I was a little slow onto understanding this business but mentally mapping out the pharma value chain, it seeems to be that FDA filing and compliance is a real choke point. Like the classic “shovels and spades” in the califrnia gold rush story, take could benefit from this - if you picturize FDA as the destination and pharma companies as cars passing through to it, take could be thought of as the service centre that keeps these cars upto scratch and makes the journey flawless. Given that revenues are annuity and recurring, this could be a nice surrogate for pharma.

Discl; planning to invest below 125 levels during a correction.

Hi Raj

The questions you prepared are very nice and crisp , the answers will provide a clear picture about take solution story. Did you get any reply back from management for those questions, if yes kindly share with us.

I have taken a tracking position in the company and will dive deeper into its details now. The reasons for my interest in the company are-

Absence of institutional imperative shown by the management by reducing its focus on commoditized SCM offering.

Focus on high margin and niche Life Sciences division with limited competitors globally

Long runway for growth because of new drug discoveries, acceptance of outsourcing practice in the field, tapping domestic clients which are facing high compliance issues, entry into biosimilars which is booming, more contracts due to entry in CRO through EA

IP and patented standardization process. This is a value add company unlike many service based IT companies

Foray into analytics and big data through Intelent which could be a major growth driver going forward

Shriram group which is highly regarded for corporate governance is invested and increased its stake

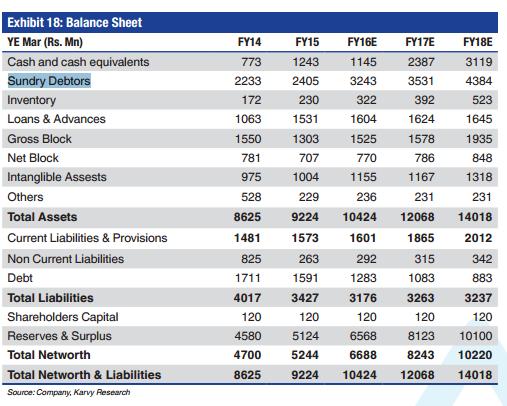

That said FCF are sub optimal and there is relatively high debt on the BS compared to others in the industry.

Please let me know if I am missing out on something

Also, there is new competition entering the market(“Larger global companies like RWS Holdings are already making moves to increase their presence in the life sciences space”) as mentioned in the article below-

Currently ,approx 45% of the market is outsourced and the top 5 hold approx. 41% market share. “The report divides the CRO market into Americas, EMEA (Europe, Middle East and Africa) and APAC (Asia Pacific) regions with the US CRO market dominating half of the world market share in 2014. However, Asian, Latin American and Eastern European countries are popular research destinations as they provide access to large, low-cost patient populations as well as low-cost manufacturing and skilled clinical workforce.”

Any idea what differentiates Take from the rest? Many of them are present in CDM too. A few of them have presence in India. How does take intend to eat into the market share?

There is no doubt that there is demand for the service. I have been looking at it from a supply cycle perspective and have noticed that there is heavy consolidation going on in the market unlike what I thought before. ICON plc has spent $300m USD on acquisitions since 2008, Prexel too has been on a buying spree(it also bought Quantam solutions India to enter pharmacovigilance market)

Icon recently acquired Aptiv ,a leader in adaptive clinical trials which differentiates its offering compared to other CROs.

These are just a few examples of acquisitions and mergers that are taking place. This has two implications. Consolidating supply with increasing demand can improve returns of the companies- provided they pay the right price for acquisitions. Secondly, Take can be an acquisition target too.

Correct me if I am wrong.

One thing that stands out for Take Solutions is their networks(Nets - Navitas Life Sciences). They are creating a strong network effect by getting all professionals in one place, gaining insights and improving their offerings.

Thanks all for the collation above incredible… I have not factored so many things in my investment rationale…

@sagararya Net Debt (Total Debt (LT & ST) - Cash & Equivalent & Sundry Debtors) for the firm should be low or zero based on check last year… will re-analyse post results and update here… hope it helps… Worth keeping an eye on the Sundry Debtors as in event of liquidation 100% might not be accessible.

