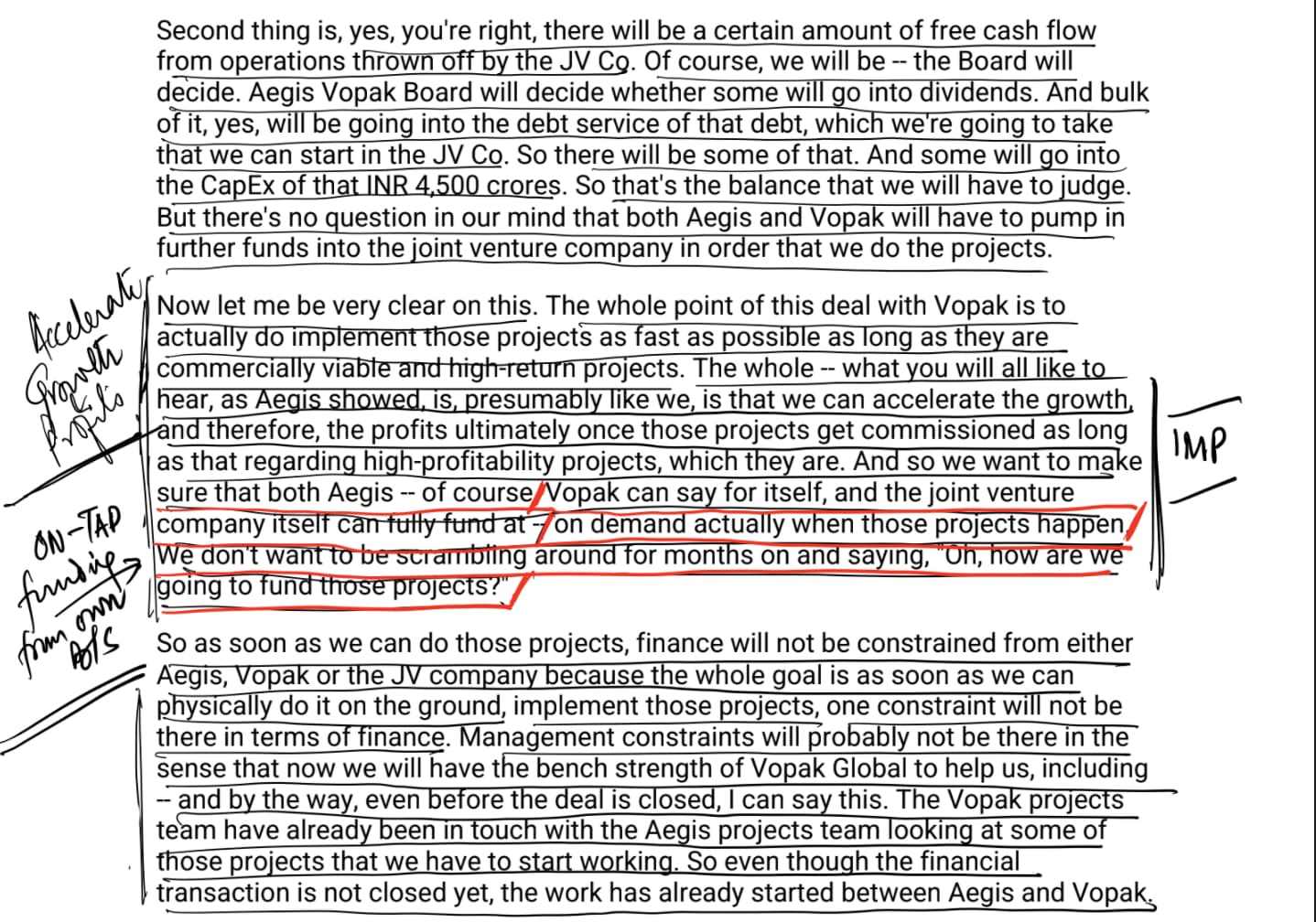

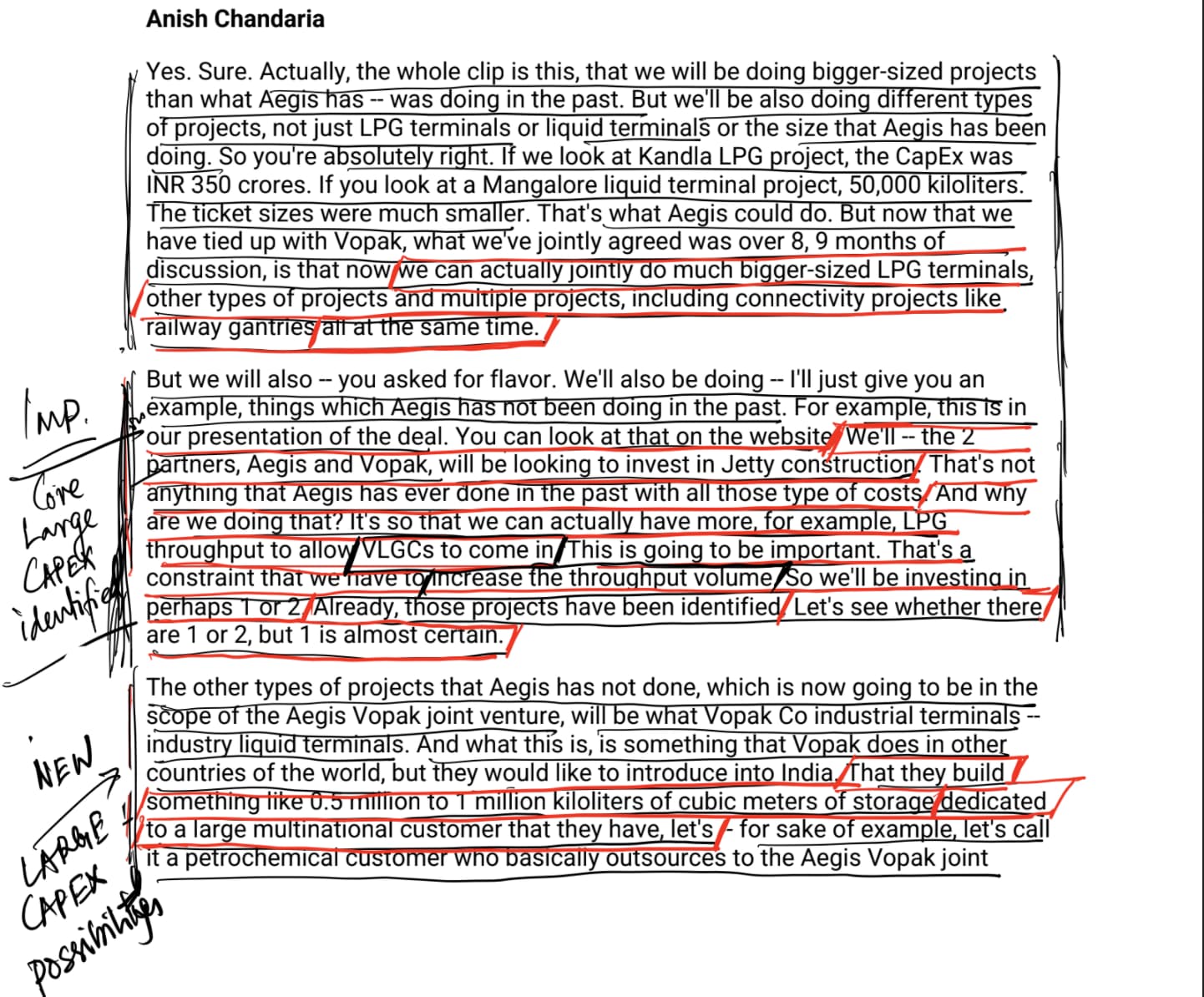

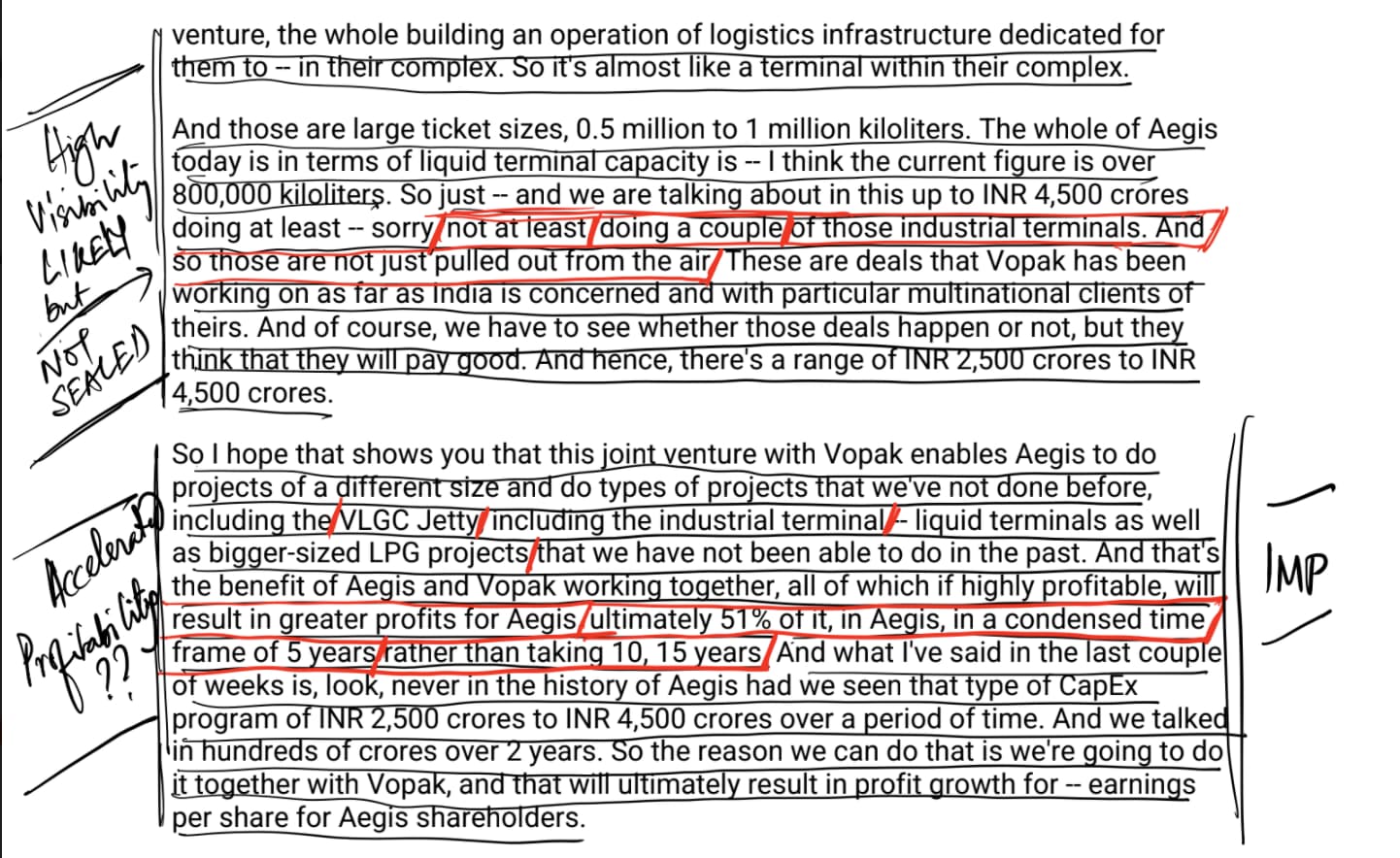

Again given the ambitions that Aegis is known to harbour, there is no doubt (in my mind) that for sure they can and probably will grow much faster. Why? For one - they have Capital in excess of 2500 Cr coming in (assuming they close the deal), so the ambitions for the kind of projects that they take on in the future will most probably be much bigger in scale if one goes by the latest Concall e.g. VLGC Jetty construction is one cited (project identified) - leads to higher throughput/efficiency; much bigger LPG Terminals is another; connectivity projects like railway gantries is another

What will they do with all the Cash?

Will minority shareholders be rewarded?

Again the answer to this lies in the answer to 2 above. Management intentions have been made very clear. There is only ONE purpose for that Cash that comes in (in the backdrop of NOT exceeding 0.5 - 0.6% D/E ratio committed/baked in into the JV agreement) - to accelerate the growth and scope of new projects to deliver accelerated profitability. Larger projects and more number of simultaneous projects, without any funding constraints. (Used to be the major ambition constraint pre-deal)? For example, Aegis total Liquid terminal capacity is over 800,000 KL, while Vopak is talking of working on 0.5 Mn to 1 Mn kind of individual Industrial Terminal requirements of MNC customers in India (note, no visibility/certainty of deal coming through).

Long story short, will all these lead to higher profitability than possible. erstwhile?

Management is on record saying there should be higher profitability now in 51% of Aegis in a condensed timeframe of 5 years, rather than taking 10-15 years. So yeah, potentially!

How do I know if all this will indeed be deliverable on (proposed/projected) accelerated growth/profitability? Can we take their word for it?

Well Investing is an ART form - every individual decides for herself/himself where the ODDS lie!

If we could place faith in the intent/bandwidth/execution capabilities of Aegis pre-deal, is there any reason for disbelief post-deal (when they are stronger) - if one accepts answers 1-3? if one doesn’t, then the answer to this, is also clear.

This is all about medium to long-term. What about the near-term? Mr Market has already reacted negatively (also pronounced because of a poor Q1)?

