Has anybody attended the AGM ? Please share the Notes

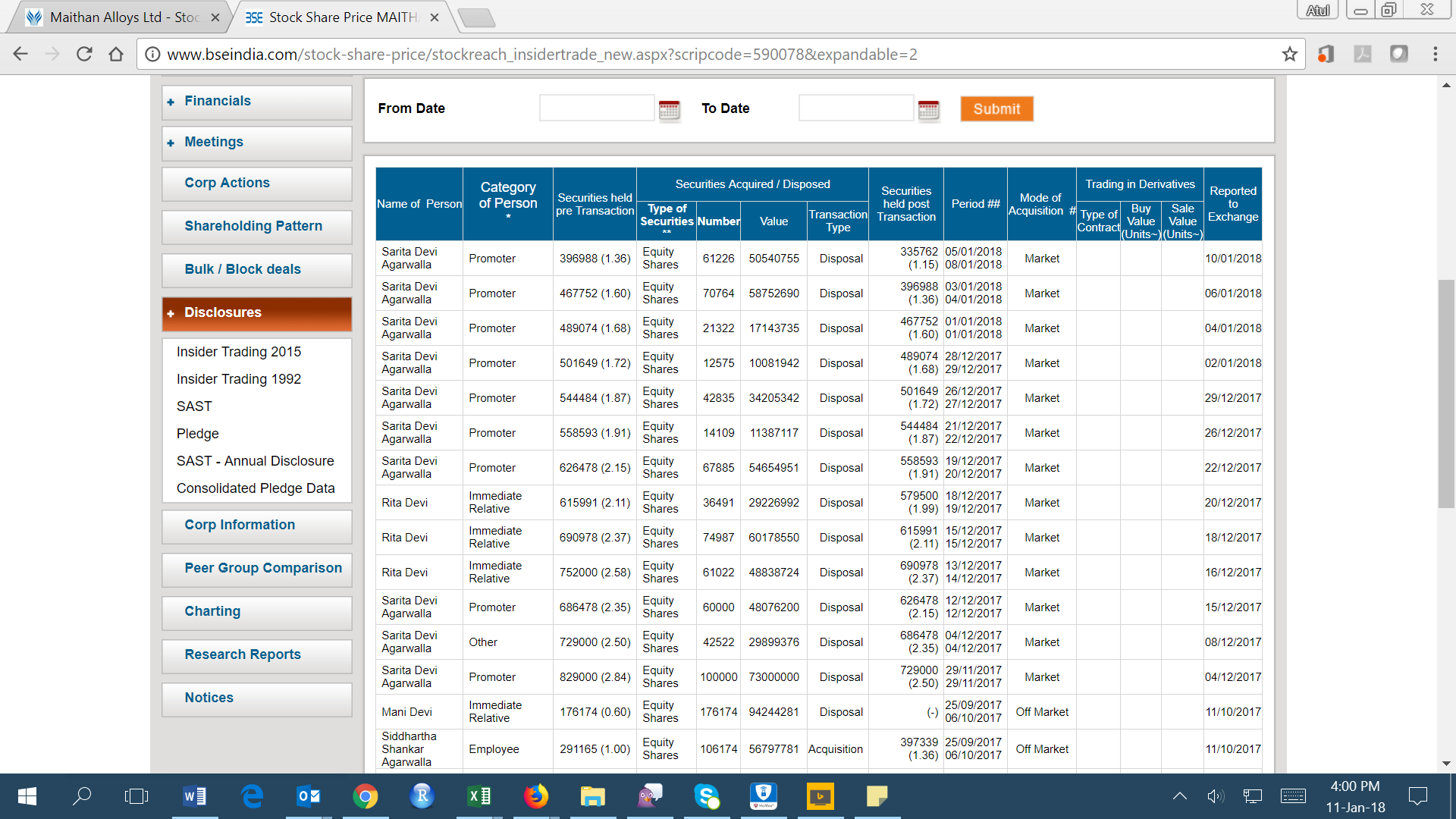

Yesterday’s data shows that relative of Promoter/Director has sold some shares via block deal. What could be inferred from this?

That might be just some profit booking. Nothing else. And it wasn’t a promoter who sold. Some immediate relative sold the shares.

Nice analysis by Dr. Vijay Malik

Disc : Booked profit for majority of my holdings recently, have a small tracking position now.