Disc. I manage a boutique portfolio invested in Indian equities for my clients here in London. I hold Take Solution for myself and clients…within a botique po

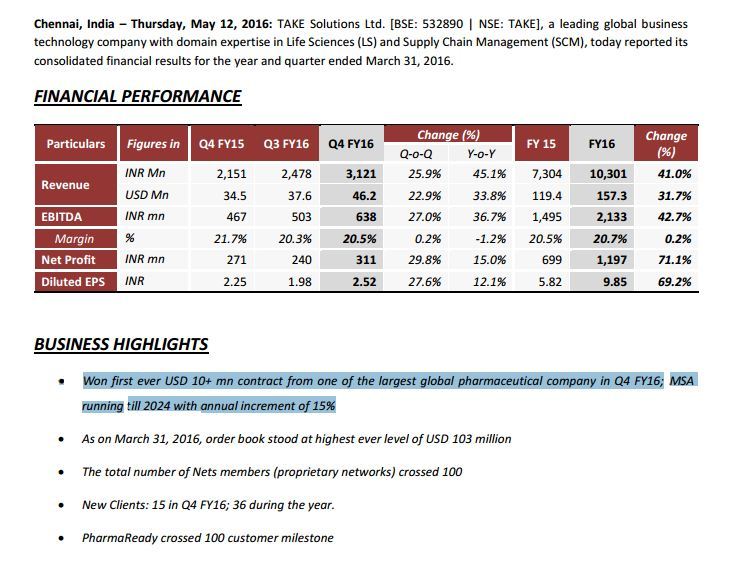

If someone is planning to attend tomorrow’s concall, please see if we can get any clarification on why the company’s tax rates are so low and by when will it start paying at full tax rates. Thanks.

Even though the tax expense looks high in absolute terms, the effective rate is still low @13.86%

