Interesting development

From October 2019, the campaign will look at busting myths related to the sector and importance of buying insurance.

Like MF industry Life insurance companies will unite for this advertising campaign

Thanks

Ashit

Interesting development

From October 2019, the campaign will look at busting myths related to the sector and importance of buying insurance.

Like MF industry Life insurance companies will unite for this advertising campaign

Thanks

Ashit

IRDAI further underlines the reason for imposing these conditions by stating: " Considering that life insurance is essentially a long term financial instrument, a fair and transparent sales process with meaningful, timely and relevant disclosures, is very important to ensure good customer outcomes and protect the interests of insuring public."

Insurance companies must comply with the above by December 1, 2019.

I think it will be good step for life insurance industry in long run as people will understand difference between savings and protection products ,and ultimately protection products penetration will increase

Thanks

Ashit

(source Credit - MoneyControl )

Hi,

Can any one share growth numbers for last 5 years for all Life Insurance companies?

I have couple of concern about HDFC Life.

Can somebody please answer to this question?

Discloser :- Invested with 6% of my portfolio holding.

Hi @ashit , if we consider the valuation on the basis of EV then HDFC life is 20-22% grower but if we consider valuation on basis of AV then it will come 24-25% grower. Is it sustainable ? What is your take?

PS : Edited

Can any one share any pointer so can understand difference between funded and non funded exposures. Please

@rupeshtatiya @ashit I have a question about calculating the multiple which decides the apprisal value. Is it calculated by subtracting the embedded value from the valuation of the company and then dividing it by the VNB? Is this multiple indicates the number of future years the insurer has to underwrite at least the same amount of business as last year and with the same level of profitability to justify the valuation?

@debesht

I think valuation on basis of AV is more appropriate as it captures value of in force business and its new business also

same question was asked in concall and management replied :

based on whatever we understand It’s the growth, the quality of the growth, the economic value generated as well as the accounting surplus emerging over a period of time. So all of these elements would form a part of the consideration set, in my view.

So that’s actually just anomaly in the life insurance business, where the accounting surplus gets affected or distorted because of growth and upfronting of expenses. So that’s the reason why economic growth is something which is given more prominence, along with the growth and the quality of growth. So new business margins and the embedded value operating profit is something which is given significant weightage, and we do that as management teams as well. But we also have a very keen eye on how the accounting surplus is emerging. Vibha mentioned earlier in the call in terms of how operating variances are panning out. That is equally important as well because ultimately, the economic value has to translate into cash or near cash, which is basically accounting profit.

I am more interested in your second question which you deleted

Is it SUSTAINABLE ? … same question I am asking myself

for that understanding of business and unit economy is important for me

probably oversimplified my way of thinking

backbook( written earlier) unwinding in to the IGAAP profit

1 backbook is dependent on VIF buildup

2 pace of VIF buildup is heavily dependent on the new business margins.

3 Unwinding also depend on few assumptions like

( a) persistency assumption (b), mortality assumption (d) expense assumption. (e) interest rate

