I misssed the concal …but .it sounds super bullish…thanks for sharing.

Hello all! Sorry I’m a little late to this party. Been going through the AR’s, financials etc. Looks promising. Haven’t seen an unqualified guidance of 25% CAGR in the current low growth environment Anyways, I had a few questions which i believe are the crux of understanding this story.

-

The current addressable market for Take is $6 Billion worldwide ($15 B if taking into account new capabilities -pharmacovigilance for biosimillars, stem cell and many others) acquired by TAKE. this is expected to grow to $30 B by 2020. So if the current opportunity size for Take is $6 Billion, and they have 9 of the top 10 Pharma companies world wide (read: Amgen, BMS, Roche etc) & most Indian companies, big Euro companies (Bayer), why is Take struggling to scrape a measly $100 odd million is sales? What is lacking in their product offering? How do they plan to plug that gap and by when? I understand the Human resource constraint, but that;s not the answer.

-

As mentioned earlier Take is guiding that the industry worldwide will grow from $15 B to $30 B by 2019, 2020. A $15 Billion addition, and TAKE is guiding that their revenues will grow 25 % CAGR from $100 ish million to $ 250 Million by 2019. So out of the incremental $ 15 billion opportunity coming up in the next few years, these guys want to try and capture $ 150 Million? Why are they aiming so low, aspiring for just 0.7% of the total addressable market share?

-

I am given to understand that the key bottle neck to their growth is the lack of skilled manpower. “TALL” is a great initiative to address this challenge, but if they plan to churn out just a 100 people a year aren’t they missing the bus in terms of the opportunity size? Why on earth would they start of with a 100, when they have a huge deficit of skilled people (main reason for EA acquisition - knowledge &people) Do these guys have a true growth mindset?

-

I think this question may indirectly answer the above questions, but still putting it out here to understand better - The CEO has no skin in the game! No shareholding, no ESOPs!! What incentive does he have? A fixed and variable salary? If he s so upbeat about the future prospects of the industry & company, why has he not invested ? Can someone please throw some light on his incentive schemes? I missed that in the AR. Is this why, there seems to be no fire to capture the monumental $15 B opportunity but settle for $150 MM? He & Ram have no incentive to!

-

We need to get a more qualitative understanding of the industry. I think Raj Panda & Vishnu have contributed greatly to this discussion, my only question is - Can this be a winner takes all market? I understand that there is consulting and other services tied into the entire life cycle (where Cognizant is clearly way way stronger, $1B practice) so if a Metadata comes out with a for the lack of a better term a “kickass” new end to end tech platform for lifecycle management (very probable as they spend 25% of rev on R&D, while Take a mere 7% that to on a base of $100 Million) why won’t everyone shift to Metadata? It is extremely scalable if sold on a licensing basis. This could be like the ERP market, just two players SAP and oracle. So is this a winner takes all market? If so, I don’t think Take has a chance competing with the big boys.

-

I think the key to truly understanding this company is evaluating their intangibles - their patents & IP. The Balance sheet is clearly the worst way of doing that. Because ultimately their IP is going to drive the numbers going forward. I would love to get a better understanding of this, could anyone throw some light on the best way to do this? I guess we could all collectively try and understand this beast, pooling in each of our skill sets.

I think this is a really interesting company, I am still digging and trying to understand this, therefore not yet invested.

3 Likes

First off, thanks for posting a counter-view to debate against in a constructive manner and help us in figuring out chinks in our investment rationale.

Like u, i too am still digging to find out any contarian perspectives which to negate the investment rationale, even though i am invested and have very high conviction on the company’s potential.

Final word of caution before i state my views, is that i am most likely heavily biased.

There are 2 templates against which one can analyse TSL.

- Quintiles - CRO with a good data analytics platform (Infosario).

- Medidata - Clinical Trial Delivery solutions (Rave, Clinical Cloud, ePRO, mHealth).

Both are successful in their own niches but with very different business models. And TSL’s business model had very little in common with either of above 2 prior to EA acquisition.

TSL primary focus in Life-sciences is Regulatory Compliance as stated multiple times by the mgmt, with their flagship PharmaReady Suite catering to different stages of regulatory compliance. It would be safe to assume that majority of their life-science segment revenue is coming from either the application suite or Consultancy(Medical Writing/Data Validation).

While they do have bio-statisticians and presence in Clinical Data Standards and Safety segments, they are primarily accelerators or as 3rd-party System Integrator as in case of Oracle Argus implementations for Drug Safety requirements of the customers.

