Yes, that is why I said the most important thing I’m tracking regarding Kitex is their Karnataka plant expansion plan and how they’re going to fund it. They have about Rs.200 Cr lying around. The plan is worth Rs. 500 Cr. In Mr. Jacob’s own words, the gap will be covered by new Free Cash Flows and a part of Debt. We will just have to wait and watch. Once again, about related party transactions, the CEO has claimed that the entities will be merged or at least brought under the control of the listed entity. We have no other option except to ask the management when this is going to happen. He is always outright about this, no hiding or anything (In Concalls, interviews).

DMart’s price is justified not by growth, but the longevity of growth. In fact, the longevity of growth is the most important factor hinging on the Value of a company. Why do FMCG companies quote at huge PEs? Not because they can grow extraordinarily, but because they can grow gradually for an extraordinary number of years. For more on this, you should read Michael Maubosisn’s piece of the MICAP (Market Implied Competitive Advantage Period): http://people.stern.nyu.edu/adamodar/pdfiles/eqnotes/cap.pdf

Sabu jacob came on TV in March and says Q4 will be better. He should have know impact of Toy r us but he chose to give bullish 13 % sales growth target and 24 % pbt figure. He keeps repeating this time and time again …basic lair. He should take full provision on TOY RUS of 17 cr but has taken 3 cr and feels they can recover money. Carter has taken 12 Million hit this on receivables this qtr.

They are no CFO in company and he definitely plays around with numbers and cash.

Too much money from profit commissions for himself and hence is incentivized to fudge higher profit figures ( using loop holes )

huge CSR spend and high profit commission is also red flag. He is definitely not worried minority shareholders.

Profits are down from last 5 years and OE (jazzy term for commodity business ) is going to be further down if you observe cash is comming down (higher working capital ) - inv and receivables increasing because of new business as well as customers consolidation .

On positive note i believe Kitex US LLC is now on track and should contribute significantly in couple of years. If this business can scale then you will get good scale and operating margins. But we did not see little star brand yet in the market.

While Operating margins of 23 % to 27% are sustainable hoping he is able to scale business with Lamaze business and grow with top 3 retailers

In short customer side dynamics are changing lot , he needs to quickly scale up Lamaze business and wholesale business with larger players like Amazon , walmart , Carter. ( these will only survive ) .

Lot of moving parts so very difficult to predict future cash flow with red flags on promoter intentions .

Disc : Invested 6% under bit of Authority bias from prof

I would be a bit careful to trust blindly.Please understand that prof has disposed his shareholding in ashiana housing.It’s not like he wont change mind if things go wrong.And though he has invested at a higher price in this company,that was a year back and if the company 's performance is bad,then maybe he will sell at a loss.

In my view, there are a few things that deserve attention in Kitex’s analysis:

Theory of being recession proof: I have never been able to wrap my head around this theory. In my book, recession proof businesses do not loose volumes even in the toughest of times – some examples include staples (toothpastes, soaps, etc.) and utilities. Barring periods of war or depression, the demand for these businesses is inelastic. Specific players may lose or win market share, but the industry as a whole moves in-line with population growth and other demographic trends. Now if we apply this yardstick to Kitex, it clearly falls short. The US economy has been on the mend for a while now and Kitex’s numbers have moved in the opposite direction for a better part of the last 3 fiscals. Some part of it can be justified by the loss of Jockey and now Toys R Us, but not all and at this stage Kitex is yet to give any proof of it being a secular recession proof franchise – instead, it’s numbers indicate that it is a B2B supplier in a cyclical industry with no pricing power and aspirations of developing a B2C franchise. It may suffer less than some other generic garment players, but it is by no means immune to the industry’s vagaries.

Refusal to look beyond the US: The second thing that beats me is Mr. Jacob’s dogged refusal to look beyond the US as a demand destination. Nobody can contest that the US is the motherlode of consumption and capitalism, but why does that mean zero focus on other high per capita geographies like the EU? Now, the lack of a FTA with the EU is a reason cited by other Indian textile players for slow growth in the region (due to competitive pricing pressure from other Asian and African producers), but that’s not the reason cited by the Kitex management. Mr. Jacob insists that the US is big enough to drive growth for many years to come – this may be true in absolute terms but exposes the company to geographic concentration risk and its impact is clearly evident in numbers. A company working in a niche space and having the experience of working with large retailers and brands in the US can command some attention (if not contracts) from clients on the other side of the Atlantic. In such a situation, the decision to by and large abstain from actively selling to European clients is counter intuitive – the management may have a solid reason for this but not that I have ever heard or read about one.