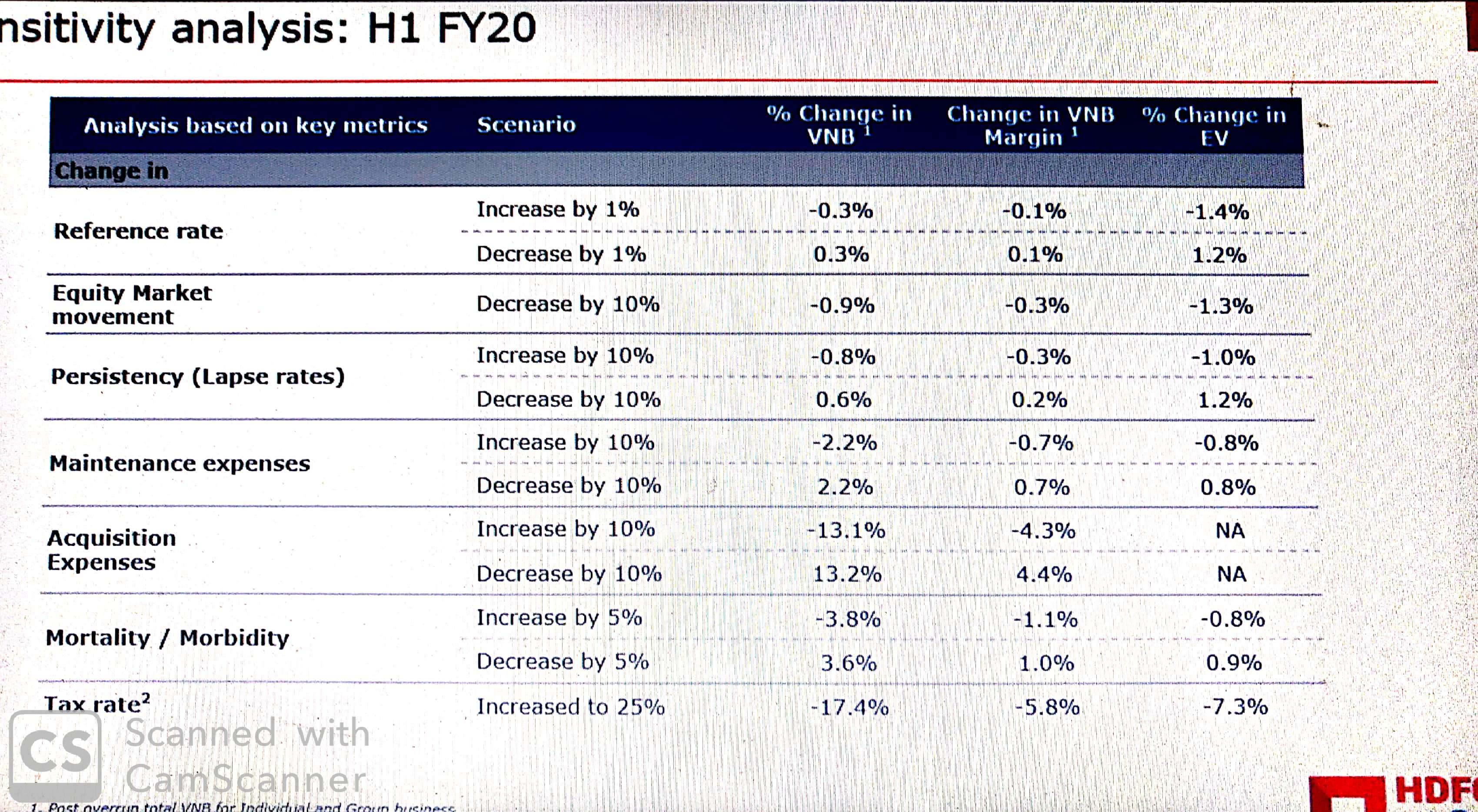

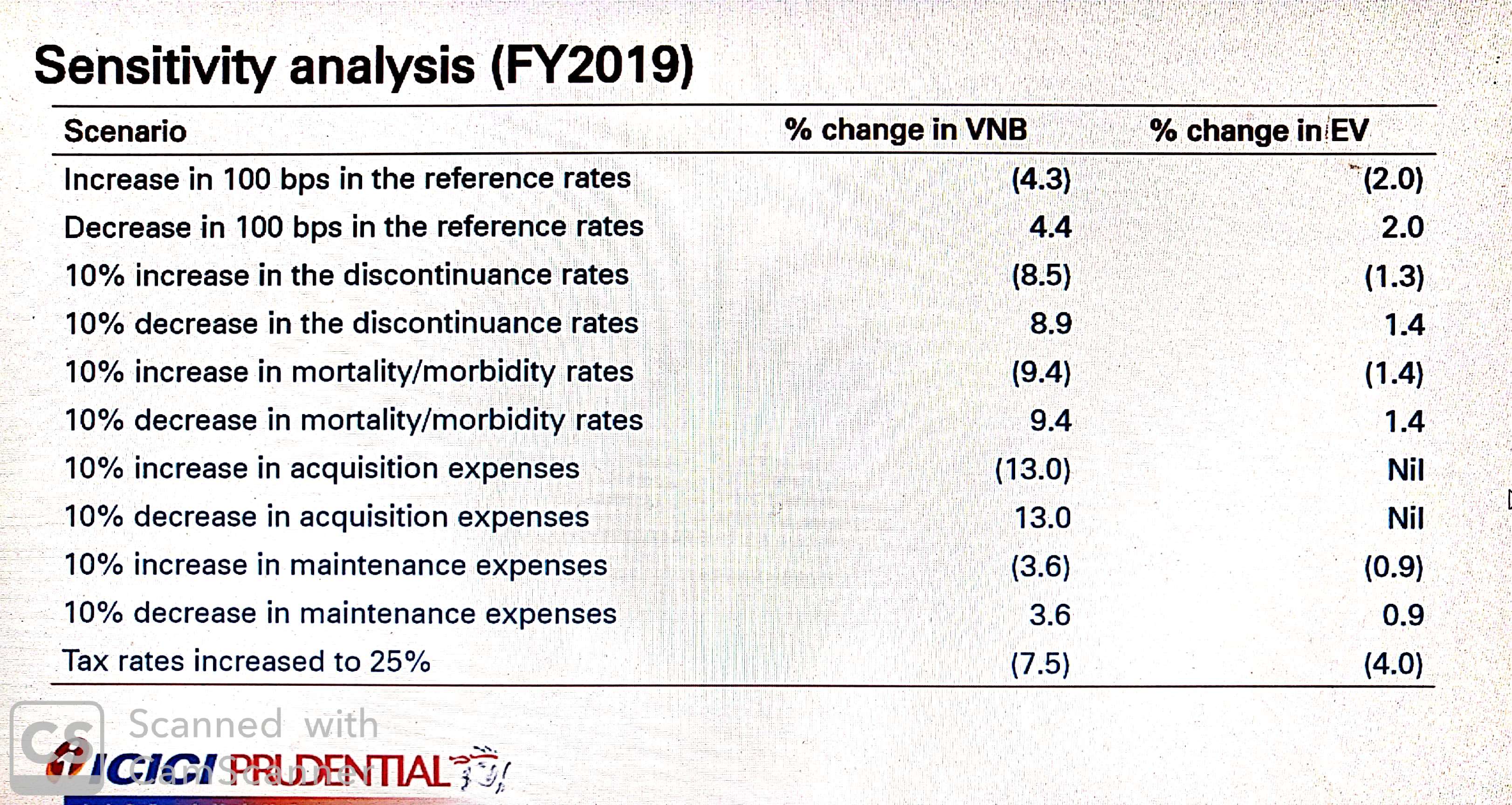

Real uniqueness of hdfc life is there ALM management which is visible in sensitivity analysis I try to compere with sbi life and icici pru life below

one can see they are less sensitivity to reference rate (there perfect Cash flow matched is been validated by external expert )

thanks

ashit

Thanks for your response . The low sensitivity due to to prudent ALM management somewhat describes the MOAT of the HDFC Life company .

One more observation, it has been mentioned in HDFC Life (applicable for all the insurance companies ) Sensitivity analysis page that

“The tax rate is assumed to increase from 14.56% to 25% and hence all the currently taxed profits in policyholder/shareholder segments are taxed at a higher rate. It does not allow for the benefit of policyholder surplus being tax-exempt as was envisaged in the DTC Bill.”

If it is implemented then it will enforce additional compliance which will result uncertainty as far as the taxation of insurance companies and policyholders are concerned. I searched in net but could not found any reference for this regulatory changes in DTC Bill post 2010 . Is this point still present in current proposed DTC Bill ?

Good initiative from Life insurance council

Hop it will increase penetration of primary protection products

Thanks

Good video on how hdfc Life innovate and progress

Second video of Vibha padalkar and LIC CEO on insurance penetrations compare to China

Thanks

Will this lead to lot of availability of insurance stocks or would they sale to global strategic investors?

