Only thing which is stopping me to invest more here is their lack of additional capacity. They are operating at peak capacity and volumes can’t go up from here on. Only the commodity prices can help get more realization.

The company is currently producing about 2.13 lakh tonnes annually and running at full capacity of about 95 percent leaving very little room for the volume growth. Growth in the coming year will be largely driven by higher realisations and marginal growth in volumes. While the company is evaluating land for the greenfield expansion, which might take time, in the interim it is looking for the acquisition as the company believes that because of the stress in the sector and marginal players unable to carry on business and are up for sale. It is thus in talks with banks exploring suitable acquisition opportunities as the company is sitting on close to Rs 190 crore of cash (Rs 585 crore net worth) in the books.

—> As per this company is thinking of some interim acquisition. Do anyone has any news regarding any acquisition opportunities being shortlisted

Maithan is not a pure cyclical valuation catch up (that stage is matured now). Capacity utilisation you would find at optimum not now, since few years back. It’s more about:

Strong trade off decisions in operational risk management- power, raw material and clustered supplier management.

Custom tailored process- in a myriad of permutations and combinations Maithan is one child who has committed and delivered specific tensile products for the industry.

Subodh is a Rolls Royce for this industry. Banks speak about him as a benchmark! His individual salary alone previous to Maithan was close to PAT of company!

Lots more I wrote under Guru Mantra (except updates), going forward you will find capacity utilisation at peak, that’s not surprising either.

Of course I am bit worried about quality growth expectation by investors at large.

Disclaimer: heavily invested since 40 rupees (pre bonus), unlikely to offload in near future with same set of behaviour.

Thanks for highlighting something which i never though of while evaluating Maithan. I have gone through some of your posts on this wonderful forum and they are thought provoking. By Guru Mantra are you referring to “Suvi Investing Journey” & “Jewels of India” or the specific Guru Mantra series on the forum?

Please see these posts, you will find loads about Maithan. Right from custom tailored process to Blue Ocean applicability.

But once again I stress this was never a battle for Maithan when it comes to my investment decision. It boils down finally to my engagement with crowd foot print, convergence with fundamentals. This is how I played the game so far! Maithan Alloys.xlsx (11.6 KB)

Note: this is an example of success, there were many drop outs. Once something works money management can do wonders as long you are up for a long shot game!

I can not stop emphasizing few things again and again:

My engagement with market depends on my money management, methodology and psychology. By handling only methodology it’s small battle won.

Competitive advantage rarely visible from financials alone. Competitive advantage is embedded to value chain of company which in turn linked to business process of company. Unless you breakdown the financials to key business process we will never be able to understand where the competitive advantage is.

Turning business process understanding to competitive advantage to financials should be your knowledge chain. For example Maithan have clustered small suppliers for a raw material supply ( so you won’t find proportionate tangible asset addition). Most of us read financials first, business drives accounting not other way.

I am glad you find them useful. Somewhere during this weekend let us get into some serious money management stuffs. I have covered basic few under this thread:

Last week I got engaged to someone who has spent three decades on subject of money management. No need to say I was blown away with his superior deliberate practice but once again I felt incredibly stupid and vulnerable.

I guess the cycle starts, then re-cycles again and again. Ultimately it depends on us as to how to distil the information than getting overwhelmed due to name and fame or any other aspect. I have been guilty of these random thoughts and still now perhaps! Few pointers:

A jam pack crowd glued to an expert (with good fan following!) couldn’t demonstrate a face which is not American or a product which is not American or a book! The guy sitting next to me was confused for 30 minutes (whether Dalal Street or Wall Street) before we decide we won’t be bhakt again and VALIDATE everything before shouting jai ho.

Easy information and resources (like online forum, free website etc) brought enormous psychological battle to mind of ordinary investor without VALIDATION process. I wonder when an news paper or regulated news paper publish certain things, have they audited the process of particular individual or company? Perhaps the rudimentary reading will be the next biggest reason for wealth destruction of ordinary investors like me.