This $15 Bn USD opportunity while true and corroborated by multiple sources is only half the story. As most of us know, the longest and most expensive phases of in drug discovery lifecycle is the Phase I-IV clinical trials phase. Thus, by extension CRO which actually perform Clinical Trials like Quintiles and Ecron Acunova stand to gain the major portion of this outsourcing pie.

Regulatory compliance while being important becomes critical post the trial phase (i.e. typically 10-12 yrs into the life cycle) and hence would not be a significant expense in the large scheme of things. Sure, the clinical data from each of the clinical trial phases would need to be updated to the different modules of the eCTD, but that is most likely a small effort compared to the heavy duty lifting actually done by CRO’s like Quintiles.

So, having Big Pharma clientele is not necessarily a good thing in terms of faster revenue recognition. There would be milestone payments, say at end of each clinical phase but major chunk would be recognized after the regulatory submissions.

In that context, having more Generic companies will be a big plus given that they file at least 1 ANDA and/or DMF per quarter.

Medidata on the other hand is primarily a technology solutions company whose primary focus is on Clinical Trial Delivery which as explained above is the most expensive and thus lucrative space for a tech vendor. So, their platform provides solutions related to Clinical Trial Management, Electronic Data Capture, Patient Management (eCRF, EHR, EMR) and so on…

Medidata Product Portfolio: https://www.mdsol.com/sites/default/files/MCC_Medidata-Clinical-Cloud_20150217_Medidata_Fact-Sheet.pdf

IMHO, TSL cannot compete with Medidata(see below for reasons) on Clinical Platforms and hence with their EA acquisition gives me an impression that that they may be following the Quintiles Template.

Navitas v/s Medidata

_http://investor.mdsol.com/releasedetail.cfm?ReleaseID=954211_

* Record full-year revenue of $392.5 million, a 17% year-over-year increase

* Provides 2016 revenue guidance of between $450 and $474 million

* Medidata added a record 201 new clients in 2015, an increase of 52% over 2014, including 59 new clients in the fourth quarter. Medidata’s client base grew to 611 by the end of the year, up 26% from the end of 2014.

* Medidata’s Contract Research Organization (CRO) program continued to expand in 2015 with 18 new partners joining. Medidata’s CRO partners now total over 90.

* Medidata’s overall revenue retention rate for the full year was 99%. The retention rate for all Medidata’s large enterprise customers over the past several years was 100%.

Medidata was started in 1999, five years before TSL and their focus was on the much more lucrative clinical trial delivery segment. Based on your assertions they seem to have not done so well either.

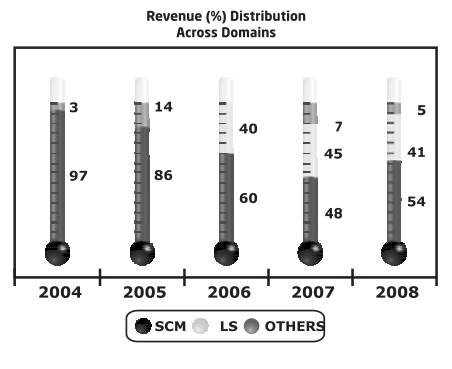

TSL on the other hand started out mainly as an SCM domain company and later got into Life-sciences in 2004, but they had captured a good rep pretty quickly and self-evidently as captured below and posted very good growth despite recession.

And considering that their focus was on an unmet need (CTD/eCTD) where the revenue recognition takes longer, the growth has been impressive.

So all things considered, TSL acquisition of EA is a game-changer and now can legitimately aspire to capturing the $30 billion USD pie. I am happy with a 25% CAGR and it will take time, but mgmt has shown they are capable enough and have good pedigree.

IMHO, prior to the EA acquisition i don’t think there was any functionality lacking in their offerings given their target segments. As an Life-sciences functional solutions provider, they covered the necessary areas in terms of technology -

- Regulatory Information Management: PharmaReady Suite

- Clinical Data: SAS, Bio-statisticians, Trial Planning, Trial Management, Data Standardization, etc.

- Drug Safety and Pharmacovigilance

I think what was lacking was their viability to be selected as a vendor for managing clinical trials as they were not a CRO (before EA)

Say, if you are a Big Pharma co. and u have a choice to select a vendor for doing a clinical trial between -

- CRO like Quintiles

- CRO using Medidata platform

- TSL + CRO (with no CTMS or Analytical Platform)

It most likely ends up between options 1 or 2.

