**Take Solutions ltd**

"TAKE "with its global headquarters in Chennai, India and U.S. headquarters in Princeton, New Jersey , is a globally recognized domain focused technology services provider with expertise in the NICHE domains it operations in, specifically Life Sciences (LS) and Supply Chain Management (SCM). As outlined last year, TAKE studied current and emergent market trends. On the strength of the considerable intelligence gathered, TAKE made the strategic decision of limiting its SCM activities to profitable segments only, while capitalizing on the growth potential of the NICHE high margin LS(LIFE SCIENCES) industry. While the total revenue for the year was INR 7,387 million, a 10.1% decline over FY 2014 due to a divestment in the low margin SCM business, the Net Profit for the period registered a 20.5% increase over the last year at INR 699 million with Q4 FY15 being TAKE’s best quarter yet. Now TAKE focusing only on high margin NICHE businesses only which can deliver higher EBITDA & can take the company to new heights in coming years as seems in the attached financial data-:

Take Data.xls (9.7 KB)

take_solutions_annual-report_2015.pdf (2.1 MB)

Disclosure-: invested

1 Like

Hi Akaash,

Based on past numbers and focus on high margin business, the company looks good. I will dig deeper into it. In the meantime, could you please throw some light on competitor analysis, market size, placement of TAKE in the domestic markets, etc. Thanks a ton in advance.

@akaashbansal - The attached excel does not work as it may be linked to another file.

Why is take paying low taxes?

I see that they are paying taxes at rates less than 7-8%.

I couldn’t find any notes or details on the low taxation in AR . Take is located on the shriram SEZ perungulathur near chennai. The SEZ must be providing tax holiday, not sure about the duration available in Takes case.

Sundaram mutual fund lift 1.56% stake in Take Solutions Ltd.BSE Announcement on 13.10.2015

Ecron Acunova has a team size of 313.

As per last data on Ecron Acunova site, out of total of 265 professionals there were 47 MD’s and PhD’s.

Acquired company had FY15 revenue of 134 cr. EBITDA of around 10%.

Steady state margins are 12%, 10% in FY15 due to some one off expense.

Take plans to improve the margins of the acquired company. Take was guiding for 24% steady state EBITDA margins by FY17 (before this acquisition)

Disc: Invested

7 Likes

Was under the impression that a player like Infosys would have it’s in house capabilities in the clinical data management space but then came across this on their site. Seems they were have a partnership with Ecron Acunova for it. This gives me some comfort on the capabilities of Ecron.

7 Likes

Yup, heard the last 2 concalls. Mgmt. seemed very optimistic.

However, to understand if the optimism is well placed, we should study more on industry from various sources/perspectives to get a well rounded view.

If you come across anything please share.

On the EBITDA front, yes we should see subdued margins for next few quarters or probably a year or 2.

It takes time to integrate a acquisition.

As highlighted by Admin and moderators please refrain from saying things such as "It may become a 5 Bagger in next 5 years from these levels."

That may cause naive investors to invest without understanding much on business/industry and that’s not what we are trying to achieve at VP.

Concentrate more on providing facts and information about company/industry/competitors etc.

If you have worked on revenue/EBITDA/PAT estimates for next few years, that would be great to share i think.

6 Likes

hi All,

Please also check Cognizant as it has more than 1B $ plus practice and is going very strong in this area.

It has acquired two companies last year ( Trizetto and healthnet).

It has hired lot of doctors/Phd’s in ths practice.

We should just check this to do the competitor comparison

Thanks

Saurabh

Congnizant healthcare practice seems to be big, contributing almost 1/3rd of their revenue.

Trying to study more about their abilities in clinical data management and drug safety field which would be a more like to like comparison with take sol.

Healthnet was acquired by Centene and not congnizant http://marketrealist.com/2015/07/centene-announces-acquisition-health-net/

On Trizettto

Congnizant’s press release says http://news.cognizant.com/2014-11-20-Cognizant-Completes-Acquisition-of-TriZetto-Creating-a-Fully-Integrated-Healthcare-Technology-and-Operations-Leader

“TriZetto software manages the health benefits of close to half the insured population of the U.S. and supports about a quarter of all U.S. care providers. The company is now a part of Cognizant’s healthcare practice whose clients include 16 of the top 20 U.S. health plans, and four of the top five pharmacy benefit management companies.”

So this seems a different kind of work than what Take does.

1 Like

This presentation probably gives a good overview of the Clinical Data Management work at a high level.

https://globalhealthtrials.tghn.org/site_media/media/articles/QAWhat_is_clinical_data_management.pdf

6 Likes

Whats the analyst views on latest acquisition by TAKE? EBIDTA margins quite low at 10-12%.what cud be the value add by TAKE which may result in margin improvement?

Thanks will keep that in mind as we should comment within Forum’s guidelines but I contradict with you on that part that novice investors could get carried away simply because this is a big forum and someone would have to blindly believe on my comment and also negate all the data written in the blog. And as I am addicted to the blog, I don’t want to get kicked out  so would refrain from writing “baggar” word in the future

so would refrain from writing “baggar” word in the future

There are few important factors which stand out in the acquisition (almost down playing the importance of lower EBITDA margins) :

- Take has revenue breakup of US: 72% , AP : 21%, Europe:7%. Whereas EA has 50% of it’s revenue coming from Europe. EA has a good base in Frankfurt. So in effect Take is expanding it’s footprint into an important market through this acquisition.

- Take has audited data facility in Chennai and US and EA has an “audit ready” facility in Europe. So from that angle Take is gaining access to a important differentiator in this business.

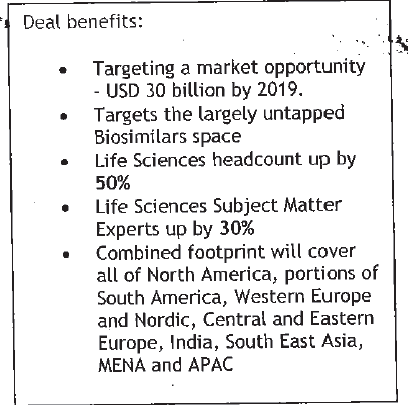

- Getting right resources (especially on pharma side) is a challenge in this business and with this acquisition TAKE’s subject matter experts will increase by 30% and its life sciences workforce will increase by 50%. So mgmt. sees it as a big positive.

- There is only a 20% overlap in the clients of TAKE and EA. EA has several marquee clients (like Roche, Fresenius, Danone,Bayer, Piramal, Dr. Reddy, Biocon). So Take sees significant opportunities to cross-sell and up-sell.

- Also, Take mgmt. thinks EA’s technology usage is on lower side and gives a lever to increase margins by use of higher automation.

- EA seems to be a CRO (Clinical Research Organization) which in turn uses services of clinical data mgmt player (previously infosys ? or may be multiple players). So in that sense there is hardly any conflict in terms opportunities to cross-sell and up-sell.

11 Likes

Thanks for taking it in good spirit.

Sire, you have been a margdarshak, so thanks to you first :).

so would refrain from writing “baggar” word in the future

so would refrain from writing “baggar” word in the future