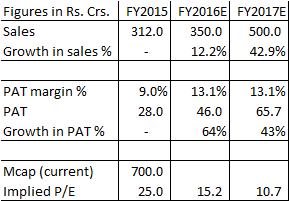

Hi @brajeshrawat, on Q2 concall mgmt. confirmed below FY2016 estimates adding that it is beneficiary of fall in crude prices… more the fall in crude prices, higher will be the margin as crude is key raw material for polyester yarn.

Further, as per earlier concall, mgmt. expects US ops to scale to 100% utilization levels in FY2017. At 100% utilization levels, USA plant has potential to make $36 million revenue (i.e. Rs. 200 crs.). Currently, USA plant is operating at 35% utilization levels.

So both sales and profit margins are expected to increase… You can already see the visible offshoots in H1 FY2016. If crude remains around these levels for CY2016, then below FY2017 estimates shall play out…

Further, once phase 1 reaches 100% utilization levels, phase 2 expansion in USA is expected to kick off. Company is already well funded for this capex plan. Mgmt. is expecting to increase dividends payout also this year.

@borapratik03

I believe the New Auto safety norms that will be enforced in mid of 2017 will open new opportunities for Sarla.

Compulsory Airbags will make inevitable for Airbag manufacturers like Takata, etc., to open up their plants in India.

This will be a huge market in a high margin segment.

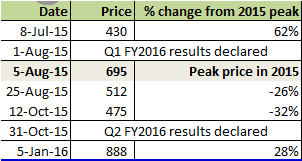

There has to be some issue in the company. Falling from 90 odd levels to 62 today is not a correction which all the mid cap stocks are going through. A fall of 30+% seems a red flag. I might be wrong but, I am skeptic.

I agree that price movement has been a real roller-coaster … But business performance has been steadily improving.

I think results will bring sanity/steadiness to stock price, as has been in past atleast…

Three key triggers :

+Company’s raw material are crude derivative so margins are expanding q-o-q.

+Also from this quarter, there are triggers to boost sales as well (Nylon 66 plant started ops, USA sales are steadily scaling)

+Capex is already funded, so no equity dilution or debt raise on cards now. Rather dividend payout might increase this year (Mgmt. hinted this on Q1 concall)

Same here. Accumulated more at 58/-. No issues. Speculators hitting the stock down. Lets greet them - its shopping time for us. Good to have sarla at such cheap levels.

Do you see any reason to hit sarla to this extent? Sarla is a very different story - catering to US markets which has recovered/recovering. Textile sector has opened and I find this company to be much undervalued at this CMP. The company is in a good position I think. It has monopoly in certain products and exceptional gross margins (70% - US). I dont see why the stock is beaten so much? 70+% down in a months time? At a PE of 10-12 the stock has good MOS. There are two points here -

1). China has lost its competence in global markets in textile sector. This gives benefit to sarla on one hand.

2). China slowdown can impact US growth, which in turn can slow down the demand for sarla products. Hanes is the biggest customer for sarla and hanes has markets in China as well (much smaller market). But, look at the products of hanes - sports wear, nightwear, underwears and other inner garments. Now these products are not that price elastic and China is a very small market for hanes as such.

Sales will be impacted definitely because of 2nd reason - but do take in point the first reason - the china supply has reduced much - which has opened the doors for Indian textile companies.Basis this I do not see any fundamental issue in the stock.

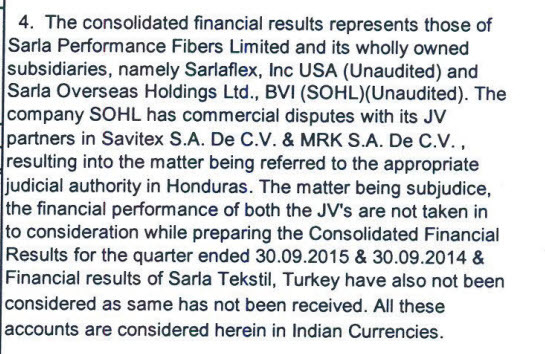

Has anyone taken note of commercial dispute with its JV partners in Honduras? What are probable outcome of this dispute? What could be liability on the company?