You get the shareholders you deserve: I completely agree with the adage that each company gets the shareholders it deserves. Let’s evaluate Kitex on this front. It is well known that Mr. Jacob devotes active time to business operations, employees, CSR and politics. Can we say the same about the management’s conduct with shareholders? The company does not hold regular investor calls, does not even put out a press release explaining the business environment and way forward, no investor presentation, no IR department (in-house or outsourced). Mr. Jacob himself makes a blink-and-you-miss-me appearance on TV channels as and when we wishes (or not) after quarterly results. The MD&A section of the annual report hardly provides any unique insights about the business apart from some motherhood aspirational statements. There has been no buy back or insider buying despite the fall in scrip price.

Is it not incumbent on the management to communicate with shareholders, in good times and bad (!)? Is it not incumbent on the management to present a transparent view of the operating conditions on a regular basis (I am by no means not talking about guidance here)? Does the current conduct not reflect apathy towards shareholders? And does it not result in a lot of speculation and second guessing of reasons behind the performance, capital allocation, business prospects (as is evident on this forum)? A review of the greatest companies will show that they treat shareholders as important as other business stakeholders and communicate with them transparently. And when your conduct with shareholders leads to speculation, it will bread just that in the long-term – speculators masked as investors. Ultimately, the question to ask yourself is – do I want to partner with a co-owner who has time and mind-space for everyone else but me?

I have a small position in this business for a long time. The position was based on performance as reflected in the numbers at that time. Being a long-term investor, I can live with fluctuation in performance and price. However, any ramp up or ramp down in the position will be based on the above (especially point 3) as I believe that once the undiscovered phase of a business is over, it is incumbent on the management to retain shareholders (just like it retains employees, clients and suppliers) through a combination of performance and communication.

In last couple of days reading about Kitex. I have following first thoughts Qs/observations -

Appreciate whoever tracking for long and have insight address them.

In 2013 & so Promoter planned to consolidated other K Childrenwear and other unlisted business to avoid conflict of interest. But no news found? Its concern.

Planning for new plant(s) in KA and/or AP, but not clarity, is existing utilization full? So that, seen growth in sales with new plants. In target export market is any scope for growth which is mainly to West - US/EURO, where birthrates muted?

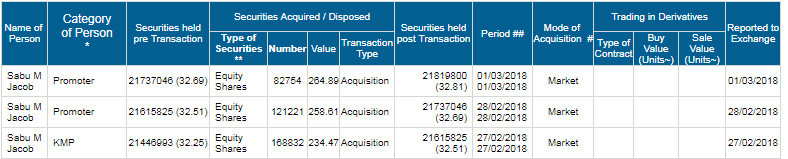

Mr Jacob’s behavioral? - a) related to above point-1, b) buys shares couple of months typically before any announcement; c) in 2013 commented to take sales to 1500cr but numbers no where. In fact, since last 3 years & so, flat sales and fluctuating PBT, like any other garment company.

so its official . The plans for Hassan (KA) plant is dropped …attributing to the current KA chaos …well it was announced earlier that the KA single window committee had cleared 52 projects and Kitex - Hassan plant was one among them …

Karnataka has been ruled out due to the present political situation,” he said.

The explanation is bizarre in my opinion!

Karnataka has seen coalition governments earlier and also many governments with politicians least interested in governance. In all these cases, industries have come up at their usual slow pace with the wheels of industry laboriously pushed by the bureaucracy. “Political will” maybe required in opening up new mines/hazardous industries/large dams or anything that requires a lot of people to move or lose their livelihood. For a garment factory of the scale of Kitex, would “political will” really matter!? Moreover, Hassan is one of textile zones I think.

Also, even in the worst of times, I thought opening up a factory in any state would be simpler than in states that favour leftist ideologies. If Kitex has survived the politics of Kerala, I assume politics in most other places would be a mere blip in the distant horizon!

Disclaimer: Was invested in Kitex. Zero investments now.

I had a look at the announcement. the numbers seem to not triangulate to each other. if the current capacity is 6 lakh tonnes and revenues are Rs. 1300 cr. that’s an average realization of Rs. 60 which seems very low for a children’s garment.Its not even a $ - this is not in syc with what the mgmt said earlier - realization was around $ 15-$ 20 was my understanding

at 22 lakh capacity a day, the yearly through put on 300 days works to about 70 Cr. pieces. About 25 Cr. of the world’s children population is below 5 and in highly developed countries which is the market for kitex. Even at say 10 garments a child, 70 cr. is about 25 % of a global market which is absurdly high for a non branded commoditized manufacturer like kitex.

HE is talking at group level … hopefully all kitex group companies … he has already aaounced 400 cr for kitex garments …and nothing ever seems to triangulate with him . Is he robinhood or crook or both . He does too good to be true community work and is not transparent with shareholders. So story is not yet very clear. But today price levels are attractive if gets Lamaze , Amazon and Walmart right. Lamaze brand is picking up …waiting for official numbers from AR or company .