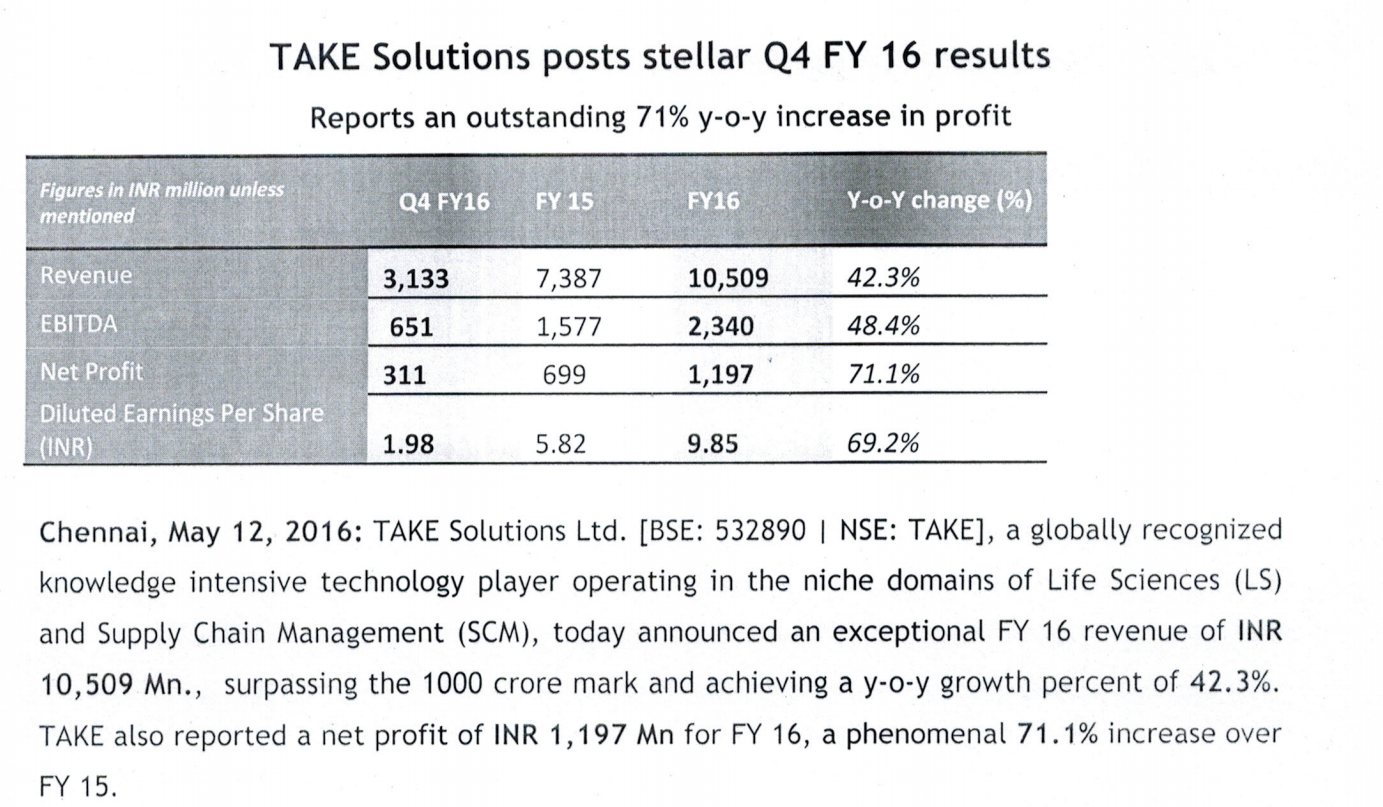

But, positives are huge quantum of client wins - 15 and reduction in debtor days from 120 to 106.

Another point is that even after consolidation of EA numbers(which had revenues of 132cr in FY14), the sales growth does look impressive.

This large $10mn order is one of the key aspects to watch out for. This speak about their capability to win large orders. Typically large orders will have big global vendors competing.

Why cash & books + debt? - Take currently has cash on books for 40 days. They would not be comfortable with letting go off liquidity. (It is a standard practice for IT companies to have cash on books to address liquidity. In 1997-98 Infy faced a big liquidity crunch. NRN started this practice of building cash on books after that)

Why lower tax rate? - Take is subjected to differential tax rates from multiple geographies. In chennai their office is located in SEZ. They get tax benefit from here. FY17 tax rate guidance is 15-16%

Take is planning to divest SCM business & has appointed investment bankers for this. (The proceeds may be used to repay debt)

They are pursuing 4 large orders (order size range from 15-28mn)

This $12mn order is recurring till 2024 (yes every year) & has clauses to hike by 15% every year.

Revenue from Ecron was 42cr in q4 with 4cr ebitda.

I had a very bad line this time and may have missed many aspects:(. Others please add if I have missed something.

I could not get a chance to ask my questions due to lack of time.

Curiously, all who got chance were analysts. There were no individual investors.

Disappointed as i had prepared a long list.

Anyways, quick updates on concall.

Excluding EA, Life-sciences grew by 50%

USD 10mn win was on a per year basis. Combination of solutions(licensing) and services. Services component will be a scaling factor for incremental growth.

Orderbook for life-sciences was approx. USD 90mn v/s 69mn last year - excluding EA.

Nets membership count is 110.

Excluding EA, 270 cr of organic revenue had a margin profile of 22%. Dip is on account of EA Acquisition cost.

On Ecron Acunova

Revenue contribution was INR 42 cr @10% EBITDA margin (Average quarter run-rate was 30cr)

Made additions to EA management.

Have made strategic changes in direction of business with aim to increase margin. To see fruits after 2 quarters.

General outlook of LS

Clients looking out for specialists/SME’s.

Rollout of unique clinical data aggregation platform. Further plans to build new solutions on top of this platform such as Risk-based monitoring applications.

Increase in RFP’s, which company believes the pipeline funnel is sustainable.

Others

Taxation: Company continues to see tax at 14-16% annually. 2 reasons given for low taxation - SEZ as was iterated by @KS16 and other was rationalization through International taxation.

Looking at divesting the SCM division.

Working with global consulting firm for next phase of growth. Working on 6 big ideas across clinical, regulatory and safety.

Company sees less competition for PharmaReady in the small and mid-pharma space, while it is a different ball-game in large pharma.

Overall a positive outlook. But would have liked to have had more qualitative insights.

Update:

Had a 30 minute call with Take IR and one of the Executive Directors.

Transcript is being reviewed, which upon completion will be updated here.

Removed the link, to refrain enthusiastic folks from spamming Take IR

Mr. Srinivasan mentioned that the proceeds will be used for growing life sciences vertical as it is more accretive to the company. Debt will be retired during normal course of business.