@abhishek90

The fall in RM prices is mainly the reason for decline in the standalone/consolidated sales at the nominal level.

The real growth do exists through volume growth of 3-4% (not commendable though ) but Sarla’s focus on value added product is a plus point.

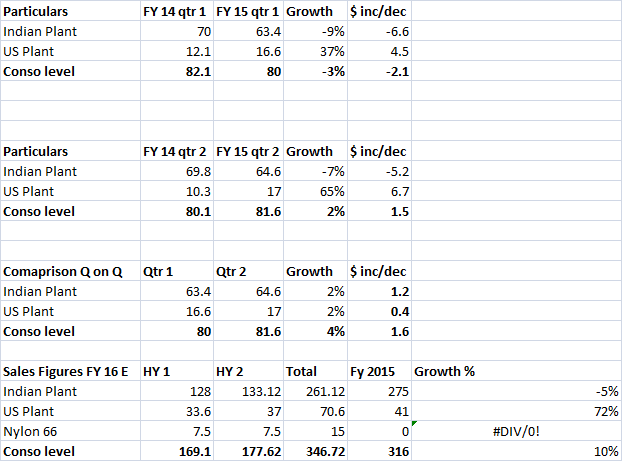

1). volume grew by 4% Y-o-Y - As per my understanding this should be at the consolidated level.

2). GP margins increased from 50% to 60%(approx) - this means that the decrease in raw material prices has not been passed out to the clients, If this is true then, the Indian sales might have been shifted to US sales and the volume growth might be just because of sales of Nylon 66. It can be also that the crude benefit might be bigger than 10% (around 15%) and 5% has been passed back to clients. In this case then, the Indian sales might not be shifting to US plant.

When we see in the above table - Q-O-Q growth in sales at India level - its a 2% growth - this has to be because of growth in sales volume only. (Since price has already been decreased at the start of the year - due to crude price reduction).

This shows that the de-growth of 9% and 7% in first 2 quarters of FY 2016 can be because of -

1). Reduction in sales price by say 10-12%

2). Growth in sales volume of say 3-4% (this is in line with mgmt guidance)

Net net effect is a negative growth of 8-9%.

This story proves since there is a Q-O-Q growth in Indian sales (though just of 2%). I might be wrong on this. Since, a mere 2% growth can be because of slight price increase. Mgmt can be the final verdict on this !!

Pratik, thanks for developing a great thread. Really liked the look of this company - traditional manufacturing company that is conservatively run while innovating with new products.

@abhishek90- as per the management call, First shipment of Nylon 66 was done in Q3- FY 2016, so Nylon 66 will come only in the H2,

2)The turnover split , (Us plant)It also includes subsidiary other than the Sarla flex(Subsidiary for the new plant) , so the comparison will never be correct.

Oh yes. You are correct Ateek. But what is your view on the sales shift? I called the IR team of Sarla - they told that they were IR people for sarla in past - they are no more now. Website of Salra not updated. Even i tried calling the mgmt - CFO of the company - they told that he is out of office and you need to call next tuesday. Meanwhile asked my textile friend to inquire on the company and its plants, products.

I think, The volume growth is there, on standalone level its 3%(as per management call), Realization declined due to the low RM prices benefits are passed on to the customer (as per management any variation more than 5%(+/-) will be passed on to customer.

Even i called the management, same reply

And if your friend can find out , how are the demand scenario’s in US?

So it means that out of say 15-20% savings due to crude prices reduction, some 10% was transferred to clients leading to reduction in top line by 10%…but volume growth of 3% came to help reduce topline by net 7%…the rest of the savings in crude prices ie 10% is reflected in gross margins expansions. .

Hi Abhishek, as I understand company passes only 5% benefit and takes only 5% hit from crude/raw material fluctuation. Rest they pass to customers. This is what your math also reflects. This policy of company reflects some significant bargaining power of company with customers. I understand that they are amongst very few specialty yarn manufacturers and not textile commodity trader so they are able to protect their margins (look at last 10 year margins).

From this quarter (Q3 FY2016) onwards around Rs. 3.5 cr. additional revenues will flow in from Nylon 66 sale.

Assuming crude remains at these levels, Co. is expected to report ~Rs. 350 cr. sales and Rs. 46 cr. net profit this year. Co. is planning to increase dividend also from this year!

In FY2017, if USA plant scales to 80-90% utilization levels then sales can fillip to ~Rs. 450 cr.

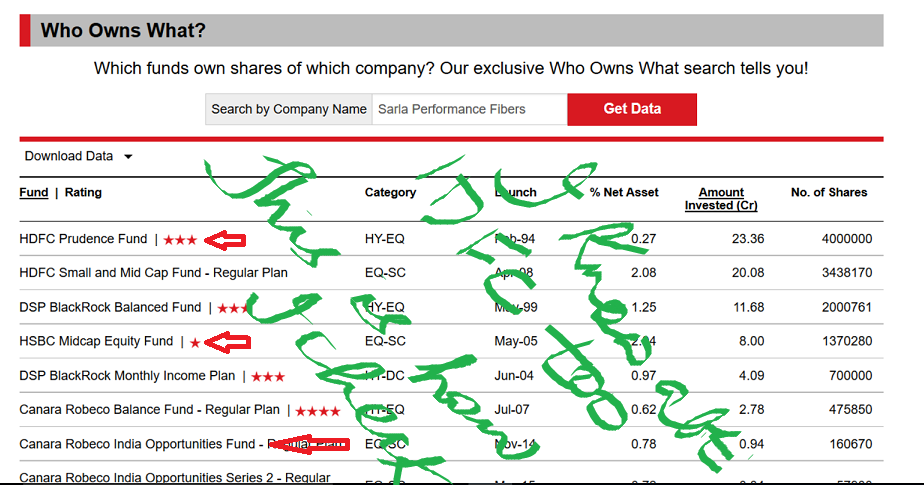

They are in the process of being picked up by MF’s like HDFC and IDFC, so once that happens they come into the open, get out there before they are known. The US business has great future. Nike and others order Nylon 66 from these fellows. Most importantly they have already done Capex, now just need to milk it.

posted pic below on the holding of a few funds, lets keep checking as this months they are expected to pick a lot more and new funds ,ike HSBC and Canara are also picking it

) but Sarla’s focus on value added product is a plus point.

) but Sarla’s focus on value added product is a plus point.