Hmm! As always that is exactly the challenge/opportunity before every individual investor to assess for herself/himself. I would think it depends a lot on individual situation/portfolio structure, components/temperament. There are no right or wrong approaches here. Some competent folks I know who have booked out. I also know many who haven’t ![]() .

.

PS: Latest Concall Transcript attached - to my mind all issues have been squarely addressed. Now, it’s one’s judgment call! Aegis_Transcript_30July2021.pdf (160.8 KB)

Please NOTE this is only ONE perspective. I am sure there are other perspectives to consider for a well-rounded, better-informed position on this issue. Requesting prolific contributors to this thread @desaidhwanil @ankitgupta @rupeshtatiya and @Rokrdude to add their own observations/comments.

Others most welcome too!

(please remember viewpoints backed by data-driven inputs pass moderation; yes Collaborator Corner threads are now open for participation from everyone - but is a moderated category now)

While there are many criteria we use to analyse a business and management but there are few which pose long-term challenges if they occur.

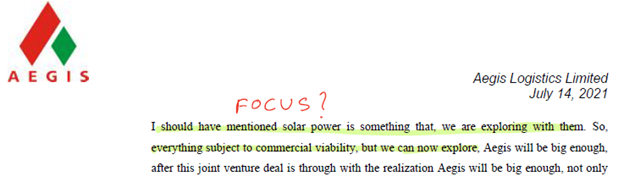

• Focus (or lack of it)

• Truthfulness (there is thin line of difference between illegal or ethically wrong.)

While I was reading there were few questions came to my mind

All valid questions but no Black and White hard answers.

Why is Aegis too aggressive in capacity expansion when they themselves say full capacity utilization may take many-many years?

• Location Location Location:

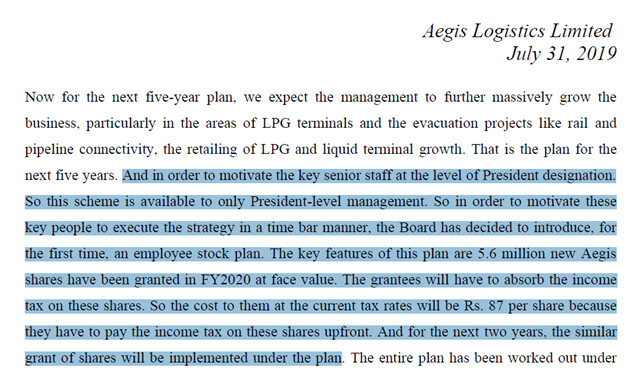

Why did they suddenly give so much equity to very few employees? Why did the company come up with ESOP 2019 when they were thinking about partnering and probably selling significant stake?

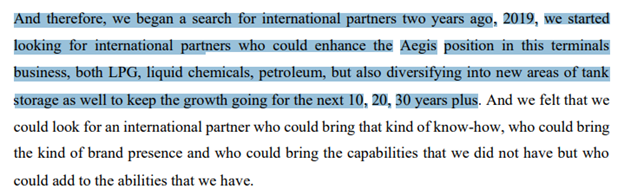

They started looking for international partners in 2019 and it seems they were thinking bid. If baffles me when I try to figure out why suddenly AEGIS in 2019 came out with a huge ESOP of close to 5% of equity. When you are trying to partner with an international player and future plans are in flux, What were they thinking when coming up with generous ESOP.

Who is the Employee who holds 4.4% of Aegis? How?

ESOP is a good idea and when a company says it is for President level employees, I may not agree with the idea of ESOP for selected few but I thought, fine.

Total ESPO: 5.6*3= 16.8 million shares. I thought, there would be quite a few Presidents who would be getting the ESOPs. But Then close to 4% went to a single person. I do not know much but I have never seen 4% ESOP to a single employee in a Non-Startup environment. I don’t know what this person brings to the table which others can’t. I could not find a valid reason. I’ll confess, I haven’t looked hard enough.

![]()

Its baffling, that too when the company was thinking of selling major stake. Is it just lack of better judgement?

Debt becomes Revenue:

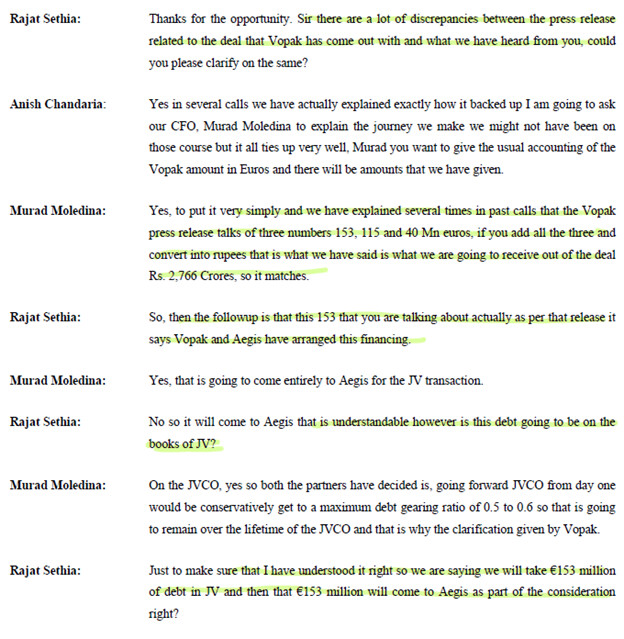

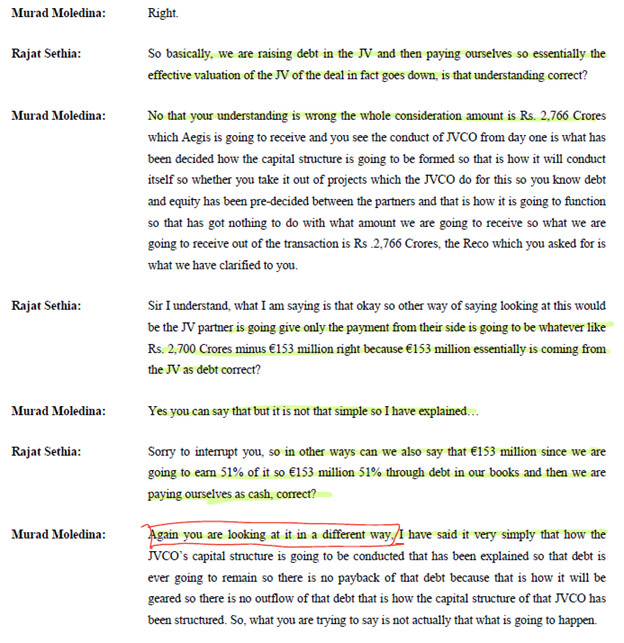

Someone shall tell ZOMATO that easiest way to become profitable is through Debt. Do a JV, transfer some asset to the JV and take a big loan in the JV. So? Nothing, just transfer the loan to the parent and it becomes pre-tax profit. Something new I have learned through Aegis – Vopak JV transaction.

