Practice notes on Competitive Landscape, competitive advantage and interlock business strategy

Few days back we discussed about how business strategy and competitive advantage are interlocked and an approach how an investor can unlock these concepts. Why are we doing all these things , basically to genuinely find out a company having advantage or edge over others. So that it can satisfy our basic requirement of sustainable growth and profit for a long time.

As times are evolving single method like Porter five force are inadequate though it helps a lot. A traditional five force doesn’t reveal new mega trends (as the identification process doesn’t depend on a market share and ROIC), or a uncontested market place for same reason. What I currently do for a company:

- Build a business model description (by using a canvas or abstracts what ever you feel right). But this must provide information on the entire value chain of company like a. the business and market segments b. value proposition c. distribution channels and marketing methods/CRM d. Cost drivers & structure (resources, infrastructure and activities), key revenue streams and partnerships. I like Business Model Canvas though I don’t think it reveals a lot about business strategy but nevertheless a good start. Don’t worry about a great deal of details, a basic understanding is required.

- Gather information key strategy assessment and those are a. market forces b. industry forces c. key trends d. macro economic forces. This is just preliminary information gathering.

- A strategy canvas (please refer to the post), this brings back focus to those key competition factors.One practice note I used in earlier post.

- Check whether industry falls under a growth trend or Blue Ocean even. Traditional five force like switching cost, entry barrier doesn’t carry a lot of relevance to Blue Ocean industries as these are created in new waters without having competition records or peer comparison. We did a value alignment last time which can confirm whether company falls under Blue Ocean or not.

- Blue Ocean companies created by expanding red ocean always prone to competition. Build a competitive landscape, and see the company positioning to landscape (this brings us back to Porter five force).

6. Identify the existence of competitive advantage, mindset of edge, and sources of competitive advantage.

7. How does the competitive advantage impacted the value chain and more importantly PL account.

8. Can we identify key business strategies that are taken by management which resulted a better value chain and PL.

I always felt by bringing in mega trend/Blue Ocean with a traditional competitive advantage identification converge both new and old world. Of course the challenge lies in spotting end to end chain of activities, no wonder it’s an iterative process and improve with more practice. Understanding a business , it’s edge and the strategy build around by management has become a pain for me over the years. Whenever I took short cut by identify few terminologies here and there it never assures. Of course at the end of day all these can go wrong, but not the learning. :)

Anyway my focus is point no 6,7 and 8, I have made them bold. This is my yesterday’s practice note for 6 and 7. That is a competitive landscape, source of competitive advantage, value chain and PL drivers. The point no 8 business strategy, a prototype I am building….will paste here once I complete. Example and disclaimer remains same- Maithan Alloys.

Competitive landscape of Maithan Alloys

A. Industry Map (please see attached excel file for the map)

Iron ore is raw material for steel making, when iron ore is feed to furnace alloys (like manganese is introduced as additive). The major three segments for Industry will be 1. Minerals and Ores (for iron ore steel manufacturing companies also own ore mines but for manganese ores its comparatively lower as it’s dominated by MOIL). In both iron ore and manganese ore there are many smaller players due to leasing by different state governments. 2. Alloys manufacturers (those who manufacture alloys by using manganese) 3. Steel manufacturers (end recipient of product).

In ferro alloys sector baring TISCO there is not much overlapping name who manage end to end. Though iron ore and steel manufacturing owners are common. A number of small players exist in each market segment. But a chance exist where steel manufacturers aggressively integrate backwards i.e. start manufacturing alloys as well.

The buyers/customers are big player (steel manufacturer) who influence the pricing , also due to a fact commodity type of product. However the cost of ferro alloys is barely 1% of steel need and a core requirement for production.

Despite of high number of suppliers, a couple like MOIL manage the bulk supplies, however with import available and auctioning price suppliers are not a major threat.

Although there is little barrier of entry, the negative margin and return on capital discourage new entrants.

There is no substitute products for ferro alloys.

The rivalry within industries is intense, this can be seen in lower profitability. The rivalry resulted lower cost to buyers.There is a high exit barrier, undifferentiated product making competition tough. Being a cyclical industry capacity often gets added in boom period leaving over capacity when downturn starts.