This shouldn’t be an issue for HDFC LIFE as the promoter is HDFC (NBFC_HFC) and not HDFC BANK. HDFC holds 51.47% only and the rest of the promoter shareholding is by STANDARD LIFE.

30% for Banks and 50% for NBFCs - from same article -

RBI informed the bankers in a meeting last week that it will soon introduce rules to cap their holdings in an insurance company to 30%, the people said, requesting anonymity as the matter is confidential. The holding limit will be 50% for non-banking financial companies such as Housing Development Finance Corp. that have insurance units, they said. Banks have been told to await RBI’s official communication on the new rules.

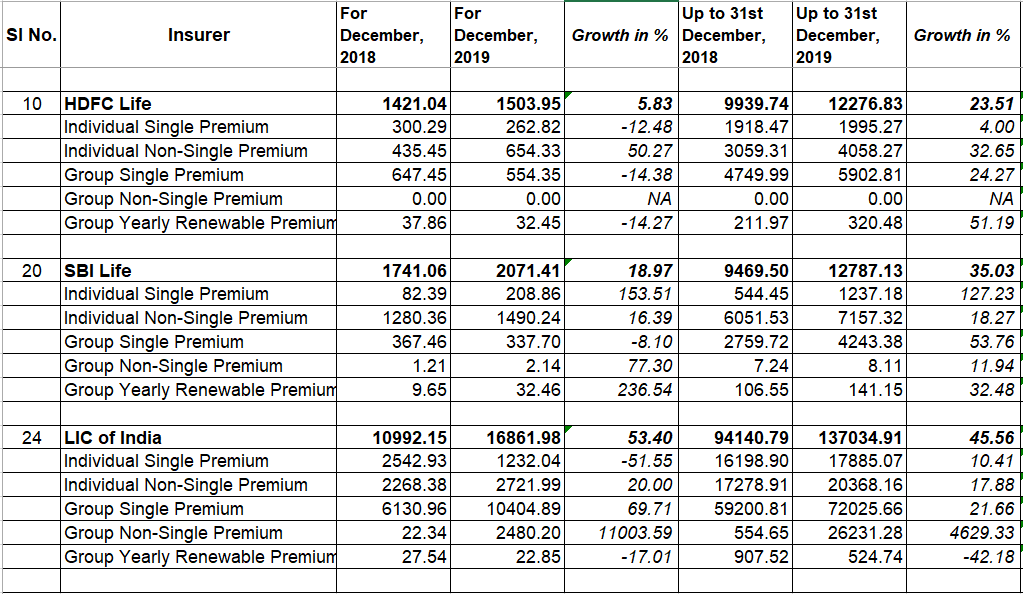

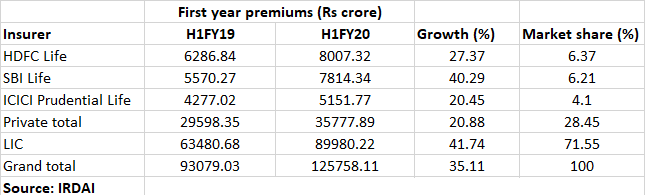

For the month of Dec 2019, the total first year premium collection for HDFC LIFE, SBI LIFE & LIC are shown below. Both SBI & LIC are very aggressive in new premium collection since past few quarters.

I have seen HDFC LIFE CEO mentioning something about growing profitably recently. Can anyone explain the numbers below w.r.t growth vs. profitability? Are SBI & LIC growing at this rate by giving up profitability to an extent?

Comparing individual non-single premium (which is a recurring income for the company) the growth is highest for HDFC followed by LIC and SBI.

comparing group non-single premium (which is a recurring income for the company) the growth is highest for LIC followed by SBI.

comparing group yearly renewal premium (which is a recurring income for the company) the growth is highest for SBI.

this shows that the future profitablity of SBI is poised better for SBI as compared to any other listed player.

disc: invested in SBI life.