If Navitas+EA follow the Quintiles template, then they could take it to the next level given the complimentary capabilities they bring together, the low-cost pricing by having trials in India, and hopefully much more conducive regulatory environment.

What are the gaps for the future?

- RBM: Risk Based Monitoring which requires emphasis on real-time data for drug safety during and post clinical trials.

RBM Infographic a better approach to risk based monitoring.pdf (105.2 KB) - EDC + EHR/EMR: Patient focus to help create data repositories for faster and more efficient recruitment (This is a differentiating factor for Quintiles to win customers confidence)

Positive triggers:

- Mandatory eCTD submission from May 2017

The Electronic Common Technical Document (eCTD) is CDER/CBER’s standard format for electronic regulatory submissions. Beginning May 5, 2017 submission types NDA, ANDA, BLA and Master Files must be submitted in eCTD format. Commercial IND submissions must be submitted in eCTD format beginning May 5, 2018. Submissions that do not adhere to the requirements stated in the eCTD Guidance will be subject to rejection.

- Much more favorable regulatory environment for clinical trials in India.

As explained above, Medidata would not consider Regulatory Compliance as lucrative as Clinical Trial Delivery solutions.

While CRO’s such as Quintiles do support Regulatory submissions, they primarily use Medical Writers or Consultants. In fact Quintiles is a customer of Navitas.

You would find the same situation with the IT biggies such as Cognizant, Infosys, etc. They have professional writers to help validate/make the submissions.

They do not have an application suite/platform like PharmaReady dedicated to Regulatory compliance.

Hence, it is not a “Winner takes all” market. There is room and niche for each of the players to grow comfortably.

As it was much publicized, they had taken a conscious decision to let go the low-margin SCM customers and focus on higher margin Life-sciences segment.

Two things which stand out:

- “Capacity to Suffer”: Willingness to take short-term pain and report lower numbers.

- Capital Allocation: Recognize the higher growth opportunity and traverse the path accordingly.

If nothing else, the Shriram Group connection gives them that benefit of doubt (not that i need any convincing)

On Management Ethos - Shriram Group Connection - Where they are coming from?

The Trust

In November 2006, Thyagarajan did something that he always wanted to do. He made good his promise of sharing his wealth with his management team who had contributed to the group’s growth. He floated a trust to govern the holding company, Shriram Capital, which houses the promoter’s shareholding. Through the trust, 75 per cent of the promoter’s holding would be transferred to the management team upon their retirement, thereby making them owners of the group.

Thyagarajan himself will get only 2 per cent along with others in top rung. The remaining 25 per cent, currently valued at Rs 500 crore, has been reserved for entrepreneurship development.

S. Abhaya Kumar (also Founder of Shasun Pharma), Vice Chairman, LifeCell International (56), was both excited and worried. He was excited because TRIcell, a company that he recently floated to do clinical research and trials on the therapeutic usage of stem cells, was an excellent business proposition. But with the world just about getting to know about stem cell research and the typical long drawn process of clinical researches, funding the project was proving to be difficult.

He approached the Shriram Group, whose Founder-Chairman R. Thyagarajan readily agreed to take 20 per cent stake and fund Rs 7 crore. “As a partner, the Shriram Group never interferes in the running of the organisation. It offers valuable inputs on regulations, taxes, governance and on anything we ask,” Kumar says. Manipal Accunova, a contract research organisation and a leading player in biotechnology and the clinical structure space, also has a similar story to tell.

For instance, H.R. Srinivasan, currently planning the group’s foray into infrastructure development, headed Sembawong Shriram, a joint venture company in the logistics field in 2001. He expressed a desire to be on his own after the Shriram Group exited the JV. He decided to foray into the IT product space with funding from the group. Today, the company, Take Solutions, which is into life science products and supply chain management products, with many intellectual properties in its name, is seeing better returns than most other IT product companies. Srinivasan has since handed over the reins to others and re-joined the group.

Is the promoter following in his mentor’s footsteps?

