The promoter shareholding as on June 2019 was 74.49% (HDFC with 51.48% & STANDARD LIFE with 23.02%). Today Standard life has sold 3.33%. And if they continue to sell like this (may be 2 more such OFS), then the overall promoter holding will come down to 65%. So, even if government implements its plans to get promoter holding to 65% cap for all listed companies, we don’t have to worry much about stock price negative impact on HDFC LIFE

Above post is not about worries of falling share price it’s about company probably creating opportunities by doing OFS

Thanks

Ashit

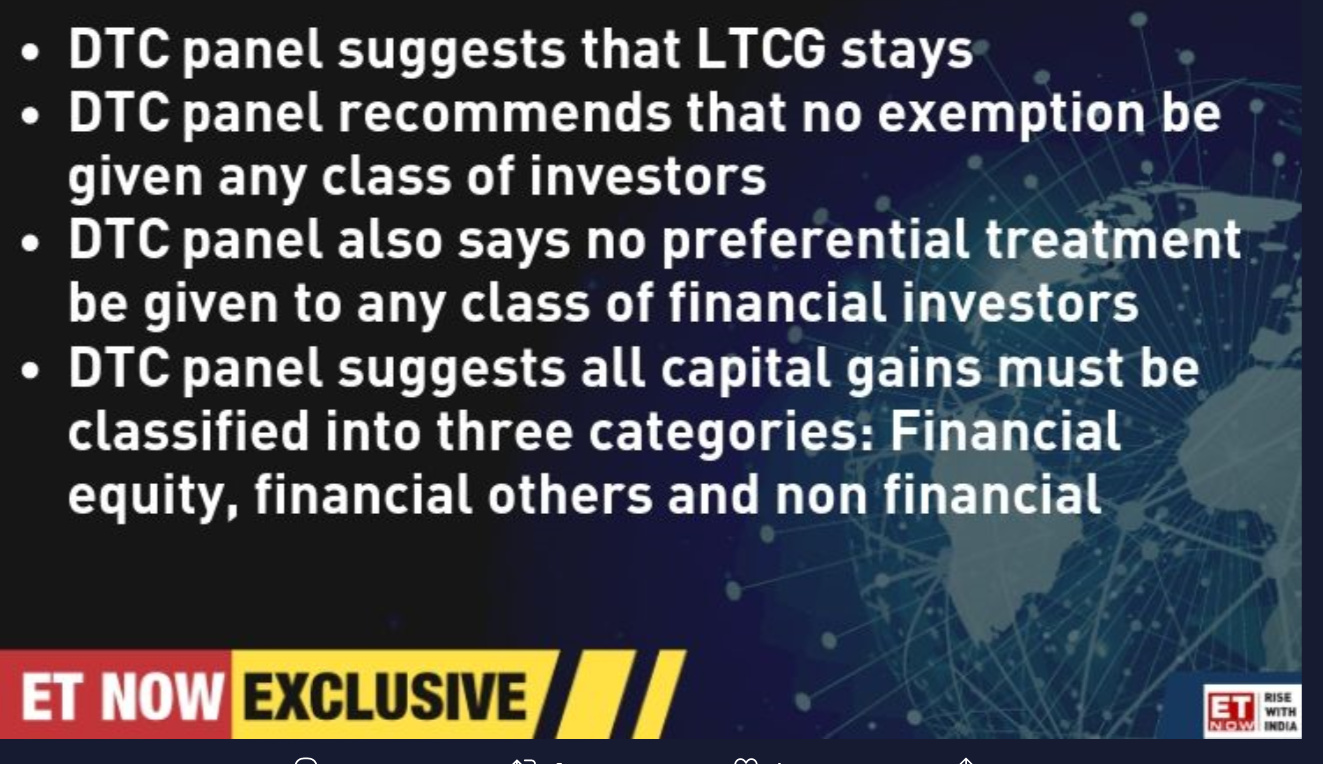

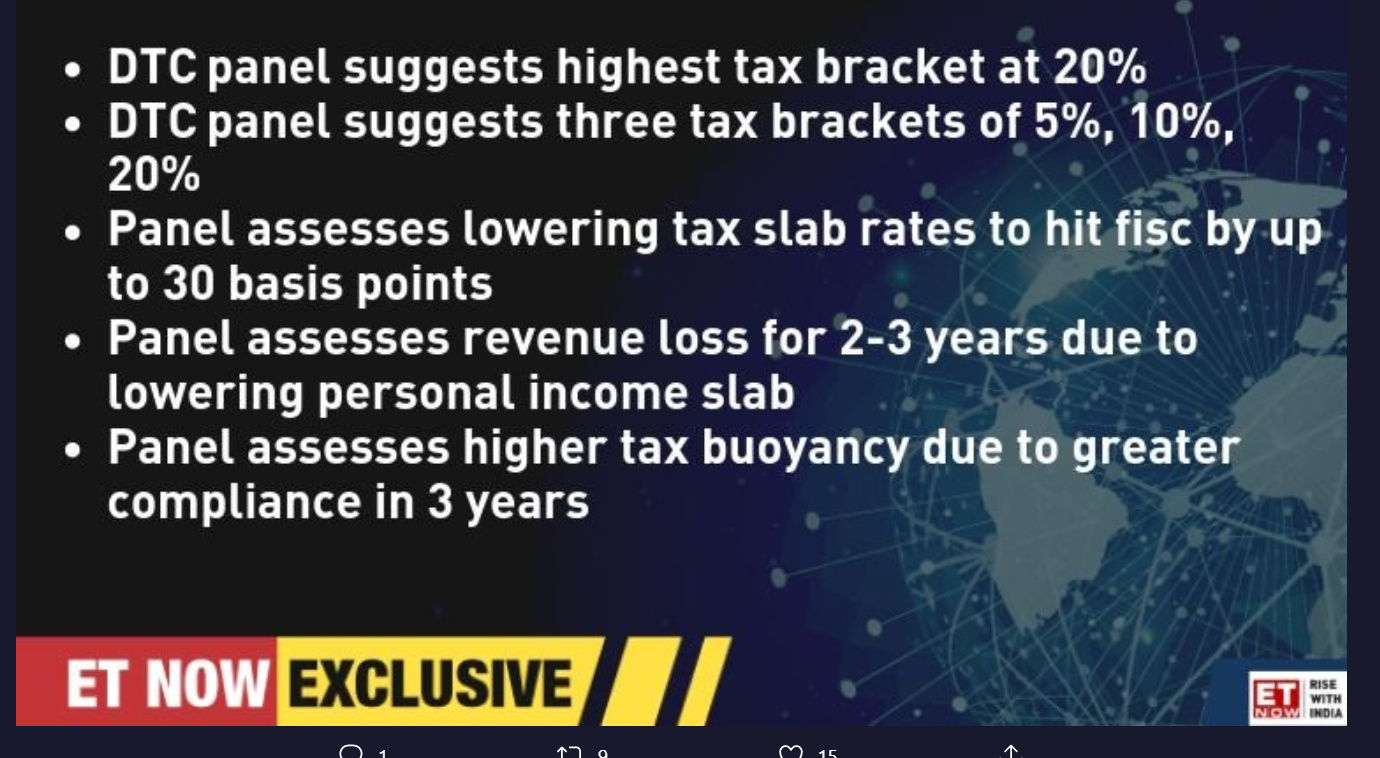

In the initial draft of the Direct Tax Code (2009), there was a proposal to remove all exemptions and reduce the income tax rate for individuals for simplification purposes. Is there an expectation that the newly submitted DTC will have similar plans to phase out exemptions (80 C/D etc)? If so, how bad will it impact the Life Insurance business as tax savings is one reasons for individuals to buy insurance plans?

From ET NOW Twitter page…not sure how authentic it is… But if implemented (removal of all tax exemptions), how does it impact the Life insurance business (& NPS) as they are marketed also as tax saving options.

Huge block deals today…Never seen this many in any scrip…Is standard life just reduced again?

https://www.moneycontrol.com/stocks/marketstats/blockdeals/index.php

Earlier sale was for regulatory requirements… volume is almost similar … approx 1.5% (3 Cr shares) worth 1650+Cr

MSCI included HDFC Life Insurance Company to its Global Standard Index effective from the closing hours of August 27.

