Kitex Garments doesn’t sell in domestic market at the moment.

After the Q3 results, there was an interview of Mr Sabu on ET Now(12th Feb). I couldn’t watch the interview(was on travel during that period) and I am not able to find it online too.

If someone had watched it, could you please be kind enough to post the summary of the same. Or if someone could pass the link to the video it would be even better. Thanks in advance.

1324acb6-7432-4e12-861f-8b5212a97e6d.pdf (150.2 KB)

3 Likes

Mr Sabu has bought some more through open market purchase today too.

3 Likes

This is interesting. Mr. Sabu continues to buy. 82K shares purchased today as per announcement to BSE. See below.

3 Likes

8 Likes

Toys R Us files for liquidation, likely spelling its end in the U.S

china general textile sector trends and problems

1 Like

us birth rate data and correct interpretation

2 Likes

The article talks about the challenges faced by the garment industry:http://www.thehindu.com/opinion/columns/endgame-for-garment-exports/article23630821.ece

The article is about the broader garments industry. We cannot categorize kids’ clothing industry with the broader garments industry. Sure, Kitex is also constrained by the GST and exchange rate troubles, but it will pan out in the future. In fact, the most important fact that makes Kitex attractive as an investment is that it is not operating in the broader garments industry and never tried to get there.

1 Like

KGL_BM_Outcome_250418.pdf (63.7 KB)

developments:1.incorporate 2 wholly owned subsidiary companies

2.Increase manufacturing capacity for future demand.

3.invest 400cr in companies through internal accruals and borrowings

4.KPMG involved for implementation of projects.

KGL has only one subsidiary - Kitex USA LLC ?? KCL is not a subsidiary ??

Results out but nothing found impressive. Profit lesser than previous year, cost of materials increased, employees cost also increased may be due to gratuity provosions, r toys filed for bankruptcy , kitex jas to take money from them

I find the results to be very poor. Both sales and profit are diving with YOY net profit down to 10cr from 26cr. Textile is among the most fragmented and commodified industry in India. On top of this, the textile industry has global competition and regulatory hurdles on the one hand. On the other hand, the buyers are some of the world’s largest chains with pricing power. So as such textile companies have very low moat in India and therefore in my opinion not for the long term unless there is some exceptional competitive advantage which I do not see any in Kitex.

1 Like

I would find it problematic to categorize Kitex into the larger textile industry (As I have mentioned just a few posts before). It sells niche products (Kidswear) which are partially recession proof.

The result is most definitely terrible and we should wait for the management to explain the reasons. Toys R Us filing for bankruptcy is going to be one of the reasons. We should fish for any other reasons that could have caused this. I don’t see any fundamental changes to Kitex’s long term performance.

By and large, Kitex still remains a ‘Buy’ in my eyes.

The only thing I am tracking about Kitex is their usage of excess cash for expansion in the south. The CEO has opined that they might be using a mix of cash and debt to fund the 500 Cr expansion.

What about the management issues?Not identifying related parties correctly?Quantitatively yes it does look cheap.

While infantswear might be recession proof, Kitex is just a supplier to other retailers. In this business costs matter a lot and there’s nothing very unique about what Kitex makes that it can’t be made by someone cheaper in Bangladesh or Vietnam. Infantswear exports market is growing faster in other countries like Vietnam and Cambodia and recently also in Bangladesh. India has been losing its market share and is not cost-competitive.

Some really great research about growth prospects has been done in this very thread last year and the year before which are very insightful. Do take a look at these at the very least.

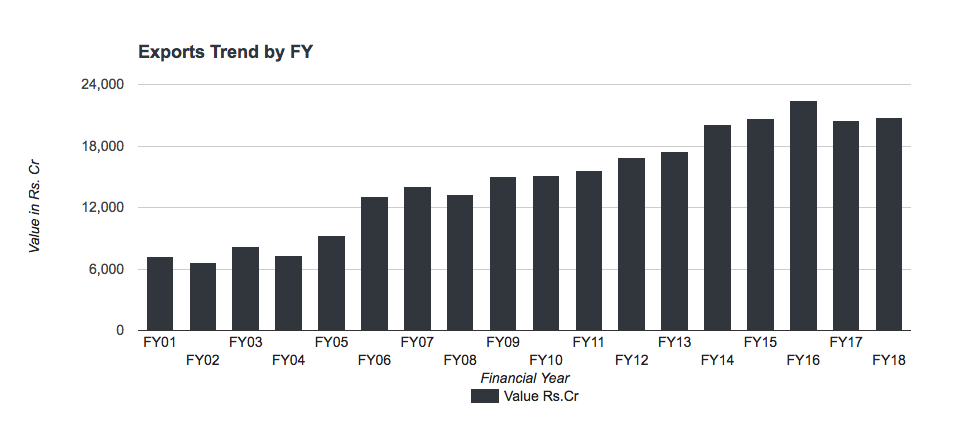

One more addition from my side. This is cotton apparel exports from India to US and UK. You can see how similar Kitex’s topline trend is, to the overall garment exports from India.

4 Likes

First of all, thank you for providing the link to the posts.

- If you read through the posts yourself, you’ll realize that the procurers like to keep their sources diversified. So, while Bangladesh/Vietnam seem to be acing the volumes game, India still owns a piece of the pie and will continue to do so. Here’s some baseline info from the Annual Report of Carter’s, one of the largest players in the US in Kidswear:

While we have no way of knowing if Kitex is one of the 3, we can safely say that the big players would at least like to keep their largest sourcing diversified.

-

As I always say, all stories/research about a company should show up in the number of the company. While I have the full force of hindsight bias behind me, the things claimed in the posts such as Kitex losing out on Market Share has not shown up in the numbers. In fact, even for the recent results, Sales has increased a bit in spite of Toys R Us going AWOL. If Kitex had received that money as well, Margins would have remained more or less the same. I’m just assuming here and we should wait for management commentary on this.

-

Kitex Garments / Indian Kidswear exporters do have a niche in exporting Kidswear. I suggest you read through this article: https://www.thedollarbusiness.com/magazine/baby-garmentsthis-is-indeed-a-big-deal-no-kidding/45848 (Notice how some of them point to the fact that India is at the nascent stages of this and needs to step up their branding game. I feel that Kitex is already there)

-

Once again, I do not understand why you keep comparing the broader textile industry to a specific, niche Kidswear industry. A more appropriate chart would be this:

This shows that over the last decade, Kidswear exports from India has grown by 3.5x (As opposed to the lower 1.5x-2x shown in your chart). Kitex’s Sales has grown by roughly 5x during the same period.

- Specific to Kitex, they are doing more Value-add to their sources while keeping costs reasonable. This is one of their most recent attempts:

Of course, we shouldn’t forget the upcoming Karnataka plant, which will benefit their Sales and Economics of Scale (Lesser costs).

- Let’s say I agree with you in stating that Kitex is mediocre. Even if you assign a very low Sales Growth of 10% to Kitex for the next 10 years (Essentially 2.5x in the next decade - Not an unbelievable estimate) and a considerate 5% for the Terminal period, with Kitex’s capacity to generate Owners’ Earnings, I think it’s still undervalued in Present Value terms.

1 Like

hello dinesh,

most of the skeptics are not worried about kitex growth or future plans. They are more worried about the curious case of idle cash and related party transactions within the group. Had these factors not been there,there would be no skepticism. If growth was the valuation metric can ,DMART share price be justified?

1 Like