Take for instance, H R Srinivasan, the MD of Take Solutions. He has built a Rs 800-crore software products company in 12 years and is now giving back his support to innovative ideas. He has funded over 10 startups and has already infused $500,000 in just ideas. “My job is to support ideas and not trouble them over success,” says Srinivasan. He adds that the best way to build a startup ecosystem is to fund ideas that can have an impact on businesses and consumers alike. His portfolio companies include InnoWatt, a smart energy firm, research organisation Solaris Pharma and Spectrum Medics, a data analytics platform, among others.

http://www.grantthornton.in/en/news-centre/risk-capital-the-new-favourite-asset-class/

Above report seems to suggest so. Though one needs to validate if the investments are in a personal capacity or not?

http://www.thechennaiangels.com/srinivasan-h-r/

Couple of additional points:

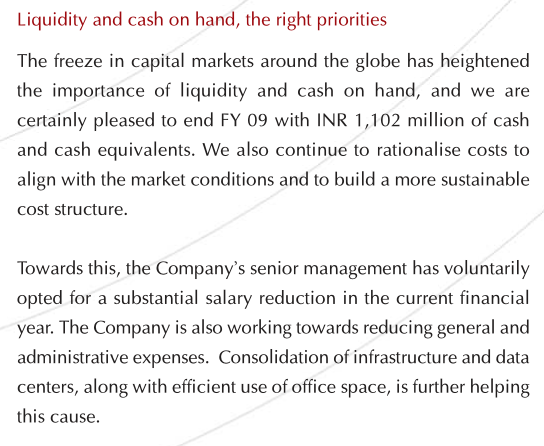

- Based on AR 09, management had taken a voluntary pay-cut.

- Admirable humanitarian services provided during recent Chennai floods and providing additional financial assistance for rehabilitation.

The shareholding is along the similar lines explained in the Shriram Group article above, which is through a trust/holding companies.

IMHO, their incentives are good enough for me.

Mgmt had stopped giving Product Licence/AMC revenue contributions in recent AR’s unlike during AR 07-09.

Also, below point highlights that domain expertise and SME’s play a more vital role.

I think u may have missed reading the Quintiles presentation which i had shared in earlier post.

Quintiles PPT

Do visit their official site and watch the below links to have a feel about the role of technology and data is playing to enhance clinical trial delivery.

http://www.quintiles.com/library/videos/the-data-driven-difference

http://www.quintiles.com/library/videos/quintiles-leaders-discuss-new-infosario-one-mobile-app

Since u made me put in this much of effort ![]() I have earned the right to give a friendly bit of advice.

I have earned the right to give a friendly bit of advice.

The way u had framed ur query in Point 2 could be construed as condescending. I hope u will be more circumspect with ur queries in future.

Regards,

Vishnu

19 Likes

Hi Vishnu,

Incredible reply, thanks for taking the time and effort, In the process of conducting some more research to carry forward this discussion. Thanks again for the effort.

About the tone in point 2 that I raised, I’m sorry it came off as condescending, that was clearly not my intent. The disconnect between the addressable market size and management aspirations completely baffled me. Point well taken though, I have edited the same.

Detailed response to your points to follow through shortly.

Rohit

2 Likes

Thanks ravi.

Very well captured concall. I listened to it and u seem to have done a great job in capturing it.

Vishnu, you take in depth digging to the next level. Thanks for the same.

I have been following the company since a long time. The one thing I like is that management is walking the talk. In his TV interview some time back he was talking about company’s transformation and growth prospects and most of these things are now playing out.

disc: re invested recently post q3 results having exited earlier during the run up.

Earlier it was an undervalued trading bet. I now start feeling it could be company that needs to be watched for longer term. How it integrates the EA acquisition and gains from it needs to be seen.

8 Likes

Thanks Hitesh Bhai for the compliments.

You have been an inspiration for all and what i have appreciated in the past 3 yrs since i joined VP has been that u drop little bits of wisdom through your posts which if one analyses, you are providing a glimpse of the breadth and depth of your mental model toolkit.

Like how one gets new insights on re-reading classics, i am sure most of us get the same feeling when we peruse all your posts from the past.

If I can attain 1/10th of the wisdom from humble folks like you, Ayush or Donald, i would consider it a pretty good achievement.

But coming back to Take, i would like to add a word of caution for fellow VP members and not get mesmerized the by the data deluge of the earlier posts.

There is a fair degree of uncertainty with respect to the stock story.

- Mixed performance with Acquisitions. One cannot predict how EA acquisition will turn out. I am in wait and watch mode.

- I have invested with a very long term view where i expect the real upside to be triggered from FY18.

- Having said above, when i would review the story post H1FY17 and if it has not played out as per my expectations, due to mgmt dropping the ball then i would not hesitate to book out of my position.

Point is, one needs to keep track of the business and not be in it with a buy and forget expectation.

Disc: Had added again after Q3 results @128 levels.