Have we even bothered Larry Williams cracked 1.1 Million from 10000 in one year (not some random article, US investing champion, AUDITED by EY). He is not alone, many goes on cracking more than 100% return on capital for years. Then it is up to us to lend an ear and try to understand whether these statements have any value to out investing philosophy.

The nature of speculation has never changed since 100 years or plus. Whether forecasting process of institutions, mis- selling of DCF by same guys, crowd foot print for money management, mathematical expectancy! Then who is trying to stop us, and of course then why do we get stopped in first place?

Let’s spend some quality time on behavioural finance and money/risk management. We will able to liberate ourselves from certain beliefs.

The acceleration in Sales (QoQ) has increased from 6.5% (Sep17/June 17) to 16.96% (Sep17/Dec17). Corresponding increase in EPS move from 9.33% to 20%.

Pointers to note:

2.5 Cr lower depreciation due to revaluation of assets, impact of 3% on EPS.

Consolidation impact at year end 2017- insignificant after completion of restructuring in business in last year itself.

Three fold increase in trading of goods clearly showing management is going to up the number further next quarter onwards. Of course acquisition as Subodh indicated has to be the organic way forward. To me personally plenty of sick and idle alloy companies exist close to their own facilities. Unless Subodh strikes a match between his own ROA and prospect ROA he will continue to evaluate. A lot of these idle plants have fixed cost and high debt component, a blind purchase may destroy wealth. EBIDTA contribution by goods trading increased by 1.25% this quarter.

Power cost slides further from 19% plus to 18% this quarter. This is indicating further rationalisation on grid front.

Raw material cost nose dived from 42% to 38%, that’s a huge improvement. With additional inventory purchase (12Cr plus changes) should help coming quarter at least.

Where I am worried:

The investment banking style of annual report continues by an extremely smart CEO. Sometime in quest for achieving satisfaction of audience facts may be twisted.

Bold trade off decisions like shutting down plant due to low margin in past. CEO may claim pressure tactics? Despite of long term contracts sales price is market driven. Even with advance orders you are obliged to supply in time, not sure how shut down help these? One time heroics?

1% cost saving add 6% EBIDTA. How long power rationalisation will pump this advantage? And what about below the line costs in future?

VIzag- 100% export plant contributes 50% of revenue. Domestic sales are difficult from this unit due to import duty. What will happen if there is a steep decline in export sales?

My CEO wants to buy old plant at a bargain to squeeze more ROA. Great, timing will play crucial in cyclical race.

At end of day when you sit on profit with a CEO firing from all cylinders I will wait and watch with all my holdings.

