Dear Members, wanted to draw your views and attention on Sarla Performance Fibres.

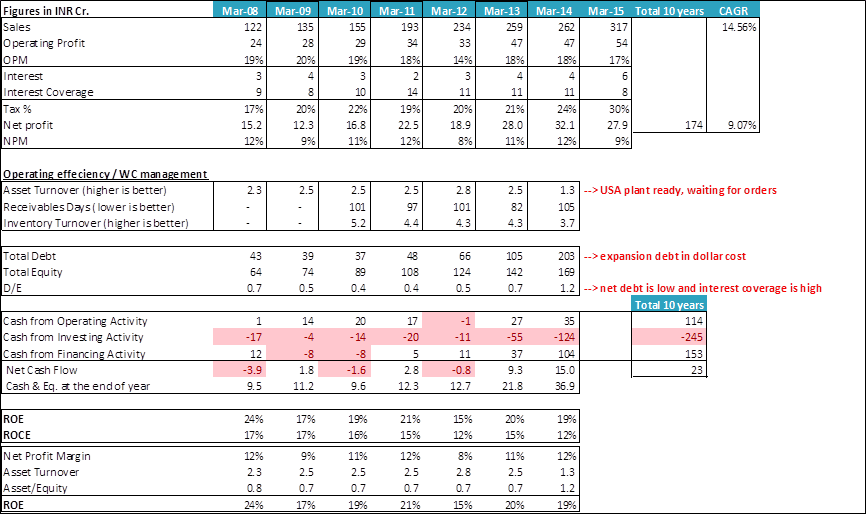

Company is manufacturer of specialty polyester and nylon yarns. Its product finds application in innerwear, hosiery, sportswear, narrow fabrics, seat belt, car airbags, fishing nets and leather goods. These products are different from commoditized yarns given their nature and it requires a strong understanding of product & customer requirements and specifications. This transpires into healthy operating margin to company - operating profit margin has been in range of 20% to 17% over last 7 years with exception of FY 2012 where it dipped to 14%.

Company has 2 manufacturing facilities at Silvassa, India with capacity of 11,000 TPA and one dyeing plant in Vapi with capacity of 3,200 TPA

Co set up wind mill with total capacity of 7.25 MW to cater captive energy needs.

Co caters to branded global players including - Jockey, Hanes, Gildan. No single customer contributes more than 15% to revenue. Yarn constitutes ~5% to total cost of final product; however a very crucial product, hence Premium paid for Quality & Consistency desired by Large Global Customers (Hedge against raw material price volatility).

~57% revenue comes from US and Europe and 43% from Asia Pacific.

Growth Triggers -

a. Co. has set up manufacturing unit in South Carolina, USA with installed capacity of 9,990 TPA. As of March 2015, it was operating at 20% capacity utilization and is expected to scale up this year. (Exact details not available as company did not conduct any investor call). Key highlights of this plant include -

- NAFTA & CAFTA treaties, allows waiver of duties upto 32% on synthetic garments manufactured in North or Central American region using US origin yarn when exported back into the United States (company claims to be only Indian company having presence in NAFTA and CAFTA regions)

- Proximity & Visibility to customers (majority clients in USA and Europe)

- Lower Logistics & Power (majority clients in USA and Europe)

- Lower Cost of Borrowing (dollar debt)

- Plan to expand current capacity to ~18000 TPA by 2017 (double in 2 years)

- Land cost of Rs. 7 crores to be paid over 7 years

b. Company has set up pilot plant at Silvassa to manufacture Nylon 66 which is high tenacity low shrinkage product used in parachutes, shoes. Company claims to be only manufacturer of Nylon 66 in India. Note capacity of this pilot plant is mere 450 TPA as of now

Financials -

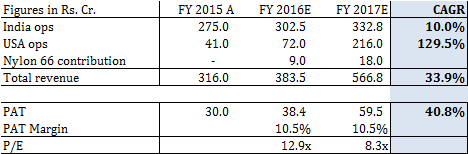

Market cap of company is Rs. 358 cr. and FY 2015 PAT is 28 cr. (P/e = 12.7x)

Sales have started to pick up : FY2015 sales of Rs. 317 cr. is 21% rise over FY2014 sales. Operating profit margin have been in range of 20% to 17% over last 7 years (with exception of FY2012 where it dropped to 14%). Due to increase in tax rates from 24% to 30% in FY 2015, net profit margin is at 9%.

Though debt levels are doubled in FY2014 over FY2013 to 205 cr. interest coverage ratio remains healthy as it is dollar debt. FY 2014 debt and equity is 203 cr. and 169 cr. resp.

Asset turn has taken hit to 1.3x from 2.5x due to recently installed USA capacity (asset base increased to 196 cr. from 102 cr.). FY 2014 ROE is 19% (net profit margin of 12.3%, asset turnover of 1.3x and asset/equity base of 1.2x)

Note : debt/equity has been conservative in range of 0.11x till recently. Expansion in USA plant has expanded leverage albeit at healthy interest coverage ratio as it is dollar debt.

Company recently concluded QIP of Rs. 46.7 cr. in Oct 2014.

Company has been dividend paying since last 11 years.

Promoter holds 55% stake in company with no pledge.

Company’s website is very informative and updated (http://www.sarlafibers.com/desk-managing-director.html?reloaded=true)

Key concern remains - response to USA plant expansion. If the USA plant delivers then growth coupled with higher margins will lead to good value accretion to shareholders.

Review comments on Sarla Performance Fibres and above write up are invited please - happy to explore this idea further.

Disclosure - invested in stock