8 Likes

@crazymama - Firstly, appreciate your detailed write-up. I just read through the entire thread. In your below comparison on Navitas vs Medidata - You are using dollar revenues for Medidata vs Rupee #s for Navitas

As rupee has depreciated in this period, the topline growth here is more due to rupee depreciation rather than $ growth. We must dig why topline growth has remained stagnant.

Have a look at the table in post # 50 by @rohitbalakrish_ .

Thanks,

Ravi S

2 Likes

Thanks Ravi for pointing out the relevant info.

I should have made the adjustments or atleast referred to Rohit’s post, which i missed to recall.

Anyways, the takeaway from the Sales in USD terms reiterates my initial view point that regulatory compliance is not as lucrative as Clinical Trial Delivery.

i came across the follow ppt from FDA.

http://www.fda.gov/downloads/Drugs/DevelopmentApprovalProcess/SmallBusinessAssistance/UCM445612.pdf

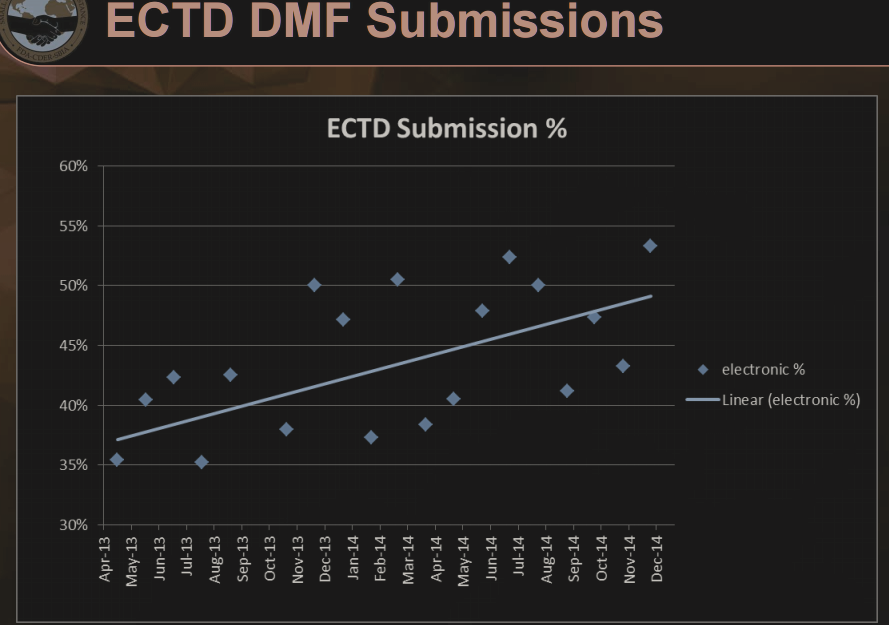

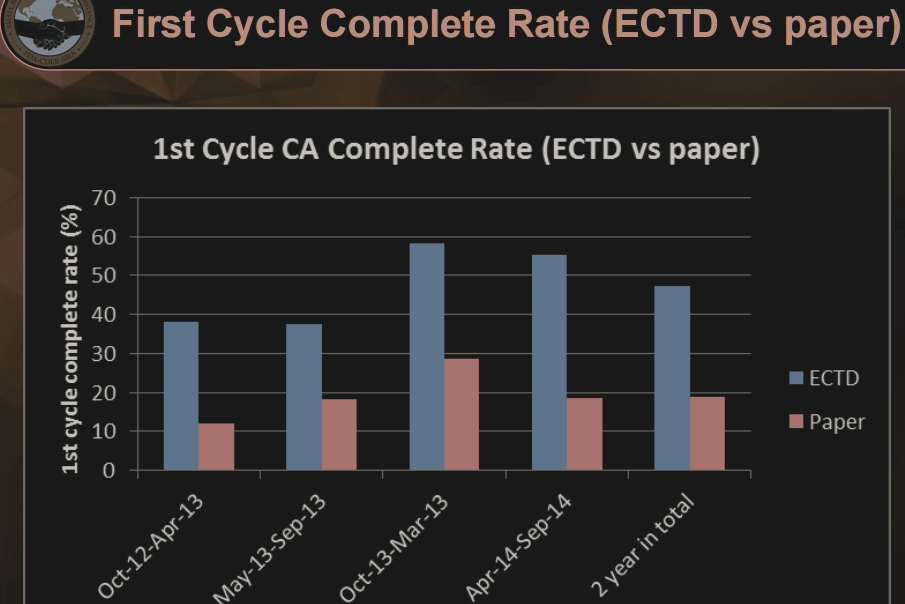

As of 2014, eCTD was still below 50% in terms of usage and additionally chances of 1st cycle approval was much higher for eCTD v/s paper.