Cabinet may ease FDI norms in single-brand retail, insurance today

** In the Budget, the government had made clear its intent to further relax FDI norms in several sectors**

Interesting, how do you compare business of HDFC AMC to HDFC life over next decade? Thanks

1 Like

What makes entire HDFC group great ? Don’t you think moat of banking operations when private banks allowed would be different now when many AMC and Insurance players are there now.

Would appreciate anyone elaborating on what is making entire HDFC group unique

If I have to sum up one thing - don’t do anything stupid when the times are good so that circle of making money - invest - then make more money … in short positive feedback loop of ‘compounding’ is not disturbed.

This has been proved more than adequately in their banking/housing fin ops but folks think this would be replicated in Life Insurance and AMC as well. Nothing to suggest otherwise so far.

I am ex-employee of this company. I must say that company’s work culture is really good. If you look at the way the life industry shaping its really very slow growth industry.The targets set by the company 5-7 years back they are able to achieve now.

I really feel market participant in India buy in bulk and make some hot story on TV sets and at different stages to make others believe in the story.

I was not surprised at all standard life the co-promoter selling its stake in company. In-fact employees of the company were shocked to see the company got such a high valuation by market.

Having said 100 PE stock is real crazy valuation at this stage. you can compare Indian Insurance with developed companies stock valuation like AIA, Aviva or prudential.

I remember in 2008 crisis when I used to serve retail clients at branch office, every one was surrendering the policy like there was no tomorrow, other big threat is Mis-selling which no one talks about. Insurance cos keep changing the name and tweak features and keep selling the product and Do remember its a Push Product and not a Pull product.

Disclosure - Invested in HDFC Bank and not in HDFC Life

15 Likes

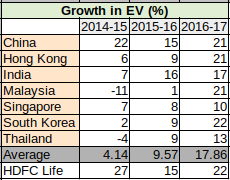

Why do you say life insurance is very slow growth industry? On the contrary HDFC Life is growing it’s Embedded value at an average growth rate of 21% for 2014-2019 period. This looks like exceptional growth to me -

embedded value (ev)

fy13 = 5,872

fy14 = 6,992 gwt=19%

fy15 = 8,890 gwt=27%

fy16 = 10,230 gwt=15%

fy17 = 12,470 gwt=22%

fy18 = 15,216 gwt=22%

fy19 = 18,301 gwt=20%

avg gwt= 21%

3 Likes

You can check most of the Asian insurance companies have EV growth in excess of 20%, but have reasonable valuation of 20-25 PE . You can check milliman report on EV of Asian companies. EV is calculated basis Actuarial Assumptions (assumptions are very dynamic and dangerous word, lot of variable are put to get the output). One of the input variable is GDP and savings rate which is on declining trend but one talking about this.But to me this company will do fair calculation on EV. If look at the US large insurance companies trade at 12-20 PE.

Increase in Health insurance allocation by government, what has Life insurance companies got to do with it, but these stock moves on this news. please do check the Unit link performance of this company and compare that with the expectation that they convey to customers while selling the policies.

To me growth in life insurance stocks can come only if Regular premium policies are being sold and to growth comes from Non metro cities. If you look at this trend of Regular premium policies growth you will get the answer. Single premiums are low margin business for the companies. Also do check the trend of increase in number of branches that have been opened by the insurance companies.

https://www.irdai.gov.in

other growth segment which is pensions and Annuities is something where regulators are working out ways to improve market for longtime now.

6 Likes

Ulips and participating policies will face this cyclical fate. Pure protection will not and probably pension and annuities will also be spared. I agree to your risk in assumptions when calculating EV etc. That’s why management quality and promoter ethics is paramount in this business. Regarding valuations, market knows the real long runway in insurance companies and their capability to grow at above many other industry growth rates for a very very long time. India is growth story and growth sells real costly. Moment the whatever calculation growth is tapered, these or rather any company will not be spared.

As an ex employee you have not spoken of the gigantic shift in focus on pure protection for this industry and on particularly HDFC life’s ahead of time focus on pension NPS annuity and on a reinsurance subsidiary? How do you see these in terms of sustainable and profitable growth? What is the long term government policy stand that you mention for pension etc.? Also how do you compare HDFC AMC business with Life insurance considering you mention the 2008 scenario…

Thanks for your views!