B. Identification of competitive advantage

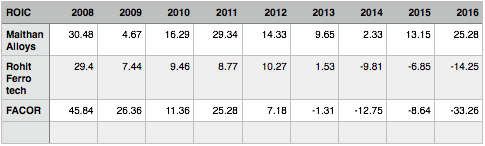

The present capacity of ferro alloys industries in India is around 5.15MT with a 3.16 Million tonnes for manganese alloys. There are more than 100 manufacturers with no clear leadership. Hence leadership stability doesn’t reflect much as margins of lead are thin and fluctuating.

Industry return on capital is getting dismal with negative, post cost of capital it will be more miserable. Where as Maithan has demonstrated a decent number though it has fluctuated.

C. The Source of competitive advantage

Chances of captive customers- in absence of switching or search cost it doesn’t justify a strong case. What may make a case is value added products due to nature of different grade of steel. This may be binding customers.

Cost advantages- there is no technology or asset related advantage in industry. The cost advantages due to operational efficiency covered separately.

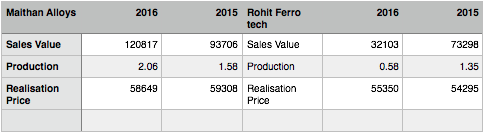

Economies of scale- 2016- 206178 tonnes, 2015-157920 tonnes. Operating cost has come down from 92% to 88.5% which is a major improvement.

Profit due to government intervention- Maithan has been availing direct and indirect tax incentives for it’s Vizag unit.

Maithan provides tailor made products, but whether that added to pricing power need to be analysed. Economies of scale is working in favour with value add product can work in favour of company. There is also temporary boost from tax incentive. Apart from this profit power may be coming from operational efficiency.

Mindset of Maithan Alloys

- Maithan has targeted to generate higher return in terms of capital and margin than producing more and more. Clearly the focus is on profits than having market share.

- Rather targeting best customer, Maithan has reached out in terms of diverse needs of customer i.e. tailor made product.

- The innovation can be seen when management has tied up with small vendors than playing in ore markets, buying power grid and making asset light avoiding captive power consumption.

Value chain and P&L of Maithan (please see attached excel file)

A. Relative Pricing Power

Though Maithan is enjoying a minor price advantage its not significant.

B. Relative cost power

Lower operating costs or using capital more efficiently including working capital.

Facor alloys though have a higher operating margin than Maithan and Rohit inventory can play spoiler.

On a working capital front Maithan is a clear winner with superiority over receivables, inventory and payables.

C. The Value Chain Analysis

The key areas of value chain leading to customer value will be supply chain management, operations and sales & marketing. This is why:

Supply chain management- all about procuring raw material in time and delivering to customer in time. Imperative to have a quicker delivery time both side either by getting close to customer location, vendor location or owning a strategic asset like mine for ores. No wonder most of alloys manufacturing stays close to steel manufacturers geographically unless you are an importer in high quality manganese ore which is not available in India.

Operations: despite a standard production process, quality and customisation plays a specific role due to alloy adds to quality of steel and different grade of steel requires different composition. Apart from this getting power in time points why operation is important.

Sales & marketing: although you have a specific customer base (only steel industry) the over capacity in industry coupled with direct imports creates a need for better marketing skills.

Maithan vis-a-vis industry value chain

Within scope of supply management Maithan has reached out small mine owners and partnered with them. The partnership cost them bit funding, knowledge transfer and robust cash flow supported them. Other key aspect is Maithan is not involved in raw material trading to garner speculative profit. I would say stay to core competency.

Tailor or custom made product is a major value enhancer as the different grades of steel are becoming diverse. This reduce the quality testing and further refinement by steel manufacturer reducing their cost. The custom made product again requires some time to get accepted by customers. This may work as entry barrier.

Maithan has focussed on long term contracts where both price of raw material and end product are speculation driven i.e. market based price. Though it has not brought any additional pricing power which saw in pricing analysis but they have been able to fill orders and use their capacity which in turn reducing the fixed cost per unit.

Power is a significant cost for the industry, due to power shortage on line supply most of manufacturers have set up their captive power plant. Maithan on other hand bought grid from power board and reduced capital spending and more importantly asset light without maintenance. We can see a significant improvement in power cost , Maithan is spending around 26% of sales as power cost against competitor spending around 40% of sales.

When you read together strategy canvas and value chain together it will clear how PL is connected with business strategy.

Attached a working file, let me know questions if any.