Even assuming that eCTD has increased to 60-65%, there is still scope for gaining new customers before the May 2017 deadline.

With respect to the stagnant growth in topline, possible theory/explanation is that -

-

there was a huge backlog from the filings before GDUFA (2012) which had to be cleared before coming to the new ANDA filings which had actually increased post GDUFA beyond FDA’s initial estimates. (Based on the assumption that ANDA/DMF make a high portion of the regulatory compliance revenues)

-

It was only recently that the entire filing backlog has been cleared, and a filer can now be guaranteed to have the acceptance/RTR within 30 days.

-

Terms of payment: When does TAKE get paid.

Is it immediately after the filing?

Or after the filing has been accepted by FDA for review?

Are their penalties for a Refuse-To-Receive?

Will keep digging further.

1 Like

P/E OF 125 IS VERY HIGH FOR FRESH INVESTOR

Its a fv 1 rs. Share

Please have a look at consolidated number as standalone numbers have no meaning for Take. It’s 80% revenue comes from subsidiary Navitas which is not reflected in standalone numbers.

Regards,

Raj

1 Like

Consolidated is around 8.0 EPS…SO ITS around 18 pe…thanks for enlightening

One needs to deduct non-recurring earning in Q1 to arrive at true PE. anyway look at forward PE rather than trailing one

Delivery rate to total trade is just 10%

Can it be treated as red flag??

Waiting to break the range of 140 to 157 with volumes on closing basis

Found the following 2 posts about eCTD clarifcation issues between FDA and Industry.

This could be seen as positive/negative depending on which angle one looks at.

The Goals Letter is replete with language about the electronic submissions and the fact that GDUFA goal dates will not be assigned unless the submission (ANDA or DMF) is in the electronic format specified by FDA at the time of submission. Exact phrases from the Goals Letter include:

- Review metric goals (described below) only apply to submissions made electronically, following the eCTD format in effect at the date of submission.

- Backlog review metric goals (described below) apply to all ANDA applications, amendments, and supplements regardless of current review status in the queue as of October 1, 2012, regardless of whether they were submitted in paper, electronic, or hybrid format.

- For Abbreviated New Drug Applications (ANDAs) in the year 5 cohort, FDA will review and act on 90 percent of complete electronic ANDAs within 10 months after the date of submission. (emphasis added) Certain amended applications may have differing metrics as discussed below.

- Electronic– refers to submissions in an all electronic eCTD format in effect at the date of submission.

Apparently FDA’s definition of “all electronic eCTD” and “complete electronic” ANDAs/DMFs may be more stringent than ever envisioned by industry. It appears that any deviation from the eCTD format, whether it is one page or fifty, whether there is one broken link, or lack of a detailed table of contents for each major section will result in a notice of deficiency, and if you fail to correct the problem within 7 days, then, while your ANDA may be filed (because the requirement for complete electronic ANDAs does not officially kick in until May 5, 2017) FDA will not assign a goal date, because we assume FDA has made a determination that the submission is not “all electronic” or “complete” and does, therefore, not qualify as a “submission made electronically following the eCTD format in effect at the date of submission”. One firm reported that as there were 2 pages in one report that “did not meet the FDA standards”, their application got filed, but no goal date was assigned. When the issue was elevated to senior OGD management, the response was that even if there is one data point that cannot be readily read by FDA or if even a single page was not fully legible, that the Filling Review group would refer this to the Policy Group for a decision. The Policy Group has determined that they need to treat all applicants in the same manner. Thus, if there are any errors, you can expect the same result.

Response from FDA

The reason most people we talked to were upset is that this came out of left field without any warning, notice, or acknowledgement of a policy change.

OGD was obviously surprised that industry was surprised by their actions. In discussions with OGD senior management, I expressed what I felt was the real reason for industry’s concern and that was OGD implemented what appeared to be a new policy to treat ANDAs that had unresolved eCTD issues

It should be noted that FDA has been up front that a paper submission or hybrid submission would not receive a GDUFA goal date and industry had always been aware of that fact.

The question then is what is the definition of an electronic submission?