How to value a company depends on the investors, I was just trying to put my thoughts. Please do try and find out why Insurance Companies delayed their respective IPO’s other then regulatory approvals you will get more answer there. Amitabh chaudhary was big loss for the company, he is a real dynamic leader, I had pleasure to speak with him twice.

The company is in no way has been leader in bringing the new products. Protection plans are old Plans which they have added certain benefits to it. If u ask me who has been got the breakthrough product in India’s Insurance market It was Birla Sunlife in 2004 which bought ULIP in insurance market. you can visit society of actuaries website to gain more knowledge on insurance industry.

In technology ICICI pru is way ahead as a leader, even in protection plan. Recently LIC has reduced 30% drop in Protection plan. protection plan major factor is mortality charges which is again based on LIC Tables.

You can google out the challenges faced by insurance companies and sustainable growth will be there but major income drawn by insurance cos are in terms of mortality charges collected and Investment income, surplus are not distributed in protection plans but in participating policies its being distributed between policy holders and share holder.

AMC business is very different from Insurance company. Margins are higher for Insurance companies as compared to AMC. Insurance companies are sticky business, but there are other risk attached to it. one has to ask to himself if the company wants to sell the business will the buyer buy at this rate or higher than this. Investors have been talking of SIP closures due to Job loses and slowdown, its evident that insurance policies which gets surrendered and Renewals being stopped, during the slowdown and panic in the markets. MF are easy to sell as compared to life insurance policies. Protection plan don’t have any benefits attached to it, impact to it will be the most.

So those who are saying Insurance companies will not be impacted due to severe slowdown let me tell you there were 20% and more layoffs during the 2008 crisis. I am not sure if its there in the records nor management would accept it. Majority of the workforce in insurance cos belong to sales vertical, so if sales is not happening what can company do.

As there is a saying Trend is my friend, enjoy the Trend.

3 Likes

No offenses to anyone. My two cents - I have worked in a number of IT companies in my over 20 years of career and thought I had a good inside view of what was not going right for the company and the industry in general. However, most companies with good management have continued to find new ways of maintaining growth even if the industry matured and growth has slowed down relatively.

Disc : Invested in HDFC Life

8 Likes

Could not agree with you more. I have been in the IT field as well for nearly 2.5 decades and I can tell you, I had a head swell that I understood this industry well enough and stayed clear of big compounders like TCS, Infy thinking that they will peter out but it proved to be a total wrong judgement, in the end. It is tough for an average employee to figure out the overall industry trend (with no offence to anyone and yes, there will be exceptions and the odd champion employee/investor will emerge from the woods)

PS - small position in HDFC life

6 Likes

Conclusion from above data table (Source attribution - Millman Research report)

1.Growth of EV by Indian life insurance companies in better Asian average.

2.Growth of EV by HDFC life is better than best in Asia.

3.Chinese companies have better EV growth than India and best in Asia.

I have looked at two of the largest life insurance companies of China namely China life insurance company and Ping An Insurance.

Both these companies should command higher valuation but for controversies of impropriety.

For China life insurance, read - 3.02 billion yuan in illegal activities

For Ping An read - Ownership

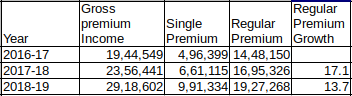

Regular premium can be derived from Jan-Mar quarter results by subtracting Single premium from Gross Premium Income.

Are you indicating that the growth is already slowing down?

There is no denying that valuation are stretched but market is looking at very high quality and assuming a very long-term growth story here.

4 Likes

In fact it’s absolutely reverse

HDFC life has gross margin of 2 to3 %

HDFC AMC has gross margin of 68%

Agree protection are old plan but adding morbidity and longevity is innovation

Valuing life insurance on PE basis is not a good idea do it by Appraisal method. Which covers EV and expected earnings from new policies in future

If you add scalability and longevity in valuation

After few years result will be obvious

Thanks

Ashit

2 Likes

Saw this news article from ICICI Prudential Life Insurance forum…does anyone know more about this?

If this is true, is it applicable only for banks as promoters? In case of HDFC LIFE, the promoter HDFC is a HFC and hence lending activities are not as widespread as a bank.