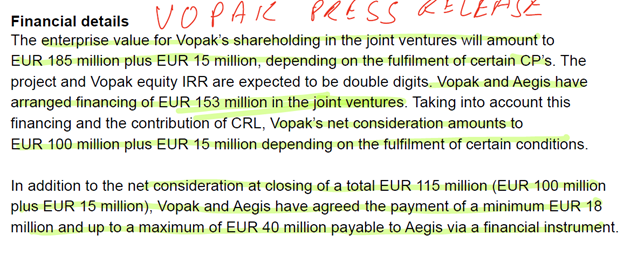

The press release of Vopak paints a very different picture than Aegis and when questioned in the conference call, Aegis could have accepted it as an oversight but there was an argument which justifyied Debt as Earning.

There is no wrongdoing, but hiding something or providing an incomplete picture was not called for.

Aegis on the transaction

JV Valuation: Different vantage point for the buyer and seller. Opinions could differ but Maths is not an opinion.

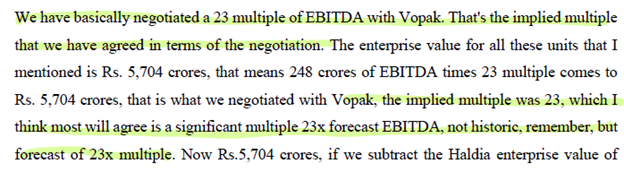

Vopak sells @ 6.3 times tailing EBITDA, though they have 70 terminals worldwide, why would they pay 23 time forward EBITDA to Aegis that too for non-controlling stake. But in Vopak’s mind they just paid 11 times EBITDA

Now look at how Vopak looks at the transaction

Are Vopak folks Pessimist? (or are they like Infosys, under promise and over deliver)

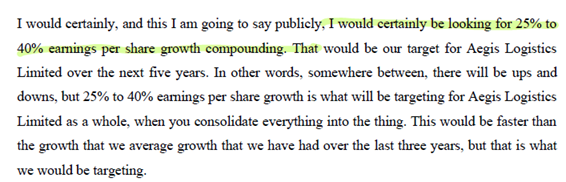

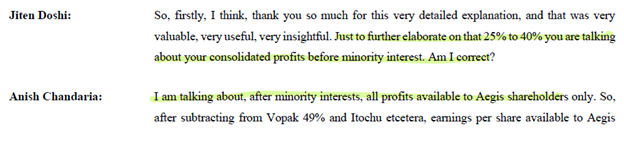

Let’s look at how similar or different Vopak and Aegis are looking at the future. Aegis expects to grow At 25-40% compounded for 5 years.

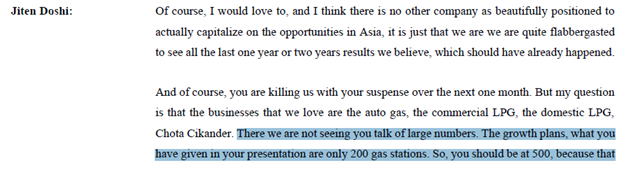

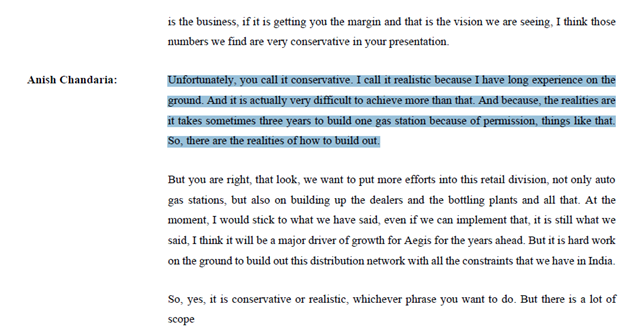

Anish himself explains why it is very difficult to scale the Auto gas business.

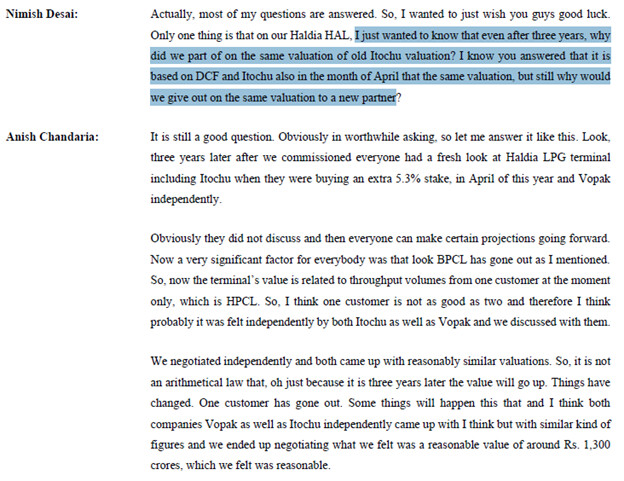

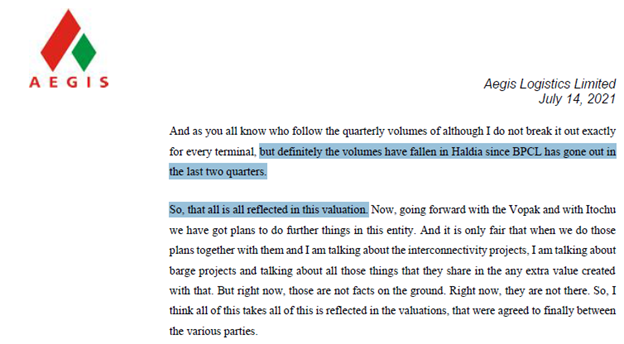

BPCL will move away from Haldia that was known well in advance: The line of response focusses on BPCL moving out of Haldia. But this was known for long. The valuation that Haldia has got, is it because of BPCL or expected long gestation period of the project?

Why were they so dismissive about competition from LNG?

When we think about LPG we are thinking about energy and not Gases only. As @Anant alluded to, we are in the market of energy and energy need can be fulfilled by LPG/ Coal/Solar/ Batteries/CNG etc. Whoever gives best output at lowest cost will take away the market share. Nobody is emotionally attached with the idea of using LPG.

Aegis has been dismissive about competition from LNG and then we are not in the market of GASES. Now they are talking about building LNG storage. I am not drawing any conclusion but did they miscalculate the market growth of LPG and built (building) huge capacities?

The capacities that Aegis has built or building, they could generate 2000 cr kind of EBITDA few years down the line. Why did they sell the stake at such low valuation?

I don’t know. But my current hypothesis is that they overestimated the LPG story. They are trying to the correct the mistake by diversifying into upcoming opportunities.

Focus or Lack of it : It’s not uncommon when business losses focus, it suffers for years. This is one the patters I have noticed where management losses focus to get into Hot Sector. It’s extremely difficult to digest large amount of money and we are talking about 2500 cr of cash. Overconfidence or too much hurry to grow leads to unrelated diversification.