Case 1 he is crook hiding 200 crores of cash than capex of 400 crore project will be easy way to do it .

case 2 he is not and you need 400cr to probably fufill demand which will come from Amazon , waltmart , Lamaze in next 3 years.

Amit Mantri case on margin is wrong as you can have 27 % margins in this business if you are backward integrated ( carter wholesale business has margins close to 23 % sitting in US).

only we need to check on cash if he is not lying there then whole market is missing big opportunity as Lamaze whatever i can read on amazon is going good. Toy r us demise will make carter even bigger and than he needs to win more business with 3 or 4 big players.

0 12 months market in US itself is USD 1 Billion.

Realization for baby suits is close to 1 USD to 1.2 depending upon the work . Retail price is 3 to 4 USD

I don’t think the realizations are $15-$20. In the conf calls in the past, Mr Sabu clearly mentioned that Kitex sells garments for around $1 to the US retailers(it could slightly vary on either side based on the type of garment). The US retailers bundle them together as a pack of 3(or 5, I don’t exactly remember the precise number) and sell.

If I remember correctly he also mentioned that, the US retailers would start selling it at $15-$16 for a pack of 3(or 5). When the inventory becomes old, the price keeps dropping as they start giving offers on the above.

The above was discussed in a conference call - although I don’t remember which quarter it was. Will try and post the source.

I recently went to London and saw kitex clothes in many stores (not sure if it was from KGL or KCL). Most of the stores selling at competitive rates had clothes imported from India and China. The price range for single piece clothes were ranging from GBP 1-5 based on intricacy of design and size.

There were many bundled pairs with pack of 2-5 pieces which were sold around GBP 6-10 but most of the clothes overall were below GBP 10.

I was surprised to see that quality, design and price of India clothes were much better in relation to Chinese clothes with limited sample of 6-7 stores that I visited.

Here is Data point from ICRA Credit report OCT 2017

Capacity = 2.7 Lakhs

Volumes concentration with top 3 customers 90 % . This was before Toy R US.

_

Top three customers of the group contribute to more than 90% of volumes, which exposes revenues to vagaries in performance of its key customers as well as order cancellation and geo-political risks. Operating performance has been impacted during recent quarters resulting in revenue de-growth for the group by ~6% during FY2017, owing to lack of customer additions, stagnation in order inflow from existing customers and shift in product profile limiting realizations.

ICRA however notes that the business performance of the group has come under pressure during recent quarters owing to a slowdown in order inflows from its major customers, lack of new customer additions and loss of business from a few customers (scaling down of business with these retailers commenced from FY2016 on account of pricing and other specific reasons)

Kitex Group revenues (KCLincluded ) was down 9 %. Sabu generally shifts orders from KCL to KGL during bad times ( not bad for KGL shareholders ) as KGL revenues were flat.

Hi Vardha,

Consumption of 10 pieces per year for baby between 0-24 months is very very conservative figure, if I take my personal experience it should be between minimum 20-30 pieces per year for this age group. Second he is talking about 22 lakh pieces by 2025… In 2025 there will be high demand from Asian countries also… Today I am buying carter’s garment online for my son which is almost available at same price as local non-branded garment with much2 better quality.

Demand may not be a problem which is only a part of the equation.

The other part of the equation is the kind of moat that the company enjoys or the lack thereof. My understanding is textile is a very fragmented, global industry with very low entry barriers. Therefore Kitex has competition around the world with some lower cost manufacturers than India such as Bangladesh, Pakistan etc. such businesses do not have much visibility in their earnings which is evident from sudden fall in profit and sales over the last year. While inability to sustain margins is a problem, a fall of 25% in sales for no apparent reason is a much bigger problem. His shows that kitex absolutely enjoys neither pricing power nor customer reach at this stage.

This is besides the apparent glaring corporate governance issues with the group with promoters having both listed and non-listed entities doing same business and with even same name.

What is happening in Indian markets. First Vakrangee , than manpasand , Atlanta , 8k miles and some other companies also. And now Kitex garments. Suddenly it is seeming like all the small , mid cap companies books are cooked and we may see some more auditors resignations in future. This is very frustrating and scary.

Kitex always had red flags from the promoter, the thread is full of examples of it. Kitex is just their MD Sabu going around giving baseless figures on TV to make people feel that turnaround is just around the corner.

Disc: Was invested long time back, exited when it was clear Sabu is just taking me for a ride.

I am not good in accounting or v strong in financial analysis. But one thing I don’t understand here is if their are really issues in fundamentals , books are cooked etc than why Sabu Jacob have bought shares worth 9.25 crores rs in last six months from open market , that too around approx price of 250 rs. Will he just spent 9 crores to fool the investors ? Would be great if someone can explain me this.