OGD provided the following rationale to me in our discussions:

- In all instances industry is given time (7 days) to correct the eCTD issues. If they or their contractor cannot meet that timeframe, then we must take some action and that action must be consistent among applicants.

- If there are problems, such as illegible pages, then it is not possible to fully review the ANDA and those items need to be fixed before the ANDA is accepted for review. If they are not fixed in time, then no GDUFA goal date will be assigned.

- The individual made an interesting point that even if an ANDA had come in when I was at OGD (when dinosaurs walked the face of the earth) where some of the pages of the application were in a foreign language, we would have refused it. (While that is correct, we would have refused-to-receive it. However, there is a regulatory provision in the ANDA refuse-to-receive provisions that address this specific issue see 21 CFR 314.101(d)(5)). In addition, we were not collecting over $300 million dollars in fees back in the day.)

- FDA also addressed another interesting point related to the level of quality control that the sponsor employs in review of the ANDA submission prior to sending it to FDA. These are the types of issues that should be caught prior to pushing the send button on the FDA gateway. Sponsors need to do a better job of QC on their submissions. (Hard to argue with that, but sometimes the problems are not evident to the sponsor – my observation was met by OGD saying if the problem is caused by the system, then OGD is willing to speak to the applicant to resolve the issue.)

- What about the fee issue if the 7-day deadline can’t be met?

The reply was, well, that is an issue that is out of FDA control and there should be a better relationship between the sponsor and any contractor to assure that a quality electronic submission is developed, or if it happens to be a bioequivalence report, that the CRO should be held responsible for assuring the quality of the report. But ultimately, it is the sponsor’s responsibility to ensure the quality of the submission. FDA noted if the time period for correction cannot be met, the sponsor could always withdraw the submission and resubmit, and will then be able to be assigned a GDUFA goal date, if the ANDA is received.

- As to the issue of the implementation without notice to the industry, FDA noted that perhaps they should have done a better job of disseminating this policy, but we had to do something and the only way we could implement the program was to treat everyone (big and small firms) the same.

In my personal opinion, i think FDA does a thankless job and they do the best they can given the constraints (resources, political wrangling with Congressional Hearings, etc).

With respect to Navitas, i think it is a positive trigger for companies to shift to eCTD even sooner and as pointed out by FDA, ensure they have proper QC processes (PharmaReady) in place to avoid these issues.

At the same time, the 7 day rectification period while challenging should be addressed much more easily by a “Regulatory Compliance Platform” than by Regulatory Process Outsourcing Consultants (Medical Writers) assuming the average fix job is more than just a page. ![]()

Would be interesting to know management’s views on this in next concall.

Disc: Invested. Not traded in last 30 days. Views may be biased.

Visit the source links for complete details and author views.

2 Likes

Hi, can somebody pls provide the Concall transcript / link. I searched the company website / RB, but its not there.

Thanks.

@crazymama Hi Vishnu, this is too basic to ask, but request you to answer if possible. Also correct my understanding, if wrong.

Consider this:

- In conventional way, the Take Solutions people will visit the client’s site, install their applications (eCTD/PharmaReady) and client starts using the same.

- With advancement of Cloud computing, Take Solutions will already have everything ready on Cloud. They can offer their applications to any client subject to availability of internet and charge for the usage (instead of selling the License) . They will basically provide their software as a service (SAAS), right?.

Asking this question as I am not sure if Take Solutions is working on/with Cloud platform.

Hello Advait,

No soft copy transcripts are available. ReasearchBytes has the audio though.

Both ur queries are answered at the below link:

Their eCTD suite is available as both Cloud and On-Premise model.

My perception is that most of their clients would be using the below model:

In earlier posts, eCTD video was shared which shows there are 5 different modules which require different datasets based on clinical, non-clinical, bio-equivalence, etc…

As i understand, there is an initial evaluation phase wherein the client provides the unstructured/structured data from their existing systems for Navitas to plug into their platform, process and generate the compliant eCTD document.

Having said that, compared to innovators, Generic companies would prefer to buy the license/subscription to the platform given the high frequency of filings through DMF/ANDA.

Innovators while filing less frequently through IND’s/NDA’s will require more complex eCTD submissions given the amount of data involved throughout the clinical phases.

In CY2015, 799 commercial IND’s were filed.

http://www.fda.gov/downloads/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/DrugandBiologicApprovalReports/INDActivityReports/UCM485375.pdf

Having the eCTD platform alone is not enough. It needs to be backed by a solid base of SME and domain experts which Navitas has claimed to have.