Are we seeing the first sign of beginning of Lack of Focus in Aegis?

The JV and possibalities gives me goosebumps but then i have no answer for the Gray area whether it tilts towards White or Black.

I could be just wrong in my interpretation and willing to change my opinion.

Disclosure: Not Invested. Still interested.

Vopak Press Release (1).pdf (569.7 KB)

Aegis Business call Update july 2021.pdf (2.4 MB)

Thanks @Donald for putting out your view point on various aspects of recent development on Aegis. I think you have covered many aspects that are directly relevant in near term and have also touched upon areas which are relevant for taking a longer term view. I want to put out my thoughts as plainly as possible

Apart from being an extremely high quality company, Aegis thesis was also built around the growth prospects in the company on account of new LPG terminal capacity coming up at Kandla, Pipavav (because of railway gantry which helps them serve north Indian market cost effectively) and Mumbai. As the capex was at fag end and based on management commentary it was expected that ramp up of capacity utilization will lead to significant growth in profitability of the company. However, with this deal with Vopak, only 51% of the earnings of newer assets like Kandla and Pipaval railway gantry will accrue to the company hence leading to change in numbers which are significant.

The second point is regarding the deal valuation. In their call Aegis management explained that the deal was closed at 23 times EV/EBIDTA based on comapny’s estimate of EBIDTA for assets being transferred to JV. Even though it may look that Aegis got a fair deal, if we scratch the surface following points need to be considered

- Aegis has transferred assets having significant amount of new capacity to JV

hence as and when capacity utilization of this asset move up, EBIDTA may move

up significantly. Thus pegging valuation based on FY 23 EBIDTA was not

reflecting on deal valuation on normalized earnings

- Secondly, in the first call done post deal, I did not realize (not sure whether I

missed it or it was not called out) that the deal structure had debt component

where in fact JV was borrowing money to pay Aegis. Even though we are not

privy to the exact structuring of this debt, ideally while calculating EV of the deal,

one should adjust for the 51% liability arising out of debt taken in JV. Even

though this is simplistic understanding, I do feel that there may be structures

possible where despite debt coming to JV, liability accruing to Aegis may not be

in direct proportion to their equity stake. However, as it stands today there is no

clarity around the same.

All in all, it is likely that on a more normalized earnings and adjusting for debt, actual valuation on EV/EBIDA may be on lower side. As per VOPAK press release they paid 11 times EV/EBIDTA. One may arrive at different valuation based on one’s view on future earning, it will be lesser than 23 times on normalized earning after additional capacity would be utilized

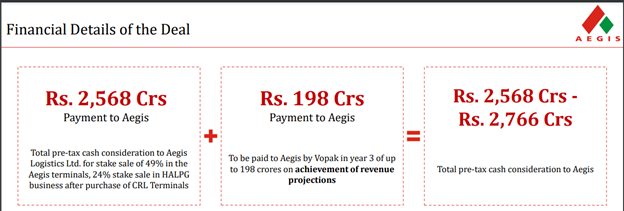

Now we have to put this in context too. Market was valuing Aegis, if you take management estimate on face value, total EBIDTA of divested and retained assets of INR 594 Crore (248 Cr and 346 Cr respectively) at 13000-14000 Cr Mcap (at time of deal). However, the accrued EBIDTA post deal to Aegis will stand at 470 Cr with the growth in EBIDTA accrual got diluted by 49% for key growth bearing assets especially Kandla. To compensate for that company would receive roughly 2568 Cr cash pre-tax and then 198 cr over 3 years based on achieving revenue projections. According to company they will have to pay anywhere between 15-20% tax so post tax accrual will be close to 2200-2300 cr. To me for parting with 125 cr EBIDTA and 49% earning of growth bearing assets that can more than double company’s capacity sounds on the lower end of valuation…at least compared to where market was valuing the company.