3 Likes

Q2 results: http://www.bseindia.com/xml-data/corpfiling/AttachLive/bd4efc04-b836-49ca-9608-04bc818793e5.pdf

YoY Comparison

Revenues: 458 cr vs 309 Cr

PAT : 65.2 cr vs 9.7 cr

2 Likes

Maintains impressive performance

Any update on increasing capacity. they seem to be running at almost 100% capacity, so now scope of growth in next year ?

Good Result.One announcement I can find on BSE. “Related Party Transaction”,Maithan is paying INR 2.82L(though very small amount) to take 100% equity share of Salanpur Sinters Pvt Ltd (SSPL).SSPL has no operation,generate no revenue. Virtually no reason for takeover. I am invested for long time in this scrips.

Kindly share the link, I have been looking for more information on this particular topic.

Disc: Vested interest and biased views

1 Like

I could only find this much!

Here it is.http://www.bseindia.com/corporates/anndet_new.aspx?newsid=8b9c3a94-47f0-4152-9ff8-0c10f208f4d6

Look for the declration made to excg in pdf.

Got super excited after listening to one of the fund manager on Maithan and was forcefully tempted to go through the numbers. Here are my two cents.

Operating at near 100% capacity and with no new greenfield or acquisition announed, the uptick in production is not visible at least over next 12 to 18 months. New greenfield capacity will take at least 2 years to come on stream and any new acquisition will take at least 12 to 18 months before the closure happen and consolidated numbers start yielding higher output. Hence the earning uptick is restricted over next 18 months and will be hinging purely on ferrous alloys price movement.THIS MAKES IT PRETTY RISKY BET.

Valuation wise,the company did 124 crore pat in 1HFY18 and assuming similar runrate, the FY18 should give not more than 240 crore pat (unless ferrous alloys price movement go up more aggressively). At 240 crore, the valuation is based on current market capital of Rs 1950 crore translate into a little over 8.5 times. Given the pat uptick is significantly limited for FY19, the valuation looks even more stretch.

The company is generating considerable cash flows over last three years and still not paying higher dividends, nor are they investing in growth, except that the same has been utilized for paying off debt which is still at Rs 76 crore in absolute terms (comfort is that D/E is at 0.12 times - FY17).

During the year FY17, the company purchased Rs 545 crore worth of investments and then sold Rs 415 crore worth of investments, made some Rs 15 to 16 crore profit on such sales and also received Rs 115 crore dividend (cost of investment for FY17 was net of dividend income). Is this the core business for the company. For this size of company, Rs 545 crore of investments. R U SERIOUS. WHY AUDITOR HAS NOT RAISED A FLAG FOR THIS.

Ability of the management to keep employee cost at barely 1.5% of sales is while on one side is commendable, it also raises doubts as how the same is possible in a industry which is highly fragmented. Maithan claims to be the largest player but account for barely 10% of the market in terms of capacity.

Disclosure: Not invested, would be waiting for significant correction and more clarity.

5 Likes

Sorry to ask one more thing. There are was no purchase and sale of investments in FY16. During FY17, the company purchased Rs 545 cr of investments on which they earn Rs 115 crore of dividend which translates into 21% dividend yield. WHY WILL ANY COMPANY EVEN IN THEIR DREAMS SELL SUCH INVESTMENTS WHICH GENERATES 21% DIVIDEND YIELD. Which investments has yielded 21% dividend. Majority of their investments are into debt funds.

1 Like

2 Likes

This is one company I am closing tracking. Although I entered two months back with a token position and stock has given me 50% returns but I believe this cyclical story might provide good medium/long term returns

With the government’s efforts to ramp up domestic steel production in the country by 200% in next 13 years and the growing demand for steel and less/reduced dependence on steel imports, raw material suppliers to steel firms should benefit with this cyclical upturn.

From the valuation perspective,the stock is trading below PE of 10, which might provide margin of safety even in case of correction.

The company seem to be performing well for last few quarters which again might be because of recovery in steel demand and if the demand sustains then we might be looking at good returns in coming quarters

https://www.screener.in/company/MAITHANALL/

Disclaimer: Invested and might increase stake if events turn positive for company

Maithain Alloys has completed acquisition of entire equity shares of Salanpur Sinters Private Limited.