Why financial results of Sarla Tekstil, Turkey not received? Is there a pending dispute in Turkey also?

I was wondering why company has disputes in many countries and what could be potential liabilities of these disputes?

Savitex (www.savitexsa.com), the Honduras JV is a co-venture between Sarla (40% stake) and its Canadian distributor, Viafil.

Another JV copany has been established by the partners in Honduras, MRK S.A. De C.V.; where Sarla holds 33.33% stake.

Sarla overseaes is holding 45% shares in Sarla Tekstil based in Turkey.they have no mention of the results in the december 2015 results.

the attached screenshot from the September results mentions in detail on the dispute in Honduras and delay of results from Turkey.

Questions:

Any mention of these matters and its impact on business in the con-call.

May i request fellow valuepickrs holding the stock, to email investor relations for more information on the matter.

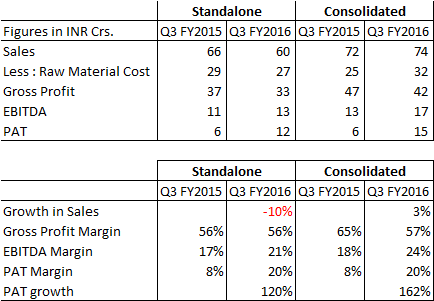

Sales at standalone and consolidated are muted. I believe this is due to realization drop, volumes must have grown marginally. Similar thing happened over last quarter - passing limited benefits of drop in crude price to clients.

Gross profit margin at standalone is intact. Gross profit margin at consolidated is decreased by 8%, but is still at 57% levels.

EBITDA margins have shooted up because of inventory adjustment and stock in trade adjustment. PAT has grown by 2.6x!

Key questions on my mind for management -

Volume growth at India and USA ops. Update on Nylon 66 ops. Any key update on USA ops picking up.

Reasons for so low tax outgo - Is there any subsidiary or tax relief?

Nature of other income.

@Gaurav, will raise JV dispute point. To my limited understanding from some past AR or calls, it is non-material, but will still raise it, if on call.

@Nityanand, past decade gross margins have been in higher range despite of crude volatility. Management attributes this to value added nature of products. Please see below table -

In FY2007, Sarla Performance Fibres floated its 100% subsidiary Sarla Overseas Holding Ltd. with capital outlay of Rs. 1.83 crs. This subsidiary is holding 40% stake in JV company in Honduras (Central America). This JV company became profitable in 15 months of its partnership.

JV company made a turnover and PAT of Rs. 27 crs. and 7 crs. in FY2008. Accordingly, Sarla Overseas Holding share was Rs. 9 crs. and Rs. 2 crs.

Sarla Overseas holding got 33.33% stake in MRK SA De C.V. which started the operations in the year 2010-2011. In FY2011, MRS SA De C.V had sales of Rs. 3.3 crs. and PAT of Rs. 1.3 crs.

In FY2012, Sarla Overseas Holding earned a net profit of Rs. 6 crs. This profit primarily came for 2 JVs only. The European and Turkey subsidiary had nominal profit/loss.

Since FY2013, company stopped consolidating JV numbers due to disputes. Although, the JVs were materially profitable by then.European and Turkey subs have no disputes.

Need to check with Mgmt. on reasons of disputes, business impact of commercial disputes, any liability, non-compete etc. But given, last reported performance, this dispute seems to be non-impactful.

i wrote to their Investor information team (investors@sarlafibers.com) yesterday. didn’t receive any reply as of now. I am likely to call their office today to know this. Centrum broking conducts the concall.

Suggest if someone else also takes lead here by reaching out to company or centrum guys…