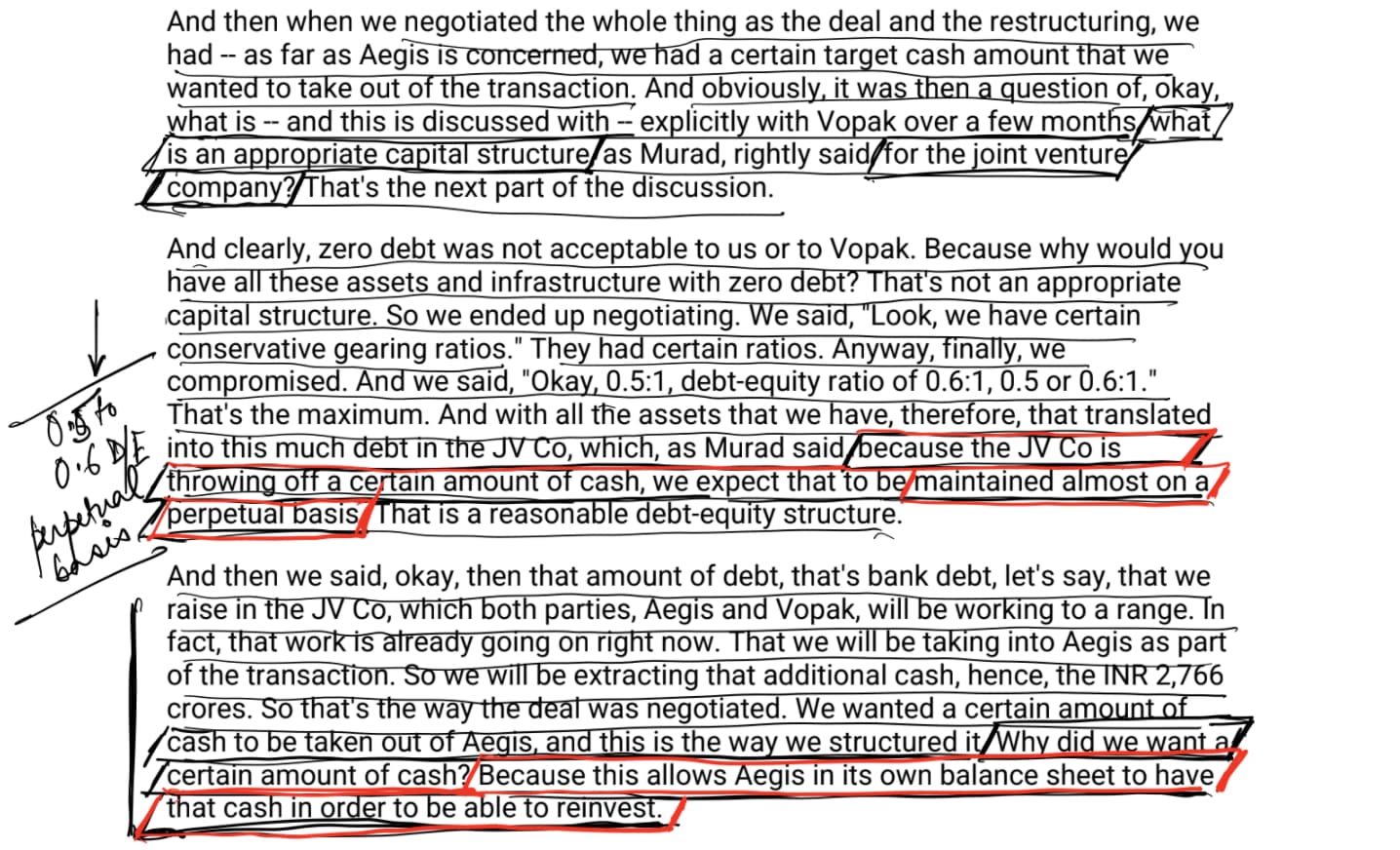

If we assume that Aegis-Vopak JV will carry out capex of 4000 Cr, which is on higher end of their guidance, given the debt equity is capped for JV at 0.6 as per deal, total equity requirement for the projects will be around 2500 Cr and rest 1500 Cr will be funded through debt. Since Aegis owns 51% of the JV, they will have to bring close to 1270 Crore as equity. Now, we must consider two things in mind.

If we take both these aspect into account, it is clear that JV it self may be able to fund significant part of equity requirement through internal cash flow reducing the need for JV partners to infuse equity. Even if we assume 250 Cr of free cash flow every year for 4 years (where we have not factored in much scale up in operations), net infusion from JV partners will come down to 1500 Crore and Aegis’s share will come down to 750 Crores.

This leaves Aegis with surplus cash of 1000-1500 Crore where there is not much clarity on deployment. Even if we assume that retained businesses of LPG distribution and Mumbai terminals will need growth capital, it has sufficient cash generation by themselves to meet that requirement considering steady state EBIDTA of 350 Crore. In fact considering that LPG distribution is a fairly asset light business, it may not need much capital for growth

Thus I feel as it stands today, there is not enough clarity on capital allocation of the money received. In general I have observed that whenever large amount of cash sits on balance sheet (which I think is a likely outcome based on the math above) it depresses RoEs and valuation both. I think this factor needs to be considered from medium term perspective.

Another point for my consideration was that even though Aegis mgmt has very good execution track record, they will undertake projects that are far larger and complex that what they have handled so far. Vopak does bring in the capability and expertise to execute such project but given Indian environment, it is important not to assume that all their plans will fructify as conceived and there may be delay/changes in the plans. Moreover, we still do not understand the contours of such large capex plans (and rightly so as it takes time for companies to firm up plan before putting up to investors) to give us more conviction/confidence on execution timeline.

Now coming to the more strategic part of the development: I feel if you are a very long term shareholder with time frame beyond 5 years, this deal brings in lot of positives. Vopak has proven capability in so many areas where creating capability from scratch would have taken years for Aegis. Some areas management mentioned such as industrial gas logistics, LNG, Hydrogen movement etc have very large potential. Considering that some of these areas are pretty nascent in India (like supply chain of industrial gases such as Ammonia, Butadiene etc) there exist white space to capitalize on the same. This also means, company can move to next level once they execute this plan. However, all this is a leap of faith as of now with very little understanding. We need to continue to gain better understanding on this and monitor this.

In my view, recent developments has brought in lot of uncertainty on outcomes in near to medium term while the growth visibility compared to pre-deal base has gone down. It is an evolving story now where we have to keep monitoring them on what kind of opportunities they capitalize on with specifics of that opportunity, how management responds to capital allocation challenge and how they execute far more complex and larger projects

Thanks Dhwanil for very relevant detailed nuances that you brought in.

I had a few simple observations to make - that may or not help to cut through the clutter

Deal structure - nobody likes it, was hard to digest given built-in expectations- BUT is a done deal. We cant do anything about it. Same comment about Valuations of Assets transferred to JV - Done deal.