1 Like

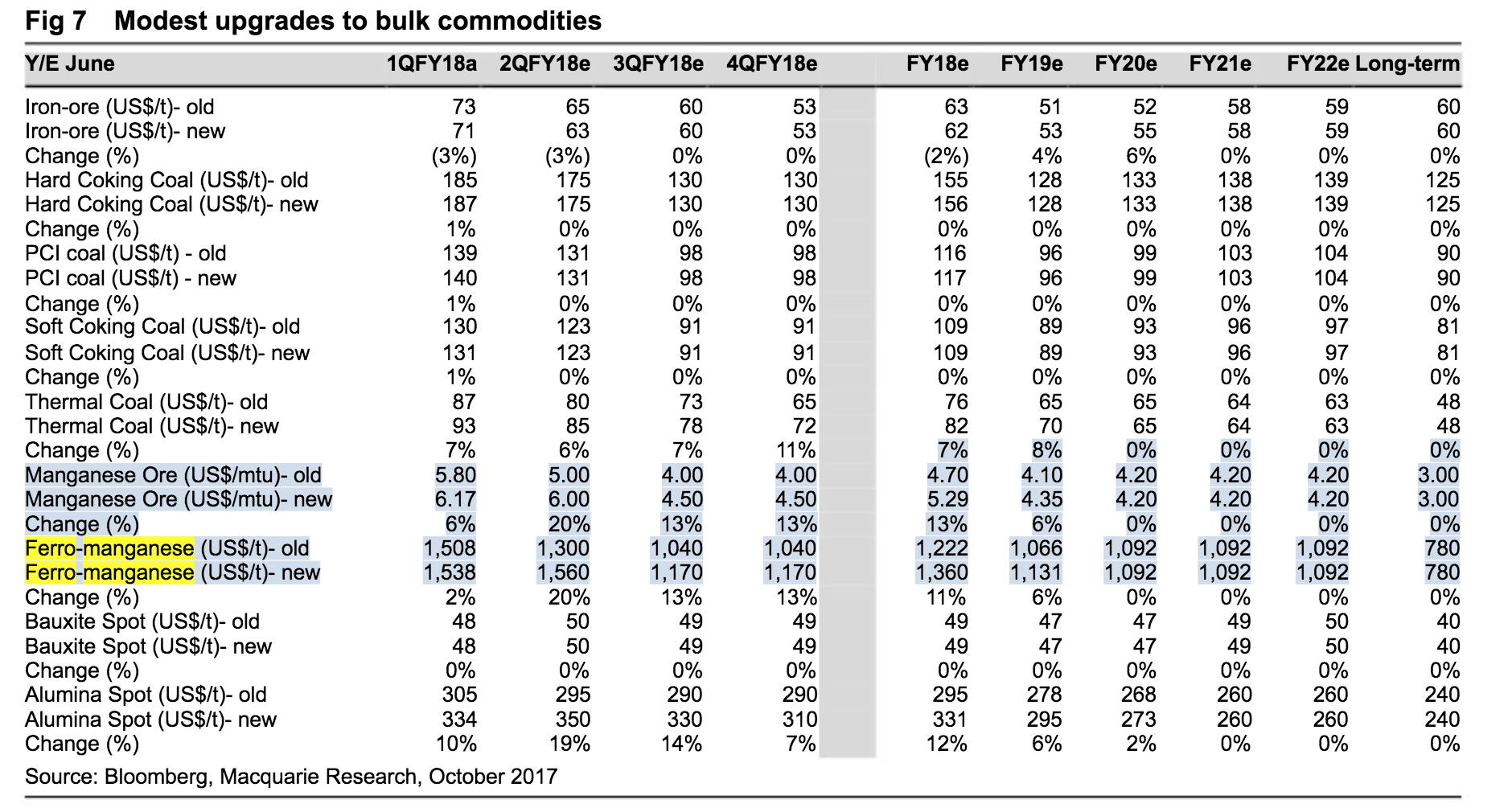

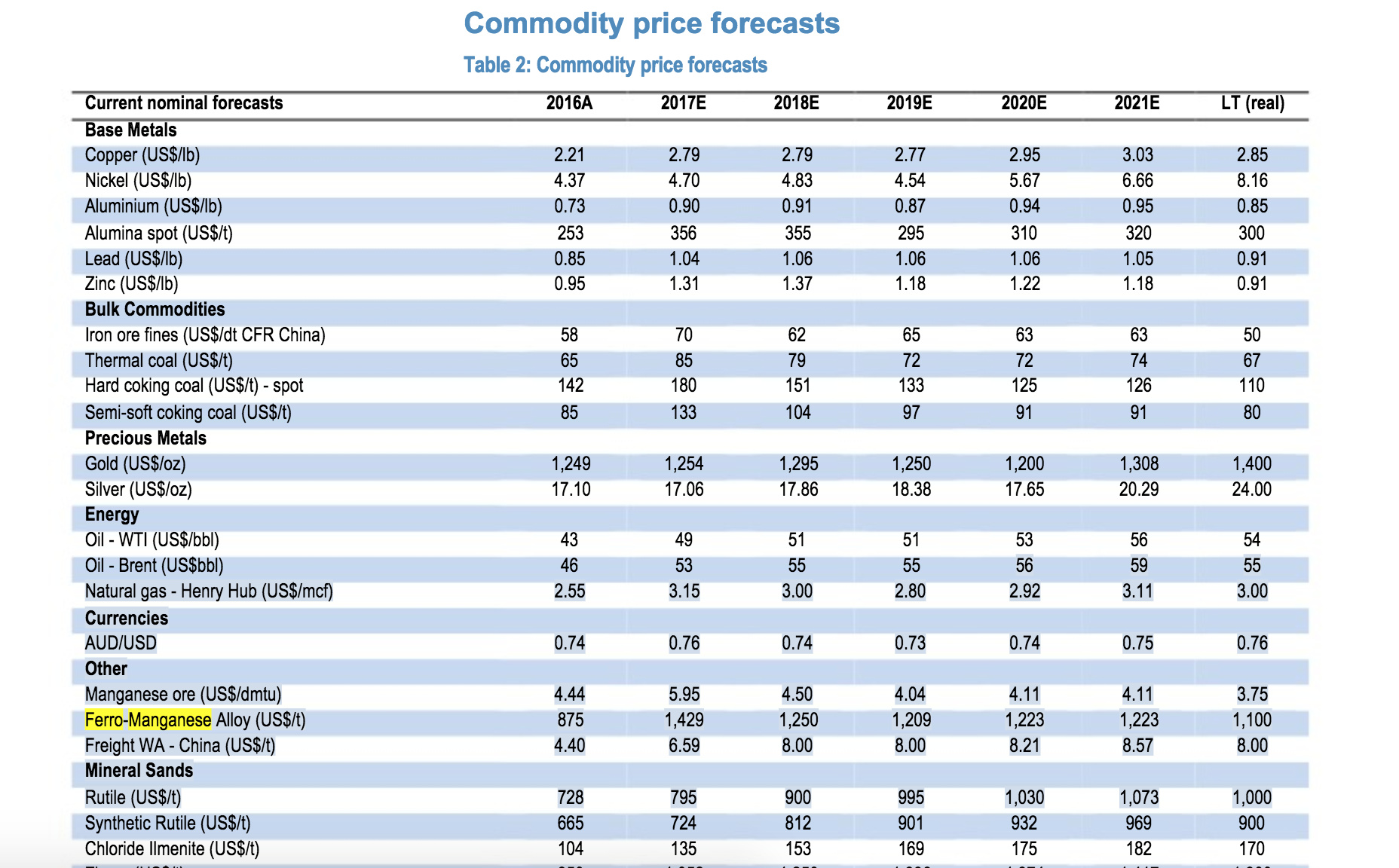

And following are the latest estimates by JP Morgan,

Can anyone please make out of these numbers to arrive at fair price for Maithan alloys.

1 Like

I really fail to understand the current circus of buying and selling by promoters.

Last 3 months 3 entities have been added as part of promoter group with around 1-1.5% stake in the company. on the other hand some promoters are selling continuously in the open market including some immediate relatives which are not part of promoter group.

Selling by promoters and close relatives:

Declaration of new additions:

If some one has clue please share what is the real shareholding of the promoters including promoters, immediate relatives and undisclosed entities.

The promoters sells but the share price continues to move up, this selling is happening since last many months now but stock price keep moving north.

Disc: Vested interest and biased views

2 Likes

This stock is on a run from quite some time. Is someone tracking this. Is that the overall steel industry sentiment changing to positive is resulting in bull run in this counter. From the valuation prospective it looks still a lot more undervalued based on EPS it is generating.

Disc: Vested interest and biased views.