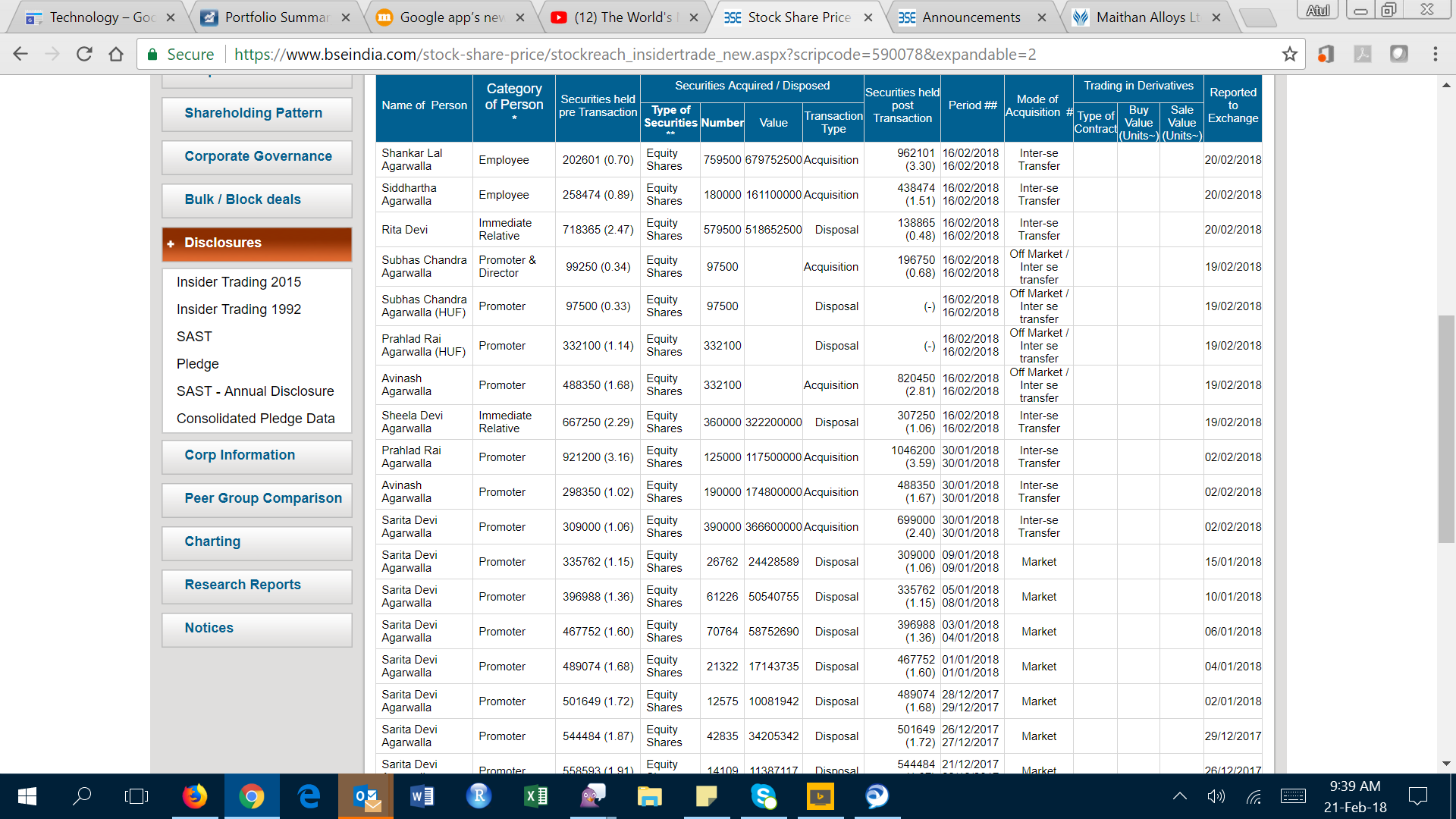

Circus of insider transfer continues… Hope company give some clarification about the future course of action. It is very clear now that promoters held more stake than disclosed in the SHP through immediate relatives which is now formally becoming part of promoters shareholding.

The things are not so simple as they look on face value. Last to last year the two promoter groups parted ways, that time holding of one group was transferred to another without any monetary disclosures. The promoter equity was same as before post this change of guard.

Question arise then who are these immediate relatives? Why the company is not disclosing how much these immediate relatives hold in total? What is the actual shareholding of promoters + Immediate relatives ? Is it more than 75%?

I dropped a couple of mails to the company and did not hear back from them. That’s the reason I call it circus. Company with shaky disclosures make me nervous specially when they become substantial part of the portfolio.

One thing I do agree with @atulastra that the company has never been prompt in replying to the queries raised. Many queries are still un-answered by the company. I am not casting any doubt on the company but as a measure of good corporate governance they should promptly reply to all the queries made by investors after all we are also stakeholders and we have every right to know what is going on inside our company.

I would also like to know whether the company is bound to share information (non price sensitive) with its investors or what kind of information can be demanded from the company.

They increased authorized share capital from 15 crore to 80 crore.Was that really necessary?Are they going to issue more shares in the future.Personally i dont see the point,the company is essentially debt free and has good amount of cash.

Actually this first recent investment after joining vp last month. I used screener to invest in the stock. Apart from fundamental I looked for management…Subodh is class apart. So recent dip in profit may not be concerned for long term. Capex and demand for steel is on way. My first view…Forgive as i m learning…