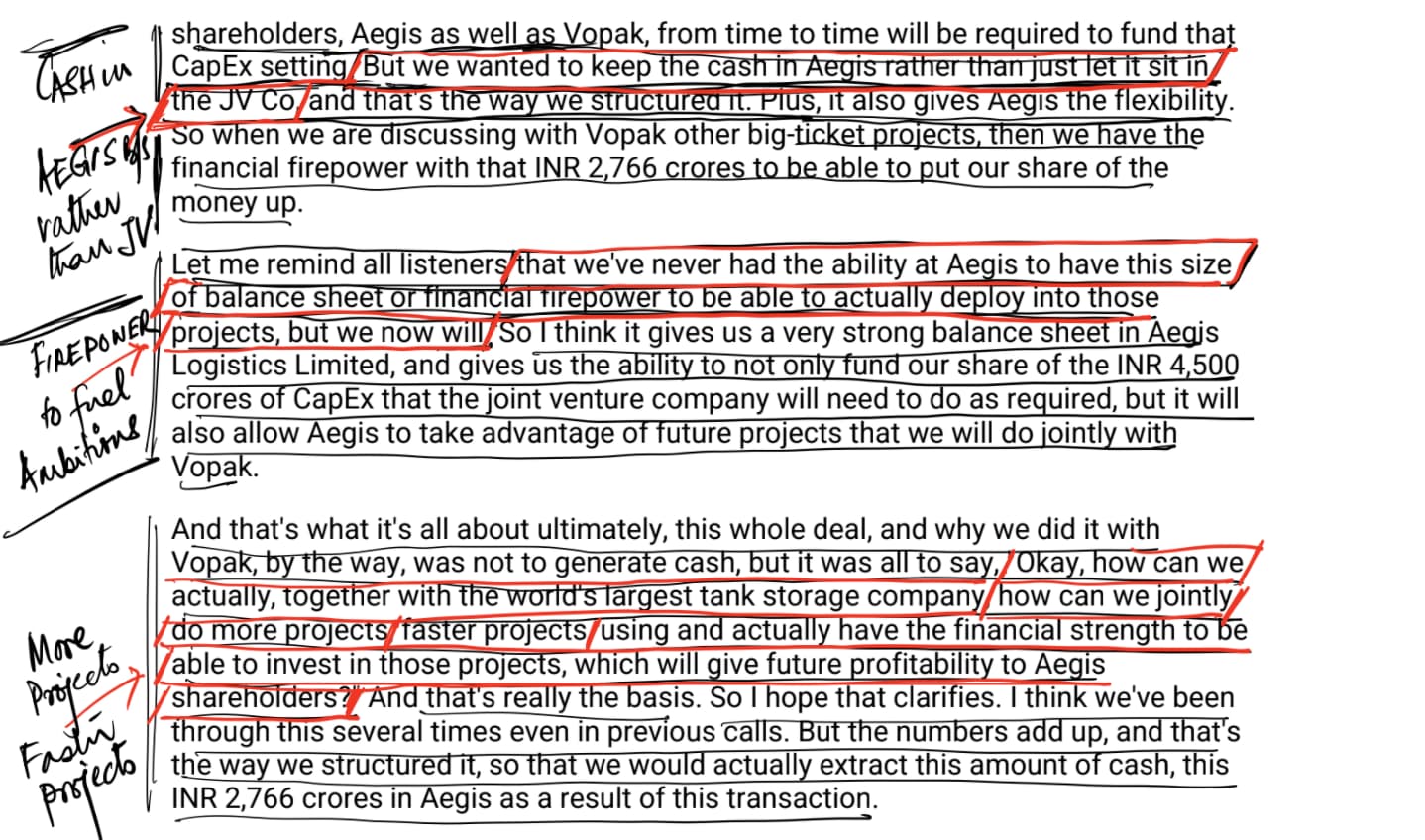

Now no one is unhappy that actually there is now huge Cash on Aegis BS - fuels their ambitions and enables them to do new larger projects and at a speed, that were unimaginable perhaps pre-deal. The moot point (fear) actually therefore is, CAN they re-invest this CASH at much higher profitability than pre-deal possibilities?

We as investors fear the worse - non-utilisation of large chunk of this CASH, de-worsification, richly valued-acquisitions, and more of such ROIC-depressing actions, right?

I actually derived great comfort that Management was very forthcoming and had cogent direct answers on Cash Utilisation prospects. Was talking only about accelerating growth and accelerating profits especially through already-identified newer larger LPG projects (the highest profitability driver currently), VLGC Jetty constructions - again that drives higher throughput for LPG Terminals, Industrial Terminals, Gantry connections in the like. And most importantly multiple projects at the same time - because with the excess CASH they don’t have to scramble to think first - how will we finance such a big projects, or so many projects at the same time?

Given Management focus, track record and ambitions I am happy that they have good cushion on excess Cash in the BS. That flexibility can be a very enabling Competitive Advantage in the hands of a Competent Management of accelerating the pace at which they can outdistance competition in India (even adjusting for ground realpolitiks)

Finally - when is it ever NOT a leap of faith? Even in a very strongly differentiated business like Aegis. Yes completed Capex in the bag (Kandla) was a great visibility booster. It still is. Excess CASH utilisation picture is what is making it less certain! That visibility will only improve/deteriorate as things unfold in the story in the next 2-3 years.

But then that is also the Opportunity??

One might get a business with some Cash-Utilisation uncertainty (different ROIC estimates) for next 2-3 years at different valuation levels. For anyone with a longer-term orientation, that works well? Yes, proof of the pudding will always be in the eating - we will NOT know, till we know!

Attaching some of the answers from Management on only these aspects with my Notes - as cited above - they might help clarify things a bit for some - especially the way Mgmt has articulated - no beating about the bush, straight from the hip, actually - that usually inspires confidence for me.

@Donald @desaidhwanil @vishalprasad Have very well covered the contours about the deal as well as its pros and cons. I will try to put in my thoughts and what changes in the thesis now:

Given whatever data we have in hand currently, I think these deal is expected to change the orbit of the company in long term. However, as we have seen, odds of even promoters with excellent past record post receipt of big money from selling of existing business has been pretty average, we need to see how Aegis promoters utilize these cash.

This is a long post. Already there has been significant work done in this thread. I wrote this to clear my head though i am still confused ![]()

First time I came across Aegis, I decided not to pursue because LPG had no future. I had seen some of the videos of Tony Seba and I knew that even if the timeline he has mentioned may not play out in India, but the story would play out eventually. There are people who want to change the Energy story. Whoever solves the problem will make significant money and hence a lot of interest in solving this problem. The more issue happens on the environmental front, the more money and brainpower will flow into new technologies.

In spite of all these, I thought let me study the business, if I find an anomaly I’ll invest else Aegis can become a good story to track disruption.

While as I had many issues, which outlined in the previous post, finally it boils down to can I figure out something, which can help me figure out if LPG is not going to go quickly and the possibilities of the JV. Numbers said Aegis is a wonderful business, with future if it pans out just based on capacity they have created then future is much better than today.

History of Aegis: It’s interesting

If I get a chance to ask only one question, my only focus would be on the trend of import volume of LPG. That will give some idea on the trend of incremental volume and if disruption is actually happening.

Questions I had in my Mind

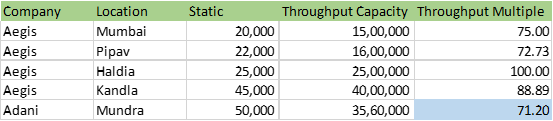

CAPEX Efficiency: I’ll just compare with Adani. Incentives of PSU is not the same as a private player. No point in comparing with them. I have avoided throughput is the parameter because with experience and with minor capex Adani can also improve the throughput sometime in the future. This comparison doesn’t show Aegis to be as efficient as it seems on paper. I could not find the Static capacity of Adani, Linkedin helped me.

Throughput: Adani is new and they are close. I understand Adani will have a lot of assumptions built in like pipeline and all but so does Aegis numbers.

EBITDA / MT or Revenue /MT for LPG handling Business: Once the terminal is in operation there is not much of a fixed cost. Do they have pricing power? Aegis says not much it is a fixed price. But look at the numbers. There is a continuous increase in Revenue/MT and any extra revenue flows directly to the bottom line.

Why they have been able to do this. As @desaidhwanil mentioned it’s the customer door price, which is important. Hint comes from HPCL shifting from Vizag to Haldia. There is significant saving for HPCL in terms of transportation and some part of it flows to Aegis (current hypothesis)

Now let’s look at how the revenue of different divisions is evolving. They don’t make much on the sourcing business so I have excluded so that focus is more on the important stuff. The data is roughly right (there could be some mistakes):

AutoGas: There is no increase in LPG Autogas stations in the last 10 years. In 2016 there were 960 CNG stations, in 4 years it became 3x. CNG is exploding. Ex: let’s take Bangalore, GAIL has given license to set up 100 CNG stations within 3 years to Confidence Petroleum and they are already working on 37. It’s costly to convert from LPG to CNG, so whoever is having the LPG shall keep on using it. With that kind of push, Auto LPG will have a tough ask to gain incremental volume. Aegis pace of expansion is also no much. The focus is more on how they can work with Essar to improve efficiency.

Commercial/ Retail : If there is a direct fight with CNG will LPG survive? In one of the calls, Aegis mentioned that LPG can only make good money if there is a 50% discount on Petrol and if it is 40% then profitability goes for a toss. But the competition is from CNG and not Petrol (I am keeping Electric out for the moment. I don’t have much handle on electric or alternate energy sources).

Even if somehow LPG price is at par with CNG, CNG is convenient and safe to use. For Commercial usage of CNG, there is no real state required to store LPG gas cylinder and risk of fire due to LPG cylinder on the campus.