Do go through the case studies at the pharmaready portal.

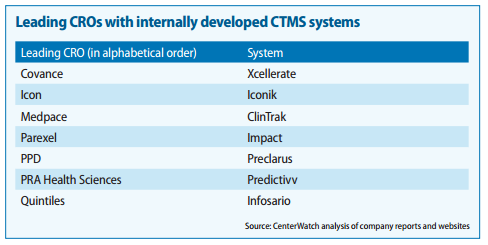

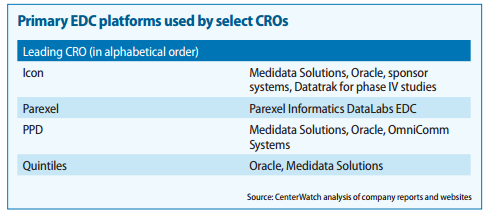

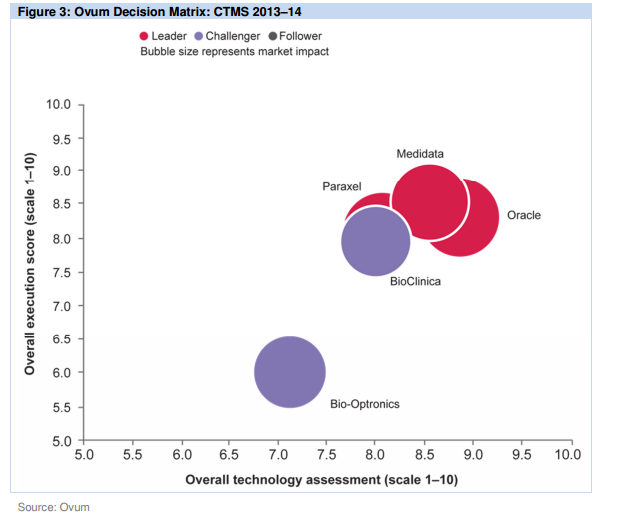

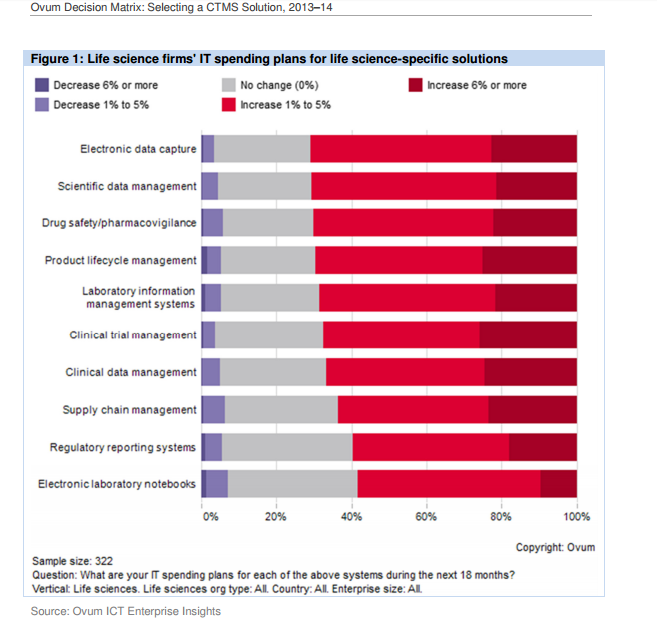

Also found couple of very good report on the CTMS players and competitiion:

https://www.mdsol.com/sites/default/files/Rave_CenterWatch_CROs-Juggle-Proprietary-Systems_20160301_Article.pdf

http://www.oracle.com/us/corporate/analystreports/ovum-odm-ctms-2241838.pdf

The last 2 slides show that more than Regulatory Compliance/Management, eClinical solutions such as EDC, CDMS, CTMS, eTMF, etc… are higher priorities.

Also, Navitas had mentioned in AR 2014 that they would like to create accelerators for Oracle CTMS (ClearTrial) similar to their Argus implementations. (Would need to follow up with mgmt)

3 Likes

Latest report on Take Solutions from Karvy - https://www.karvyonline.com/viewdocument.aspx?DocumentID=12439

Disclosure: Invested

I am sorry for not adding any value but who else is a buyer at this price? I have bought substantial amount of Take solution for my portfolio today. It forms 15% of my portfolio at avg price of 130.

Only thing I have to add is that for an investor it is a wonderful opportunity to buy a good company which is sidelined because of the market Euphoria.