If I look at what price does Aegis sells in the Domestic segment. What does show? Looks like they would not be able to convert the PSU customers as their pricing is higher and how many would like to go through the inconvenience of getting a higher-priced connection and going through PSU’s process of returning the connection. I have no handle on this but to me, it looks like people who cant afford to buy 14.2KG cylinder buy 2/4 kg refill and this gives Aegis good margin. What’s the size of this market - i don’t know.

Industrial: What happens if option of CNG is available? Hint is in 2011 AR

LPG usage in India : one way to look at how LPG consumption has changed over a period of time and what lies in the future (if there is no obsolesce risk). One way is to look at the number of household having LPG connection. As someone mentioned here in this thread, the data could be biased. Quality of data depends on the incentives and it could be grossly wrong. So I decided to remove biases and take hard data to analyze LPG consumption over the years.

If we breakdown the data, whenever there is government push the incremental volume, increases significantly but then it tapers off. The volume has been sustaining over last 6 years but slowly tapering off. While the LPG reach has improved significantly over the last 6 years, in the future this may not be able to sustain in terms of increase in penetration.

If we look closely LPG volume growth is more than per capita growth and that takes care of population increase.

Incremental Volume: When there is continuous volume growth there is space of many players. This is a market with few Logistics service providers and few customers. Whoever is able to capture the incremental growth can make a business out of it. Most of the terminal capacities has been created in partnership with the PSUs. It’s the incremental volume, which is easier to capture even so when you are providing better service at somewhat lower cost. There is a need for someone to capture this incremental volume and that is what Aegis has been doing over last 6 years. Let’s look at incremental volume growth and what Aegis has been able to capture. It could also be some customers moving from far-off port to nearby (before Haldia HPCL used to source from Vizag). It’s the final delivery cost that matters.

We notice that there is a sudden spike when new capacity comes. That’s going to happen with Kandla as well. As long as there is incremental volume is available it is easier to grow. But the question is how long this incremental volume will be available. All the low handing growth is gone and now the incremental volume is tapering off. We may not have the big bang 2015-2020 period in the future, as most of the household has at least got the connection now.

Forecast and Government Data : I am aware there is significant pipeline capacity is being created and there is rosy forecast being made by the government/PSU. The question is shall we trust it? First, it is forecast and second, it is from people who have the incentive of forecasting a bright future so that they can be in the business of creating capacity that may not be required. Disruption will not come from within, it’s going to come from outside so I will trade with care.

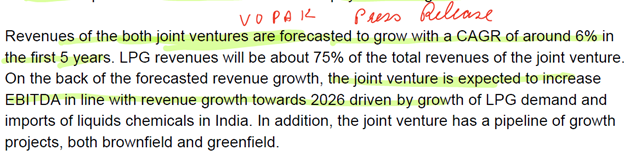

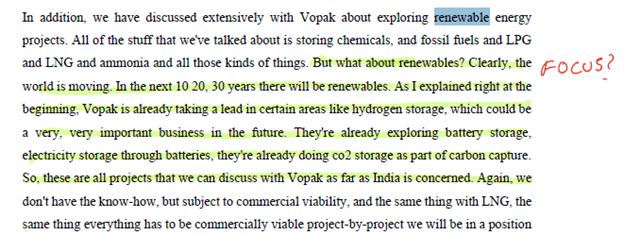

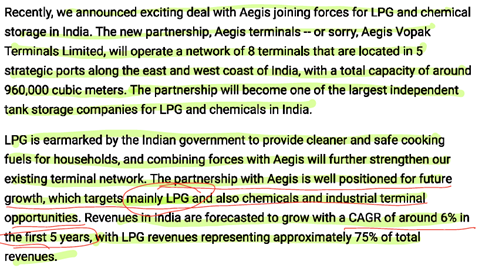

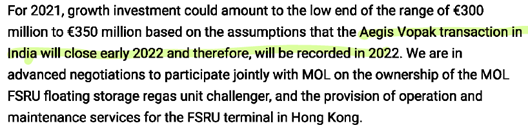

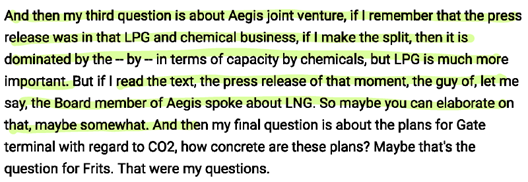

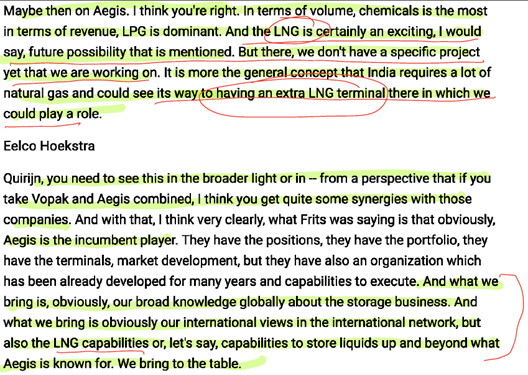

Interesting conversation During Vopak conference call:

Inference 1: By the time the transaction is closed, Kandla LPG would already be online. So revenue jump due to Kandla LPG already taken care of, the JV will grow 6% from there.

Inference 2: There is a lot of focus on LNG

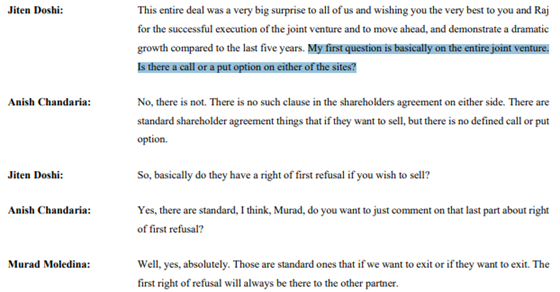

Call/Put Option : This is above my paygrade but this has been used by Aegis to move out of a business earlier and this was one question asked in the recent call.

Return on Capital: When we calculate this, we shall remove 292 as it was for land revaluation done for liquid business and 280 cr. which is Lease as part of Gross block. Gross block is not as huge as it seems ![]()

Future/ Risk:

Finally I ask myself – do I have some handle on the business? The answer is no since this is an evolving story where many things are possible. The range of outcomes has become large enough to discomfort me. To pin down on leavers of business has become difficult with JV acting as a spanner. Aegis has never done a CAPEX of scale that they are talking now.

Once Kandla plays out it becomes evolving story and it boils down to what the management wants.

Unless there is some disconfirming evidence, historically management has been focussed and nimble. What interests me is the JV about which I know nothing about. ![]()

@desaidhwanil @ankitgupta @Rokrdude Would you know if the PSU terminals work round the clock? I remember Aegis telling in one of the calls that now they have 24x7 capability. The answer to this quesiton may through some light on lower throughput being achieved by PSUs.